0001171838

false

FY

http://fasb.org/us-gaap/2023#RelatedPartyMember

http://fasb.org/us-gaap/2023#RelatedPartyMember

P5Y

P3Y

0001171838

2022-04-01

2023-03-31

0001171838

2023-06-29

0001171838

2022-09-30

0001171838

2023-03-31

0001171838

2022-03-31

0001171838

us-gaap:NonrelatedPartyMember

2023-03-31

0001171838

us-gaap:NonrelatedPartyMember

2022-03-31

0001171838

us-gaap:RelatedPartyMember

2023-03-31

0001171838

us-gaap:RelatedPartyMember

2022-03-31

0001171838

2021-04-01

2022-03-31

0001171838

us-gaap:CommonStockMember

2021-03-31

0001171838

us-gaap:AdditionalPaidInCapitalMember

2021-03-31

0001171838

us-gaap:RetainedEarningsMember

2021-03-31

0001171838

2021-03-31

0001171838

us-gaap:CommonStockMember

2022-03-31

0001171838

us-gaap:AdditionalPaidInCapitalMember

2022-03-31

0001171838

us-gaap:RetainedEarningsMember

2022-03-31

0001171838

us-gaap:CommonStockMember

2021-04-01

2022-03-31

0001171838

us-gaap:AdditionalPaidInCapitalMember

2021-04-01

2022-03-31

0001171838

us-gaap:RetainedEarningsMember

2021-04-01

2022-03-31

0001171838

us-gaap:CommonStockMember

2022-04-01

2023-03-31

0001171838

us-gaap:AdditionalPaidInCapitalMember

2022-04-01

2023-03-31

0001171838

us-gaap:RetainedEarningsMember

2022-04-01

2023-03-31

0001171838

us-gaap:CommonStockMember

2023-03-31

0001171838

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001171838

us-gaap:RetainedEarningsMember

2023-03-31

0001171838

SUND:ConsultingAgreementMember

2022-01-01

2022-01-02

0001171838

SUND:ConsultingAgreementMember

srt:MaximumMember

2022-01-01

2022-01-02

0001171838

SUND:ConsultingAgreementMember

srt:MinimumMember

2022-01-01

2022-01-02

0001171838

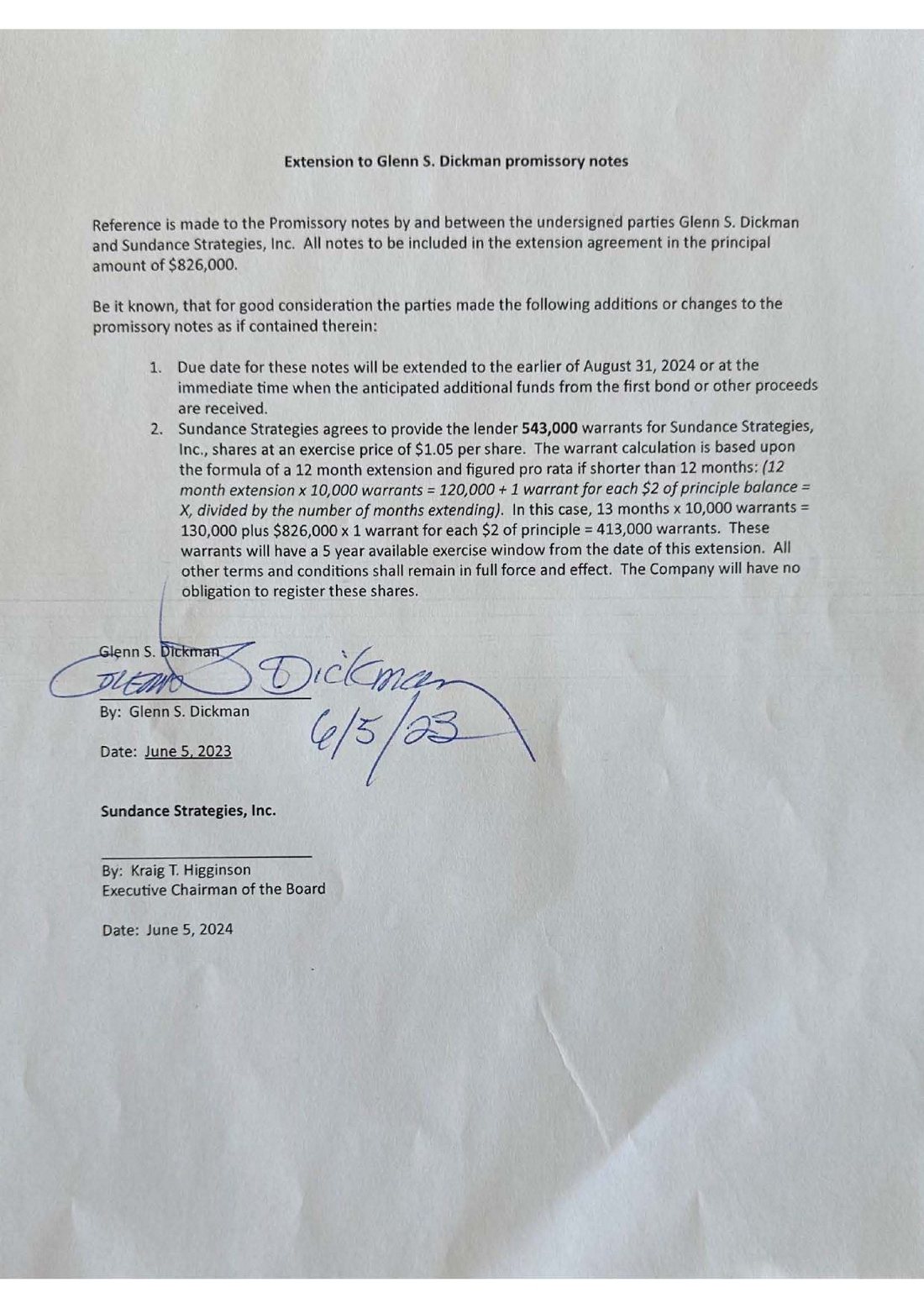

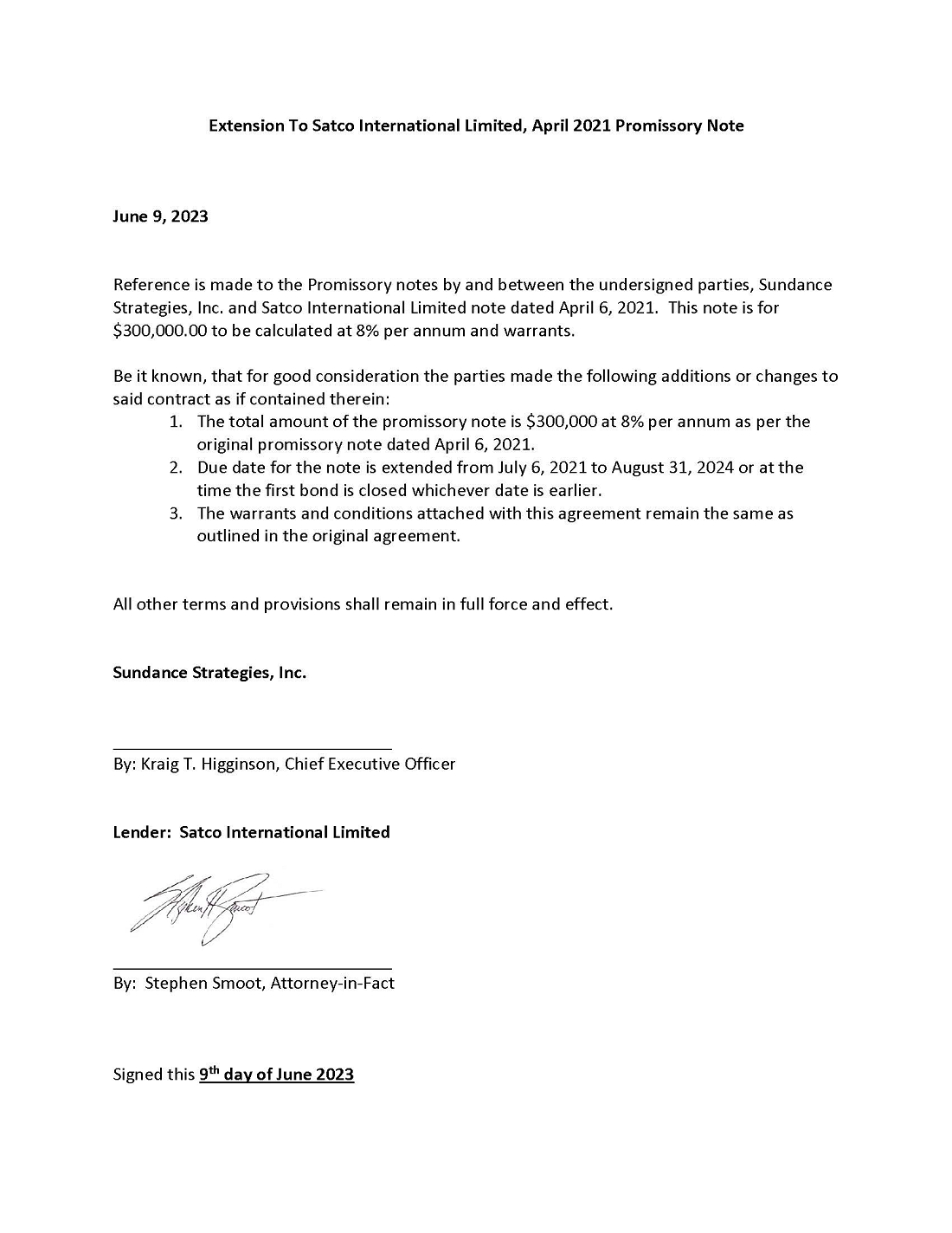

SUND:UnsecuredPromissoryNoteMember

2021-04-06

0001171838

SUND:UnsecuredPromissoryNoteMember

2022-01-06

2022-01-06

0001171838

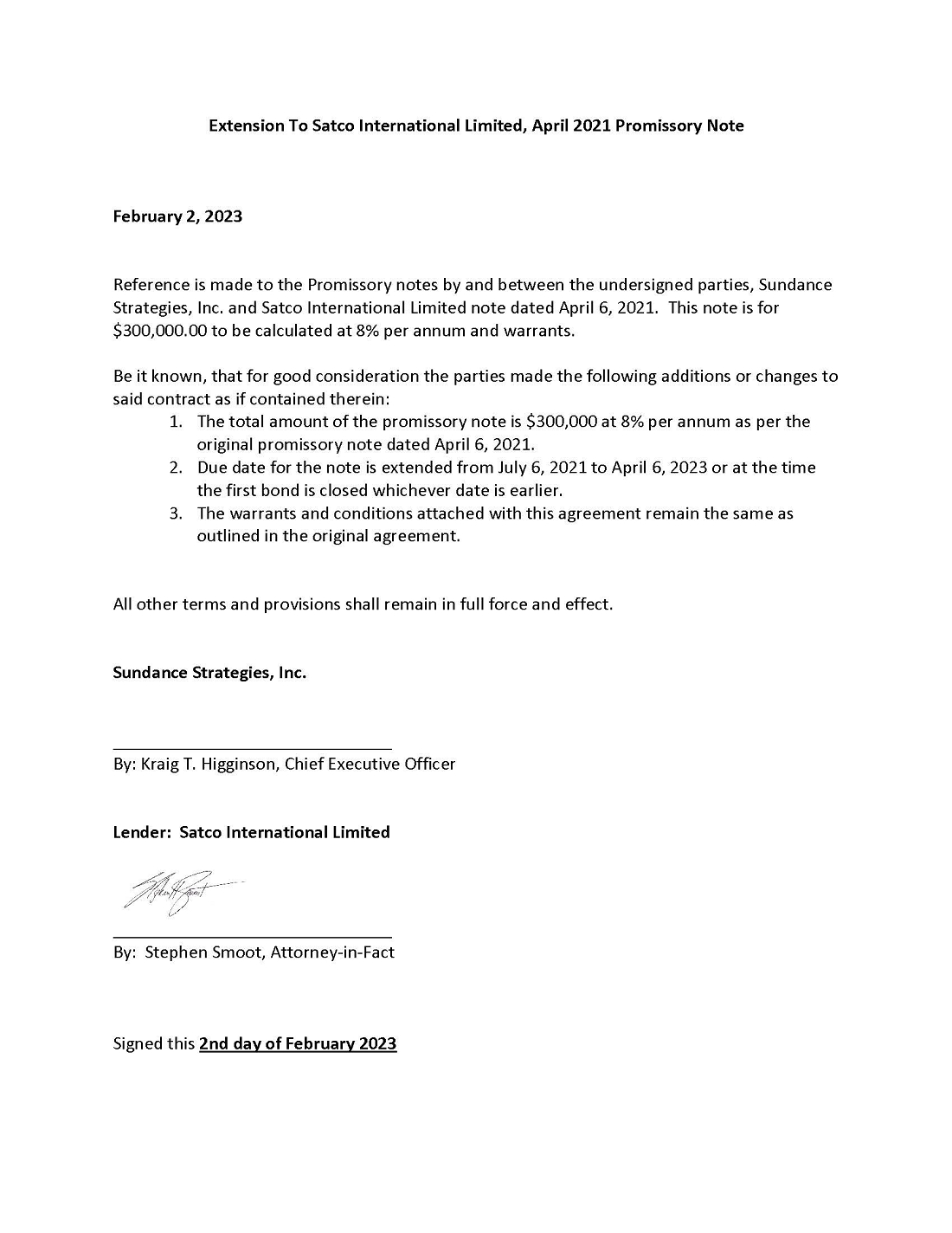

us-gaap:SubsequentEventMember

SUND:EightPecentageConvertibleDebentureAgreementMember

