| 2727

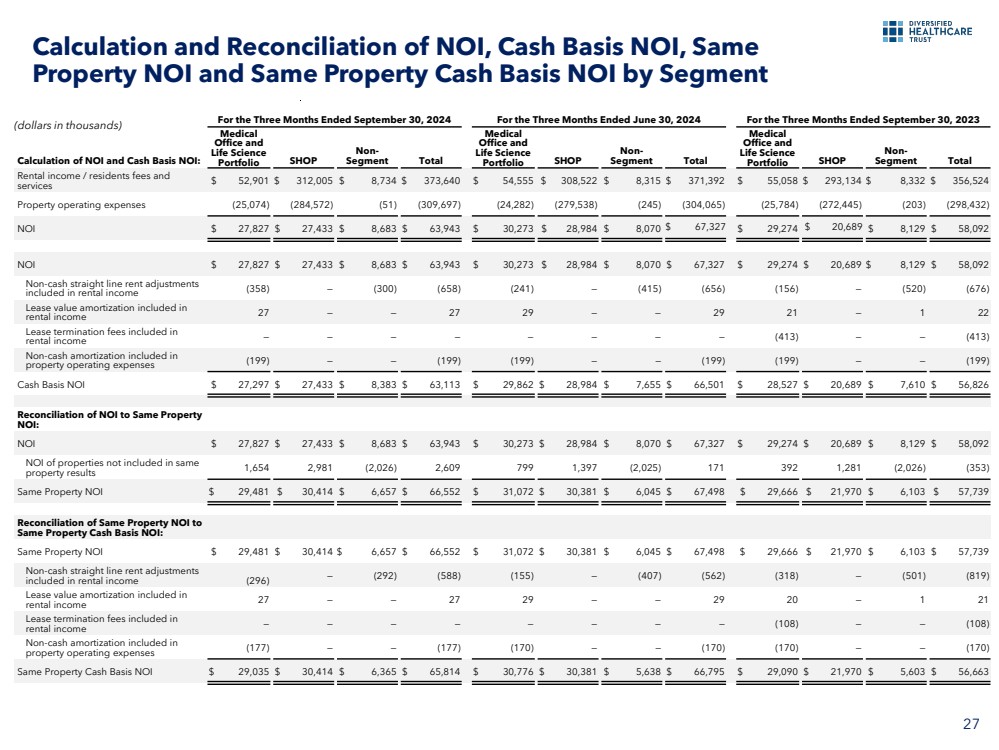

(dollars in thousands)

Calculation and Reconciliation of NOI, Cash Basis NOI, Same

Property NOI and Same Property Cash Basis NOI by Segment

For the Three Months Ended September 30, 2024 For the Three Months Ended June 30, 2024 For the Three Months Ended September 30, 2023

Calculation of NOI and Cash Basis NOI:

Medical

Office and

Life Science

Portfolio SHOP

Non-Segment Total

Medical

Office and

Life Science

Portfolio SHOP

Non-Segment Total

Medical

Office and

Life Science

Portfolio SHOP

Non-Segment Total

Rental income / residents fees and

services $ 52,901 $ 312,005 $ 8,734 $ 373,640 $ 54,555 $ 308,522 $ 8,315 $ 371,392 $ 55,058 $ 293,134 $ 8,332 $ 356,524

Property operating expenses (25,074) (284,572) (51) (309,697) (24,282) (279,538) (245) (304,065) (25,784) (272,445) (203) (298,432)

NOI $ 27,827 $ 27,433 $ 8,683 $ 63,943 $ 30,273 $ 28,984 $ 8,070 $ 67,327 $ 29,274 $ 20,689 $ 8,129 $ 58,092

NOI $ 27,827 $ 27,433 $ 8,683 $ 63,943 $ 30,273 $ 28,984 $ 8,070 $ 67,327 $ 29,274 $ 20,689 $ 8,129 $ 58,092

Non-cash straight line rent adjustments

included in rental income (358) — (300) (658) (241) — (415) (656) (156) — (520) (676)

Lease value amortization included in

rental income 27 — — 27 29 — — 29 21 — 1 22

Lease termination fees included in

rental income — — — — — — — — (413) — — (413)

Non-cash amortization included in

property operating expenses (199) — — (199) (199) — — (199) (199) — — (199)

Cash Basis NOI $ 27,297 $ 27,433 $ 8,383 $ 63,113 $ 29,862 $ 28,984 $ 7,655 $ 66,501 $ 28,527 $ 20,689 $ 7,610 $ 56,826

Reconciliation of NOI to Same Property

NOI:

NOI $ 27,827 $ 27,433 $ 8,683 $ 63,943 $ 30,273 $ 28,984 $ 8,070 $ 67,327 $ 29,274 $ 20,689 $ 8,129 $ 58,092

NOI of properties not included in same

property results 1,654 2,981 (2,026) 2,609 799 1,397 (2,025) 171 392 1,281 (2,026) (353)

Same Property NOI $ 29,481 $ 30,414 $ 6,657 $ 66,552 $ 31,072 $ 30,381 $ 6,045 $ 67,498 $ 29,666 $ 21,970 $ 6,103 $ 57,739

Reconciliation of Same Property NOI to

Same Property Cash Basis NOI:

Same Property NOI $ 29,481 $ 30,414 $ 6,657 $ 66,552 $ 31,072 $ 30,381 $ 6,045 $ 67,498 $ 29,666 $ 21,970 $ 6,103 $ 57,739

Non-cash straight line rent adjustments

included in rental income (296) — (292) (588) (155) — (407) (562) (318) — (501) (819)

Lease value amortization included in

rental income 27 — — 27 29 — — 29 20 — 1 21

Lease termination fees included in

rental income — — — — — — — — (108) — — (108)

Non-cash amortization included in

property operating expenses (177) — — (177) (170) — — (170) (170) — — (170)

Same Property Cash Basis NOI $ 29,035 $ 30,414 $ 6,365 $ 65,814 $ 30,776 $ 30,381 $ 5,638 $ 66,795 $ 29,090 $ 21,970 $ 5,603 $ 56,663 |