UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K/A

(Amendment No. 1)

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of August 2023

Commission File Number: 001-38766

MMTEC, INC.

(Translation of registrant’s name into English)

c/o MM Future Technology Limited

Room 2302, 23rd Floor

FWD Financial Center

308 Des Voeux Road Central

Sheung Wan, Hong Kong

Tel: + 852 36908356

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file

annual reports under cover of Form 20-F or Form 40-F. Form 20-F ☒

Form 40-F ☐

Indicate by check mark whether the registrant by furnishing the information

contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the

Securities Exchange Act of 1934.

Yes ☐ No ☒

If “Yes” is marked, indicate below the file number assigned

to the registrant in connection with Rule 12g3-2(b): 82-________.

Completion of Acquisition or Disposition of Assets.

On June 7, 2023, MMTec, Inc.,

a British Virgin Islands company (“MMTec” or the “Company”), completed its previously announced acquisition of

Alpha Mind Technology Limited, a British Virgin Islands company (“Alpha Mind”), pursuant to an Equity Acquisition Agreement

dated May 16, 2023 between MMtec, Alfa Crest Investment Limited, a British Virgin Islands company (“Alfa Crest”), CapitoLabs

Limited, a British Virgin Islands company (“CapitoLabs”, and together with Alfa Crest, the “Sellers”) and Alpha

Mind.

On

June 8, 2023, MMtec filed a Current Report on Form 6-K (the “Prior Report”) with the Securities and Exchange Commission to

report the completion of the acquisition and other related matters. MMTec is filing this amendment to the Prior Report to provide the

financial statements of Alpha Mind as of and for the years ended December 31, 2022 and 2021, the accompanying notes thereto

and the related Independent Auditor’s Report, which are filed as Exhibit 99.1 and incorporated herein by reference, and pro forma financial information as of and for the year ended

December 31, 2022, which is filed as Exhibit 99.2.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934,

the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| |

MMTEC, INC.

|

| |

|

|

| |

By: |

/s/ Min Kong |

| |

|

Name: |

Min Kong |

| |

|

Title: |

Chief Financial Officer |

| |

|

|

| Date: August 29, 2023 |

|

|

2

Exhibit 23.1

Consent of Independent Registered Public

Accounting Firm

We hereby consent to the incorporation of our

report dated August 29, 2023 in the Report of Foreign Private Issuer on Form 6-K, under the Securities Exchange Act of 1934, with respect

to the consolidated balance sheets of Alpha Mind Technology Limited, its subsidiaries, and variable interest entities (collectively the

“Company”) as of December 31, 2022 and 2021, and the related consolidated statements of income (loss) and comprehensive income

(loss), shareholders’ equity, and cash flows for each of the years in the two-year period ended December 31, 2022, and the related

notes included herein.

| |

|

| San Mateo, California |

WWC, P.C. |

| August 29, 2023 |

Certified Public Accountants |

|

PCAOB ID: 1171 |

Exhibit 99.1

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING

FIRM

To the Board of Directors and Stockholders of

Alpha Mind Technology Limited

Opinion on the Financial Statements

We have audited the accompanying consolidated

balance sheets of Alpha Mind Technology Limited, subsidiaries, and variable interest entities (collectively the “Company”)

as of December 31, 2022 and 2021, and the related consolidated statements of income (loss) and comprehensive income (loss), changes in

shareholders’ equity, and cash flows in each of the years for the two-year period ended December 31, 2022, and the related notes

(collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects,

the financial position of the Company as of December 31, 2022 and 2021, and the results of its operations and its cash flows for each

of the years in the two-year period ended December 31, 2022, in conformity with accounting principles generally accepted in the United

States of America.

Basis for Opinion

These financial statements are the responsibility

of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our

audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are

required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and

regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the

standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial

statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged

to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding

of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s

internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess

the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond

to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements.

Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating

the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ WWC, P.C.

WWC, P.C.

Certified Public Accountants

PCAOB ID No.1171

We have served as the Company’s auditor since 2022.

San Mateo, California

August 29, 2023

ALPHA MIND TECHNOLOGY LIMITED, SUBSIDIARIES,

AND VARIABLE INTEREST ENTITIES

CONSOLIDATED BALANCE SHEETS

(In U.S. dollars, except for share and

per share data, or otherwise noted)

| | |

As of | |

| | |

December 31,

2022 | | |

December 31,

2021 | |

| ASSETS | |

| | |

| |

| CURRENT ASSETS: | |

| | |

| |

| Cash and cash equivalents | |

$ | 341,743 | | |

$ | 512,028 | |

| Accounts receivable, net | |

| 2,892,960 | | |

| 3,601,345 | |

| Prepayments | |

| 1,412,266 | | |

| 2,449,349 | |

| Other receivables, net | |

| 31,227 | | |

| 97,112 | |

| Due from related parties | |

| 20,784 | | |

| 34,361 | |

| Short-term investment | |

| 273,182 | | |

| 393,651 | |

| Other current assets | |

| 100,558 | | |

| 171,019 | |

| Total Current Assets | |

| 5,072,720 | | |

| 7,258,865 | |

| | |

| | | |

| | |

| NON-CURRENT ASSETS: | |

| | | |

| | |

| Restricted Cash- non-current | |

| 717,916 | | |

| 784,228 | |

| Property and equipment, net | |

| 68,541 | | |

| 48,086 | |

| Deferred tax assets | |

| 25,360 | | |

| 4,280 | |

| Total Non-current Assets | |

| 811,817 | | |

| 836,594 | |

| | |

| | | |

| | |

| Total Assets | |

$ | 5,884,537 | | |

$ | 8,095,459 | |

| | |

| | | |

| | |

| LIABILITIES AND SHAREHOLDERS’ (DEFICIT) EQUITY | |

| | | |

| | |

| CURRENT LIABILITIES: | |

| | | |

| | |

| Accounts payable | |

$ | 2,496,587 | | |

$ | 3,504,865 | |

| Salary payable | |

| 65,709 | | |

| 42,082 | |

| Other payables | |

| 780,247 | | |

| 1,132,451 | |

| Due to related parties | |

| 16,723 | | |

| 74,739 | |

| Taxes payable | |

| 154,585 | | |

| 203,114 | |

| Advance from customer | |

| 5,306 | | |

| 13,617 | |

| Total Current Liabilities | |

| 3,519,157 | | |

| 4,970,868 | |

| | |

| | | |

| | |

| NON-CURRENT LIABILITIES: | |

| | | |

| | |

| Long-term liabilities | |

| — | | |

| 439,167 | |

| Total Non-current Liabilities | |

| — | | |

| 439,167 | |

| Total Liabilities | |

| 3,519,157 | | |

| 5,410,035 | |

| | |

| | | |

| | |

| SHAREHOLDERS’ EQUITY: | |

| | | |

| | |

| Common shares (par value $1.00 per share; 50,000 shares authorized as of April 17, 2023) | |

| 50,000 | | |

| 50,000 | |

| Subscription receivable | |

| (50,000 | ) | |

| (50,000 | ) |

| Additional paid-in capital | |

| 8,649,321 | | |

| 8,205,976 | |

| Accumulated deficit | |

| (5,636,318 | ) | |

| (5,110,749 | ) |

| Accumulated other comprehensive loss | |

| (647,623 | ) | |

| (409,803 | ) |

| | |

| | | |

| | |

| Total Shareholders’ Equity | |

| 2,365,380 | | |

| 2,685,424 | |

| | |

| | | |

| | |

| Total Liabilities and Shareholders’ Equity | |

$ | 5,884,537 | | |

$ | 8,095,459 | |

The

accompanying notes are an integral part of these consolidated financial statements.