SUND:SatcoInternationalLtdMember

2023-06-08

2023-06-09

0001171838

2021-04-06

0001171838

SUND:UnsecuredPromissoryNoteMember

2023-03-31

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

us-gaap:RelatedPartyMember

2023-03-31

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

us-gaap:RelatedPartyMember

2022-03-31

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

2023-03-31

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

2022-03-31

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

2022-11-10

2022-11-10

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

srt:ScenarioForecastMember

2023-06-05

2023-06-05

0001171838

us-gaap:CommonStockMember

SUND:MrDickmanMember

2022-11-10

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

srt:ScenarioForecastMember

2023-06-05

0001171838

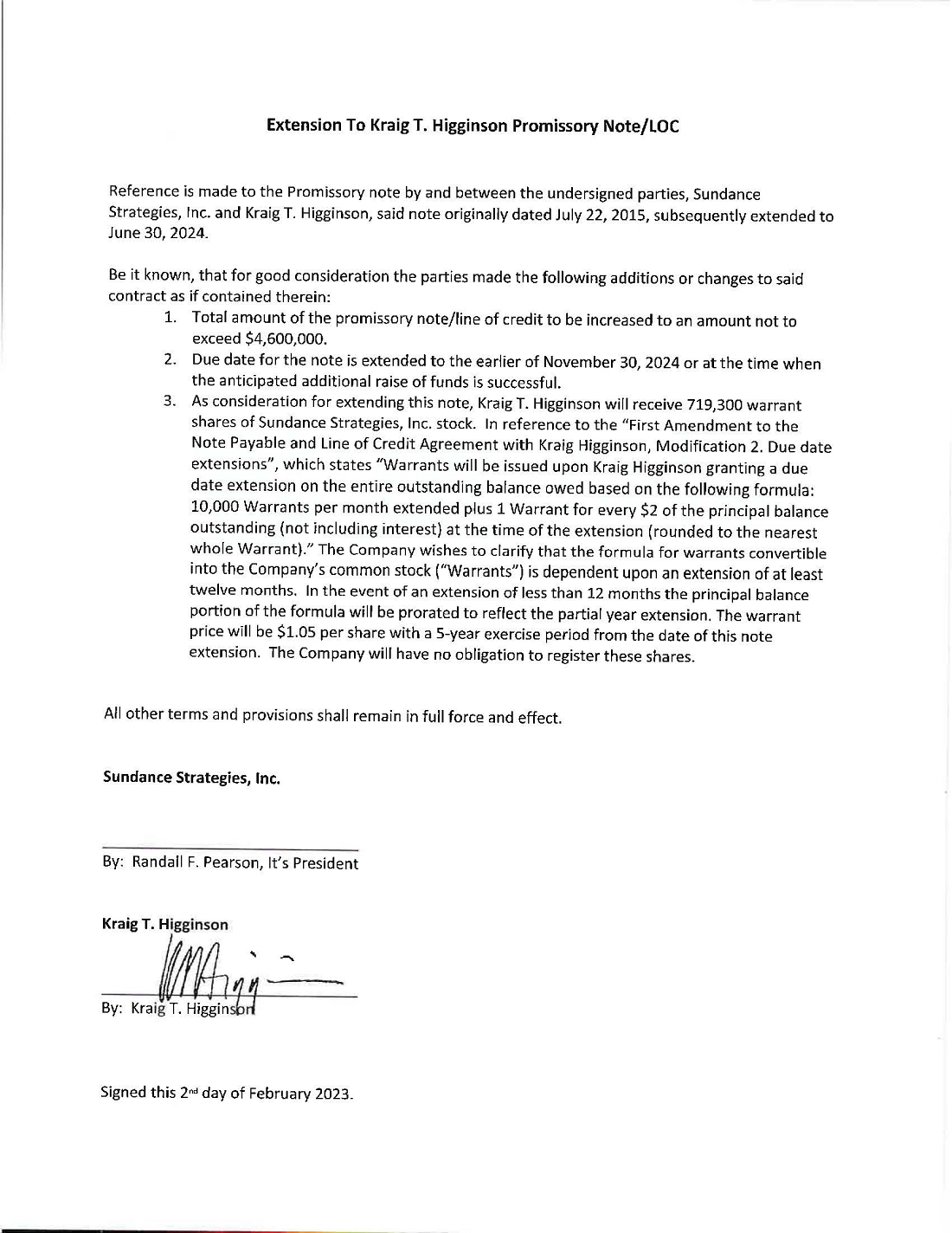

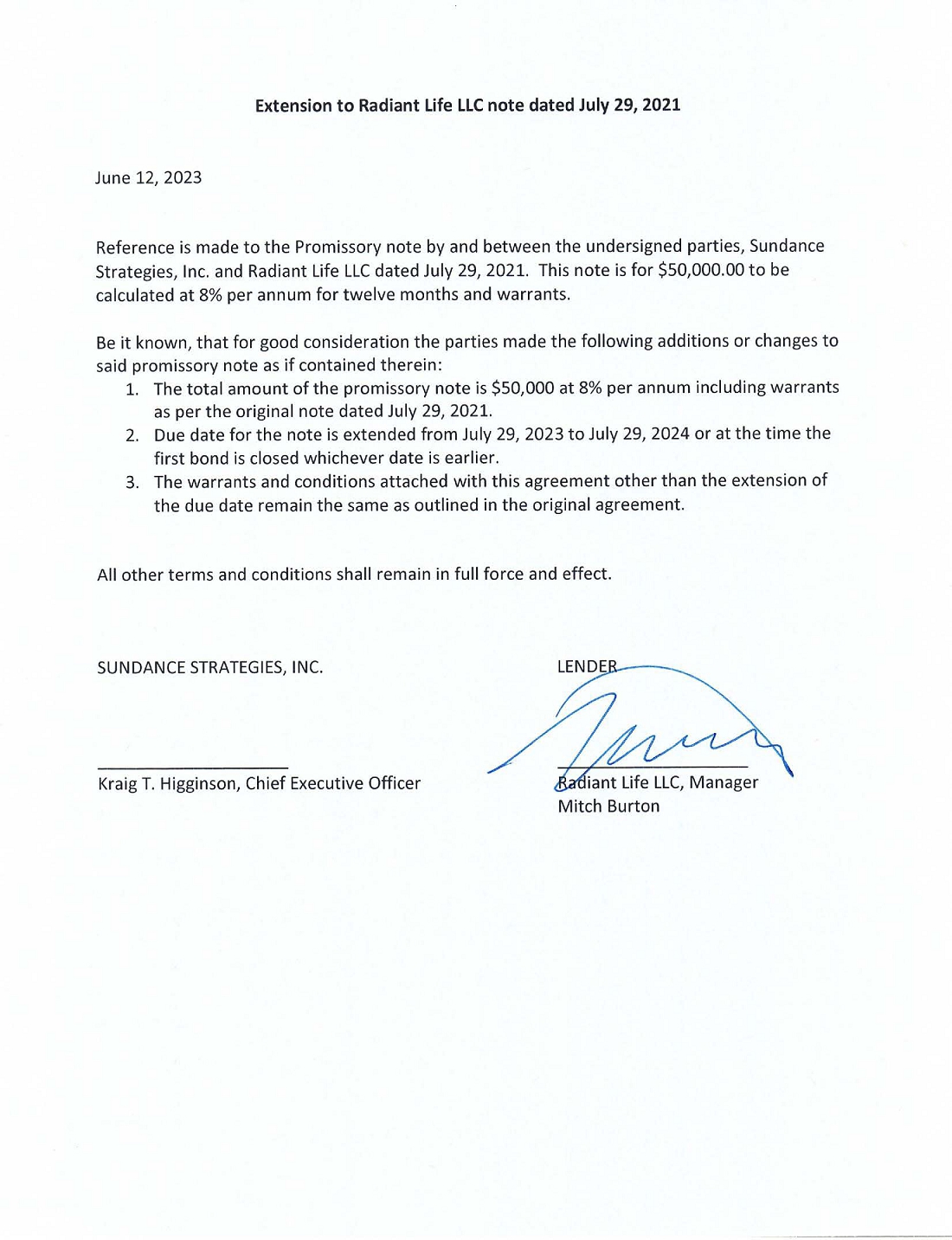

SUND:UnsecuredPromissoryNoteMember

2021-07-29

0001171838

SUND:UnsecuredPromissoryNoteMember

2021-07-29

2021-07-29

0001171838

SUND:RadiantLifeLLCMember

2021-07-29

0001171838

SUND:UnsecuredNotePayableMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

us-gaap:RelatedPartyMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

us-gaap:RelatedPartyMember

2022-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

us-gaap:ExtendedMaturityMember

2022-04-01

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

srt:MaximumMember

2023-03-31

0001171838

SUND:LineOfCreditAgreementMember

2022-04-01

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:RadiantLifeLLCMember

2023-03-31

0001171838

SUND:RadianLifeLLCMember

SUND:NotesPayableAndLinesOfCreditAgreementMember

2023-03-31

0001171838

us-gaap:LineOfCreditMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:RelatedPartyLenderMember

2023-03-31

0001171838

SUND:LineOfCreditAgreementMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:TheCompanysNibsMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:RadiantLifeLLCMember

