Filing pursuant to Rule 425 under the

Securities Act of 1933, as amended

Deemed filed under Rule 14a-12 under the

Securities Exchange Act of 1934, as amended

Filer: TLGY Acquisition Corporation

Subject Company: TLGY Acquisition Corporation

Filer’s Commission File Number: 001-41101

Date: October 12, 2023

On October 12, 2023, TLGY Acquisition Corporation released the following

presentation:

| : TLGY INVESTOR PRESENTATION / OCTOBER 2023

REVOLUTIONIZING

With a Viable Green

Biodegradable Solution

THE GLOBAL

PLASTICS MARKET |

| INVESTOR PRESENTATION / OCTOBER 2023 2

DISCLAIMER

This presentation has been prepared in making an evaluation with respect to a proposed business combination (the “Proposed Transaction”) between TLGY Acquisition Corporation (“TLGY”) and Verde Bioresins, Inc.

(“Verde”).

This presentation does not purpose to contain all information that may be required to evaluate a possible transaction. This presentation is not intended to form the basis of any investment decision by the recipient and

does not constitute investment, tax or legal advice. No representation or warranty, express or implied, is or will be given by TLGY or Verde or any of their respective affiliates, directors, officers, employees or advisers or any

other person as to the accuracy or completeness of the information in this presentation or any other written, oral or other communications transmitted or otherwise made available to any party in the course of its

evaluation of a possible transaction, and no responsibility or liability whatsoever is accepted for the accuracy or sufficiency thereof or for any errors, omissions or misstatements, negligent or otherwise, relating thereto.

Accordingly, none of TLGY or Verde or any of their respective affiliates, directors, officers, employees or advisers or any other person shall be liable for any direct, indirect or consequential loss or damages suffered by any

person as a result of relying on any statement in or omission from this presentation and any such liability is expressly disclaimed.

Forward-Looking Information

This presentation and oral statements accompanying this presentation contain forward-looking statements within the meaning of the federal securities laws with respect to the Proposed Transaction, and any statements

other than statements of historical fact contained in this presentation could be deemed to be forward-looking statements. These forward-looking statements include, among other things, expectations, beliefs, intentions,

plans, prospects, financial results or strategies regarding Verde and the Proposed Transaction and the future held by the respective management teams of TLGY or Verde, the anticipated benefits and the anticipated

timing of the Proposed Transaction, future financial condition and performance of Verde and expected financial impacts of the Proposed Transaction (including future revenue, pro forma enterprise value and cash

balance), the satisfaction of closing conditions to the Proposed Transaction, financings transactions, if any, related to the Proposed Transaction, the level of redemptions of TLGY’s stockholders and the products and

markets and expected future performance and market opportunities of Verde. These forward-looking statements generally are identified by the words “anticipate,’ “believe,” “could,” “expect,” “estimate,” “future,” “intent,”

“may,” “might,” “strategy,” “opportunity,” “plan,” “project,” “possible,” “potential,” “project,” “predict,” “scales,” “representation of,” “valuation,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar

expressions, but the absence of these words does not mean that a statement is not forward-looking.

These forward-looking statements are based on management’s current expectations and actual results and future events may differ materially due to risks and uncertainties, including but not limited to, those set forth

under the caption “Risk Factors” contained elsewhere in this presentation. Recipients should carefully consider such other risks and uncertainties to be described in the “Risk Factors” section of the registration statement

on Form S-4 (the “Form S-4”) filed by TLGY in connection with the Proposed Transaction and other documents filed or to be filed by TLGY from time to time with the Securities and Exchange Commission (“SEC”). These

filings identify and address other important risks and uncertainties which could cause actual events and results to differ materially from those contained in the forward-looking statements. Recipients are cautioned not to

put undue reliance on forward-looking statements, which speak only as of the date this presentation is given. Each of Verde and TLGY disclaim any obligation to update information contained in these forward-looking

statements, whether as a result of new information, future events, or otherwise, except as required by law. Neither Verde nor TLGY gives any assurance that either Verde or TLGY, or the combined company, will achieve its

expectations. By attending or receiving this presentation, you acknowledge that you will be solely responsible for your own assessment of the market and our market position and that you will conduct your own analysis

and be solely responsible for forming your own view of the potential future performance of the business.

Any financial projections or similar forward-looking information presented in this presentation represent current estimates by Verde’s management of future performance based on various assumptions, which may or may

not prove to be correct. Verde’s independent registered public accounting firm has not audited, reviewed, compiled or performed any procedures with respect to any projections or similar forward- looking information

and accordingly they did not express an opinion or provide any other form of assurance with respect thereto. Any projections or similar forward-looking information should not be relied upon as being necessarily indicative

of future results. The assumptions and estimates underlying any projections or similar forward-looking information are inherently uncertain and are subject to a wide variety of significant business, economic and

competitive risks that could cause actual results to differ materially from those contained in such projections or similar forward-looking information. Accordingly, there can be no assurance that any projections or similar

forward-looking information will be realized. Further, industry experts may disagree with these assumptions and with management’s view of the market and the prospects for Verde.

While the information contained in this presentation is believed to be accurate, no representation or warranty is given or made, express or implied, as to the achievement, reasonableness, completeness, accuracy of, and no

reliance should be placed on, any projections, estimates, forecasts, analyses or forward-looking statements contained in this presentation which involve by their nature a number of risks, uncertainties or assumptions that

could cause actual results or events to differ materially from those expressed or implied in this presentation. Only those particular representations and warranties made in the definitive agreement and subject to such

limitations and restrictions as may be specified in such agreement, shall have any legal effect. By its acceptance hereof, each recipient agrees that neither TLGY or Verde shall be liable for any direct, indirect, consequential

or any other loss or damages suffered by any person as a result of relying on any statement in or omission from this presentation, along with other information furnished in connection therewith, and any such liability is

expressly disclaimed. |

| INVESTOR PRESENTATION / OCTOBER 2023 3

DISCLAIMER

Certain Assumptions

Unless otherwise expressly stated herein, all information relating to the Proposed Transaction: (i) assumes no redemptions by TLGY stockholders in connection with the Proposed Transaction; (ii) does not give effect to any

PIPE or other financing that may be raised in connection with or in anticipation of the Proposed Transaction; (iii) does not assume the future exercise of or otherwise give effect to TLGY’s outstanding warrants held by

public investors or TLGY’s sponsor or Verde’s management or any additional warrants that may be issued in connection with the Proposed Transaction; (iv) assumes that no additional shares of common stock will be issued

in the future as earnout merger consideration in connection with the Proposed Transaction; and (v) does not give effect to future equity awards contemplated to be issued in connection with or following completion of the

Proposed Transaction.

Industry and Market Data

The information contained herein also includes information provided by third parties, such as market research firms. None of TLGY, Verde or their respective affiliates and any third parties that provide information to TLGY

or Verde, such as market research firms, guarantees the accuracy, completeness, timeliness or availability of any information. None of TLGY, Verde or their respective affiliates and any third parties that provide information

to TLGY or Verde, such as market research firms, are responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or the results obtained from the use of such context. None of TLGY, Verde or

their respective affiliates gives any express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use, and they expressly disclaim any responsibility or

liability for direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees or losses (including lost income or profits and opportunity costs) in connection with

the use of the information herein.

All Biodegradable and Compostable Claims are based on preliminary third-party ASTM D5511 and D5338 test results which are available upon request. In California you cannot claim biodegradability of products. In California

you may only claim a product is compostable in an industrial composting environment upon passing ASTM D6400 testing, which testing is currently ongoing by Verde. Resin test results will vary based on application and

related ingredients. Products should be tested individually and biodegradability and compostability will vary based on formula and application related thickness and density of product among other factors. For more

information, please see California and US FTC Green Guides.

Trademarks and Intellectual Property

All trademarks, service marks, and trade names of Verde, TLGY or their respective affiliates used herein are trademarks, service marks, or registered trade names of Verde, TLGY, respectively, as noted herein. Any other

product, company names, or logos mentioned herein are the trademarks and/or intellectual property of their respective owners, and their use is not alone intended to, and does not alone imply, a relationship with Verde,

TLGY, or an endorsement or sponsorship by or of Verde or TLGY. Solely for convenience, the trademarks, service marks and trade names referred to in this presentation may appear without the ®, TM or SM symbols, but

such references are not intended to indicate, in any way, that Verde, TLGY or the applicable rights owner will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these

trademarks, service marks and trade names.

This presentation contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this presentation may appear without the ® or ™

symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend

our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

Non-GAAP Financial Information

Certain financial information and data contained in this presentation are unaudited and do not conform to Regulation S-X. Accordingly, such information may not be included in, may be adjusted in, or may be presented

differently in, any proxy statement/prospectus or registration statement or other report or documents to be filed or furnished by TLGY with the SEC. Some of the financial information and data contained in this

presentation, including EBIDTA, has not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). TLGY and Verde believe this non-GAAP financial information to be a helpful

measure to assess Verde’s operational performance and for financial and operational decision-making. You should review Verde’s audited financial statements prepared in accordance with GAAP, which are included in the

Form S-4. |

| INVESTOR PRESENTATION / OCTOBER 2023 4

DISCLAIMER

Additional Information and Where to Find it

In connection with the Proposed Transaction, TLGY filed a registration statement on Form S-4 with the SEC, which includes a preliminary prospectus with respect to its securities to be issued in connection with the

Proposed Transaction and a preliminary proxy statement with respect to a stockholder meeting at which TLGY’s stockholders will be asked to vote on the Proposed Transaction. TLGY and Verde urge investors,

stockholders, and other interested persons to read the Form S-4, including the proxy statement/prospectus, any amendments thereto, and any other documents filed with the SEC, before making any voting or investment

decision because these documents will contain important information about the Proposed Transaction. After the Form S-4 is declared effective, TLGY will mail the definitive proxy statement/prospectus to stockholders of

TLGY as of a record date to be established for voting on the Proposed Transaction. TLGY’s stockholders will also be able to obtain a copy of such documents, without charge, by directing a request to: TLGY Acquisition

Corporation, mail@tlgyacquisition.com. These documents, once available, can also be obtained, without charge, at the SEC’s website www.sec.gov.

Participants in the Solicitation

TLGY and its directors and officers may be deemed participants in the solicitation of proxies of TLGY’s shareholders in connection with the Proposed Transaction. Security holders may obtain more detailed information

regarding the names, affiliations, and interests of certain of TLGY’s executive officers and directors in the solicitation by reading TLGY’s final prospectus filed with the SEC on December 3, 2021, and the proxy

statement/prospectus and other relevant materials filed with the SEC in connection with the Proposed Transaction when they become available. Information concerning the interests of TLGY’s participants in the

solicitation, which may, in some cases, be different from those of their shareholders generally, will be set forth in the proxy statement/prospectus relating to the Proposed Transaction when it becomes available. These

documents can be obtained free of charge from the source indicated above. Verde and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the shareholders of TLGY

in connection with the Proposed Transaction. A list of the names of such directors and executive officers and information regarding their interests in the Proposed Transaction will be included in the proxy

statement/prospectus for the Proposed Transaction.

No Offer or Solicitation

Neither the dissemination of this presentation nor any part of its contents is to be taken as any form of commitment on the part of TLGY or Verde or any of their respective affiliates to enter any contract or otherwise create

any legally binding obligation or commitment. This presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase any interests in TLGY or Verde, nor shall it or any

part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contract or commitment or investment decisions relating thereto, nor does it constitute a recommendation regarding the

interests in TLGY or Verde. No securities commission or regulatory authority in the United States or in any other country has in any way opined upon the accuracy or adequacy of this presentation or the materials contained

herein. This presentation is not, and under no circumstances is to be construed as, a prospectus, a public offering or an offering memorandum as defined under applicable securities laws and shall not form the basis of any

contract. |

| INVESTOR PRESENTATION / OCTOBER 2023 5

PLASTIC POLLUTION IS

A GLOBAL PROBLEM

175 countries4

endorsed to

“end plastic pollution”

4.9B Tons

Of plastic disposed of

in landfills or the

environment1

25M Tons

Of plastic textiles

landfilled or

incinerated annually2

1. Zero Waste Europe: The El Dorado of Chemical Recycling, 2019 | 2. Ellen MacArthur Foundation, A new textiles economy: Redesigning fashion’s future, 2017 | 3. W E Forum, Plastics

Europe, 2021 | 4. UN: 175 countries endorsed to end plastic pollution, 2022 | 5. OECD: Plastic pollution is growing relentlessly as waste management and recycling fall short, 2022

400M Tons

Of plastic is

littered around earth’s

crust and oceans3

Where do

plastics go?