ALPHA MIND TECHNOLOGY LIMITED, SUBSIDIARIES,

AND VARIABLE INTEREST ENTITIES

CONSOLIDATED STATEMENTS OF INCOME (LOSS) AND

COMPREHENSIVE INCOME (LOSS)

(In U.S. dollars, except for share and per share

data, or otherwise noted)

| | |

For the Year Ended | |

| | |

December 31,

2022 | | |

December 31,

2021 | |

| | |

| | |

| |

| REVENUE | |

$ | 47,443,458 | | |

$ | 44,948,234 | |

| COST OF REVENUE | |

| 43,614,455 | | |

| 41,946,093 | |

| GROSS PROFIT | |

| 3,829,003 | | |

| 3,002,141 | |

| | |

| | | |

| | |

| OPERATING EXPENSES: | |

| | | |

| | |

| Selling and marketing | |

| 3,380,556 | | |

| 2,440,581 | |

| General and administrative | |

| | | |

| | |

| Payroll and related benefits | |

| 641,389 | | |

| 803,833 | |

| Other general and administrative | |

| 1,152,245 | | |

| 601,128 | |

| Total Operating Expenses | |

| 5,174,190 | | |

| 3,845,542 | |

| | |

| | | |

| | |

| LOSS FROM OPERATIONS | |

| (1,345,187 | ) | |

| (843,401 | ) |

| | |

| | | |

| | |

| OTHER INCOME (EXPENSE): | |

| | | |

| | |

| Interest income | |

| 18,559 | | |

| 40,275 | |

| Interest expense | |

| (13,266 | ) | |

| (70,196 | ) |

| Other income, net | |

| 818,372 | | |

| 239,305 | |

| Total Other income (expense) | |

| 823,665 | | |

| 209,384 | |

| | |

| | | |

| | |

| LOSS BEFORE INCOME TAXES | |

| (521,522 | ) | |

| (634,017 | ) |

| | |

| | | |

| | |

| INCOME TAXES | |

| (4,047 | ) | |

| (16,393 | ) |

| | |

| | | |

| | |

| NET LOSS | |

$ | (525,569 | ) | |

$ | (650,410 | ) |

| | |

| | | |

| | |

| OTHER COMPREHENSIVE (LOSS) INCOME | |

| | | |

| | |

| Foreign currency translation adjustments | |

| (237,820 | ) | |

| 68,723 | |

| COMPREHENSIVE LOSS | |

$ | (763,389 | ) | |

$ | (581,687 | ) |

The

accompanying notes are an integral part of these consolidated financial statements.

ALPHA MIND TECHNOLOGY LIMITED, SUBSIDIARIES,

AND VARIABLE INTEREST ENTITIES

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(In U.S. dollars, except for share and per share

data, or otherwise noted)

| | |

Common Shares | | |

| | |

Additional | | |

| | |

Accumulated

Other | | |

Total | |

| | |

Number of | | |

| | |

Subscription | | |

Paid-in | | |

Accumulated | | |

Comprehensive | | |

Shareholders’ | |

| | |

Shares | | |

Amount | | |

Receivable | | |

Capital | | |

Deficit | | |

Loss | | |

Equity | |

| Balance, January 1, 2021 | |

| 50,000 | | |

$ | 50,000 | | |

$ | (50,000 | ) | |

$ | 8,205,976 | | |

$ | (4,460,339 | ) | |

$ | (478,526 | ) | |

$ | 3,267,111 | |

| Net loss for the year ended December 31, 2021 | |

| - | | |

| - | | |

| - | | |

| - | | |

| (650,410 | ) | |

| - | | |

| (650,410 | ) |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 68,723 | | |

| 68,723 | |

| Balance, December 31, 2021 | |

| 50,000 | | |

$ | 50,000 | | |

$ | (50,000 | ) | |

$ | 8,205,976 | | |

$ | (5,110,749 | ) | |

$ | (409,803 | ) | |

$ | 2,685,424 | |

| Capital contribution from shareholders | |

| - | | |

| - | | |

| - | | |

| 443,345 | | |

| - | | |

| - | | |

| 443,345 | |

| Net loss for the year ended December 31, 2022 | |

| - | | |

| - | | |

| - | | |

| - | | |

| (525,569 | ) | |

| - | | |

| (525,569 | ) |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| | | |

| - | | |

| - | | |

| (237,820 | ) | |

| (237,820 | ) |

| Balance, December 31, 2022 | |

| 50,000 | | |

$ | 50,000 | | |

$ | (50,000 | ) | |

$ | 8,649,321 | | |

$ | (5,636,318 | ) | |

$ | (647,623 | ) | |

$ | 2,365,380 | |

The

accompanying notes are an integral part of these consolidated financial statements.

ALPHA MIND TECHNOLOGY LIMITED, SUBSIDIARIES,

AND VARIABLE INTEREST ENTITIES

CONSOLIDATED STATEMENTS OF CASH FLOW

(In U.S. dollars, except for share and per share

data, or otherwise noted)

| | |

For the Years Ended | |

| | |

December 31, | |

| | |

2022 | | |

2021 | |

| CASH FLOWS FROM OPERATING ACTIVITIES: | |

| | |

| |

| Net loss | |

$ | (525,569 | ) | |

$ | (650,410 | ) |

| Adjustments to reconcile net income to net cash provided by operating activities: | |

| | | |

| | |

| Depreciation expense | |

| 16,305 | | |

| 17,322 | |

| Allowance for bad debts | |

| 81,073 | | |

| 16,488 | |

| Deferred taxes expense | |

| (22,202 | ) | |

| (4,230 | ) |

| Noncash other expense | |

| - | | |

| 4,650 | |

| Changes in operating assets and liabilities: | |

| | | |

| | |

| Accounts receivable | |

| 391,791 | | |

| (1,217,065 | ) |

| Advance to suppliers | |

| 859,406 | | |

| 642,790 | |

| Due from related parties | |

| 13,577 | | |

| (4,850 | ) |

| Prepaid expenses and other current assets | |

| 60,505 | | |

| (458,129 | ) |

| Accounts Payable | |

| (737,165 | ) | |

| 1,669,768 | |

| Salary payable | |

| 28,150 | | |

| 24,463 | |

| Accrued liabilities and other payables | |

| (287,925 | ) | |

| 154,413 | |

| Net cash provided by (used in) operating activities | |

| (122,054 | ) | |

| 195,210 | |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING ACTIVITIES: | |

| | | |

| | |

| Purchase of property and equipment | |

| (41,695 | ) | |

| - | |

| Purchase of short-term investment | |

| 90,274 | | |

| (389,025 | ) |

| Net cash provided by (used in) investing activities | |

| 48,579 | | |

| (389,025 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES: | |

| | | |

| | |

| Cash borrowed from related parties | |

| - | | |

| 434,008 | |

| Repayment to related parties | |

| (58,016 | ) | |

| (11,791 | ) |

| Net cash provided by (used in) financing activities | |

| (58,016 | ) | |

| 422,217 | |

| | |

| | | |

| | |

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS AND RESTRICTED CASH | |

| (131,491 | ) | |

| 228,402 | |

| | |

| | | |

| | |

| Effect of exchange rate changes on cash | |

| (105,106 | ) | |

| 23,502 | |

| | |

| | | |

| | |

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT BEGINNING OF YEAR | |

| 1,296,256 | | |

| 1,044,352 | |

| | |

| | | |

| | |

| CASH AND CASH EQUIVALENTS AND RESTRICTED CASH AT END OF YEAR | |

$ | 1,059,659 | | |

$ | 1,296,256 | |

| | |

| | | |

| | |

| RECONCILIATION OF CASH, CASH EQUIVALENTS AND RESTRICTED CASH | |

| | | |

| | |

| Cash and cash equivalents at beginning of year | |

$ | 512,028 | | |

$ | 278,057 | |

| Restricted cash at beginning of year | |

| 784,228 | | |

| 766,295 | |

| Total cash, cash equivalents and restricted cash at beginning of year | |

$ | 1,296,256 | | |

$ | 1,044,352 | |

| | |

| | | |

| | |

| Cash and cash equivalents at end of year | |

$ | 341,743 | | |

$ | 512,028 | |

| Restricted cash at end of year | |

| 717,916 | | |

| 784,228 | |

| Total cash, cash equivalents and restricted cash at end of year | |

$ | 1,059,659 | | |

$ | 1,296,256 | |

| | |

| | | |

| | |

| SUPPLEMENTAL CASH FLOW INFORMATION: | |

| | | |

| | |

| Cash paid for income tax | |

$ | (16,986 | ) | |

$ | (22,017 | ) |

| Cash paid for interest | |

$ | (13,266 | ) | |

$ | (70,196 | ) |

The

accompanying notes are an integral part of these consolidated financial statements.