us-gaap:RelatedPartyMember

2023-03-31

0001171838

SUND:RadiantLifeLLCMember

us-gaap:RelatedPartyMember

2022-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:RadiantLifeLLCMember

srt:MaximumMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

SUND:RadiantLifeLLCMember

SUND:TheCompanysNibsMember

2023-03-31

0001171838

us-gaap:WarrantMember

SUND:RadiantLifeLLCMember

2023-03-31

0001171838

SUND:NotesPayableAndLinesOfCreditAgreementMember

2023-03-31

0001171838

SUND:LenderMember

2023-03-31

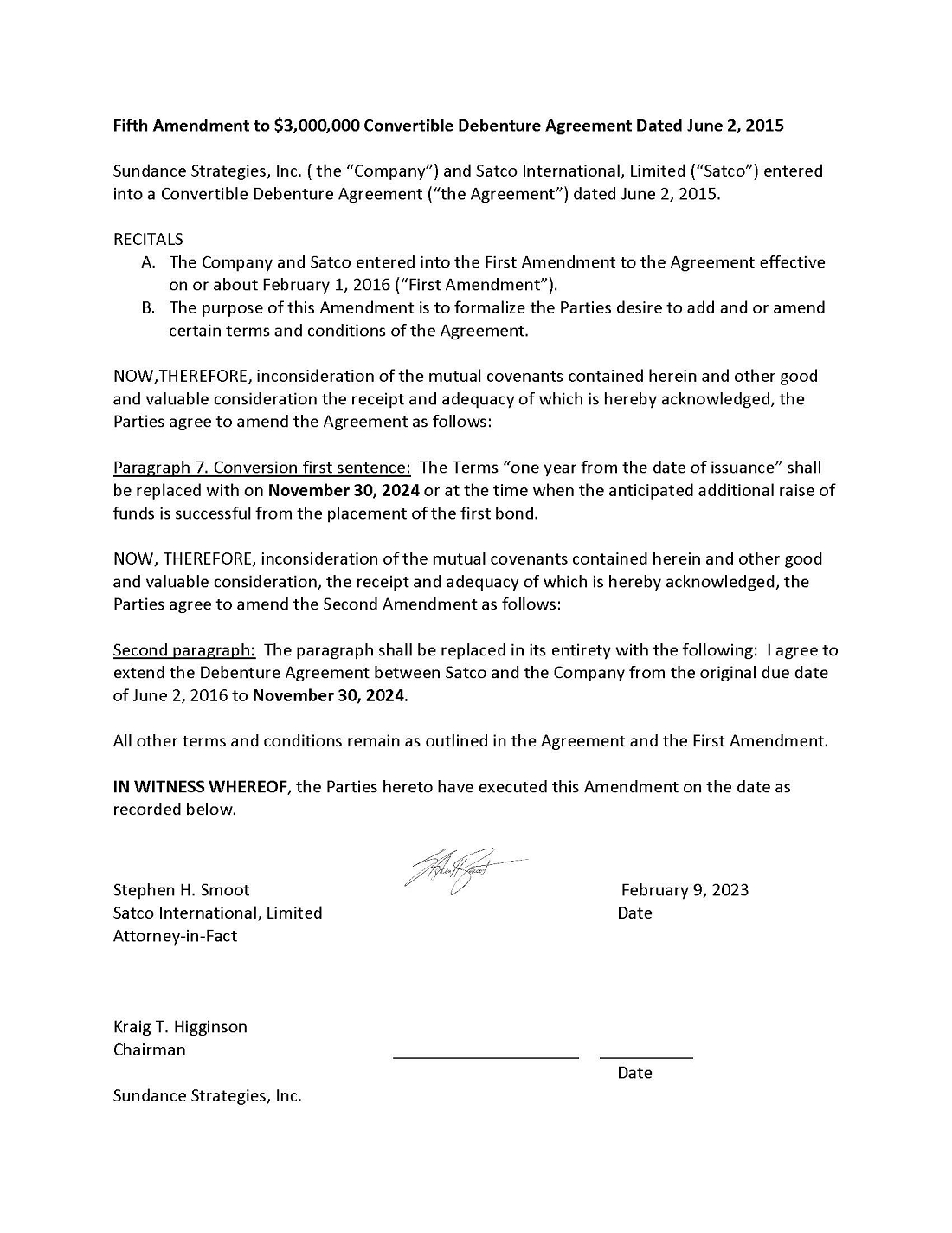

0001171838

SUND:EightPecentageConvertibleDebentureAgreementMember

SUND:SatcoInternationalLtdMember

2023-03-31

0001171838

SUND:EightPercentageConvertibleDebentureAgreementMember

SUND:SatcoInternationalLtdMember

2022-04-01

2023-03-31

0001171838

SUND:EightPecentageConvertibleDebentureAgreementMember

SUND:SatcoInternationalLtdMember

2022-04-01

2023-03-31

0001171838

SUND:EightPecentageConvertibleDebentureAgreementMember

SUND:SatcoInternationalLtdMember

us-gaap:ExtendedMaturityMember

2022-04-01

2023-03-31

0001171838

us-gaap:RestrictedStockMember

SUND:PrivatePlacementOfferingMember

2021-10-28

2021-10-29

0001171838

us-gaap:RestrictedStockMember

SUND:PrivatePlacementOfferingMember

2021-10-29

0001171838

SUND:SubscriptionAgreementMember

2021-11-05

2022-03-28

0001171838

SUND:SubscriptionAgreementMember

2022-03-28

0001171838

srt:DirectorMember

2021-05-03

2021-05-04

0001171838

srt:DirectorMember

2021-05-04

0001171838

SUND:ThreeExistingShareholdersMember

2018-12-06

0001171838

SUND:ThreeExistingShareholdersMember

2018-12-05

2018-12-06

0001171838

SUND:NotesPayableAndLinesOfCreditAgreeMember

SUND:RadiantLifeLLCMember

2022-04-01

2023-03-31

0001171838

SUND:RadianLifeLLCMember

2023-03-31

0001171838

us-gaap:WarrantMember

SUND:BoardOfDirectorsMember

2023-03-31

0001171838

SUND:MrDickmanMember

us-gaap:WarrantMember

2023-03-31

0001171838

SUND:MrDickmanMember

2023-03-31

0001171838

us-gaap:ValuationTechniqueOptionPricingModelMember

SUND:MrDickmanMember

2023-03-31

0001171838

SUND:MrDickmanMember

srt:MinimumMember

2022-04-01

2023-03-31

0001171838

SUND:MrDickmanMember

srt:MaximumMember

2022-04-01

2023-03-31

0001171838

SUND:MrDickmanMember

2022-04-01

2023-03-31

0001171838

SUND:ChairmanOfTheBoardDirectorsMember

2023-03-31

0001171838

SUND:ChairmanOfTheBoardDirectorsMember

us-gaap:WarrantMember

2023-03-31

0001171838

us-gaap:ValuationTechniqueOptionPricingModelMember

SUND:ChairmanOfTheBoardDirectorsMember

2023-03-31

0001171838

SUND:ChairmanOfTheBoardDirectorsMember

srt:MinimumMember

2022-04-01

2023-03-31

0001171838

SUND:ChairmanOfTheBoardDirectorsMember

srt:MaximumMember

2022-04-01

2023-03-31

0001171838

SUND:ChairmanOfTheBoardDirectorsMember

2022-04-01

2023-03-31

0001171838

SUND:RadiantLifeLLCMember

2022-02-05

0001171838

us-gaap:WarrantMember

SUND:BoardOfDirectorsMember

2022-02-05

0001171838

SUND:MrDickmanMember

us-gaap:WarrantMember

2022-02-05

0001171838

SUND:MrDickmanMember

2022-02-05

0001171838

us-gaap:ValuationTechniqueOptionPricingModelMember

SUND:MrDickmanMember

2022-02-05

0001171838

SUND:MrDickmanMember

srt:MaximumMember

2022-02-05

2022-02-05

0001171838

SUND:MrDickmanMember

2022-02-05

2022-02-05

0001171838

SUND:MrDickmanMember

srt:MinimumMember

2022-03-31

0001171838

SUND:MrDickmanMember

srt:MaximumMember

2022-03-31

0001171838

SUND:RadiantLifeLLCMember

2022-01-05

0001171838

us-gaap:ValuationTechniqueOptionPricingModelMember

2022-01-05

0001171838

2022-01-05

0001171838

2022-01-05

2022-01-05

0001171838

2022-02-07

0001171838

SUND:RadiantLifeLLCMember

srt:MinimumMember

2022-03-31

0001171838

SUND:RadiantLifeLLCMember

srt:MaximumMember

2022-03-31

0001171838

SUND:RadiantLifeLLCMember

us-gaap:WarrantMember

2022-03-31

0001171838

SUND:BoardOfDirectorsMember

SUND:RadiantLifeLLCMember

2022-03-31

0001171838

SUND:MrDickmanMember

2022-03-31

0001171838

SUND:MrDickmanMember

srt:MinimumMember

2021-04-01

2022-03-31

0001171838

SUND:MrDickmanMember

srt:MaximumMember

2021-04-01

2022-03-31

0001171838

SUND:MrDickmanMember

2021-04-01

2022-03-31

0001171838

SUND:SubscriptionAgreementMember

us-gaap:InvestorMember

2021-11-05

2022-03-28

0001171838

SUND:SubscriptionAgreementMember

us-gaap:InvestorMember

2022-03-28

0001171838

SUND:RadianLifeLLCMember

us-gaap:RelatedPartyMember

2021-07-29

0001171838

SUND:RadianLifeLLCMember

2021-07-29

0001171838

SUND:RadianLifeLLCMember

2021-07-28

2021-07-29

0001171838

SUND:DickmanMember

2021-04-06

0001171838

SUND:DickmanMember

2021-04-01

2021-12-31

0001171838

us-gaap:WarrantMember

2021-03-31

0001171838

us-gaap:WarrantMember

2021-04-01

2022-03-31

0001171838

us-gaap:WarrantMember

2022-03-31

0001171838

us-gaap:WarrantMember

2022-04-01

2023-03-31

0001171838

us-gaap:WarrantMember

2023-03-31

0001171838

SUND:ExercisePriceOneMember

2023-03-31

0001171838

SUND:ExercisePriceOneMember

2022-04-01

2023-03-31

0001171838

SUND:ExercisePriceTwoMember

2023-03-31

0001171838

SUND:ExercisePriceTwoMember

2022-04-01

2023-03-31

0001171838

SUND:ExercisePriceThreeMember

2023-03-31

0001171838

SUND:ExercisePriceThreeMember

2022-04-01

2023-03-31

0001171838

SUND:ExercisePriceFourMember

2023-03-31

0001171838

SUND:ExercisePriceFourMember

2022-04-01