9%

Is recycled5

19%

Is incinerated5

50%

Ends up in landfills5 22%

Is in uncontrolled

dumpsites, open pits burns

or terrestrial and aquatic

environments5 |

| INVESTOR PRESENTATION / OCTOBER 2023 6

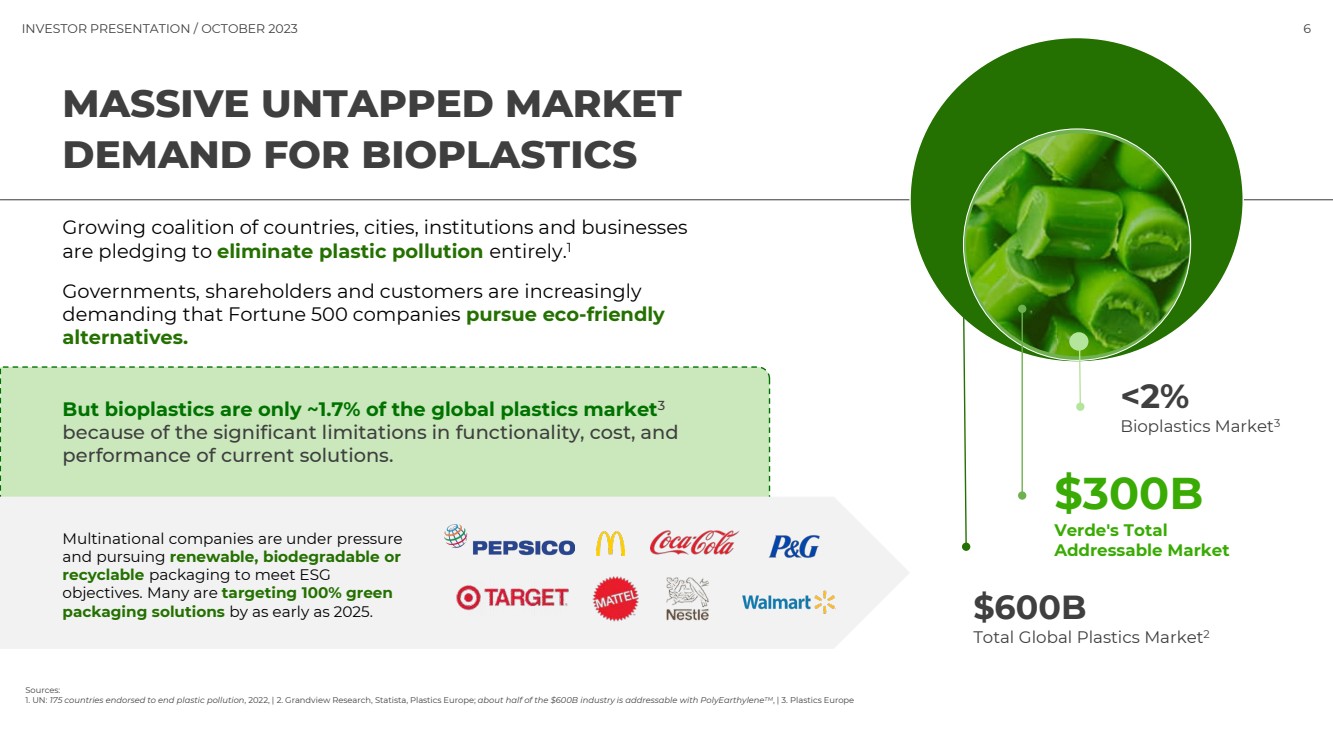

MASSIVE UNTAPPED MARKET

DEMAND FOR BIOPLASTICS

But bioplastics are only ~1.7% of the global plastics market3

because of the significant limitations in functionality, cost, and

performance of current solutions.

Sources:

1. UN: 175 countries endorsed to end plastic pollution, 2022, | 2. Grandview Research, Statista, Plastics Europe; about half of the $600B industry is addressable with PolyEarthyleneTM, | 3. Plastics Europe

$600B

Total Global Plastics Market2

$300B

Verde's Total

Addressable Market

<2%

Bioplastics Market3

Growing coalition of countries, cities, institutions and businesses

are pledging to eliminate plastic pollution entirely.1

Governments, shareholders and customers are increasingly

demanding that Fortune 500 companies pursue eco-friendly

alternatives.

Multinational companies are under pressure

and pursuing renewable, biodegradable or

recyclable packaging to meet ESG

objectives. Many are targeting 100% green

packaging solutions by as early as 2025. |

| INVESTOR PRESENTATION / OCTOBER 2023 7

VERDE BIORESINS

AT A GLANCE

2020

FOUNDED

• A full-service bioplastics company specializing

in the development and manufacturing of

innovative biopolymer resins using its

proprietary plant-based PolyEarthylene™

bioresin (“PEL”)

• State-of-the-art research and development

laboratories and manufacturing facility

capable of producing up to 50 million

pounds of PolyEarthylene™ per year in the

second half of 2024

INVESTOR PRESENTATION / OCTOBER 2021 7

R&D AND MANUFACTURING

IN FULLERTON, CALIFORNIA |

| INVESTOR PRESENTATION / OCTOBER 2023 8

TRANSACTION OVERVIEW

• Verde Bioresins Inc., a pioneer in proprietary biopolymer resins.

• TLGY Acquisition Corp, a SPAC with deep roots in private equity and transformational operations.

• To raise capital for commercial and capacity expansion globally.

Overview

• Pre-money EV of $365 million based on financial outlook and public valuation comps, which

could support a potential valuation range between $300M and $700M.

Valuation1

• $63 million pro forma cash: $78 million TLGY cash in trust less up to $15 million in estimated

transaction expenses, assuming no further redemptions and no PIPE.

• Minimum cash condition: $15 million (termination right with certain cost reimbursement

obligations).

• Non-detachable warrants: 5,750,000 public warrants granted to non-redeeming shareholders.

• Non-detachable warrant exchange right2: the right to exchange them for common at 5:1 ratio

• Interest alignment between public shareholders, Verde, and the Sponsor: significant Sponsor

and Verde economics tied to stock performance of 35% IRR over a 5-year horizon and/or capital

raising.

Other Key Terms

1. Valuation based on referenced industry peer comps for FY24 and FY25 Revenue and EBITDA multiples, which support potential valuation range of $300M to $700M using several multiples (see appendix 1). Peers include NYSE: DNMR, NASDAQ: PCT, and NASDAQ: ORGN | 2. We intend to offer to

shareholders who do not redeem their shares in connection with the closing of an initial business combination the option to receive distributable redeemable warrants, as described in our IPO prospectus, or one share of common stock in lieu of every five of such distributable redeemable warrants. | 3.

Assumes no redemptions by TLGY public shareholders. (3.1) Public Shareholder Ownership includes 7,318,182 Common Shares, it excludes 11,500,000 detachable public warrants and 5,750,000 non-detachable public warrants. The non-detachable public warrants holders are expected to have the right to

convert 5,750,000 at 5:1 warrant units to common share ratio at closing. (3.2) Sponsor ownership excludes 2,750,000 additional common shares to be granted within 4 years from Closing based on achieving the target cash requirement. (3.3) If the combined Company’s stock price achieves an IRR of 35%

over a 5-year horizon, Verde receives up to an additional 36,500,000 shares and the Sponsor an additional 3,000,000 shares.

Verde Share Price $10

Shares Outstanding (M)3 50

Pro Forma Equity Value $496M

Existing Net Debt -

(-) Net Cash to Balance Sheet (63)

Pro Forma Enterprise Value $433M

Estimated Sources & Uses

Sources ($M)

Cash Held in Trust 78

Verde Shareholder Equity Rollover 365

Total Sources of Funds $443M

Uses ($M)

Equity Issued to Verde 365

Estimated Transaction Fees 15

Remaining Cash (Balance Sheet) 63

Total Uses of Funds $443M

Illustrative Pro Forma Valuation (post-money) |

| INVESTOR PRESENTATION / OCTOBER 2023 9

INVESTMENT HIGHLIGHTS

First mover advantage with breakthrough technology –

Verde has developed PolyEarthylene™, a proprietary

bioresin that Verde believes to have the potential to achieve

a full set of environmental1 and industry requirements

capable of significant market adoption.

Large addressable market with unmet needs – the

estimated $600 billion global plastics market is under

regulatory pressure to develop more eco-friendly

solutions, while market penetration of bioplastics is

estimated to be still below 2%.

Strong customer interest – Verde’s solution has the

potential to address approximately 50%1 of the plastics

sector with a wide range of applications (i.e., potential

total addressable market of up to $300 billion), supported

by a distribution partnership with Vinmar and a potential

sales pipeline of over $250 million.

Potential to secure feedstock supplies – strategic

supplier relationship with Braskem is expected to secure

sufficient feedstock to enable Verde to achieve its

expansion plan for most of Year 1 and Year 2.2

Strong unit economics and ROIC – strong margin

business with low operating costs and capital expenditures

expected to deliver operational breakeven, potentially as

early as the beginning of Year 2.2 The unique warrant

structure of TLGY is expected to provide a potential

counterweight to redemption pressure, while having the

potential to generate high returns for existing

shareholders.

Verde's skilled management team and TLGY’s value-add – Verde’s experienced management team, assisted

by TLGY’s deep roots in private equity and operations, is

expected to drive scalable production. TLGY's value-add

includes in-depth due diligence and

attractive transaction terms such as valuation.

01

02

03

04

05

06

Note:

1. Grand View Research, Expert Interviews, Verde, TLGY analysis

2. Year 1 represents the 12 month period from T minus six months (T-6) to T plus six months (T+6), where T is the closing date. For example, if the Proposed Transaction were to close on December 31, 2023 then Year 1 would be between July 1, 2023 to June 30, 2024. |