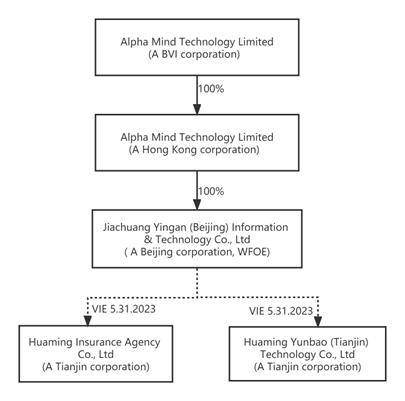

NOTE 1 – ORGANIZATION AND NATURE OF OPERATIONS

Alpha Mind Technology Limited (“Alpha Mind

BVI” or the “Company”) is a holding company incorporated on April 17, 2023 under the laws of British Virgin Islands

(the “BVI”). The Company has no substantive operations other than holding all of the outstanding share capital of Alpha Mind

Technology Limited (“Alpha Mind HK”), which is also a holding company incorporated in Hong Kong on October 19, 2021. The Company

operates as an agency to sell insurance products in the People’s Republic of China (“PRC” or “China”), through

variable interest entities (“VIE”), Huaming Insurance Agency Co., Ltd (“Huaming Insurance”), which was established

on March 7, 2014, and Huaming Yunbao (Tianjin) Technology Co., Ltd (“Huaming Yunbao”), which was established on May 8, 2015.

On April 13, 2022, Alpha Mind HK became the sole

shareholder of Jiachuang Yingan (Beijing) Information & Technology Inc. (“Jiachuang Yingan”, or “WFOE”), a

Beijing company incorporated on August 2, 2019. Jiachuang Yingan entered into a series of contractual arrangements, or VIE agreements

with Huaming Insurance and Huaming Yunbao and the equity holders of Huaming Insurance and Huaming Yunbao, through which the Company obtained

control and became the primary beneficiary of Huaming Insurance and Huaming Yunbao. As a result, Huaming Insurance and Huaming Yunbao

became the Company’s VIE.

The structure of the Company as follows:

Contractual Arrangements

The Company, through the WFOE, has the following

contractual arrangements with the VIE and its shareholders that enable the Company to (1) to direct the activities that most significantly

affect the economic performance of the VIE, and (2) receive the economic benefits of the VIE that could be significant to the VIE.

Accordingly, the WFOE was considered the primary beneficiary of the VIE and had consolidated the VIE’s financial results of operations,

assets and liabilities in the Company’s consolidated financial statements.

The significant terms of the Contractual Arrangements

are as follows:

Exclusive Business Cooperation Agreement

Pursuant to the exclusive business cooperation

agreement between Jiachuang Yingan WFOE and Huaming Insurance and Huaming Yunbao, Jiachuang Yingan WFOE has the exclusive right to provide

Huaming Insurance and Huaming Yunbao with technical support services, consulting services and other services requested by Huaming Insurance

and Huaming Yunbao from time to time to the extent permitted under PRC law. In exchange, Jiachuang Yingan WFOE is entitled to a service

fee that equals to all of the consolidated net income of each of Huaming Insurance and Huaming Yunbao. The service fee may be adjusted

by Jiachuang Yingan WFOE based on the actual scope of services rendered by Jiachuang Yingan WFOE and the operational needs and expanding

demands of Huaming Insurance and Huaming Yunbao. Pursuant to the exclusive business cooperation agreement, the service fees may be adjusted

based on the actual scope of services rendered by Jiachuang Yingan WFOE and the operational needs of Huaming Insurance and Huaming Yunbao.

The exclusive business cooperation agreement remains

in effect unless terminated in accordance with the following provision of the agreement or terminated in writing by Jiachuang Yingan WFOE.

During the term of the exclusive business cooperation

agreement, Jiachuang Yingan WFOE and Huaming Insurance and Huaming Yunbao shall renew the operation term prior to the expiration thereof

so as to enable the exclusive business cooperation agreement to remain effective. The exclusive business cooperation agreement shall be

terminated upon the expiration of the operation term of either Jiachuang Yingan WFOE or Huaming Insurance and Huaming Yunbao if the application

for renewal of the operation term is not approved by relevant government authorities. If an application for renewal of the operation term

is not approved, according to the PRC Company Law, the expiration of the operation term may lead to the dissolution and cancellation of

such PRC company.

Exclusive Option Agreement

Pursuant to the exclusive option agreement among

Jiachuang Yingan WFOE, Huaming Insurance and Huaming Yunbao and the shareholders who collectively owned all of Huaming Insurance and Huaming

Yunbao, such shareholders jointly and severally granted Jiachuang Yingan WFOE an option to purchase their equity interests in Huaming

Insurance and Huaming Yunbao. The purchase price upon exercise of the option will be the lowest price then permitted under applicable

PRC laws. Jiachuang Yingan WFOE or its designated person may exercise such option at any time to purchase all or part of the equity interests

in Huaming Insurance and Huaming Yunbao until it has acquired all equity interests of Huaming Insurance and Huaming Yunbao, which is irrevocable

during the term of the agreements.

The exclusive option agreement remains in effect

until all equity interest held by shareholders in Huaming Insurance and Huaming Yunbao have been transferred or assigned to Jiachuang

Yingan WFOE and/or any other person designated by the Jiachuang Yingan WFOE in accordance with such agreement.

Equity Interest Pledge Agreements

Pursuant to the equity interest pledge agreements,

among Jiachuang Yingan WFOE, Huaming Insurance and Huaming Yunbao, and the shareholders who collectively owned all of Huaming Insurance

and Huaming Yunbao, such shareholders pledged all of the equity interests in Huaming Insurance and Huaming Yunbao to Jiachuang Yingan

WFOE as collateral to secure the obligations of Huaming Insurance and Huaming Yunbao under the exclusive business cooperation agreement,

shareholders’ powers of attorney and exclusive option agreements. These shareholders are prohibited from transferring the pledged

equity interests without the prior consent of Jiachuang Yingan WFOE unless transferring the equity interests to Jiachuang Yingan WFOE

or its designated person in accordance to the exclusive option agreements.

The equity interest pledge agreements will remain

in effect until all of the obligations to Jiachuang Yingan WFOE have been fulfilled completely by Huaming Insurance and Huaming Yunbao.

Shareholders’ Powers of Attorney (“POAs”)

Pursuant to the shareholders’ POAs, the

shareholders of Huaming Insurance and Huaming Yunbao have given Jiachuang Yingan WFOE an irrevocable proxy to act on their behalf on all

matters pertaining to Huaming Insurance and Huaming Yunbao and to exercise all of their rights as shareholders of Huaming Insurance and

Huaming Yunbao, including the (i) right to attend shareholders meeting; (ii) to exercise voting rights and all of the other rights including

but not limited to the sale or transfer or pledge or disposition of their shares held in part or in whole; and (iii) designate and appoint

on behalf of the shareholders the legal representative, the directors, supervisors, the chief executive officer and other senior management

members of Huaming Insurance and Huaming Yunbao, and to sign transfer documents and any other documents in relation to the fulfillment

of the obligations under the exclusive option agreements and the equity interest pledge agreements. The shareholders’ POAs remain

in effect while the shareholders of Huaming Insurance and Huaming Yunbao hold the equity interests in Huaming Insurance and Huaming Yunbao.