2023-03-31

0001171838

SUND:ExercisePriceFiveMember

2023-03-31

0001171838

SUND:ExercisePriceFiveMember

2022-04-01

2023-03-31

0001171838

us-gaap:SubsequentEventMember

SUND:SatcoInternationalLtdMember

us-gaap:UnsecuredDebtMember

2023-06-04

2023-06-05

0001171838

SUND:UnsecuredPromissoryNoteMember

SUND:MrGlennSDickmanMember

us-gaap:SubsequentEventMember

2023-06-05

0001171838

SUND:LineOfCreditAgreementMember

us-gaap:SubsequentEventMember

2023-06-05

0001171838

SUND:RadiantLifeLLCMember

us-gaap:SubsequentEventMember

2023-06-05

0001171838

SUND:VendorsMember

us-gaap:SubsequentEventMember

2023-06-06

0001171838

us-gaap:SubsequentEventMember

SUND:SatcoInternationalLtdMember

us-gaap:UnsecuredDebtMember

2023-06-08

2023-06-09

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

SUND:Integer

xbrli:pure

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

DC 20549

FORM

10-K

(Mark

One)

| ☒ |

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the fiscal year ended March 31,

or

| ☐ |

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the transition period from ________ to ________

Commission

file number: 000-50547

SUNDANCE

STRATEGIES, INC.

(Exact

name of registrant as specified in its charter)

| Nevada |

|

88-0515333 |

(State

or other jurisdiction

of

incorporation or organization) |

|

(I.R.S.

Employer

Identification

No.) |

| |

|

|

| 4626

North 300 West, Suite No. 365, Provo, Utah |

|

84604 |

| (Address

of principal executive offices) |

|

(Zip

Code) |

(801)

717-3935

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to section 12(b) of the Exchange Act:

None

Securities

registered pursuant to Section 12(g) of the Act:

Title

of each

class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which

registered |

| Common

Stock, $0.001 par value |

|

SUND |

|

OTCQB |

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files.) Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting

company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller

reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| |

Large

accelerated filer ☐ |

Accelerated

filer ☐ |

| |

Non-accelerated

filer ☒ |

Smaller

reporting company ☒ |

| |

|

Emerging

Growth Company ☒ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ☐ No ☒

As

of June 29, 2023 the registrant had 41,408,441

shares of common stock, par value $0.001, issued and outstanding. The aggregate market value of common shares held by non-affiliates

as of September 30, 2022 (the most recent second quarter), was $25,630,383. The total number of shares of common stock beneficially owned by executives, directors, and 10% stockholders as of March 31, 2023, and

September 30, 2022, is 29,725,163 and 27,571,760 respectively.

Documents

incorporated by reference.

None.

Table

of Contents

SUNDANCE

STRATEGIES, INC.

In

this Annual Report, references to “Sundance,” the “Company,” “we,” “us,” “our”

and words of similar import refer to Sundance Strategies, Inc., a Nevada corporation and its wholly-owned subsidiary, ANEW LIFE, INC.,

a Utah corporation (“ANEW LIFE”), unless the context requires otherwise.

Information

Concerning Forward-Looking Statements

This

annual report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended,

(the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)

that are based on management’s beliefs and assumptions and on information currently available to management. For this purpose any

statement contained in this report that is not a statement of historical fact may be deemed to be forward-looking, including, but not

limited to, statements relating to our future actions, intentions, plans, strategies, objectives, results of operations, cash flows and

the adequacy of or need to seek additional capital resources and liquidity. Without limiting the foregoing, words such as “may”,

“should”, “expect”, “project”, “plan”, “anticipate”,

“believe”, “estimate”, “intend”, “budget”, “forecast”,

“predict”, “potential”, “continue”, “should”, “could”,

“will” or comparable terminology or the negative of such terms are intended to identify forward-looking statements,

however, the absence of these words does not necessarily mean that a statement is not forward-looking. These statements by their nature

involve known and unknown risks and uncertainties and other factors that may cause actual results and outcomes to differ materially depending

on a variety of factors, many of which are not within our control. Such factors include, but are not limited to, economic conditions

generally and in the industry in which we and our customers participate; competition within our industry; legislative requirements or

changes which could render our products or services less competitive or obsolete; our failure to successfully develop new products and/or

services or to anticipate current or prospective customers’ needs; price increases; employee limitations; or delays, reductions,

or cancellations of contracts we have previously entered into; sufficiency of working capital, capital resources and liquidity and other

factors detailed herein and in our other filings with the United States Securities and Exchange Commission (the “SEC” or

“Commission”). Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect,

actual outcomes may vary materially from those indicated.