| INVESTOR PRESENTATION / OCTOBER 2023 10

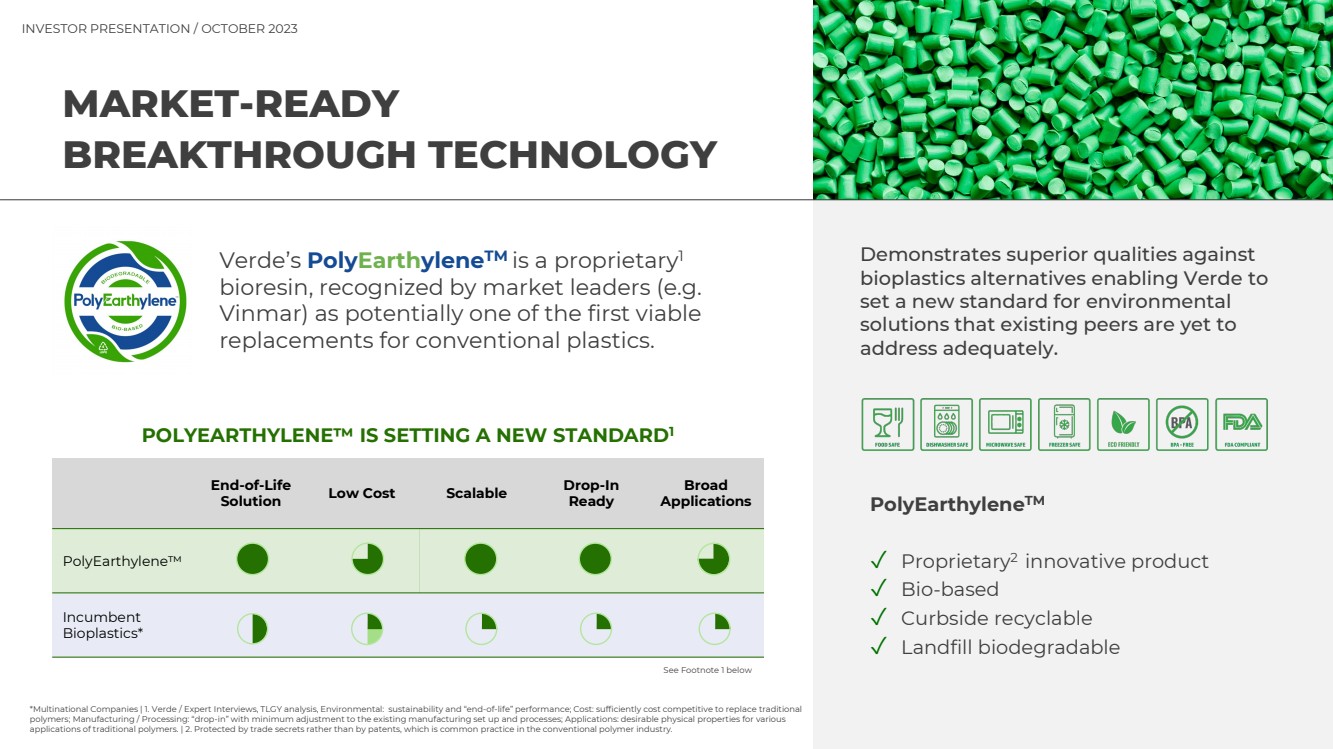

End-of-Life

Solution Low Cost Scalable Drop-In

Ready

Broad

Applications

PolyEarthylene™

Incumbent

Bioplastics*

POLYEARTHYLENE™ IS SETTING A NEW STANDARD1

*Multinational Companies | 1. Verde / Expert Interviews, TLGY analysis, Environmental: sustainability and “end-of-life” performance; Cost: sufficiently cost competitive to replace traditional

polymers; Manufacturing / Processing: “drop-in” with minimum adjustment to the existing manufacturing set up and processes; Applications: desirable physical properties for various

applications of traditional polymers. | 2. Protected by trade secrets rather than by patents, which is common practice in the conventional polymer industry.

MARKET-READY

BREAKTHROUGH TECHNOLOGY

Verde’s PolyEarthyleneTM is a proprietary1

bioresin, recognized by market leaders (e.g.

Vinmar) as potentially one of the first viable

replacements for conventional plastics.

Demonstrates superior qualities against

bioplastics alternatives enabling Verde to

set a new standard for environmental

solutions that existing peers are yet to

address adequately.

PolyEarthyleneTM

✓ Proprietary2 innovative product

✓ Bio-based

✓ Curbside recyclable

✓ Landfill biodegradable See Footnote 1 below |

| INVESTOR PRESENTATION / OCTOBER 2023 11

Source: Verde / Expert Interviews, TLGY analysis

1. Environmental: sustainability and “end-of-life” performance; Cost: sufficiently cost competitive to replace traditional polymers; Manufacturing / Processing: “drop-in” with minimum adjustment to the existing

manufacturing set up and processes; Applications: desirable physical properties for various applications of traditional polymers and wide range of applications. Comparison matrix based on management’s updated view.

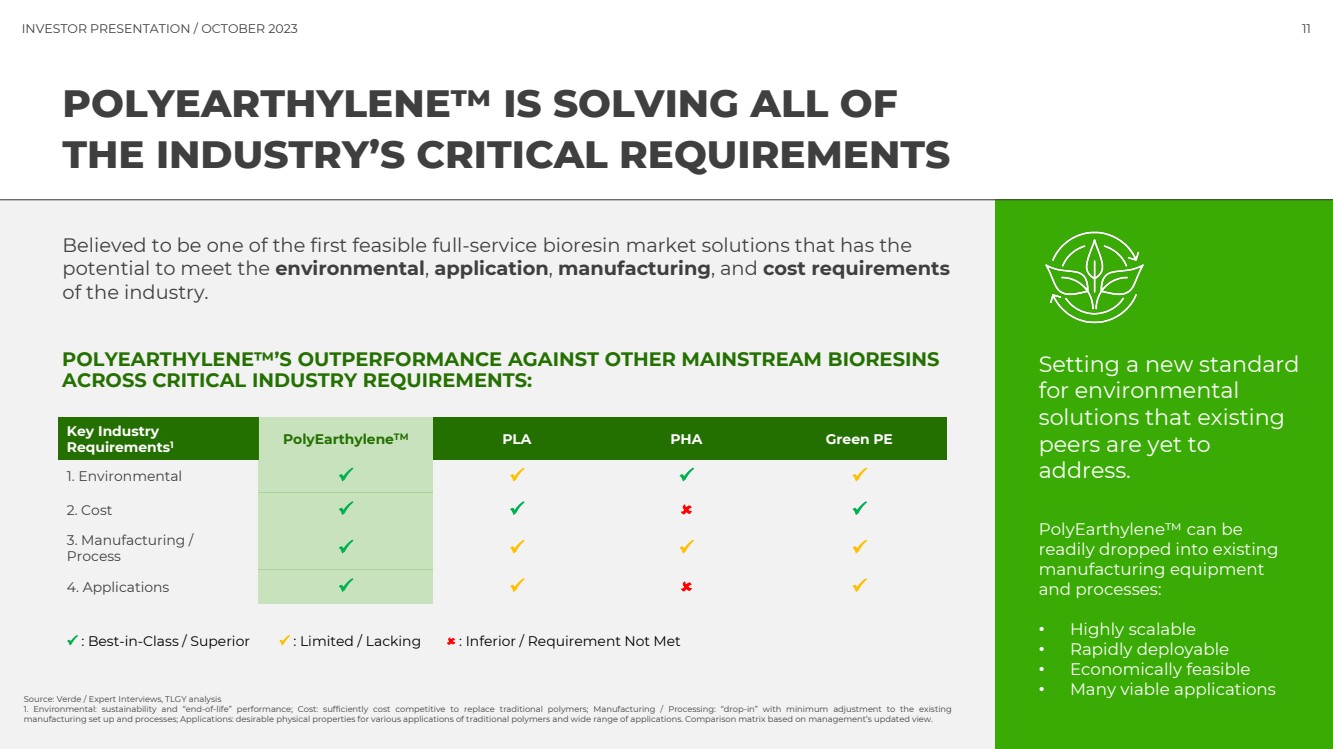

Believed to be one of the first feasible full-service bioresin market solutions that has the

potential to meet the environmental, application, manufacturing, and cost requirements

of the industry.

POLYEARTHYLENE™’S OUTPERFORMANCE AGAINST OTHER MAINSTREAM BIORESINS

ACROSS CRITICAL INDUSTRY REQUIREMENTS:

POLYEARTHYLENE™ IS SOLVING ALL OF

THE INDUSTRY’S CRITICAL REQUIREMENTS

PolyEarthylene™ can be

readily dropped into existing

manufacturing equipment

and processes:

• Highly scalable

• Rapidly deployable

• Economically feasible

• Many viable applications

Setting a new standard

for environmental

solutions that existing

peers are yet to

address.

Key Industry

Requirements1 PolyEarthyleneTM PLA PHA Green PE

1. Environmental

2. Cost

3. Manufacturing /

Process

4. Applications

: Best-in-Class / Superior : Limited / Lacking : Inferior / Requirement Not Met |

| INVESTOR PRESENTATION / OCTOBER 2023 12

LANDFILL BIODEGRADATION

PEL’S STAGES OF USE TO END-OF-LIFE

01

Standard Use

• PolyEarthyleneTM

manufactured and sold to

customer.

• Resin retains standard

polyolefin properties, no

change in performance

following conversion into

product and regular use.

• PEL is shelf-stable and will

not degrade during normal

use or on the shelf.

02

Disposal

• User disposes product.

• If product is not recycled,

then natural microbial

attachment at surface

begins in landfill, industrial

composting facility or by

the side of the road.

• Bacteria create hydrophilic

surface using protein

attachment.

03

Bacteria Formation

• Bacteria coat and colonize

surface in continuous film.

• Bacteria implement

peroxidase and other

enzymes to break polyolefin

bonds at surface.

04

Bacteria Proliferation

• Through chain scission and

oxidation polyolefin chains

are shortened.

• Material softens and

becomes waxy but does not

disintegrate.

• Molecular weight is reduced.

05

End of Life

• Plastic hydrocarbons are

transformed to CO2, water,

methane and biomass.

• Inorganic component

becomes part of the soil.

• No microplastics generated

during process due to a

complete breakdown of

PEL. |

| INVESTOR PRESENTATION / OCTOBER 2023 13

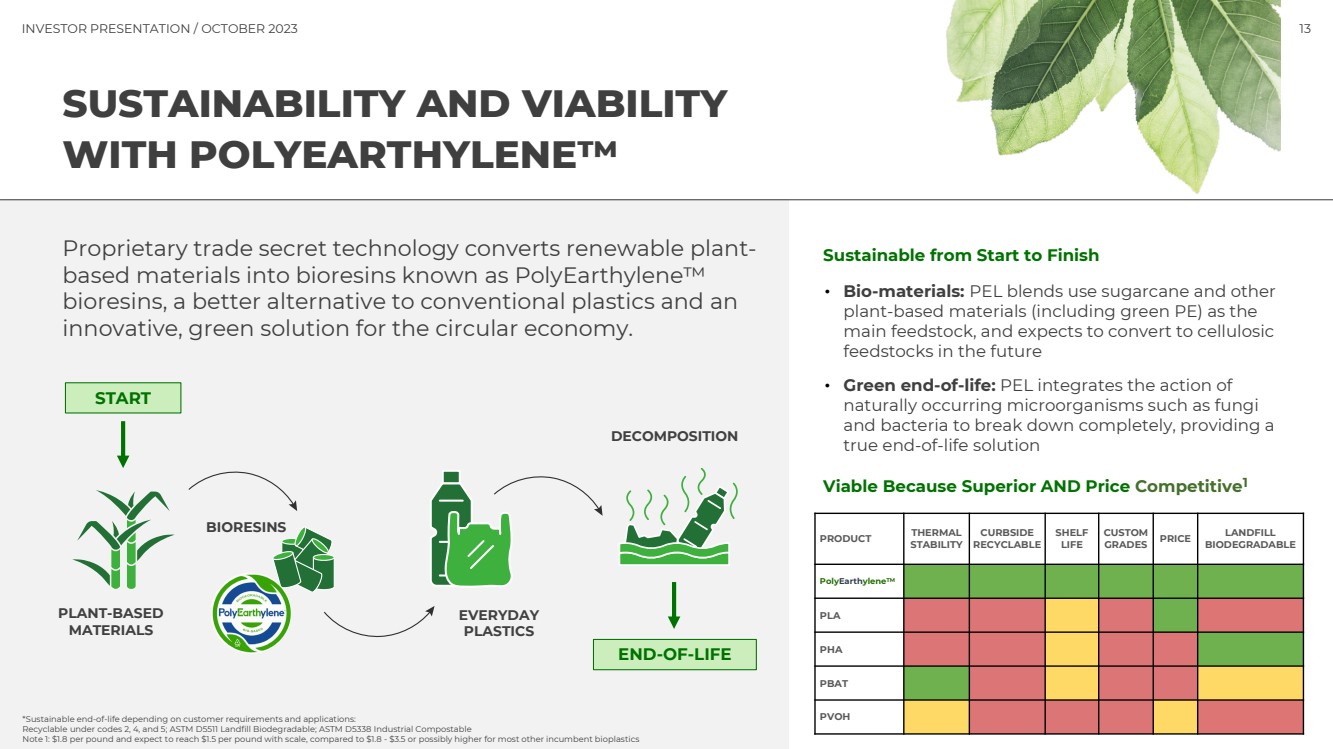

SUSTAINABILITY AND VIABILITY

WITH POLYEARTHYLENE™

Proprietary trade secret technology converts renewable plant-based materials into bioresins known as PolyEarthylene™

bioresins, a better alternative to conventional plastics and an

innovative, green solution for the circular economy.