Spousal Consent Letters

Pursuant to the spousal consent letters, the spouses

of the shareholders of Huaming Insurance and Huaming Yunbao commit that they have no right to make any assertions in connection with the

equity interests of Huaming Insurance and Huaming Yunbao, which are held by the shareholders. In the event that the spouses obtain any

equity interests of Huaming Insurance and Huaming Yunbao, which are held by the shareholders, for any reasons, the spouses of the shareholders

shall be bound by the exclusive option agreement, the equity interest pledge agreement, the shareholder POA and the exclusive business

cooperation agreement and comply with the obligations thereunder as a shareholder of Huaming Insurance and Huaming Yunbao. The letters

are irrevocable and shall not be withdrawn without the consent of Jiachuang Yingan WFOE.

Based on the foregoing contractual arrangements,

which grant Jiachuang Yingan WFOE effective control of Huaming Insurance and Huaming Yunbao and enable Jiachuang Yingan WFOE to receive

all of their expected residual returns, the Company accounts for Huaming Insurance and Huaming Yunbao as a VIE. Accordingly, the Company

consolidates the accounts of Huaming Insurance and Huaming Yunbaofor the periods presented herein, in accordance with Regulation S-X-3A-02

promulgated by the Securities Exchange Commission (“SEC”), and Accounting Standards Codification (“ASC”) 810-10,

Consolidation.

NOTE

2 – BASIS OF PRESENTATION

The

accompanying consolidated financial statements and related notes have been prepared in accordance with accounting principles generally

accepted in the United States of America (“U.S. GAAP”) and with the rules and regulations of the U.S. Securities and Exchange

Commission for financial information, and include all normal and recurring adjustments that management of the Company considers necessary

for a fair presentation of its financial position and operation results.

The

consolidated financial statements include the financial statements of the Company and its subsidiaries, which include the wholly-owned

foreign enterprise and VIE over which the Company exercises control and, when applicable, entities for which the Company has a controlling

financial interest or is the primary beneficiary for accounting purposes. Jiachuang Yingan WFOE is

deemed to have a controlling financial interest and be the primary beneficiary for accounting purposes of Huaming Insurance and

Huaming Yunbao because it has both of the following characteristics: (1) the power to direct

activities at Huaming Insurance and Huaming Yunbao that most significantly impact such entity’s

economic performance, and (2) the right to receive benefits from Huaming Insurance and Huaming Yunbao that

could potentially be significant to such entity. All transactions and balances among the Company and its subsidiaries have been eliminated

upon consolidation.

The

Company adopted a fiscal year end of December 31st.

NOTE 3 – SUMMARY OF SIGNIFICANT ACCOUNTING

POLICIES

Use

of Estimates and assumptions

The

preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the

reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements

and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from these estimates.

Significant

estimates and assumptions reflected in the Company’s consolidated financial statements during the years ended December 31, 2022

and 2021 include, but not are not limited to, the allowance for doubtful accounts, the useful life of property and equipment, and assumptions

used in assessing impairment of long-lived assets, revenue recognition, allowance for deferred tax assets and the associated valuation

allowance. Management bases the estimates on historical experience and various other assumptions that are believed to be reasonable, the

results of which form the basis for making judgments about the carrying values of assets and liabilities. Actual results could materially

differ from those estimates.

Foreign

Currency Translation

The

reporting currency of the Company is the U.S. dollar (“USD”). The Company’s functional currency is the RMB, result of

operations and cash flows are translated at average exchange rates during the period, assets and liabilities are translated at the unified

exchange rate at the end of the period, and equity is translated at historical exchange rates. As a result, amounts relating to assets

and liabilities reported on the statements of cash flows may not necessarily agree with the changes in the corresponding balances on the

balance sheets. Translation adjustments resulting from the process of translating the local currency financial statements into U.S. dollars

are included in determining comprehensive income/loss.

All

of the Company’s revenue and expense transactions are transacted in the functional currency. The Company does not enter into any

material transaction in foreign currencies. Transaction gains or losses have not had, and are not expected to have, a material effect

on the results of operations of the Company.

The

consolidated balance sheet amounts, with the exception of equity, at December 31, 2022 and 2021 were translated at RMB 6.9646 to $1.00

and at RMB 6.3757 to $1.00, respectively. Equity accounts were stated at their historical rates. The average translation rates applied

to consolidated statements of income and cash flows for the years ended December 31, 2022 and 2021 were RMB 6.7261 and RMB 6.4515 to $1.00,

respectively.

Cash

and Cash Equivalents

The

Company considers all highly liquid investments purchased with an original maturity of three months or less to be cash equivalents. Cash

and cash equivalents are comprised primarily of bank accounts. At December 31, 2022 and 2021, cash and cash equivalents balances held

in China amounted to $341,743 and $512,028, respectively.

Restricted

Cash

The

Company, as an insurance agency, is required to reserve 10% of its registered capital in cash held in an escrow bank account pursuant

to the China Banking and Insurance Regulatory Commission (“CBIRC”) rules and regulations, in order to protect insurance premium

appropriation by insurance agency which is restricted as to withdrawal for other than current operations. Thus, the Company classified

the balance for guarantee deposit as a non-current asset. As of December 31, 2022 and 2021, the non-current restricted cash amounted to

$717,916 and $784,228, respectively.

Concentrations

of Credit Risk

The

Company has operations carried out in China. Accordingly, the Company’s business, financial condition and results of operations

may be influenced by the political, economic and legal environment in China, and by the general state of China’s economy. The Company’s

operations in China are subject to specific considerations and significant risks not typically associated with companies in North America.

The Company’s results may be adversely affected by changes in governmental policies with respect to laws and regulations, anti-inflationary

measures, currency conversion and remittance abroad, and rates and methods of taxation, among other things.

Accounts

Receivable, Net

Accounts receivable represents

insurance agency service fee or commission receivable on insurance products sold from insurance companies stated at net realizable values.

The Company reviews its accounts receivable on a periodic basis to determine if the bad debt allowance is adequate, and adjust the allowance

when necessary.

In establishing the allowance

for doubtful accounts, management considers historical collection experience, aging of the receivables, the economic environment, industry

trend analysis, and the credit history and financial conditions of the customers. Accounts are written off after exhaustive efforts at

collection.

As

of December 31, 2022 and 2021, allowance for doubtful accounts were $38,360 and $14,054 respectively.

Other Receivables, Net

Other receivables primarily include advances to

employees and other deposits. Management regularly reviews the aging of receivables and changes in payment trends and records allowances

when management believes collection of amounts due are at risk. Accounts considered uncollectable are written off against allowances after

exhaustive efforts at collection are made.

As of December 31, 2022 and 2021, allowance for

doubtful accounts were $611,382 and $610,174, respectively.

Prepayments

Prepayments

are advanced to suppliers for future service rendering. As of December 31, 2022 and 2021, prepayments amounted to $1,412,266 and $2,449,349,

respectively. For any advances to suppliers determined by management that such advances will not be in receipts or refundable, the Company

will recognize an allowance account to reserve such balances. Management reviews its advances to suppliers on a regular basis to determine

if the allowance is adequate, and adjusts the allowance when necessary. Delinquent account balances are written off against allowance

for doubtful accounts after management has determined that the likelihood of collection is not probable. Management continues to evaluate

the reasonableness of the valuation allowance policy and update it if necessary. As of December 31, 2022 and 2021, no allowance for the

doubtful accounts were deemed necessary.

Property and Equipment

Property

and equipment are stated at cost less accumulated depreciation, and depreciated on a straight-line basis over the estimated useful lives

of the assets. Cost represents the purchase price of the asset and other costs incurred to bring the asset into its existing use. The

cost of repairs and maintenance is expensed as incurred; major replacements and improvements are capitalized. When assets are retired

or disposed of, the cost and accumulated depreciation are removed from the accounts, and any resulting gains or losses are included in

income/loss in the year of disposition. Estimated useful lives are as follows:

| |

|

Estimated

Useful Life |

| Automobile |

|

3 - 5 Years |

Impairment of Long-lived Assets

In

accordance with ASC Topic 360, the Company reviews long-lived assets for impairment whenever events or changes in circumstances indicate

that the carrying amount of the assets may not be fully recoverable, or at least annually. The Company recognizes an impairment loss when

the sum of expected undiscounted future cash flows is less than the carrying amount of the asset. The amount of impairment is measured

as the difference between the asset’s estimated fair value and its book value. The Company did not record any impairment charge

for the years ended December 31, 2022 and 2021.