Forward-looking

statements are predictions and not guarantees of future performance or events. Forward-looking statements are based on current industry,

financial and economic information which we have assessed but which by its nature is dynamic and subject to rapid and possibly abrupt

changes. Our actual results could differ materially from those stated or implied by such forward-looking statements due to risks and

uncertainties associated with our business. Although we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither we nor any other person

assumes responsibility for the accuracy and completeness of these forward-looking statements and we hereby qualify all our forward-looking

statements by these cautionary statements.

These

forward-looking statements speak only as of their dates and should not be unduly relied upon. We undertake no obligation to amend this

report or revise publicly these forward-looking statements (other than pursuant to reporting obligations imposed on registrants pursuant

to the Exchange Act) to reflect subsequent events or circumstances, whether as the result of new information, future events or otherwise.

The

following discussion should be read in conjunction with our financial statements and the related notes contained elsewhere in this report

and in our other filings with the Commission.

PART

I

Item

1. Business

Organizational

Background

Java

Express, Inc., was organized under the laws of the State of Nevada on December 14, 2001, for the purpose of selling coffee and other

related items to the general public from retail coffee shop locations. These endeavors ceased in 2006, and it had no material business

operations from 2006 until March of 2013. On March 29, 2013, the Company, its newly formed and wholly-owned subsidiary, Anew Acquisition

Corp., a Utah corporation (“Merger Sub”), and ANEW LIFE, INC., a Utah corporation (“ANEW LIFE”), executed and

delivered an Agreement and Plan of Merger (the “Merger Agreement”), pursuant to which Merger Sub merged with and into ANEW

LIFE, ANEW LIFE was the surviving company under the merger and became a wholly-owned subsidiary of the Company on the closing of the

merger (the “Merger”). On April 17, 2013, the Company filed a Certificate of Amendment with the Secretary of State of the

State of Nevada to change its name from “Java Express, Inc.” to “Sundance Strategies, Inc.” Sundance Strategies,

Inc. is referred to as the Company, us or we.

Our

Business

Our

historical business model has focused on purchasing or acquiring life insurance policies and residual interests in or financial products

tied to life insurance policies, including notes, drafts, acceptances, open accounts receivable and other obligations representing part

or all of the sales price of insurance, life settlements and related insurance contracts being traded in the secondary marketplace, often

referred to as the “life settlements market.”

We

currently do not hold life settlement or life insurance policies but, rather, previously held a contractual right to receive the net

insurance benefits, or “NIBs”, from a portfolio of life insurance policies held by a third party (“the Owners”

or “the Holders”). These NIBs represented an indirect, residual ownership interest in a portfolio of individual life insurance

policies, and they allowed us to receive a portion of the settlement proceeds from such policies, after expenses related to the acquisition,

financing, insuring and servicing of the policies underlying our NIBs have been paid.

NIBs

are generally sold by an entity that holds the underlying life settlement or life insurance policies, either directly or indirectly through

a subsidiary, such an entity being referred to herein as a “Holder.” A Holder, either directly or through a wholly owned

subsidiary, purchases life insurance policies either from the insured or on the secondary market and aggregates them into a portfolio

of policies. At the time of purchase, the Holder also (i) contracts with a service provider to manage the servicing of the policies until

maturity, (ii) consider purchasing mortality re-insurance (“MRI”) coverage under which payments will be made to the Holder

in the event the insurance policies do not mature according to actuarial life expectancies, and (iii) arranges financing to cover the

initial purchase of the insurance policies, the servicing of the life insurance policies until maturity and the payment of the MRI premiums.

The financing obtained by the Holder for a portfolio of life settlement or life insurance policies is secured by the insurance policies

for which the financing was obtained. After a Holder purchases policies, aggregates them into a portfolio and arranges for the servicing,

MRI coverage and financing, the Holder contracts to sell NIBs related to the policies, which gives the holder of the NIBs the right to

receive the proceeds from the settlement of the insurance policies after all of the expenses related to such policies have been paid.

When an insurance policy underlying our NIBs comes to maturity, the insurance proceeds are first used to pay expenses associated with

such policy. Once all of the expenses have been paid, the Holder will retain a small percentage of the proceeds and then will pay the

remaining insurance proceeds to us.

During

the latter part of the fiscal year ended March 31, 2021, we began developing an additional business offering, providing professional

services to specialty structured finance groups, bond issuers and life settlement aggregators. We have assembled an experienced team

from the life settlement marketplace, as well as from other areas such as financial services and public financial markets. As a professional

services provider, we apply industry best practices to advise on the selection of specific portfolios of life insurance policies that

are tailored to meet the needs of its clients. Our clients may include bond issuers, bond investors, or other structured finance product

issuers. We develop strategies and methodologies which include the acquisition of life insurance portfolios, then use common structured

finance techniques and proprietary analytics to structure bonds for issuances, including principal protected bonds. Our goal is to deliver

long-term value and profitability to shareholders by growing our professional services business and asset base, resulting in the ability

to pay dividends to its shareholders.

During

the latter part of the year ended March 31, 2021, we began working closely with bond placement agents and aggregators to establish various

aspects of a proprietary, investment grade bond offering. In this arrangement, we participate as the sole originator in the role of structuring

and advising on the structure of the proprietary bond instrument. Included in the role of structuring financial assets, we use proprietary

analytics to establish the makeup of the rated instrument, including but not limited to, life settlement assets (life insurance policies)

and managed cash, and implements a process of selective assembly of the underlying assets and cash management that will meet the policy

requirements and analytics. We provide current and ongoing resources for all analytics, as well as advisement support for the investment

and non-investment grade ratings for the managed asset pool and the managed cash accounts. In our advisory role, we are reimbursed for

all expenses associated with the structuring and preparation of any bond offering, will receive an advisory payment upon the closing

of any bond offering, and then will hold residual rights on the balance of assets once the bond is retired.

On

January 1, 2022, we entered into a marketing and consulting agreement with Tradability, LLC (“Consultant”) that required

us to make an initial $100,000 payment and up to an additional $400,000 in the future (which will be financed by the Consultant via a

promissory note). The $400,000 obligation is contingent upon the Consultant and us successfully reaching certain milestones. Further,

the agreement requires us to issue between 1,000,000 and 10,000,000 stock options (which are exercisable into our common stock at prices

between $1.00 to $2.50 per share) contingent upon the Consultant and us successfully reaching certain milestones. The milestones primarily

relate to the Consultant finalizing the tokenization of 500 million non-fungible tokens (“NFTs”) and the successful placement

of NFTs with proceeds of between $100 million and $500 million. The proceeds will be used to purchase Life Settlements for which we will

be an advisor. As of the issuance of these financial statements, none of the milestones related to the potential issuance of equity have

been met.

Life

Settlements Market

There

are a number of reasons a policy owner may choose to sell his or her life insurance policy. The policy owner may no longer need or want

his or her policy, he or she may wish to purchase a different kind of insurance policy, premium payments may no longer be affordable

or the policy owner may need cash to fund healthcare or other expenses. In particular, policy holders 65 years of age and older and their

families are faced with a variety of challenges as they seek to address their post-retirement financial needs and selling one’s

life insurance policy may provide a unique and valuable financial solution to such challenges. From the early 2000s through 2008, the

market for newly originated life settlements grew from virtually no activity to a peak of an estimated $12 billion of face value of U.S.

life settlement policies settled annually in 2007 and 2008. Economic factors slowed the growth in 2009, when an estimated $8 billion

of face value of U.S. life insurance was settled and growth has continued to decline since that time. Participants in the secondary life

settlement market have included major insurance companies which have purchased available pools of policies for their own investment,

portfolio aggregators, private equity funds, and independent third-party investors.

Predictability

of Future Cash Flows. Predictability of future cash flows is one of the biggest challenges facing companies engaged in the life

settlements industry. If a Holder is not able to adequately predict future cash flows and does not continually have enough cash to make

a policy portfolio’s premium payments, the policies in the portfolio may lapse and we may lose our right to receive the proceeds

from the settlement of the policies at maturity. Prediction of future cash flow requires the use of financial models, which rely on various

assumptions. These assumptions include the amount and timing of projected net cash receipts, expected maturity events, counter party

performance risk, changes to applicable regulation of the investment, shortage of funds needed to maintain the asset until maturity,

changes in discount rates, life expectancy estimates and their relation to premiums, interest, and other costs incurred, among other

items. These uncertainties and contingencies are difficult to predict and are subject to future events that may impact our estimates

and interest income. As a result, actual results could differ significantly from those estimates. If projections of life expectancies

are wrong, Holders may be obligated to service the related insurance policies for longer than expected, thereby increasing their costs

and reducing the net insurance benefit available.

Financing

a portion of the purchase price. Financing a portion of the purchase price of a policy portfolio allows the Holder to leverage

its investment and create a larger and diversified policy portfolio. When making an investment in a portfolio of life insurance policies,

a Holder utilizes actuarial tables to determine when the policies in the portfolio can be expected to come to maturity. However, the

Holder assumes the risk that the policies in the portfolio will come to maturity later than was predicted by the actuarial tables used

at the time of purchase. The life expectancies provided by the actuarial tables are based on actual death rates in large populations

of individuals with similar demographic characteristics. Thus, the more policies underlying a policy portfolio, the more reliable the

use of actuarial tables becomes. In other words, the larger the policy portfolio, the more closely the underlying insureds would be expected

to, on average, follow actuarial predictions and the lower the risk associated with future cash flows will be. Because of the general

uncertainty of maturity of life insurance policies, financing for their purchase and servicing has historically been difficult to secure.