• Bio-materials: PEL blends use sugarcane and other

plant-based materials (including green PE) as the

main feedstock, and expects to convert to cellulosic

feedstocks in the future

• Green end-of-life: PEL integrates the action of

naturally occurring microorganisms such as fungi

and bacteria to break down completely, providing a

true end-of-life solution

Sustainable from Start to Finish

*Sustainable end-of-life depending on customer requirements and applications:

Recyclable under codes 2, 4, and 5; ASTM D5511 Landfill Biodegradable; ASTM D5338 Industrial Compostable

Note 1: $1.8 per pound and expect to reach $1.5 per pound with scale, compared to $1.8 - $3.5 or possibly higher for most other incumbent bioplastics

Viable Because Superior AND Price Competitive1

PLANT-BASED

MATERIALS

BIORESINS

EVERYDAY

PLASTICS

DECOMPOSITION

START

END-OF-LIFE

PRODUCT THERMAL

STABILITY

CURBSIDE

RECYCLABLE

SHELF

LIFE

CUSTOM

GRADES PRICE LANDFILL

BIODEGRADABLE

PolyEarthyleneTM

PLA

PHA

PBAT

PVOH |

| INVESTOR PRESENTATION / OCTOBER 2023 14

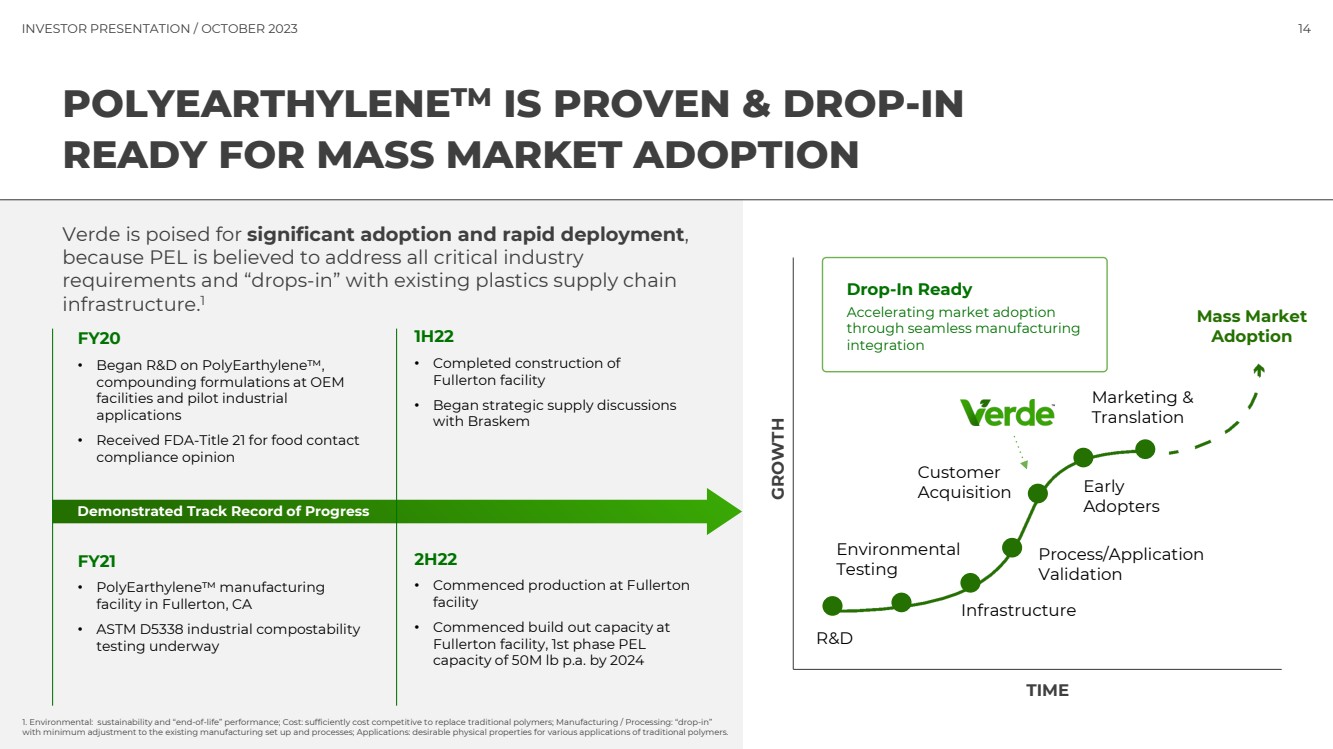

POLYEARTHYLENETM IS PROVEN & DROP-IN

READY FOR MASS MARKET ADOPTION

Drop-In Ready

Accelerating market adoption

through seamless manufacturing

integration

R&D

Mass Market

Adoption

Environmental

Testing

Infrastructure

Process/Application

Validation

Customer

Acquisition Early

Adopters

Marketing &

Translation

TIME

GROWTH

Verde is poised for significant adoption and rapid deployment,

because PEL is believed to address all critical industry

requirements and “drops-in” with existing plastics supply chain

infrastructure.

1

Demonstrated Track Record of Progress

FY20

• Began R&D on PolyEarthylene™,

compounding formulations at OEM

facilities and pilot industrial

applications

• Received FDA-Title 21 for food contact

compliance opinion

FY21

• PolyEarthylene™ manufacturing

facility in Fullerton, CA

• ASTM D5338 industrial compostability

testing underway

1H22

• Completed construction of

Fullerton facility

• Began strategic supply discussions

with Braskem

2H22

• Commenced production at Fullerton

facility

• Commenced build out capacity at

Fullerton facility, 1st phase PEL

capacity of 50M lb p.a. by 2024

1. Environmental: sustainability and “end-of-life” performance; Cost: sufficiently cost competitive to replace traditional polymers; Manufacturing / Processing: “drop-in”

with minimum adjustment to the existing manufacturing set up and processes; Applications: desirable physical properties for various applications of traditional polymers. |

| INVESTOR PRESENTATION / OCTOBER 2023 INVESTOR PRESENTATION / OCTOBER 2021 15

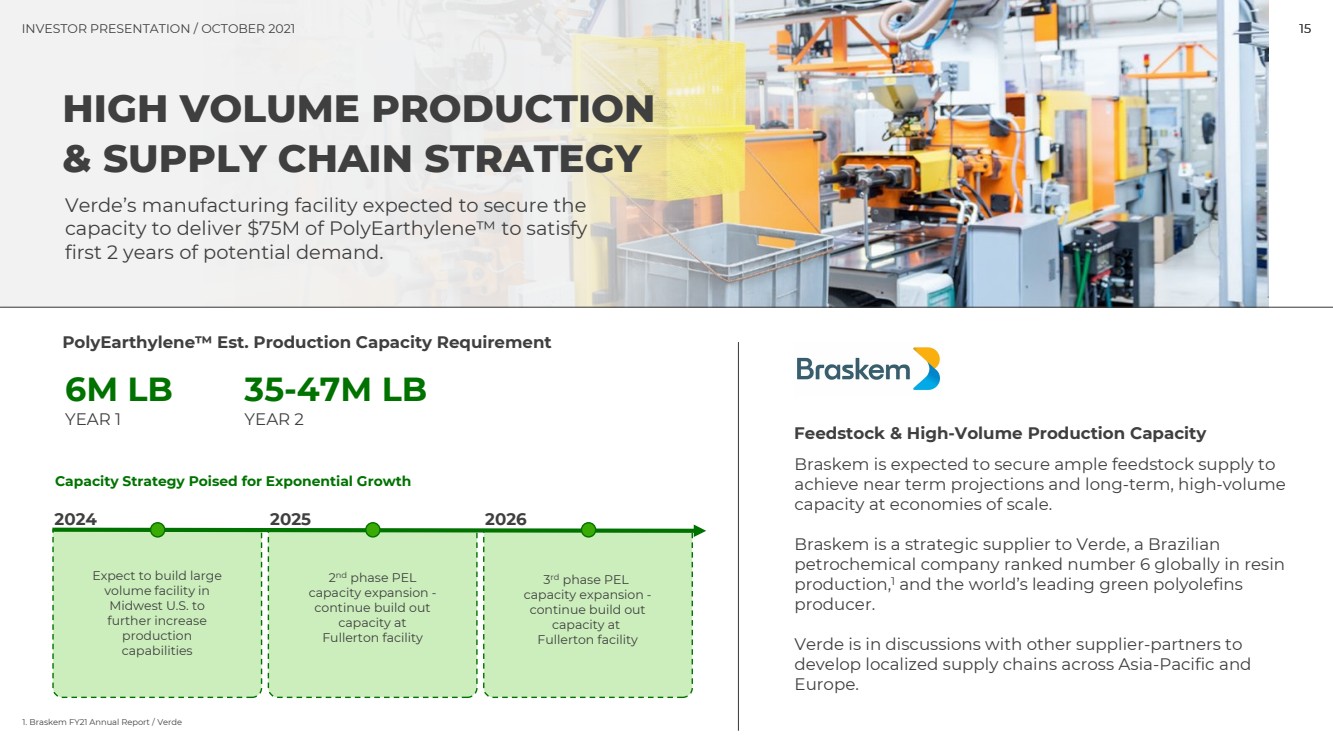

HIGH VOLUME PRODUCTION

& SUPPLY CHAIN STRATEGY

Verde’s manufacturing facility expected to secure the

capacity to deliver $75M of PolyEarthylene™ to satisfy

first 2 years of potential demand.

Braskem is expected to secure ample feedstock supply to

achieve near term projections and long-term, high-volume

capacity at economies of scale.

Braskem is a strategic supplier to Verde, a Brazilian

petrochemical company ranked number 6 globally in resin

production,1 and the world’s leading green polyolefins

producer.

Verde is in discussions with other supplier-partners to

develop localized supply chains across Asia-Pacific and

Europe.

Feedstock & High-Volume Production Capacity

Capacity Strategy Poised for Exponential Growth

2024 2026

Expect to build large

volume facility in

Midwest U.S. to

further increase

production

capabilities

2nd phase PEL

capacity expansion -

continue build out

capacity at

Fullerton facility

3rd phase PEL

capacity expansion -

continue build out

capacity at

Fullerton facility

PolyEarthylene™ Est. Production Capacity Requirement

6M LB

YEAR 1

35-47M LB

YEAR 2

1. Braskem FY21 Annual Report / Verde

2025 |

| INVESTOR PRESENTATION / OCTOBER 2023 16

Formulations capable of meeting high industrial

performance requirements for durable goods and other

advanced applications such as rigid packaging

Demonstrated shelf-life stability

Customizable to achieve a specific set of physical

and mechanical performance goals for single-use

applications to durable goods

Capable of injection moulding, extrusion coating,

extruded and blown film, blow molding, thermoform

and other applications

Available in electrostatic dissipative grades and

antistatic grades

Has the ability to handle high processing

temperature consistent with petro-polymers

HIGH PERFORMANCE POLYEARTHYLENE™ FOR

A WIDE RANGE OF TRADITIONAL PLASTICS

APPLICATIONS

PolyEarthylene™ bioresins outperform most bio-based materials in many common applications and is a high-performance alternative to a wide variety of petroleum-based plastics. |