Value

Added Tax

Pursuant

to the PRC tax legislation, general taxpayers normally applies value-added-tax (VAT) of 6% in the modern service industries on a nationwide

basis. The Company is subject to VAT of 6% for providing insurance agency service as general taxpayer, while the branch office in Liaoning

Yixian subjects to 3% VAT as small taxpayer until September 2022, and then applied to general taxpayer in October 2022 . Entities that

are VAT general taxpayers are allowed to offset qualified input VAT paid to suppliers against their output VAT liabilities. Net VAT balance

between input VAT and output VAT is recorded in tax payable. The amount of VAT liability is determined by applying the applicable tax

rate to the invoiced amount. The Company reports revenue net of PRC’s VAT for all the periods presented on the statements of operations

and comprehensive income (loss).

Revenue

Recognition

The

Company recognizes revenue under Accounting Standards Codification (“ASC”) Topic 606, Revenue from Contracts with Customers

(“ASC 606”). The core principle of the revenue standard is that a company should recognize revenue to depict the transfer

of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in

exchange for those goods or services. The following five steps are applied to achieve that core principle:

| |

● |

Step 1: Identify the contract with the customer |

| |

|

|

| |

● |

Step 2: Identify the performance obligations in the contract |

| |

|

|

| |

● |

Step 3: Determine the transaction price |

| |

|

|

| |

● |

Step 4: Allocate the transaction price to the performance obligations in the contract |

| |

|

|

| |

● |

Step 5: Recognize revenue when the company satisfies a performance obligation |

The

Company generates revenue primarily from its insurance agency services. According to the agency service contracts made by and between

the Company and insurance carriers, the Company is authorized to sell insurance products provided by insurance carriers to the insureds

as an insurance agent, and collects commission from the respective insurance carriers as revenue.

The

commission charged is determined by the terms agreed in the agency service contract, typically a percentage of insurance premium. The

performance obligation is considered met and revenue is recognized when the insurance agency services are rendered and completed at the

time an insurance policy becomes effective and the premium is collected from the insured.

The

necessary data to reasonably determine the revenue amount is controlled by the insurance carriers, and bill statement is confirmed with

the Company on a monthly basis. The Company has met all the criteria of revenue recognition when the premiums are collected by the respective

insurance carriers and not before, because collectability is not ensured until receipt of the premium. Therefore, the Company does not

accrue any commissions prior to the receipt of the related premiums of insurance carriers, due to the specific practice in the industry.

The Company

recorded insurance agency commission revenue in the amount of $47,443,458 and $44,948,234 for the years ended December 31, 2022 and 2021,

respectively.

Cost

of Revenues

Cost of

revenues consists primarily of commissions paid to distribution channels. The Company generally recognizes commissions as cost of revenues

when incurred. For the years ended December 31, 2022 and 2021, the cost of revenue amounted to $43,775,753 and $41,946,093 respectively.

Selling

Expenses

Selling

expenses mainly consisted of advertising and marketing expenses. For the years ended December 31, 2022 and 2021, the selling expenses

amounted to $3,380,556 and $2,440,581 respectively.

Operating

Leases

The Company

adopted FASB Accounting Standards Codification, Topic 842, Leases (“ASC 842”) using the modified retrospective approach, electing

the practical expedient that allows the Company not to restate prior to the adoption of the standard on January 1, 2019.

The Company

applied the following practical expedients in the transition to the new standard allowed under ASC 842:

| Practical Expedient |

|

Description |

| Reassessment of expired or existing contracts |

|

The Company elected not to reassess, at the application date, whether any expired or existing contracts contained leases, the lease classification for any expired or existing leases, and the accounting for initial direct costs for any existing leases. |

| Use of hindsight |

|

The Company elected to use hindsight in determining the lease term (that is, when considering options to extend or terminate the lease and to purchase the underlying asset) and in assessing impairment of right-to-use assets. |

| Reassessment of existing or expired land easements |

|

The Company elected not to evaluate existing or expired land easements that were not previously accounted for as leases under ASC 840, as allowed under the transition practical expedient. Going forward, new or modified land easements will be evaluated under ASU No. 2016-02. |

| Separation of lease and non-lease components |

|

Lease agreements that contain both lease and non-lease components are generally accounted for separately. |

| Short-term lease recognition exemption |

|

The Company also elected the short-term lease recognition exemption and will not recognize ROU assets or lease liabilities for leases with a term less than 12 months. |

The Company determines if an arrangement is a

lease at inception under FASB ASC Topic 842, Right of Use Assets (“ROU”) and lease liabilities are recognized at commencement

date based on the present value of remaining lease payments over the lease term. For this purpose, the Company considers only payments

that are fixed and determinable at the time of commencement. As most of its leases do not provide an implicit rate, it uses its incremental

borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company’s

incremental borrowing rate is a hypothetical rate based on its understanding of what its credit rating would be. The ROU assets include

adjustments for prepayments and accrued lease payments. The ROU asset also includes any lease payments made prior to commencement and

is recorded net of any lease incentives received. The Company’s lease terms may include options to extend or terminate the lease

when it is reasonably certain that it will exercise such options.

ROU assets are reviewed for impairment when indicators

of impairment are present. ROU assets from operating and finance leases are subject to the impairment guidance in ASC 360, Property, Plant,

and Equipment, as ROU assets are long-lived nonfinancial assets.

ROU assets are tested for impairment individually

or as part of an asset group if the cash flows related to the ROU asset are not independent from the cash flows of other assets and liabilities.

An asset group is the unit of accounting for long-lived assets to be held and used, which represents the lowest level for which identifiable

cash flows are largely independent of the cash flows of other groups of assets and liabilities. The Company recognized no impairment of

ROU assets as of December 31, 2022 and 2021. Operating leases are included in operating lease ROU and operating lease liabilities (current

and non-current), on the consolidated balance sheets.

Employee

Benefits

The

Company makes mandatory contributions to the PRC government’s health, retirement benefit and unemployment funds in accordance with

the relevant Chinese social security laws. The costs of these payments are charged to the same accounts as the related salary costs in

the same period as the related salary costs incurred. Employee benefit costs totaled $641,389 and $803,833 for the years ended December

31, 2022 and 2021, respectively.

Income

Taxes

The Company accounts for income taxes using the

asset/liability method prescribed by ASC 740, “Income Taxes.” Under this method, deferred tax assets and liabilities are determined

based on the difference between the financial reporting and tax bases of assets and liabilities using enacted tax rates that will be in

effect in the period in which the differences are expected to reverse. The Company records a valuation allowance to offset deferred tax

assets if, based on the weight of available evidence, it is more-likely-than-not that some portion, or all, of the deferred tax assets

will not be realized. The effect on deferred taxes of a change in tax rates is recognized as income or loss in the period that includes

the enactment date.

The Company follows the accounting guidance for

uncertainty in income taxes using the provisions of ASC 740 “Income Taxes”. Using that guidance, tax positions initially need

to be recognized in the financial statements when it is more likely than not the position will be sustained upon examination by the tax

authorities. For the years ended December 31, 2022 and 2021, the Company had no significant uncertain tax positions that qualify for either

recognition or disclosure in the financial statements. Tax years that remain subject to examination are the years ended December 31, 2022

and 2021. The Company recognizes interest and penalties related to significant uncertain income tax positions in other expense. No such

interest and penalties incurred for the years ended December 31, 2022 and 2021.