The lender (the “Holders’ Lender”) has provided financing to the Holders to finance the purchase of the insurance policies.

We believe there are few lenders within this market.

Mortality

Re-Insurance (MRI) Coverage. Because of the uncertainty of maturity of insurance policies the Holders had, on occasion, previously

contracted with an insurance provider for MRI coverage. MRI coverage typically provides guaranteed cash flow based on the expected death

benefits of the pool of policies being insured calculated at the issuance of the coverage and thereby provides credit enhancement to

any bank providing financing to a Holder. The term of the MRI policies is usually 15 years. Any claims paid by the MRI to the Holder

must be paid back to the MRI provider out of death benefit proceeds from the pool of policies being insured when such death benefit proceeds

are eventually received. This enables the Holder to receive a smoother cash flow from a pool of policies over time and avoid “lumpiness”

in the cash flows that would otherwise be more pronounced in the absence of the MRI coverage. Any claim payment balances would accrue

interest, typically at a spread of 250 basis points over LIBOR, to the extent they remain outstanding. The MRI coverage is obtained by

paying an MRI premium, typically at equal to 2% of the cumulative death benefit of the covered life insurance policies, at the outset

of the coverage and, depending on the specific terms of the MRI policy, possibly an additional premium amount at a predetermined time

during the effective coverage period (the “Commitment Fee”), which is typically 1% of the cumulative death benefits of the

covered policies. The insurer under the MRI policy typically must approve the sale of any life insurance policies covered by the MRI

policy if such sale does not result in the full repayment of any outstanding recovery amounts. It is our understanding that there is

only one MRI Provider. While the MRI coverage is relatively expensive, we believe that insurance policies that are covered by MRI have

less volatility, are more liquid and should achieve higher values for purposes of financing and secondary market sales.

Financing

a policy portfolio’s premium payments gives a Holder additional cash needed to satisfy the premium obligations of its portfolio.

In addition, obtaining MRI increases the probability that the Holder will receive future cash flows in the event the underlying insureds

live longer than expected. This combination provides the Holder with sufficient liquidity to stabilize its cash position.

Life

Settlement Purchasing Guidelines as an Advisor

Our

objective is to advise and assist entities as they acquire Life Insurance policies and portfolios that will produce returns in excess

of any and all purchase, financing, servicing and insuring costs incurred by the Holder. The guidelines we generally follow regarding

the purchase of policies and portfolios include:

| |

● |

the

insured is 75 years old or older; |

| |

● |

all

NIBs relate to U.S. Universal Life Insurance policies; |

| |

● |

all

underlying insurance policies have qualified for financing that will cover at least four years of premiums; |

| |

● |

each

policy must first be reviewed by the legal due diligence team of the lender providing financing for the acquisition and servicing

of the life insurance policies, second by the MRI company’s due diligence team and then finally approved by our due diligence

processes; |

| |

● |

all

policies must qualify for MRI; and |

| |

● |

the

projected proceeds payable on each life insurance policy upon the death of the underlying insured are projected to exceed the costs

to service the life insurance policies, amounts due to creditors secured by such life insurance policy, such as the Holders’

Lender or the MRI provider, other costs and fees incurred by the Holder and the percentage of the remaining insurance benefit retained

by the Holder |

Competition

We

encounter significant competition in the life settlements industry generally from numerous companies, including hedge funds, investment

banks, secured lenders, specialty life insurance finance companies and life insurance companies themselves who purchase life settlements.

Many of these competitors have greater financial and other resources than we do and may have a significantly lower cost of funds because

they have greater access to insured deposits or the capital markets. Moreover, some of these competitors have significant cash reserves

and can better fund shortfalls in collections that might have a more pronounced impact on companies such as ours. They also have greater

market share. For example, Berkshire Hathaway purchased a portfolio of $300 million (face value) in life insurance policies in 2013.

According to The Deal Pipeline, total life settlement transactions grew to $2.57 billion (face value) in 2013. In 2014 transaction

volumes were reported higher by market participants in all major segments of the industry and Conning & Co. forecast an average annual

gross market potential for life settlements of $180 billion from 2014-2023, with an average volume of approximately $3 billion per year

in life settlement transactions.

A

report from the AAP Life Settlement Market Update indicated that internal rates of return for life settlement transactions conducted

in 2013 were in the high-teens, an attractive return at a time when fixed income and other hedge positions were delivering minimal rates

of return. In the event that certain better-financed companies make a significant effort to compete against our business or the secondary

market in general, prices paid for existing portfolios of life insurance policies may rise and our ability to purchase satisfactory assets

may decline. In addition, recent shrinking of the market for life settlements has resulted in fewer available pools of insurance policies.

As a result, price competition for the remaining pools has increased. Our limited resources prohibit us from competing for larger pools.

These factors could adversely affect our profitability by reducing our return on investment or increasing our risk.

Employees

On

March 31, 2023, we had one full-time employee: Randall F. Pearson, our President.

Available

Information

Our

website address is www.sundancestrategies.com. We make available free of charge on the Investor Relations portion of our website, our

annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished

pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file

such material with, or furnish it to, the Securities and Exchange Commission.

Item

1A. Risk Factors

We

have identified the following risks and uncertainties that may have a material adverse effect on our business, financial condition, results

of operations and future growth prospects. Our business could be harmed by any of these risks. The risks and uncertainties described

below are not the only ones we face. The trading price of our common stock could decline due to any of these risks, and you may lose

all or part of your investment. In assessing these risks, you should also refer to other information contained in this Form 10-K, including

our consolidated financial statements and related notes.

Summary

of Risk Factors

Our

business is subject to a number of risks and uncertainties including those described at length in the Risk Factors section below. We

consider the following to be our most material risks:

Risks Relating to Our Business

| |

● |

We

have historically used significant amounts of cash in operating activities since our inception and may continue to use significant

amounts of cash for operating activities in the foreseeable future. |

| |

● |

We may not be able to secure additional financing on favorable terms, or at all, to meet our future capital needs

and our failure to obtain additional financing when needed could force us to delay, reduce or eliminate our product development programs

and commercialization efforts or cause us to become insolvent. |

| |

● |

There may be substantial doubt about our ability to continue as a going concern, and we will need additional financing

to execute our business plan, to fund our operations and to continue as a going concern. |

| |

● |

We may default on our obligations under various debt arrangements, which may accelerate our repayment obligations

or otherwise limit our access to future financing. |

| |

● |

We

are pursuing opportunities relating to the tokenization and sale of digital assets that are subject to volatile market prices, impairment

and unique risks of loss. |

| |

● |

Our

management team relies on outside consultants and others in our industry to make informed business decisions; potential conflicts

of interest involving those parties who are relied upon could adversely affect the execution of our business model. |

| |

● |

Current

and future federal regulation under the Dodd-Frank Act’s consumer protection provisions may have an adverse effect on our business

and our planned business operations. |

| |

● |

General

economic conditions could have an adverse effect on our business. |

| |

● |

The

costs in time and expense of being a publicly-held company are substantial and will only increase if our business model is successful. |

| |

● |

Inadequate

funding will impede execution of our business model. |

| |

● |

We

are new to the bond, life settlement, and financial advisory industry and may not be able to successfully compete in this industry. |

| |

● |

Historically,

99% of our total assets are interests in life settlement policies, resulting in a lack of diversification of assets and concentration

in assets that are subject to significant fluctuations in value. |

| |

● |

Limitations

to the financial model we use may result in inaccurate or incomplete projections of future cash flow from the insurance policies. |

| |

● |

The

individuals insured by the life insurance policies may live longer than their actuarial life expectancies and thereby, cash flows

from life insurance policies may be delayed. |

| |

● |

Having

relatively few insureds could cause the overall performance to be unduly influenced by a relatively small number of underlying policies

that perform better or worse than expected. |

| |

● |

Increased

general market interest rates could increase the carrying costs of the life insurance policies and reduce the related cash

flows. |

| |

● |

Changes

to foreign banking laws and regulations or decreased lending capacity for life settlements could have a negative impact on ability

of Holders to obtain loans with respect to purchases of life settlements. |

| |

● |

Holders

may be required to obtain MRI coverage as a condition of our business model, which, if unavailable, could potentially increase our

risk of failure. |

| |

● |

The

lapse of life insurance policies will result in the entire loss of our interest in the death benefits from those particular policies. |

| |

● |

Actual

results from life settlement products may not match expected results, which could reduce returns and also adversely affect the ability

to service and grow a portfolio for actuarial stability. |

| |

● |

The

limited number of sellers of life settlement products in the secondary market may limit the ability to negotiate favorable prices

in the acquisition of such life settlement interests. |

| |

● |

We

do not track concentrations of pre-existing medical conditions of insureds in our guidelines for purchasing life settlement products. |

| |

● |

If

life settlement products are determined to be “securities,” Holders may be required to register as an investment company

under the Investment Company Act, which would substantially increase SEC reporting costs and oversight of a Holder’s business

operations. |

| |

● |

There

is poor liquidity in the secondary market for life insurance and life settlements. |