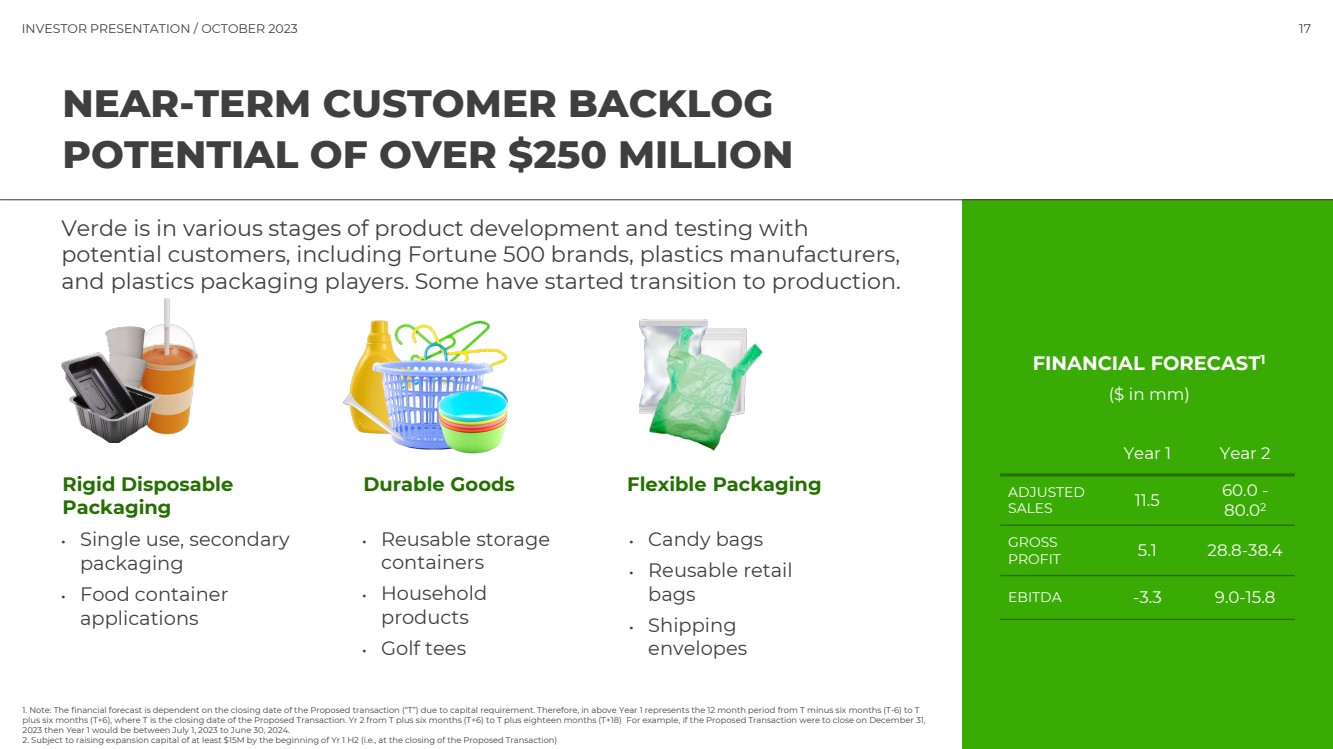

| INVESTOR PRESENTATION / OCTOBER 2023 17

Year 1 Year 2

ADJUSTED

SALES 11.5 60.0 -

80.02

GROSS

PROFIT 5.1 28.8-38.4

EBITDA -3.3 9.0-15.8

FINANCIAL FORECAST1

($ in mm)

NEAR-TERM CUSTOMER BACKLOG

POTENTIAL OF OVER $250 MILLION

Verde is in various stages of product development and testing with

potential customers, including Fortune 500 brands, plastics manufacturers,

and plastics packaging players. Some have started transition to production.

• Single use, secondary

packaging

• Food container

applications

Rigid Disposable

Packaging

• Reusable storage

containers

• Household

products

• Golf tees

Durable Goods Flexible Packaging

• Candy bags

• Reusable retail

bags

• Shipping

envelopes

1. Note: The financial forecast is dependent on the closing date of the Proposed transaction (“T”) due to capital requirement. Therefore, in above Year 1 represents the 12 month period from T minus six months (T-6) to T

plus six months (T+6), where T is the closing date of the Proposed Transaction. Yr 2 from T plus six months (T+6) to T plus eighteen months (T+18) For example, if the Proposed Transaction were to close on December 31,

2023 then Year 1 would be between July 1, 2023 to June 30, 2024.

2. Subject to raising expansion capital of at least $15M by the beginning of Yr 1 H2 (i.e., at the closing of the Proposed Transaction) |

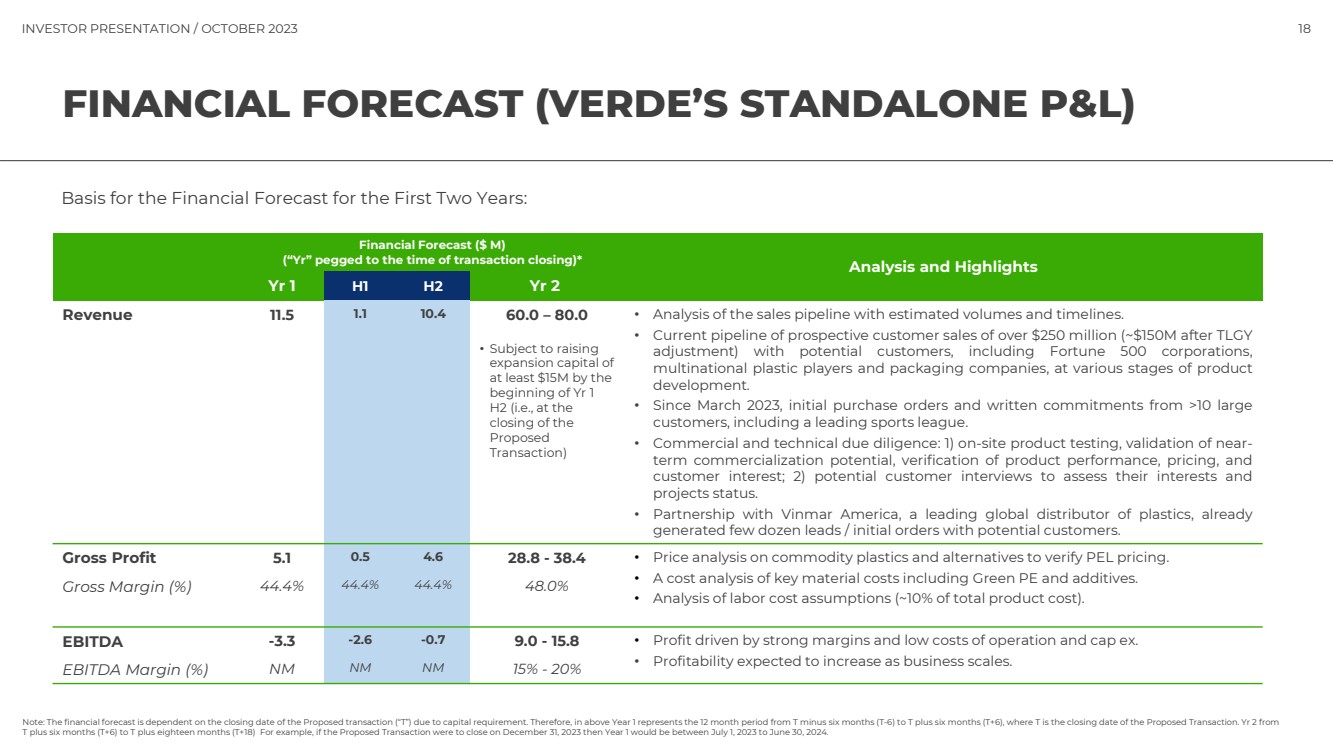

| INVESTOR PRESENTATION / OCTOBER 2023 18

FINANCIAL FORECAST (VERDE’S STANDALONE P&L)

Financial Forecast ($ M)

(“Yr” pegged to the time of transaction closing)* Analysis and Highlights

Yr 1 H1 H2 Yr 2

Revenue 11.5 1.1 10.4 60.0 – 80.0

• Subject to raising

expansion capital of

at least $15M by the

beginning of Yr 1

H2 (i.e., at the

closing of the

Proposed

Transaction)

• Analysis of the sales pipeline with estimated volumes and timelines.

• Current pipeline of prospective customer sales of over $250 million (~$150M after TLGY

adjustment) with potential customers, including Fortune 500 corporations,

multinational plastic players and packaging companies, at various stages of product

development.

• Since March 2023, initial purchase orders and written commitments from >10 large

customers, including a leading sports league.

• Commercial and technical due diligence: 1) on-site product testing, validation of near-term commercialization potential, verification of product performance, pricing, and

customer interest; 2) potential customer interviews to assess their interests and

projects status.

• Partnership with Vinmar America, a leading global distributor of plastics, already

generated few dozen leads / initial orders with potential customers.

Gross Profit 5.1 0.5 4.6 28.8 - 38.4 • Price analysis on commodity plastics and alternatives to verify PEL pricing.

• A cost analysis of key material costs including Green PE and additives.

• Analysis of labor cost assumptions (~10% of total product cost). Gross Margin (%) 44.4% 44.4% 44.4% 48.0%

EBITDA -3.3 -2.6 -0.7 9.0 - 15.8 • Profit driven by strong margins and low costs of operation and cap ex.

• Profitability expected to increase as business scales. EBITDA Margin (%) NM NM NM 15% - 20%

Note: The financial forecast is dependent on the closing date of the Proposed transaction (“T”) due to capital requirement. Therefore, in above Year 1 represents the 12 month period from T minus six months (T-6) to T plus six months (T+6), where T is the closing date of the Proposed Transaction. Yr 2 from

T plus six months (T+6) to T plus eighteen months (T+18) For example, if the Proposed Transaction were to close on December 31, 2023 then Year 1 would be between July 1, 2023 to June 30, 2024.

Basis for the Financial Forecast for the First Two Years: |

| INVESTOR PRESENTATION / OCTOBER 2023 19

STRATEGIC PARTNERSHIPS

VALIDATE EXPANSION PATHWAY

+

Strategic partnership with Vinmar Polymers America, a

division of Vinmar International, a leading global distributor of

plastics, expected to expand reach of the PolyEarthyleneTM

product line to a diverse range of potential customers from

various industries:

• Can accelerate the market penetration of PolyEarthylene™

through its established distribution network

• Able to support the development and service of PolyEarthylene™,

providing end-users with a reliable alternative to existing plastic

products

• Global reach in North America, South America, Europe, and Asia

• Generated leads and initial orders with dozens of potential

customers through partnership |

| INVESTOR PRESENTATION / OCTOBER 2023 20

LEADERSHIP TEAM WITH STRONG INDUSTRY

EXPERIENCE AND DEEP TECHNICAL CAPABILITY

Terry Retin

Senior Director, Sales

• 15+ years leading

global partnerships

strategy

• Shapes customer

engagement,

retention strategies

• Market and

business

intelligence lead

Joseph Paolucci

CEO

• 40 years of

Petrochemical

Business

Development

leadership

• Commodity & resin

engineering

expertise

• JV Management:

Phillips Petroleum,

Ineos, Groupo Idessa

Yvonne Soulliere

Director of

Engineering

• Oversees R&D and

project engineering

• Expertise in full-cycle

product engineering

• Led model

engineering, tooling

development and

quality control for

mass manufacturing

Brian Gordon

Chairman/President/

COO

• 20+ years C-level

experience:

multinational, VC/PE

• IBM, Merck & Co.

roots

• Extensive M&A, JV,

licensing, leasing,

capital raising

transactions

Gary Metzger

Chief Sustainability

Officer

• 40+ years in polymer

industry

• Executive roles at

Amco International,

Inc. (Ravago) &

President/CEO of

Amco Plastics

Materials, Inc.

• Led recycled and bio-based polymer

application R&D

Jin-Goon Kim

Founder, Chairman &

CEO of TLGY

Chairman of the

Merged Company

• 20+ years in private

equity, CEO

• Former Partner at

TPG Capital

• $40B value creation.

#1 auto platform,

China sportswear.

Awarded TPG CEO,

Man of the Year

Christopher Rankin,

Ph.D.