Comprehensive

Income

Comprehensive

income is comprised of net income and all changes to the statements of equity, except those due to investments by shareholders, changes

in paid-in capital and distributions to shareholders. For the Company, comprehensive income for the years ended December 31, 2022 and

2021 consisted of net income and unrealized (loss) gain from foreign currency translation adjustment.

Fair

Value of Financial Instruments and Fair Value Measurements

The

Company adopted the guidance of ASC 820 for fair value measurements which clarifies the definition of fair value, prescribes methods for

measuring fair value, and establishes a fair value hierarchy to classify the inputs used in measuring fair value as follows:

| |

● |

Level 1-Inputs are unadjusted quoted prices in active markets for identical assets or liabilities available at the measurement date. |

| |

|

|

| |

● |

Level 2-Inputs are unadjusted quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets and liabilities in markets that are not active, inputs other than quoted prices that are observable, and inputs derived from or corroborated by observable market data. |

| |

|

|

| |

● |

Level 3-Inputs are unobservable inputs which reflect the reporting entity’s own assumptions on what assumptions the market participants would use in pricing the asset or liability based on the best available information. |

The

carrying amounts reported in the balance sheets for cash and cash equivalents, accounts receivable, prepaid expenses and other current

assets, taxes payable, accrued liabilities and other payables, and due from (to) related parties, approximate their fair market value

based on the short-term maturity of these instruments.

Commitments

and Contingencies

In

the normal course of business, the Company is subject to contingencies, such as legal proceedings and claims arising out of its business,

that cover a wide range of matters. Liabilities for such contingencies are recorded when it is probable that a liability has been incurred

and the amount of the assessment can be reasonably estimated.

Segment

Reporting

ASC

280 “Segment reporting” establishes standards for reporting information on operating segments in interim and annual financial

statements. Operating segments are defined as the components of an enterprise about which separate financial information is available

that is evaluated regularly by the chief operating decision maker in deciding how to allocate resources and in assessing performance.

Our chief operating decision makers direct the allocation of resources to operating segments based on the profitability, cash flows, and

growth opportunities of each respective segment.

The

Company manages its business as a single operating segment engaged in the provision of insurance agent services in the PRC. Substantially

all of its revenues are derived in the PRC. All long-lived assets are located in PRC.

Related

Parties

Parties

are considered to be related to the Company if the parties, directly or indirectly, through one or more intermediaries, control, are controlled

by, or are under common control with the Company. Related parties also include principal owners of the Company, its management, members

of the immediate families of principal owners of the Company and its management and other parties with which the Company may deal with

if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting

parties might be prevented from fully pursuing its own separate interests. The Company discloses all significant related party transactions.

NOTE 4 – ACCOUNTS

RECEIVABLE, NET

Accounts receivable, net consist of the following:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Accounts receivable | |

$ | 2,931,320 | | |

$ | 3,615,399 | |

| Less: Allowance for doubtful accounts | |

| (38,360 | ) | |

| (14,054 | ) |

| Total accounts receivable, net | |

$ | 2,892,960 | | |

$ | 3,601,345 | |

Movements of allowance for doubtful accounts are as follows:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Beginning balance | |

$ | 14,054 | | |

$ | - | |

| Addition | |

| 26,399 | | |

| 13,889 | |

| Exchange rate effect | |

| (2,093 | ) | |

| 165 | |

| Ending balance | |

$ | 38,360 | | |

$ | 14,054 | |

NOTE

5 – PREPAYMENTS

Prepayments consist of the following:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Advances to suppliers | |

$ | 1,411,026 | | |

$ | 2,427,469 | |

| Prepaid expenses | |

| 1,240 | | |

| 21,880 | |

| Total | |

$ | 1,412,266 | | |

$ | 2,449,349 | |

NOTE

6 – SHORT-TERM INVESTMENT

Short-term

investments are investments in wealth management product with underlying in bonds offered by private entities and other equity products.

The investments can be redeemed upon one workday’s notice and their carrying values approximate their fair values. The gain (loss)

from sale of any investments and fair value change are recognized in the statements of income and comprehensive income.

As

of December 31, 2022 and 2021, the ending balance of short-term investments were $273,182 and $393,651 respectively.

NOTE

7 – PROPERTY AND EQUIPMENT

Property

and equipment consisted of the following at December 31, 2022 and 2021:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Automobile | |

$ | 113,075 | | |

$ | 79,533 | |

| Less: Accumulated depreciation | |

| (44,534 | ) | |

| (31,447 | ) |

| Property and equipment, net | |

$ | 68,541 | | |

$ | 48,086 | |

For

the years ended December 31, 2022 and 2021, depreciation expense amounted to $16,305 and $17,322, respectively, all of which were included

in operating expenses.

NOTE

8 – OTHER PAYABLES

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Borrowing from other parties | |

| 635,102 | | |

| 966,662 | |

| Accrued expense | |

| 3,010 | | |

| 51,740 | |

| Others | |

| 142,135 | | |

| 114,049 | |

| Total | |

$ | 780,247 | | |

$ | 1,132,451 | |

NOTE

9 – RELATED PARTY BALANCES AND TRANSACTIONS

Due from related parties

At December 31, 2022 and 2021, due from related

party consisted of the following:

| Name of related party | |

Relationship | |

December 31,

2022 | | |

December 31,

2021 | |

| Yangwei Cui | |

A Key Management Personnel | |

$ | 19,799 | | |

$ | 14,934 | |

| Shumei Wang | |

A Key Management Personnel | |

| 63 | | |

| 69 | |

| Xin Wang | |

A Key Management Personnel | |

| 922 | | |

| 1,007 | |

| Jianlong Zhao | |

A Key Management Personnel | |

| — | | |

| 18,351 | |

| Total | |

| |

$ | 20,784 | | |

$ | 34,361 | |

The balance of due from related parties is interest

free, unsecured and repayable on demand. Management believes that the related party receivable is fully collectable. Therefore, no allowance

for doubtful accounts is deemed to be required on its due from related party at December 31, 2022 and 2021. The Company historically has

not experienced an uncollectible receivable from the related party.

Due to related parties

| Name of related party | |

Relationship | |

December 31,

2022 | | |

December 31,

2021 | |

| Jian Guo | |

Chairman of the Board of Directors | |

$ | — | | |

$ | 50,354 | |

| Xiaodan Chen | |

A Key Management Personnel | |

| 5,743 | | |

| — | |

| Jianlong Zhao | |

A Key Management Personnel | |

| 1,205 | | |

| 18,679 | |

| Wei Meng | |

A Key Management Personnel | |

| 4,525 | | |

| 4,943 | |

| Guixin Ye | |

A Key Management Personnel | |

| 4,551 | | |

| — | |

| Xin Wang | |

A Key Management Personnel | |

| 699 | | |

| 763 | |

| Total | |

| |

$ | 16,723 | | |

$ | 74,739 | |

The balance of due to related parties represents

expenses paid by these related parties on behalf of the Company. The related parties’ payable is short-term in nature, interest

free, unsecured and repayable on demand.

NOTE

10 – INCOME TAXES

Hong

Kong

Alpha Mind HK is

incorporated in Hong Kong and is subject to 16.5% income tax on their taxable income generated from operations in Hong Kong. The first

HK$2 million of profits arising in or derived from Hong Kong are taxed at 8.25% and any assessable profits over HK$2 million are taxed

at 16.5%. Alpha Mind HK had no operations for the years ended December 31, 2022 and 2021.

Therefore, there was no provision for income taxes in the years ended December 31, 2022 and 2021.

PRC

Jiachuang Yingan WFOE, Huaming Insurance and Huaming

Yunbao are subject to PRC Enterprise Income Tax (“EIT”) on the taxable income in accordance with the relevant PRC income tax

laws. The EIT rate for companies operating in the PRC is 25%.