Risks

Related to the Life Insurance Policies

| |

● |

Life settlements,

and therefore our common stock, are highly speculative and may lose all of their value. |

| |

● |

Policies may be determined

to have been issued without an “insurable interest” and could be void or voidable. |

| |

● |

Additional insurable interest

concerns regarding life insurance policies originated pursuant to premium finance transactions may also result in adverse decisions

that could effect policies. |

| |

● |

Fraud in the application

for life insurance can also affect assets and interest in policies. |

| |

● |

The risk of litigation

with issuing insurance companies could substantially raise our costs of operation and increase our risk of loss. |

| |

● |

The contestation of the

life insurance policies by the applicable issuing insurance companies could result in the loss of the benefits from such life insurance

policies. |

| |

● |

Increases in cost of insurance

could reduce estimated returns and lower revenues. |

| |

● |

Carrier and service partner

credit risk can adversely affect life settlements. |

| |

● |

The inability to keep track

of the insureds could keep us from updating the medical records of the insured. |

| |

● |

Lost insureds can result

in a delay or a loss of an insurance benefit that would have a negative effect on revenues and prospects. |

| |

● |

U.S. life settlement and

viatical regulations may result in determination(s) of applicable law violations. |

| |

● |

State protections for the

insolvency of an insurance company are limited. |

| |

● |

Liability for failing to

comply with U.S. privacy safeguards. |

| |

● |

Cyber-attacks or other

security breaches could have a material adverse effect on our business. |

| |

● |

U.S. privacy concerns may

affect the access to accurate and current medical information regarding the insured under life insurance policies. |

Risk

Factors Related to Our Common Stock

| |

● |

There is a

limited public market for our common stock, and any market that may develop could be volatile. |

| |

● |

We are an emerging growth

company and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common

stock less attractive to investors. |

| |

● |

Our management and two

stockholders beneficially own approximately 65% of our outstanding common stock and therefore can exert control over our business. |

| |

● |

Future sales of our common

stock could adversely affect our stock price and our ability to raise capital in the future, resulting in our inability to raise

required funding for our operations. |

Risk

Factors relating to Our Business

We

have historically used significant amounts of cash in operating activities since our inception and may continue to use significant amounts

of cash for operating activities in the foreseeable future.

We

have historically used substantial amounts of cash in operating activities. To date, our operations have not generated sufficient cash

flow to fund our operations and we have relied on cash provided by financing activities, including amounts received under notes payable

and lines-of-credit with related parties. Our default under these obligations may also limit our ability to obtain future financing from

related or third parties.

Our

inability to access capital may limit our ability to adequately fund our operations. In order to continue to fund our operations, including

the potential purchase of NIBs, we will need to raise substantial amounts of capital. Absent additional financing, we will not have the

resources to execute our business plan.

We

may not be able to secure additional financing on favorable terms, or at all, to meet our future capital needs and our failure to obtain

additional financing when needed could force us to delay, reduce or eliminate our product development programs and commercialization

efforts or cause us to become insolvent.

We

will need to raise additional funds through future equity or debt financings in the near future to meet our operational needs and capital

requirements. We can provide no assurance that we will be successful in raising funds pursuant to additional equity or debt financings

or that such funds will be raised at prices that do not create substantial dilution for our existing stockholders. Given the volatility

of our stock price, any financing that we undertake could cause substantial dilution to our existing stockholders.

To

date, we have financed our operations primarily through net proceeds from the issuance of capital stock and debt financings. We do not

know when or if our operations will generate sufficient cash to fund our ongoing operations. We cannot be certain that additional capital

will be available as needed on acceptable terms, or at all.

We

may raise additional funds in equity or debt financings or enter into credit facilities in order to access funds for our capital needs.

Any debt financing obtained by us in the future would cause us to incur additional debt service expenses and could include restrictive

covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for

us to obtain additional capital and pursue business opportunities. In addition, future equity investors may require that we convert all

or a portion of our debt to equity, and our debtholders may not agree to such terms. If we raise additional funds through further issuances

of equity or convertible debt securities, and/or if we convert all or a portion of our existing debt to equity, our existing stockholders

could suffer significant dilution in their percentage ownership of our company, and any new equity securities we issue could have rights,

preferences and privileges senior to those of holders of our common stock. If we are unable to obtain adequate financing or financing

on terms satisfactory to us when we require it, we may significantly scale back our operations or we may become insolvent. If this were

to occur, our ability to continue to grow and support our business and to respond to business challenges could be significantly limited.

There

may be substantial doubt about our ability to continue as a going concern, and we will need additional financing to execute our business

plan, to fund our operations and to continue as a going concern.

Since

inception, we have experienced recurring operating losses and negative cash flows and we expect to continue to generate operating losses

and consume significant cash resources for the foreseeable future. There may be substantial doubt regarding our ability to continue as

a going concern. We have prepared our financial statements on a going concern basis, which contemplates the realization of assets and

the satisfaction of liabilities and commitments in the normal course of business. Our financial statements for the fiscal year ended

March 31, 2023 do not include any adjustment to reflect the possible future effects on the recoverability and classification of assets

or the amounts and classification of liabilities that may result from the outcome of this uncertainty, with the exception that all borrowings

are classified as current on the balance sheets.

Our

inability to access capital may limit our ability to adequately fund our operations and continue as a going concern. To continue as a

going concern we will need to raise substantial amounts of capital. Absent additional financing, we will not have the resources to execute

our business plan and continue as a going concern.

Inadequate

funding will impede execution of our business model.

At

present, we are a minor participant in both the life settlement market and in the bond advisory industry. We face significant competition

from much larger competitors. We will need substantial additional funds to effectively compete in these industries, and no assurance

can be given that we will be able to adequately fund our current and intended operations. We expect to finance our operating working

capital requirements, with proceeds from planned public and/or private offerings of our securities and debt financing. There can be no

assurance that we will be successful in raising debt or equity capital or that we will be successful in raising additional capital in

the future on terms acceptable to us, or at all. If we are not able to obtain sufficient funding to execute our business strategies,

we may be required to scale back or discontinue our operations, which would materially adversely affect our financial condition and results

of operations.

We

may default on our obligations under various debt arrangements, which may accelerate our repayment obligations or otherwise limit our

access to future financing.

If

we fail to make timely repayments of amounts received under notes payable and lines-of-credit with related parties or the 8% convertible

debenture agreement we will be in default of such obligations, which could materially adversely affect our operations and financial condition.

Our default under these obligations may also limit our ability to obtain future financing from related or third parties, which would

materially adversely affect our operations and our ability to execute our business strategy.

We

are pursuing opportunities relating to the tokenization and sale of digital assets that are subject to volatile market prices, impairment

and unique risks of loss.

We

are exploring opportunities to pursue the tokenization and sale of non-fungible tokens (“NFTs”). There is no guarantee that

we will be able to successfully tokenize and sell such NFTs, and our use of NFTs exposes us to additional risks.

The

prices of digital assets have been in the past and may continue to be highly volatile due to various associated risks and uncertainties.

For example, the prevalence of such assets is a relatively recent trend, and their long-term adoption by investors, consumers, and businesses

is unpredictable. Moreover, their lack of a physical form, their reliance on technology for their creation, existence and transactional

validation and their decentralization may subject their integrity to the threat of malicious attacks and technological obsolescence.

As a result, the value that we may realize, if any, from the sale of NFTs is uncertain.

Digital

assets, as intangible assets without centralized issuers or governing bodies, have been, and may in the future be, subject to security

breaches, cyberattacks or other malicious activities, as well as human errors or computer malfunctions that may result in the loss or

destruction of private keys needed to access such assets. While we intend to take all reasonable measures to secure any digital assets,

if such threats are realized or the measures or controls we create or implement to secure our digital assets fail, it could result in

a partial or total misappropriation or loss of our digital assets, and our financial condition and operating results may be harmed.

At

this time, the regulation of digital assets and NFTs remains in an early stage. The extent to which securities laws or other regulations

apply or may apply in the future to such assets is unclear at this time. However, on March 9, 2022, the White House issued an Executive

Order on Ensuring Responsible Development of Digital Assets proposing, among other things, regulation of digital assets. Future regulation

of such assets may increase our compliance costs or adversely impact our business.

NFTs

may also be subject to regulations of the Financial Crimes Enforcement Network (“FinCEN”) of the U.S. Department of Treasury

and the Bank Secrecy Act. Further, the Office of Foreign Assets Controls (“OFAC”) has signaled sanctions could apply to digital

transactions and has pursued enforcement actions involving cryptocurrencies and digital asset accounts. The nature of many NFT transactions

also involve circumstances which present higher risks for potential violations, such as anonymity, subjective valuation, use of intermediaries,

lack of transparency, and decentralization associated with blockchain technology. In addition, the Commodity Futures Trading Commission

has stated that cryptocurrencies, with which NFTs have some similarities, fall within the definition of “commodities.” If

NFTs were deemed to be a commodity, NFT transactions could be subject to prohibitions on deceptive and manipulative trading or restrictions

on manner of trading (e.g., on a registered derivatives exchange), depending on how the transaction is conducted. Moreover, if NFTs were

deemed to be a “security,” it could raise federal and state securities law implications, including exemption or registration

requirements for marketplaces for NFT transactions, sellers of NFTs, and the NFT transactions themselves, as well as liability issues,

such as insider trading or material omissions or misstatements, among others. NFT transactions may also be subject to laws governing

virtual currency or money transmission. For example, New York has legislation regarding the operation of virtual currency businesses.