Head of R&D

• 15+ years of experience

in materials science,

engineering, and

polymers

• Specialized in

photochemistry of

ferroelectric polymer

and polyvinylidene

fluoride

• Holds several patents

related to water-repellant and abrasion-resistant coatings |

| INVESTOR PRESENTATION / OCTOBER 2023 21

TLGY OVERVIEW

AND VALUE-ADD

TLGY Differentiation

Led by Jin-Goon Kim, a serial transformational CEO of market

leading companies and a former Partner at TPG Capital with

over $40 billion in value-creation track record.

• Address root causes of SPAC challenges – inflated valuation

and/or low quality of targets that increase redemption.

- Private equity approach in due diligence and value

creation

- Disruptive business with high growth potential as a

successful investment

- Lower valuation with earnouts at high IRR hurdles

- Innovative SPAC structure to encourage roll-over

investments and mitigate redemptions.

• A team of executives, advisors, and investors with proven track

record of building and running market leaders expected to

assist the company’s growth as public market leader post-DeSPAC.

On-site testing of PEL in a third-party factory.

Product Testing and Market Validation

TLGY advisor conducted:

✓ On-site testing and development in advanced applications

(blown film and extrusion coating)

✓ Validation of value proposition with Asia distributors and

prospective customers

✓ Validation of value proposition with key participants at an

industry conference

Confirmation of PolyEarthyleneTM's superior value proposition across

the four key criteria:

1) Environmental

2) Cost

3) Manufacturing / Processing

4)Applications |

| INVESTOR PRESENTATION / OCTOBER 2023 22

UNIQUE SPAC STRUCTURE

• $10/share transaction closing

price potentially represents a

fair value based on peer comps

• Structural innovation with fixed

pool of warrants and exchange

for common mechanism

creates upside potential and

downside protection

• Potentially sufficient incentive

to buy shares in the open

market before the DeSPAC

completes

• Naturally embedded multiplier

quickly escalates upside and

downside protection if

redemption rises

DOWNSIDE PROTECTION IF PRICE DECLINES

CAPTURE UPSIDE IF PRICE RISES

POST-DESPAC (Illustrative price scenarios with 90% redemption)

$26

$39

$51

$64

$77

$10

$30

$50

$70

$90

$10 $15 $20 $25 $30

Potential Unredeemed Share Value

Illustrative Common Share Price Scenarios

$6.1

$4.2

$2.6

$0.0

$5.0

$10.0

Cost Basis per Share

1.8

2.6

4.1

0.0

5.0

Total Shares per Common

Implied Redemption 80% 90% 95%

INCENTIVES TO INVEST AND/OR NOT REDEEM

PRE-DESPAC (illustrative redemption scenarios)

Cost per share declines as redemption rate increases

Value of one unredeemed share expected to increase faster than one common

share price (potentially 2.6 x faster)

Downside protection if common share price drops below the cost basis (assumed $10.90)

due to higher expected value of one unredeemed share

Receive more shares as redemption rate increases

If redemption 90%

These are for illustrative purposes only and may not be reflective of actual performance. For more information, view Appendix slides 2 and 3

$26

$21

$15

$10

$5

Cost basis

$0

$5

$10

$15

$20

$25

$30

$10 $8 $6 $4 $2

Potential Unredeemed Share Value

Illustrative Common Share Price Scenarios |

| : TLGY INVESTOR PRESENTATION / OCTOBER 2023

APPENDIX |

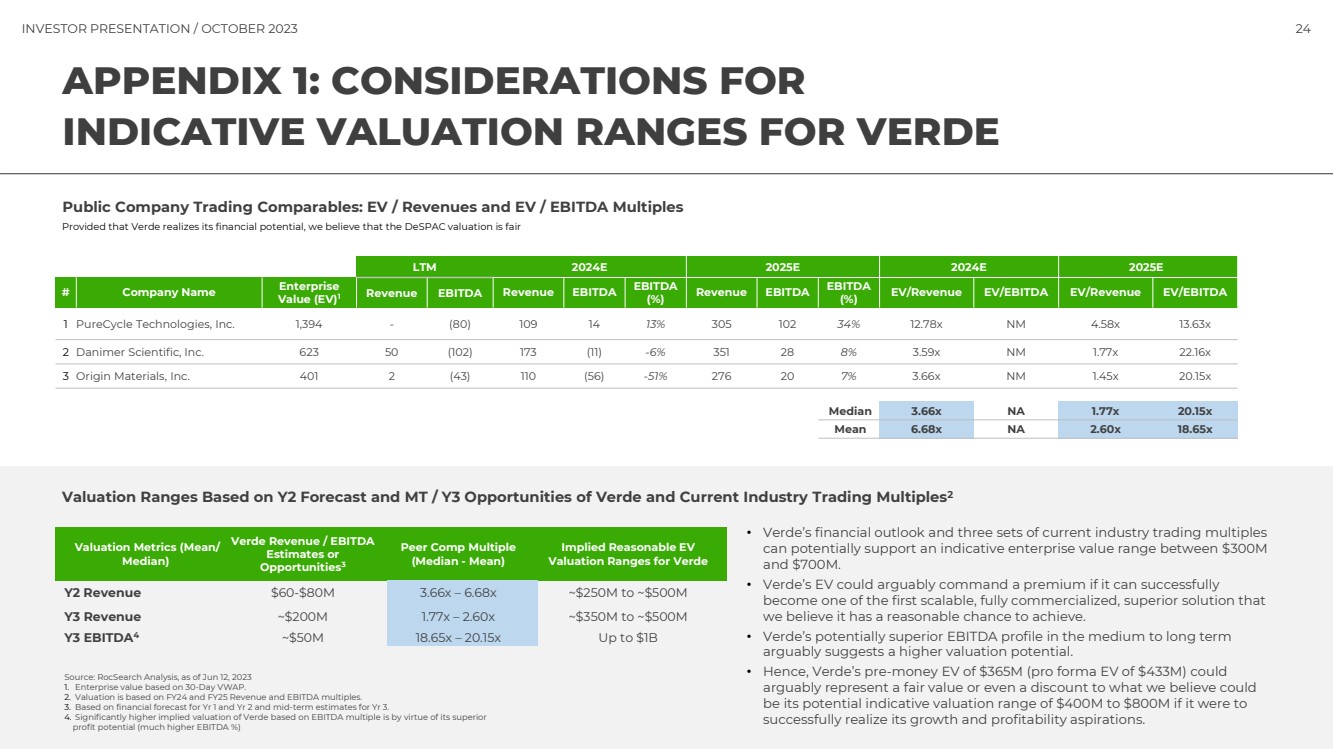

| INVESTOR PRESENTATION / OCTOBER 2023 24

APPENDIX 1: CONSIDERATIONS FOR

INDICATIVE VALUATION RANGES FOR VERDE

LTM 2024E 2025E 2024E 2025E

# Company Name Enterprise

Value (EV)1 Revenue EBITDA Revenue EBITDA EBITDA

(%) Revenue EBITDA EBITDA

(%) EV/Revenue EV/EBITDA EV/Revenue EV/EBITDA

1 PureCycle Technologies, Inc. 1,394 - (80) 109 14 13% 305 102 34% 12.78x NM 4.58x 13.63x

2 Danimer Scientific, Inc. 623 50 (102) 173 (11) -6% 351 28 8% 3.59x NM 1.77x 22.16x

3 Origin Materials, Inc. 401 2 (43) 110 (56) -51% 276 20 7% 3.66x NM 1.45x 20.15x

Median 3.66x NA 1.77x 20.15x

Mean 6.68x NA 2.60x 18.65x

Provided that Verde realizes its financial potential, we believe that the DeSPAC valuation is fair

Public Company Trading Comparables: EV / Revenues and EV / EBITDA Multiples

Valuation Ranges Based on Y2 Forecast and MT / Y3 Opportunities of Verde and Current Industry Trading Multiples2

Valuation Metrics (Mean/

Median)

Verde Revenue / EBITDA

Estimates or

Opportunities3

Peer Comp Multiple

(Median - Mean)

Implied Reasonable EV

Valuation Ranges for Verde

Y2 Revenue $60-$80M 3.66x – 6.68x ~$250M to ~$500M

Y3 Revenue ~$200M 1.77x – 2.60x ~$350M to ~$500M

Y3 EBITDA4 ~$50M 18.65x – 20.15x Up to $1B

Source: RocSearch Analysis, as of Jun 12, 2023

1. Enterprise value based on 30-Day VWAP.

2. Valuation is based on FY24 and FY25 Revenue and EBITDA multiples.

3. Based on financial forecast for Yr 1 and Yr 2 and mid-term estimates for Yr 3.

4. Significantly higher implied valuation of Verde based on EBITDA multiple is by virtue of its superior

profit potential (much higher EBITDA %)

• Verde’s financial outlook and three sets of current industry trading multiples

can potentially support an indicative enterprise value range between $300M

and $700M.

• Verde’s EV could arguably command a premium if it can successfully

become one of the first scalable, fully commercialized, superior solution that

we believe it has a reasonable chance to achieve.

• Verde’s potentially superior EBITDA profile in the medium to long term

arguably suggests a higher valuation potential.

• Hence, Verde’s pre-money EV of $365M (pro forma EV of $433M) could

arguably represent a fair value or even a discount to what we believe could

be its potential indicative valuation range of $400M to $800M if it were to

successfully realize its growth and profitability aspirations. |

| INVESTOR PRESENTATION / OCTOBER 2023 25

APPENDIX 2: NON-REDEEMING SHAREHOLDER

SCENARIOS BASED ON REDEMPTIONS

Redemptions (% of total trust cash) 0% 50% 75% 80% 90% 95%

Total Common Shares & Warrants of Public Shareholders

Number of TLGY Common Shares Post-Redemption 7,318,182 3,659,091 1,829,546 1,463,636 731,818 365,909

Number of TLGY Detachable Public Warrants 11,500,000 11,500,000 11,500,000 11,500,000 11,500,000 11,500,000

Number of TLGY Non-Detachable Public Warrants 5,750,000 5,750,000 5,750,000 5,750,000 5,750,000 5,750,000

Economics per One Common Share held by Non-Redeemed Public Shareholders

(Excluding 0.5 detachable warrant, which does not have a right for the warrant holder to be converted to Common Shares at DeSPAC)

One Common Share 1.00 1.00 1.00 1.00 1.00 1.00

Number of TLGY Non-Detachable Public Warrants per One Common Share 0.79 1.57 3.14 3.93 7.86 15.71

Preemptive Warrant Conversion: The non-redeeming public shareholders are expected to be given a right to convert the Non-Detachable Public Warrants to Common

Shares at a ratio of 5 to 1

Warrant to Common Share Conversion Ratio of Non-Detachable Warrants at

Closing 5.0x 5.0x 5.0x 5.0x 5.0x 5.0x

Number of Common Shares Converted from Non-Detachable Warrants at

Closing 0.16 0.31 0.63 0.79 1.57 3.14

Total Implied Total Common Shares for Each Unredeemed Common Share

Post-DeSPAC (Conversion to be rounded off to whole units) 1.16 1.31 1.63 1.79 2.57 4.14

Indicative Value of One Unredeemed Common Share Post-DeSPAC

(fixed at $10.9/share1

; value would fluctuate based on actual price) $12.6 $14.4 $17.8 $19.5 $28.0 $45.1

Note 1: Trading price for a common share close to closing (also close to redemption date) is likely to be around or higher than the redeeming value of trust cash at closing, which is expected to be around $10.9 per share by Q4; trading around $10.9 per share in mid-September.