On March 16, 2007, the National People’s

Congress enacted a new enterprise income tax law, which took effect on January 1, 2008. The law applies a uniform 25% enterprise income

tax rate to both foreign invested enterprises and domestic enterprises. In the years ended December 31, 2022 and 2021, Jiachuang Yingan

WFOE did not generate any taxable income. Therefore, there was no provision for income taxes in the years ended December 31, 2022 and

2021.

The components of the provision for income taxes

for the years ended December 31, 2022 and 2021 consisted of the following:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| Current | |

$ | (26,249 | ) | |

$ | (20,623 | ) |

| Deferred | |

| 22,202 | | |

| 4,230 | |

| Total income tax expense | |

| (4,047 | ) | |

| (16,393 | ) |

Reconciliation of the Differences Between Statutory

Tax Rate and the Effective Tax Rate

The following table reconciles China statutory

rates to the Company’s effective tax rate:

| | |

December 31,

2022 | | |

December 31,

2021 | |

| China statutory income tax rate | |

| 25 | % | |

$ | 25 | % |

| Change in valuation allowance | |

| (24 | )% | |

| (22 | )% |

| Effective tax rate | |

| 1 | % | |

| 3 | % |

The Company’s approximate net deferred tax

assets as of December 31, 2022 and 2021 attributable to tax filings in the PRC are as follows:

| Deferred Tax Assets | |

December 31,

2022 | | |

December 31,

2021 | |

| Net operating loss carry-forwards | |

$ | - | | |

$ | - | |

| Allowance for doubtful account | |

| 25,360 | | |

| 4,280 | |

| Net deferred tax assets | |

$ | 25,360 | | |

$ | 4,280 | |

The Company provided a valuation allowance equal

to the deferred income tax assets related to net operating loss carryforward for the year ended December 31, 2022, because it was not

known whether future taxable income will be sufficient to utilize the loss carryforward. The potential tax benefit arising from the loss

carryforward will begin to expire in 2026.

As of December 31, 2022 and 2021, the Company

had no significant uncertain tax positions that qualify for either recognition or disclosure in the financial statements. As of December

31, 2022, income tax returns for the tax years ended December 31, 2017 through December 31, 2021 remain open for statutory examination

by PRC tax authorities.

The uncertain tax positions are related to tax

years that remain subject to examination by the relevant tax authorities. Based on the outcome of any future examinations, or as a result

of the expiration of statute of limitations for specific jurisdictions, it is reasonably possible that the related unrecognized tax benefits

for tax positions taken regarding previously filed tax returns, might materially change from those recorded as liabilities for uncertain

tax positions in the Company’s consolidated financial statements as of December 31, 2022 and 2021. In addition, the outcome of these

examinations may impact the valuation of certain deferred tax assets (such as net operating losses) in future periods. The Company’s

policy is to recognize interest and penalties accrued on any unrecognized tax benefits, if any, as a component of other expense. The Company

does not anticipate any significant increases or decreases to its liability for unrecognized tax benefits within the next twelve months.

Accounting for Uncertainty in Income Taxes

The tax authority of the PRC government conducts

periodic and ad hoc tax filing reviews on business enterprises operating in the PRC after those enterprises complete their relevant tax

filings. Therefore, the Company’s PRC entities’ tax filings results are subject to change. It is therefore uncertain as to

whether the PRC tax authority may take different views about the Company’s PRC entities’ tax filings, which may lead to additional

tax liabilities.

ASC 740 requires recognition and measurement of

uncertain income tax positions using a “more-likely-than-not” approach. The management evaluated the Company’s tax positions

and concluded that no provision for uncertainty in income taxes was necessary as of December 31, 2022 and 2021.

NOTE

11 – SHAREHOLDERS’ EQUITY

Alpha Mind BVI was established under the laws

of British Virgin Islands on April 17, 2023. The Company is authorised to issue a maximum of 50,000 shares of US$1.00 par value each of

a single class and series.

NOTE

12 – COMMITMENTS AND CONTINGENCIES

Contingencies

From time to time, the Company may be subject

to certain legal proceedings, claims and disputes that arise in the ordinary course of business. Although the outcomes of these legal

proceedings cannot be predicted, the Company does not believe these actions, in the aggregate, will have a material adverse impact on

its financial position, results of operations or liquidity.

Variable Interest Entity Structure

In the opinion of the management, (i) the corporate

structure of the Company is in compliance with existing PRC laws and regulations; (ii) the VIE Agreements are valid and binding, and do

not result in any violation of PRC laws or regulations currently in effect; and (iii) the business operations of WFOE, VIE and VIE’s

subsidiaries are in compliance with existing PRC laws and regulations in all material respects.

However, there are substantial uncertainties regarding

the interpretation and application of current and future PRC laws and regulations. Accordingly, the Company cannot be assured that PRC

regulatory authorities will not ultimately take a contrary view to the foregoing opinion of its management. If the current corporate structure

of the Company or the VIE Agreements are found to be in violation of any existing or future PRC laws and regulations, the Company may

be required to restructure its corporate structure and operations in the PRC to comply with changing and new PRC laws and regulations.

In the opinion of management, the likelihood of loss in respect of the Company’s current corporate structure or the VIE Agreements

is remote based on current facts and circumstances.

NOTE

13 – SUBSEQUENT EVENTS

The Group has evaluated subsequent events through

the date the consolidated financial statements are issued, and concluded that no subsequent events have occurred that would require recognition

or disclosure in the consolidated financial statements.

22

Exhibit 99.2

UNAUDITED PRO FORMA COMBINED FINANCIAL INFORMATION

On May 31,

2023, the Company completed the subscription for 85% of the issued and outstanding shares of Alpha Mind Technology Limited (“Alpha

Mind”), at a total consideration of $99,650,000, consisting of $92,650,000 in cash and $7.0 million in the form of a convertible

promissory note (the “Share Subscription”).

We refer the acquired company, Alpha Mind as “the

acquired company”, and the corresponding transactions collectively as “Acquisition”.

The following unaudited pro forma combined financial

information of the Company and the acquired company is presented to illustrate the estimated effects of the Acquisition described below

(“Adjustments” or “Pro Forma Adjustments”).

The unaudited pro forma combined balance sheet

as of December 31, 2022 combines the historical consolidated balance sheet of the Company and the consolidated balance sheet of the acquired

company, after giving effect to the Acquisition as if it had occurred on December 31, 2022. The unaudited pro forma statement of operations

for the year ended December 31, 2022 combines the historical consolidated statement of comprehensive loss of the Company and the consolidated

statement of profit or loss and other comprehensive income or loss of the acquired company, after giving effect to the Acquisition as

if it had occurred on January 1, 2022. These unaudited pro forma combined balance sheet and unaudited pro forma combined statement of

operations are referred to collectively as the “pro forma financial information.”

The pro forma financial information should be

read in conjunction with the accompanying notes. In addition, the pro forma financial information is derived from and should be read in

conjunction with the following historical financial statements and accompanying notes of the Company and the acquired companies:

(i) audited consolidated financial statements

as of and for the fiscal year ended December 31, 2022 and the related notes included in the annual report on Form 20-F for the year ended

December 31, 2022 filed by the Company; and

(ii) audited consolidated financial statements

of Alpha Mind as of and for the year ended December 31, 2022 and the related notes included as Exhibit 99.1 to this Current Report on

Form 6-K filed August 29, 2023.

Unaudited Pro Forma Combined Balance Sheet

| | |

As

of December 31, 2022 | |

| | |

MMTEC

Historical | | |

Alpha

Mind Historical | | |

Pro

Forma Adjustments for Acquisitions | | |

Note | |

Pro

Forma Combined | |

| | |

US$ | | |

US$ | | |

US$ | | |

| |

US$ | |

| ASSETS | |

| | |

| | |

| | |

| |

| |

| Current assets: | |

| | |

| | |

| | |

| |

| |

| Cash and cash

equivalents | |

| 3,825,477 | | |

| 341,743 | | |

| - | | |

| |

| 4,167,220 | |

| Accounts receivable, net | |

| 295,683 | | |

| 2,892,960 | | |

| - | | |

| |

| 3,188,643 | |

| Loan receivable, net | |

| 4,620,824 | | |

| - | | |

| - | | |

| |

| 4,620,824 | |

| Security

deposits - current | |

| 8,274 | | |

| - | | |

| - | | |

| |

| 8,274 | |

| Prepaid expenses and other

current assets | |

| 172,205 | | |

| - | | |

| 1,564,835 | | |

A | |

| 1,737,040 | |

| Prepayments | |

| - | | |

| 1,412,266 | | |

| (1,412,266 | ) | |

A | |

| - | |

| Other receivables, net | |

| - | | |

| 52,011 | | |

| (52,011 | ) | |

A | |

| - | |

| Short-term investment | |

| - | | |

| 273,182 | | |

| - | | |

| |

| 273,182 | |

| Other current assets | |

| - | | |

| 100,558 | | |

| (100,558 | ) | |

A | |

| - | |

| Deferred

offering cost | |

| 112,748 | | |

| - | | |

| - | | |

| |

| 112,748 | |

| Total

current assets | |

| 9,035,211 | | |

| 5,072,720 | | |

| - | | |

| |

| 14,107,931 | |

| | |

| | | |

| | | |

| | | |

| |

| | |

| Non-current

assets: | |

| | | |

| | | |

| | | |

| |

| | |

| Restricted Cash- noncurrent | |

| - | | |

| 717,916 | | |

| - | | |

| |

| 717,916 | |

| Security deposit - noncurrent | |

| 140,746 | | |

| - | | |

| - | | |

| |

| 140,746 | |

| Property and equipment, net | |

| 184,423 | | |

| 68,541 | | |

| - | | |

| |

| 252,964 | |

| Deposit for business acquisition | |

| 1,000,000 | | |

| - | | |

| - | | |

| |

| 1,000,000 | |

| Operating lease right-of-use

asset | |

| 1,055,127 | | |

| - | | |

| - | | |

| |

| 1,055,127 | |

| Deferred tax assets | |

| | | |

| 25,360 | | |

| - | | |

| |

| 25,360 | |

| Intangible assets, net | |

| - | | |

| - | | |

| 5,500,959 | | |

B | |

| 5,500,959 | |

| Goodwill | |

| - | | |

| - | | |

| 109,368,955 | | |

B | |

| 109,368,955 | |

| Total

non-current assets | |

| 2,380,296 | | |

| 811,817 | | |

| 114,869,914 | | |

| |

| 118,062,027 | |

| TOTAL

ASSETS | |

| 11,415,507 | | |

| 5,884,537 | | |

| 114,869,914 | | |

| |

| 132,169,958 | |

| | |

| | | |

| | | |

| | | |

| |

| | |

| LIABILITIES

AND SHAREHOLDERS’ EQUITY | |

| | | |

| | | |

| | | |

| |

| | |

| Current

liabilities: | |

| | | |

| | | |

| | | |

| |

| | |

| Accounts payable | |

| - | | |

| 2,496,587 | | |

| - | | |

| |

| 2,496,587 | |

| Salary payable | |

| 372,980 | | |

| 65,709 | | |

| - | | |

| |

| 438,689 | |

| Accrued liabilities and other

payables | |

| 395,352 | | |

| - | | |

| 796,970 | | |

A | |

| 1,192,322 | |

| Other payables | |

| - | | |

| 796,970 | | |

| (796,970 | ) | |

A | |

| - | |

| Taxes payable | |

| - | | |

| 154,585 | | |

| - | | |

| |

| 154,585 | |

| Advance from customer | |

| - | | |

| 5,306 | | |

| - | | |

| |

| 5,306 | |

| Operating

lease liabilities, current | |

| 405,591 | | |

| - | | |

| - | | |

| |

| 405,591 | |

| Total

current liabilities | |

| 1,173,923 | | |

| 3,519,157 | | |

| - | | |

| |

| 4,693,080 | |

| | |

| | | |

| | | |

| | | |

| |

| | |

| Non-current

liabilities: | |

| | | |

| | | |

| | | |

| |

| | |

| Accrued liabilities, noncurrent | |

| 209,250 | | |

| - | | |

| - | | |

| |

| 209,250 | |

| Long term debt | |

| - | | |

| - | | |

| 99,650,00 | | |

B | |

| 99,650,00 | |

| Operating

lease liabilities, noncurrent | |

| 647,983 | | |

| - | | |

| - | | |

| |

| 647,983 | |

| Total

non-current liabilities | |

| 857,233 | | |

| - | | |

| 99,650,00 | | |

| |

| 100,507,233 | |

| TOTAL

LIABILITIES | |

| 2,031,156 | | |

| 3,519,157 | | |

| 99,650,00 | | |

| |

| 105,200,313 | |

| | |

| | | |

| | | |

| | | |

| |

| | |

| Shareholders’

Equity: | |

| | | |

| | | |

| | | |

| |

| | |

| Common shares | |

| 51,451 | | |

| 50,000 | | |

| (50,000 | ) | |

B | |

| 51,451 | |

| Subscription receivable | |

| - | | |

| (50,000 | ) | |

| 50,000 | | |

B | |

| - | |

| Additional paid-in capital | |

| 31,727,407 | | |

| 8,649,321 | | |

| (8,649,321 | ) | |

B | |

| 31,727,407 | |

| Accumulated deficit and statutory

reserve | |

| (22,253,030 | ) | |

| (5,636,318 | ) | |

| 5,636,318 | | |

B | |

| (22,253,030 | ) |

| Accumulated

other comprehensive income | |

| (141,477 | ) | |

| (647,623 | ) | |

| 647,623 | | |

B | |

| (141,477 | ) |

| Total

MMTEC shareholders’ equity | |

| 9,384,351 | | |

| 2,365,380 | | |

| (2,365,380 | ) | |

| |

| 9,384,351 | |

| Noncontrolling

interests | |

| - | | |

| - | | |

| 17,585,294 | | |

| |

| 17,585,294 | |

| Total

shareholders’ equity | |

| 9,384,351 | | |

| 2,365,380 | | |

| 15,219,914 | | |

| |

| 26,969,645 | |

| TOTAL

LIABILITIES AND SHAREHOLDERS’ EQUITY | |

| 11,415,507 | | |

| 5,884,537 | | |

| 114,869,914 | | |

| |

| 132,169,958 | |

The accompanying notes are an integral part of

these unaudited pro forma combined financial statements

Unaudited Pro Forma Combined Statements of Operations

| |

|

For

the year ended December 31, 2022 |

| |

|

MMTEC

Historical |

|

|

Alpha Mind

Historical |

|

|

Pro Forma

Adjustments

for Acquisitions |

|

|

Note |

|

Pro Forma

Combined |

|

| |

|

US$ |

|

|

US$ |

|

|

US$ |

|

|

|

|

US$ |

|

| Revenue |

|

|

1,099,133 |

|

|

|

47,443,458 |

|

|

|

- |

|

|

|

|

|

48,542,591 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cost of revenue |

|

|

231,084 |

|

|

|

43,775,753 |

|

|

|

- |

|

|

|

|

|

44,006,837 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gross profit |

|

|

868,049 |

|

|

|

3,667,705 |

|

|

|

- |

|

|

|

|

|

4,535,754 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Selling and marketing |

|

|

1,007,652 |

|

|

|

3,380,556 |

|

|

|

- |

|

|

|

|

|

4,388,208 |

|

| General and administrative |

|

|

5,753,012 |

|

|

|

1,632,336 |

|

|

|

- |

|

|

|

|

|

7,385,348 |

|

| Total operating expenses |

|

|

6,760,664 |

|

|

|

5,012,892 |

|

|

|

- |

|

|

|

|

|

11,773,556 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loss from operations |

|

|

(5,892,615 |

) |

|

|

(1,345,187 |

) |

|

|

- |

|

|

|

|

|

(7,237,802 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other income (expense) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest income |

|

|

94,372 |

|

|

|

18,559 |