Potentially higher common shareholding for non-redeeming shareholders as redemption rates increase. |

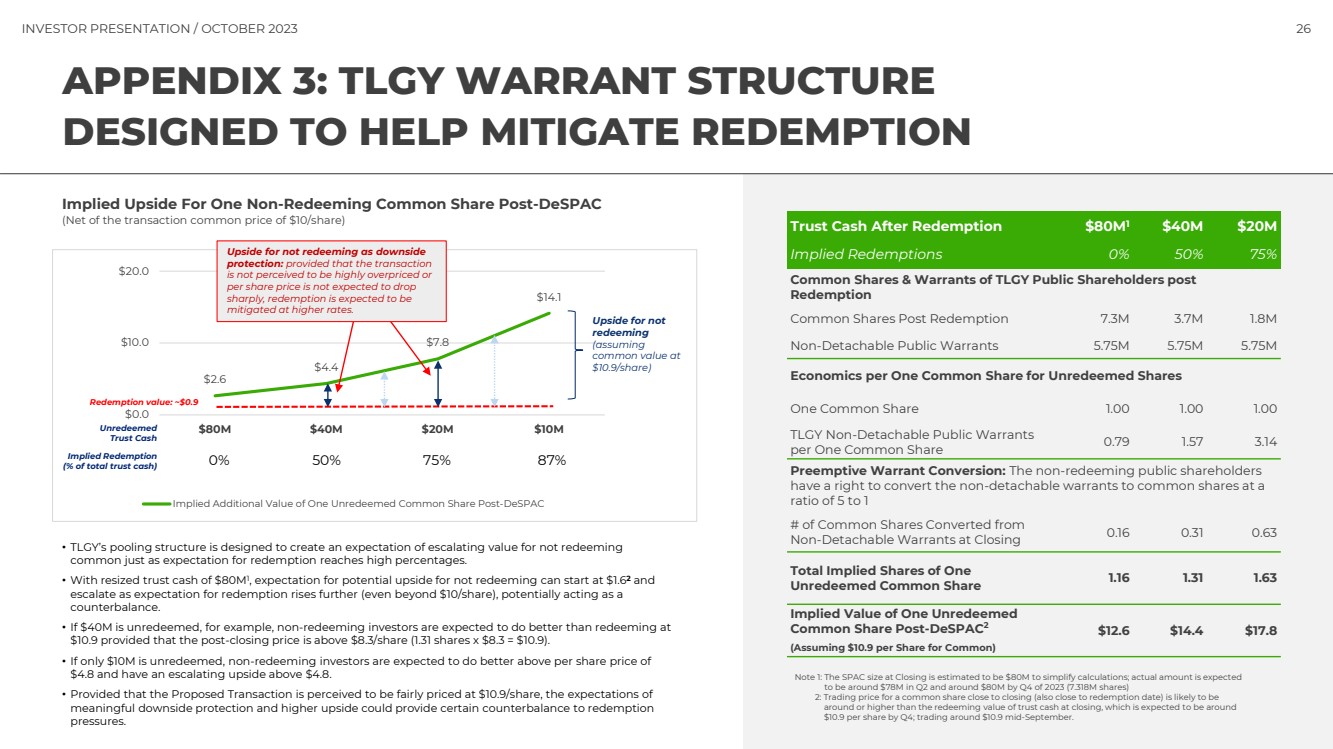

| INVESTOR PRESENTATION / OCTOBER 2023 26

APPENDIX 3: TLGY WARRANT STRUCTURE

DESIGNED TO HELP MITIGATE REDEMPTION

• TLGY’s pooling structure is designed to create an expectation of escalating value for not redeeming

common just as expectation for redemption reaches high percentages.

• With resized trust cash of $80M1

, expectation for potential upside for not redeeming can start at $1.62 and

escalate as expectation for redemption rises further (even beyond $10/share), potentially acting as a

counterbalance.

• If $40M is unredeemed, for example, non-redeeming investors are expected to do better than redeeming at

$10.9 provided that the post-closing price is above $8.3/share (1.31 shares x $8.3 = $10.9).

• If only $10M is unredeemed, non-redeeming investors are expected to do better above per share price of

$4.8 and have an escalating upside above $4.8.

• Provided that the Proposed Transaction is perceived to be fairly priced at $10.9/share, the expectations of

meaningful downside protection and higher upside could provide certain counterbalance to redemption

pressures.

Trust Cash After Redemption $80M1 $40M $20M

Implied Redemptions 0% 50% 75%

Common Shares & Warrants of TLGY Public Shareholders post

Redemption

Common Shares Post Redemption 7.3M 3.7M 1.8M

Non-Detachable Public Warrants 5.75M 5.75M 5.75M

Economics per One Common Share for Unredeemed Shares

One Common Share 1.00 1.00 1.00

TLGY Non-Detachable Public Warrants

per One Common Share 0.79 1.57 3.14

Preemptive Warrant Conversion: The non-redeeming public shareholders

have a right to convert the non-detachable warrants to common shares at a

ratio of 5 to 1

# of Common Shares Converted from

Non-Detachable Warrants at Closing 0.16 0.31 0.63

Total Implied Shares of One

Unredeemed Common Share 1.16 1.31 1.63

Implied Value of One Unredeemed

Common Share Post-DeSPAC2

(Assuming $10.9 per Share for Common)

$12.6 $14.4 $17.8

Note 1: The SPAC size at Closing is estimated to be $80M to simplify calculations; actual amount is expected

to be around $78M in Q2 and around $80M by Q4 of 2023 (7.318M shares)

2: Trading price for a common share close to closing (also close to redemption date) is likely to be

around or higher than the redeeming value of trust cash at closing, which is expected to be around

$10.9 per share by Q4; trading around $10.9 mid-September.

Implied Upside For One Non-Redeeming Common Share Post-DeSPAC

(Net of the transaction common price of $10/share)

$2.6

$4.4

$7.8

$14.1

$0.0

$10.0

$20.0

$80M $40M $20M $10M

Implied Additional Value of One Unredeemed Common Share Post-DeSPAC

Implied Redemption

(% of total trust cash) 0% 50% 75% 87%

Unredeemed

Trust Cash

Redemption value: ~$0.9

Upside for not

redeeming

(assuming

common value at

$10.9/share)

Upside for not redeeming as downside

protection: provided that the transaction

is not perceived to be highly overpriced or

per share price is not expected to drop

sharply, redemption is expected to be

mitigated at higher rates. |

| INVESTOR PRESENTATION / OCTOBER 2023 27

RISK FACTORS RELATED TO VERDE

Verde’s business is subject to numerous risks, including but not limited to the following:

• Verde is an early-stage company with a history of losses, and its future profitability is uncertain.

• To date, Verde has not generated any revenues from product sales.

• Verde’s operating results may fluctuate significantly as a result of a variety of factors, many of which are outside of its control.

• Verde’s business is not diversified.

• Verde may be unable to manage growth effectively.

• Verde will need to secure additional funding and may be unable to raise additional capital on favorable terms, if at all.

• Changes in tax laws may adversely affect Verde or its investors.

• Construction of Verde’s manufacturing facilities may not be completed in the expected timeframe or in a cost-effective manner. Any delays in the construction of Verde’s manufacturing facilities could severely impact

its business, financial condition, results of operations and prospects.

• Initially, Verde will rely on a single facility for all of its operations.

• Verde may be delayed in or unable to procure necessary capital equipment.

• Verde has not produced its products in commercial quantities.

• Verde expects to rely on a limited number of customers for a significant portion of its near-term revenue.

• Verde may be unable to obtain certifications required by its prospective customers.

• Verde’s products may not achieve market success. If Verde’s products do not achieve market success, it may be unable to generate significant revenues, if at all.

• Verde faces and will face substantial competition.

• Verde produces biopolymer products from raw materials, including renewable resources, whose pricing and availability may be impacted by factors out of its control. Increases or fluctuations in the costs of Verde’s raw

materials may affect its cost structure.

• Verde’s success will be influenced by the price of petroleum relative to the price of bio-based feedstocks.

• The failure of Verde’s raw material suppliers to perform their obligations under supply agreements, or Verde’s inability to replace or renew these agreements when they expire, could increase Verde’s cost for these

materials, interrupt production or otherwise adversely affect its results of operations.

• Maintenance, expansion and refurbishment of Verde’s facilities, the construction of new facilities and the development and implementation of new manufacturing processes involve significant risks.

• Verde may not be successful in finding future strategic partners for continuing development of additional feedstock opportunities or tolling and downstream conversion of Verde’s products.

• Verde may rely heavily on future collaborative and supply chain partners.

• Compliance with extension environmental, health and safety laws could require material expenditures, changes in Verde’s operations or site remediation.

• Verde’s operating plan may require it to source feedstock and supplies internationally, and foreign currency exchange rate fluctuations and changes to international trade agreements, tariffs, import and excise duties,

taxes or other governmental rules and regulations could adversely affect Verde’s business, financial condition, results of operations and prospects.

• Verde’s business could suffer form negative publicity and other adverse consequences with recent civil and criminal charges brought against Terren Peizer, Verde’s former Executive Chairman; and Founder and

Chairman of Humanitario Capital, LLC. Verde’s largest stockholder, by the Securities Exchange Commission and the United States Department of Justice.

• From time to time, Verde may be involved in litigation, regulatory actions or government investigations and inquiries, which could have an adverse impact on Verde’s profitability and consolidated financial position.

• If Verde experiences a significant disruption in its information technology systems, including security breaches, or if it fails to implement new systems and software successfully, its business operations and financial

condition could be adversely affected.

• Verde may not be able to protect adequately its intellectual property assets, which could adversely affect its competitive position and reduce the value of its products, and litigation to protect its intellectual property

could be costly.

• Third parties may claim that Verde infringes on their proprietary rights and may prevent Verde from commercializing and selling its products.

• Verde relies in part on trade secrets to protect its technology, and its failure to obtain or maintain trade secret protection could limit its ability to compete.

• Verde’s management has limited experience operating as a public company.

• Verde depends on its teams, and Verde’s business would suffer if it fails to retain its key personnel and attract additional highly skilled employees.

• If the Proposed Transaction’s benefits do not meet the expectations of investors or securities analysts or for other reasons the market price of TLGY’s securities or, following the Proposed Transaction, the combined

company’s securities, may decline.

• If, following the Proposed Transaction, securities or industry analysts do not public research or reports about the combined company, or if they issue unfavorable or inaccurate research regarding its business, its share

price and trading volume could decline.

• Following the Proposed Transaction, the combined company will incur increased costs as a result of operating as a public company, and its management will be required to devote substantial time to new compliance

initiatives and corporate governance practices. |

| INVESTOR PRESENTATION / OCTOBER 2023 28

KEY RISKS RELATED TO THE TRANSACTION AND TLGY

TLGY is subject to numerous risks, including but not limited to:

• TLGY’s Initial Shareholders have entered into the Acquiror Support Agreement with TLGY and Verde to vote in favor of the Transaction, regardless of how TLGY’s public shareholders vote.

• Neither the TLGY Board nor any committee thereof obtained a third-party valuation or fairness opinion in determining whether or not to pursue the Transaction.

• Since TLGY’s Initial Shareholders, directors and executive officers have interests that are different, or in addition to (and which may conflict with), the interests of its shareholders, a conflict of interest may have existed in

determining whether the Transaction with Verde is appropriate as TLGY’s initial business combination. Such interests include that TLGY’s Initial Shareholders, directors and executive officers, will lose their entire

investment in TLGY if the initial business combination is not completed.

• If the conditions to closing contained in the Merger Agreement are not met or waived, the Transaction may not occur. TLGY may change or waive one or more of the terms of, or conditions to, the Transaction, and the

exercise of TLGY’s directors’ and executive officers’ discretion in agreeing to such changes may result in a conflict of interest when determining whether such changes to the terms of the Transaction or waivers of

conditions are appropriate and in TLGY’s shareholders’ best interest.

• TLGY will not have any right to make damage claims against Verde for the breach of any representation, warranty or covenant made by Verde in the Merger Agreement.

• The consummation of the Transaction is subject to compliance with the HSR Act, and, if certain conditions are not satisfied or waived, the Transaction may not be completed.

• The Transaction may be completed even though material adverse effects may result from the announcement of the Transaction, industry-wide changes and other causes.

• The merged company after the closing of the Transaction with Verde (“Verde PubCo”) may issue additional shares of Verde PubCo Common Stock or other equity securities without your approval, which would dilute

your ownership interests and may depress the market price of your shares.

• Verde’s financial forecasts, which were presented to the TLGY Board and are included in this proxy statement/prospectus, may not prove accurate.

• The Sponsor is liable to ensure that proceeds of the Trust Account are not reduced by vendor claims in the event an initial business combination is not consummated. The Sponsor has also agreed to pay for any

liquidation expenses if an initial business combination is not consummated. Such liability may have influenced the Sponsor’s decision to pursue the Transaction.

• TLGY and Verde have incurred and expect to incur significant transaction costs in connection with the Transaction.

• Past performance by TLGY and by its management team may not be indicative of future performance of an investment in TLGY or Verde PubCo.

• The loss of any member or change in structure of Verde’s senior management team could adversely affect its business.

• TLGY’s Existing Governing Documents waive the doctrine of corporate opportunity.

• Activities taken by existing TLGY shareholders to increase the likelihood of approval of the Transaction Proposal and the other proposals described in this proxy statement/prospectus could have a depressive effect on

TLGY’s securities.

• Because Verde is not conducting an underwritten public offering of its securities, no underwriter has conducted due diligence of Verde’s business, operations or financial condition or reviewed the disclosure in this

proxy statement/prospectus.

• The SEC has recently issued proposed rules relating to certain activities of SPACs. Certain of the procedures that TLGY, a potential business combination target, or others may determine to undertake in connection with

such proposals may increase TLGY’s costs and the time needed to complete its initial business combination and may constrain the circumstances under which TLGY could complete an initial business combination. The

need for compliance with the SPAC Rule Proposals may cause us to liquidate the funds in the Trust Account or liquidate the Company at an earlier time than we might otherwise choose.

• If we are deemed to be an investment company for purposes of the Investment Company Act, we would be required to institute burdensome compliance requirements and our activities would be severely restricted. As

a result, in such circumstances, unless we are able to modify our activities so that we would not be deemed an investment company, we would expect to abandon our efforts to complete an initial business combination

and instead to liquidate the Company.

• Changes in laws or regulations, or a failure to comply with any laws and regulations, may adversely affect TLGY’s business, including its ability to negotiate and complete its initial business combination, and results of

operations.

• To mitigate the risk that TLGY might be deemed to be an investment company for purposes of the Investment Company Act, TLGY may, at any time, instruct the trustee to liquidate the securities held in the Trust

Account and instead instruct the trustee to hold the funds in the Trust Account in cash until the earlier of the consummation of TLGY’s initial business combination or its liquidation. As a result, following the liquidation

of securities in the Trust Account, TLGY would likely receive minimal interest, if any, on the funds held in the Trust Account, which would reduce the dollar amount the public shareholders would receive upon any

redemption or liquidation of the Company.

• Subsequent to the consummation of the Business Combination, Verde PubCo may be required to take write-downs or write-offs, restructuring and impairment or other charges that could have a significant negative

effect on its financial condition, results of operations and the share price of its securities, which could cause you to lose some or all of your investment.

• TLGY may be targeted by securities actions and derivative suits that could result in substantial costs and may delay or prevent the consummation of the Transaction.

• TLGY’s independent registered public accounting firm’s report for TLGY contains an explanatory paragraph that expresses substantial doubt about its ability to continue as a “going concern.”

• Verde PubCo will incur increased costs as a result of being a public company.

• TLGY’s shareholders who do not redeem their public shares will have a reduced ownership and voting interest after the Transaction and will exercise less influence over management.

• Verde PubCo’s future success depends in part on recruiting and retaining key personnel. The loss of key personnel or the hiring of ineffective personnel after the Transaction could negatively impact the operations and

profitability of Verde PubCo. |

| INVESTOR PRESENTATION / OCTOBER 2023 29

KEY RISKS RELATED TO THE TRANSACTION AND TLGY

(CONTINUED)

TLGY is subject to numerous risks, including but not limited to:

• The unaudited pro forma financial information included elsewhere in this proxy statement/prospectus may not be indicative of what Verde PubCo’s actual financial position or results of operations would have been.

• The ability of TLGY’s public shareholders to exercise redemption rights with respect to a large number of its public shares may not allow it to complete the Transaction or optimize the capital structure of Verde PubCo

and may increase the probability that the Transaction would be unsuccessful and that you will have to wait for liquidation in order to redeem your shares.

• TLGY’s Initial Shareholders, as well as Verde, TLGY’s directors, executive officers, advisors and their respective affiliates may elect to purchase public shares prior to the consummation of the Transaction, which may

influence the vote on the Transaction and reduce the public “float” of its Class A ordinary shares.

• If our Initial Shareholders, officers, directors or their affiliates elect to purchase public shares from public shareholders, such purchases may affect the market price of TLGY’s securities.

• If third parties bring claims against TLGY, the proceeds held in the Trust Account could be reduced and the per share redemption amount received by shareholders may be less than $10.00 per share (which was the

offering price in its initial public offering).

• TLGY’s directors may decide not to enforce the indemnification obligations of the Sponsor, resulting in a reduction in the amount of funds in the Trust Account available for distribution to the public stockholders.

• TLGY may not have sufficient funds to satisfy indemnification claims of its directors and executive officers.

• In the event TLGY distributes the proceeds in the Trust Account to its public shareholders and subsequently files a bankruptcy petition or an involuntary bankruptcy petition is filed against TLGY that is not dismissed, a

bankruptcy court may seek to recover such proceeds, and TLGY and the TLGY Board may be exposed to claims of punitive damages.

• If, before distributing the proceeds in the Trust Account to TLGY’s public shareholders, TLGY files a bankruptcy petition or an involuntary bankruptcy petition is filed against TLGY that is not dismissed, the claims of

creditors in such proceeding may have priority over the claims of its shareholders and the per share amount that would otherwise be received by its shareholders in connection with its liquidation may be reduced.

• TLGY’s shareholders may be held liable for claims by third parties against TLGY to the extent of distributions received by them upon redemption of their shares.

• TLGY is and Verde PubCo will be an emerging growth company and a smaller reporting company within the meaning of the Securities Act, and if Verde PubCo takes advantage of certain exemptions from disclosure

requirements available to “emerging growth companies” or “smaller reporting companies,” this could make its securities less attractive to investors and may make it more difficult to compare its performance with other

public companies.

• Compliance obligations under the Sarbanes-Oxley Act may make it more difficult for TLGY to effectuate the Transaction, require substantial financial and management resources and increase the time and costs of

completing a business combination.

• A significant portion of TLGY’s total outstanding shares are restricted from immediate resale but may be sold into the market in the near future. This could cause the market price of Verde PubCo Common Stock to

drop significantly, even if Verde PubCo’s business is doing well.

• Verde PubCo’s directors, executive officers and principal stockholders will continue to have substantial control over Verde PubCo’s company after the consummation of the Transaction, which could limit Verde PubCo’s

ability to influence the outcome of key transactions, including a change of control.

• Humanitario Capital, LLC., Verde’s principal stockholder, beneficially owns greater than 50% of Verde’s outstanding shares of common stock and is expected to own greater than 50% of Verde PubCo Common Stock

following the consummation of the Transaction which will cause Verde PubCo to be deemed a “controlled company” under the rules of Nasdaq.

• The public shareholders may experience immediate dilution as a consequence of the issuance of Verde PubCo Common Stock as consideration in the Transaction.

• Warrants will become exercisable for Verde PubCo Common Stock, which, if exercised, would increase the number of shares eligible for future resale in the public market and result in dilution to its shareholders.

• Even if the Transaction is consummated the terms of the warrants may be amended in a manner adverse to a holder if holders of at least 50% of the then outstanding public warrants approve of such amendment.

• Verde PubCo may redeem a warrant holder’s unexpired warrants prior to their exercise at a time that may be disadvantageous to such warrant holder, thereby making its warrants worthless.

• A warrant holder may only be able to exercise its public warrants on a “cashless basis” under certain circumstances, and if a warrant holder does so, such warrant holder will receive fewer Verde PubCo Common Stock

from such exercise than if a warrant holder were to exercise such warrants for cash.

• Even if we consummate the Transaction, there can be no assurance that our public warrants will be in the money at the time they become exercisable, and they may expire worthless.

• If you elect to exercise your redemption rights with respect to your Class A ordinary shares, you will be deemed to have tendered your contingent right to receive distributable redeemable warrants for no additional

consideration, and as a result, will not receive any distributable redeemable warrants in respect of such redeemed public shares.

• If the amount of Class A ordinary shares redeemed by shareholders is low, shareholders who choose not to redeem their shares may only receive a small amount of distributable redeemable warrants.

• TLGY’s warrant agreement designates the courts of the State of New York or the United States District Court for the Southern District of New York as the sole and exclusive forum for certain types of actions and

proceedings that may be initiated by holders of its warrants, which could limit the ability of warrant holders to obtain a favorable judicial forum for disputes with TLGY.

• Nasdaq may not list Verde PubCo’s securities on its exchange, which could limit investors’ ability to make transactions in Verde PubCo’s securities and subject Verde PubCo to additional trading restrictions.

• An active, liquid trading market for Verde PubCo’s securities may not develop, which may limit your ability to sell such securities. |

| INVESTOR PRESENTATION / OCTOBER 2023 30

KEY RISKS RELATED TO THE TRANSACTION AND TLGY

(CONTINUED)

TLGY is subject to numerous risks, including but not limited to:

• Reports published by analysts, including projections in those reports that differ from Verde PubCo’s actual results, could adversely affect the price and trading volume of its common shares.

• Verde PubCo may fail to meet Verde PubCo’s publicly announced guidance or other expectations about Verde PubCo’s business, which would cause Verde PubCo’s stock price to decline.

• Verde PubCo does not intend to pay cash dividends for the foreseeable future.

• Because Verde PubCo does not anticipate paying any cash dividends on its capital stock in the foreseeable future, capital appreciation, if any, will be your sole source of gain.

• TLGY is subject to, and Verde PubCo will be subject to, changing law and regulations regarding regulatory matters, corporate governance and public disclosure that have increased both TLGY’s costs and the risk of non-compliance and will increase both Verde PubCo’s costs and the risk of non-compliance.

• During the pendency of the Transaction, TLGY will not be able to solicit, initiate or take any action to facilitate or encourage any inquiries or the making, submission or announcement of, or enter into a Transaction with

another party because of restrictions in the Merger Agreement. Furthermore, certain provisions of the Merger Agreement will discourage third parties from submitting alternative takeover proposals, including

proposals that may be superior to the arrangements contemplated by the Merger Agreement.

• Recent increases in inflation and interest rates in the United States and elsewhere could make it more difficult for TLGY to consummate the Transaction.

• Military conflict in Ukraine or elsewhere may lead to increased volatility for publicly traded securities, which could make it more difficult for us to consummate an initial business combination.

• Verde PubCo’s business and operations could be negatively affected if it becomes subject to any securities litigation or stockholder activism, which could cause Verde PubCo to incur significant expense, hinder

execution of business and growth strategy and impact its stock price.

• Verde PubCo will need, but may be unable to obtain, funding following the consummation of the Transaction on satisfactory terms, which could dilute Verde PubCo’s stockholders and investors, or impose burdensome

financial restrictions on its business.

Risks Related to the Domestication

• The Domestication may result in adverse tax consequences for holders of TLGY Class A Ordinary Shares and TLGY public warrants, including holders exercising their redemption rights with respect to the TLGY Common

Stock (such term to be used throughout this section “Risks Related to the Domestication” as such term is used in the section entitled “Material U.S. Federal Income Tax Considerations”).

• Verde PubCo could be subject to changes in tax rates or the adoption of new tax legislation, whether in or out of the United States, or could otherwise have exposure to additional tax liabilities, which could harm its

business.

• Upon consummation of the Transaction, the rights of holders of Verde PubCo Common Stock arising under the DGCL as well as the Proposed Governing Documents will differ from and may be less favorable to the

rights of holders of public shares arising under Cayman Islands Companies Law as well as the Existing Governing Documents.

• Delaware law and Verde PubCo’s Proposed Governing Documents contain certain provisions, including anti-takeover provisions, that limit the ability of stockholders to take certain actions and could delay or discourage

takeover attempts that stockholders may consider favorable.