NFT transactions also raise issues regarding compliance with laws of foreign jurisdictions, many of which present complex compliance

issues and may conflict with one another. Our launch and operation of our NFT platform expose us to the foregoing risks, among others,

any of which could materially and adversely affect the success of our NFT platform and harm our business, financial condition, results

of operations, reputation, and prospects.

Our

management team relies on outside consultants and others in our industry to make informed business decisions; potential conflicts of

interest involving those parties who are relied upon could adversely affect the execution of our business model

Our

management team has relied and will continue to rely on consultants and service providers in our industry. Many of these consultants

or service providers represent or provide services to others in this industry, and no assurance can be given that we, as a small competitor

competing with larger competitors in our industry, will be able to engage these consultants. In addition, our inability to retain such

consultants would negatively affect our ability to identify and evaluate life insurance products for purchase. Even as our management

accumulates expertise in this industry, we will still rely on the expertise of outside consultants for a variety of information, including

valuation, life expectancies, actuarials and other matters specific to life insurance policies. If we cannot obtain such services at

an affordable price, our business will be harmed.

Current

and future federal regulation under the Dodd-Frank Act’s consumer protection provisions may have an adverse effect on our business

and our planned business operations.

On

July 21, 2010, President Barack Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank

Act”). The Dodd-Frank Act contains significant changes to the regulation of financial institutions including the creation of new

federal regulatory agencies and the granting of additional authorities and responsibilities to existing regulatory agencies to identify

and address emerging systemic risks posed by the activities of financial services firms. The Dodd-Frank Act also provides for enhanced

regulation of derivatives and asset-backed securities offerings, restrictions on executive compensation and enhanced oversight of credit

rating agencies. The provisions include a new independent Bureau of Consumer Financial Protection to regulate consumer financial services

and products, and life settlement transactions may be within the scope of its jurisdiction. Actions taken by the Bureau of Consumer Financial

Protection may have material adverse effects on the life settlement industry and could affect the value of insurance policies. In addition,

the Dodd-Frank Act also limits the ability of federal laws to preempt state and local consumer laws. Prospective investors should be

aware that the changes in the regulatory and business landscape as a result of the Dodd-Frank Act could have an adverse impact on us

and the entities from which we may acquire NIBs and similar life settlement products.

General

economic conditions could have an adverse effect on our business.

Changes

in general economic conditions, including, for example, interest rates, investor sentiment, market and regulatory changes specifically

affecting the insurance industry, competition, technological developments, political and diplomatic events, tax laws, and other factors

not known to us today, can substantially and adversely affect our business and prospects. There continues to be uncertainty about the

prospects for growth in the U.S. economy as well as economies of other countries, driven by factors such as high current unemployment,

rising government debt levels, prospective Federal Reserve (and similar foreign bodies) policy shifts, the withdrawal of government interventions

in financial markets, changing consumer spending patterns, and changing expectations for inflation and deflation. These factors have

adversely affected the financial markets and the claims-paying ability of many insurers. Such uncertainties and general economic trends

can affect the ability to obtain funds to finance life settlement products. None of these risks are or will be within our control.

The

costs in time and expense of being a publicly-held company are substantial and will only increase if our business model is successful.

We

are required to file annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports respecting certain events on Form

8-K, along with proxy or information statements for any meeting of stockholders or written consents of stockholders holding sufficient

securities to effect corporate actions. Most of these reports require generating and compiling significant accounting, legal and financial

information, including audited year-end financial statements and reviewed quarterly financial statements. The preparation of these reports,

their review by management and professionals and the auditing and review process of such financial statements consumes significant resources,

in terms of management time and focus, as well as expenses related to legal, accounting and audit fees. It is difficult to quantify these

costs, but we believe them to be not less than between approximately $175,000 and $250,000 annually. As our business grows, these costs

can only increase.

We

are new to the bond, life settlement, and financial advisory industry and may not be able to successfully compete in this industry.

We

only recently began providing advisory services relating to bond issuances and life settlement transactions. In order for these operations

to be successful, we will need to develop sufficient expertise and establish relationships with clients. Identifying and acquiring clients

in this industry will require us to compete with other larger, more experienced, and better capitalized service providers and we may

not be successful in developing such client relationships. If we are not able to successful market our advisory business, our financial

condition and results of operations will be materially adversely affected.

Historically,

99% of our total assets are interests in life settlement policies, resulting in a lack of diversification of assets and concentration

in assets that are subject to significant fluctuations in value.

Although

we currently have no ownership in life settlement policies, generally speaking, our previous investment in NIBs was usually the primary

asset on our balance sheet. Life settlement products like NIBs are subject to substantial fluctuations in value, primarily based upon

matters that are not within our control, such as the current health and life expectancy of the insureds underlying our NIBs, the solvency

of the Holders of the policies and the Holders’ Lender, the Holders’ financing costs and ability to acquire policies and

the solvency of the insurance companies. Each of these factors can result in significant fluctuations of the value of the life insurance

policies underlying the NIBs, thereby affecting potential future interests.

Limitations

to the financial model we use may result in inaccurate or incomplete projections of future cash flow from the insurance policies.

The

financial model we utilized to project future cash flows from potential life settlement assets was chosen because of its straight-forward

approach in calculating expected cash flows. We believe the methodology used in the model is particularly desirable because it has parameters

that are easily verifiable and does not require complex calculations or mathematical simulations to confirm results. However, with every

financial model, there are limitations. Most require assumptions to be made. Our model is no exception. Our assumptions may prove to

be incorrect and, therefore, our model may be incorrect. Our model relies on actuarial life-expectancy reports prepared by third parties

from which the estimated date of maturity is calculated. It is assumed that these reports were accurately made and properly reflect real

life expectancies. Our model also requires other inputs including but not limited to the following: (i) a 15-year period for projections;

(ii) a distinct number of lives; (iii) a distinct number of policies; (iv) life expectancy tables and projections; (v) premiums; (vi)

senior lending fees; (vii) MRI fees; and (viii) insurance, servicing and custodial fees. While this method of modeling cash flows is

helpful in setting general expectations of potential returns that might be produced from a given portfolio, there is no way such results

can be guaranteed. In addition to our assumptions, there are many factors that may affect the selection of inputs for the model.

The

individuals insured by the life insurance policies may live longer than their actuarial life expectancies and thereby, cash flows from

life insurance policies may be delayed.

The

actual date of death of an insured with respect to a life insurance policy is uncertain. Life expectancies are projected from the medical

records of the insured and actuarial data based upon the historical experience of similarly situated persons. However, it is impossible

to predict with certainty any insured’s life expectancy. We have and will continue to base our longevity assumptions on the reports

of third-party life expectancy providers, among whom there is no uniformity of assumptions, approach or procedure. There are also significant

disputes among third-party life expectancy providers regarding the mortality rate relating to certain disease states and the efficacy

of certain treatments. Some factors that may affect the accuracy of a life expectancy report or other calculation of the estimated length

of an individual’s life are:

| |

● |

the

experience and qualifications of the medical professional or life expectancy company providing the life expectancy estimate; |

| |

|

|

| |

● |

the

completeness and accuracy of medical records received by the life expectancy company; |

| |

|

|

| |

● |

the

reliability of, and revisions to, actuarial tables or other mortality data published by public and private organizations or developed

by a life expectancy company and utilized by its medical professionals; |

| |

|

|

| |

● |

the

nature of any illness or health conditions of the insured disclosed or undisclosed; |

| |

|

|

| |

● |

changes

in living habits and lifestyle of an insured and medical treatments, medications and therapies available to and used by an insured;

and |

| |

|

|

| |

● |

future

improvements in medical treatments and cures, and the quality of medical care the insured receives. |

We

rely primarily on various different life expectancy providers. A life expectancy (“LE”), can be considered the life expectancy provider’s

“best estimate” as to how long a person would live. We assume that the life expectancies were accurately calculated and properly

assessed for purposes of our model. To introduce some “checks and balances” into our cash flow projections, we use at least

two LE reports from different third-party LE providers for each policy. We do this to try to avoid any systemic bias introduced by dependency

on life expectancies produced by a single source. In addition, our model gives greater weight to the longer (and more conservative) of

the two LEs. By using such a long/short weighted average, our model attempts to hedge against unexpected longevities in a portfolio.

Changes

in actuarial based life expectancy methodologies (which are determined by the Society of Actuaries and are amended every three to five

years) could have the effect of reducing the internal rate of return on the life insurance policies and could cause increased difficulty

in financing premiums. If changes are significant, they could lower prices for life insurance policies, but could also lower the value

of the life insurance policies due to the lower resulting present value of the death benefits forecasted to be paid at later dates. Holders’

senior loans require that certain loan to value ratios be maintained and decreases in policy values could result in violations of these

provisions. Default by Holders on their senior loans may impair their ability to obtain financing necessary to maintain the life insurance

policies.

In

addition, because our cash flow is usually dependent on life insurance policies coming to maturity, if life expectancies prove wrong

cash flows will change. If the insured lives longer than any or all of the life expectancy appraisals predict, then the amounts available

to life settlement interests could be diminished, perhaps significantly, due to the additional time during which premiums will have to

be paid and financing and other related expenses incurred in order to keep the related policy in force. If the insureds with respect

to too many life insurance policies live longer than their respective life expectancies, then Holders may have to liquidate such life

insurance policies. The market value of such Policies will necessarily be significantly less than the related death benefits.

Having

relatively few insureds could cause the overall performance to be unduly influenced by a relatively small number of underlying policies

that perform better or worse than expected.

Our

life expectancy actuarial results related to smaller portfolios may not be as reliable as they would be if the underlying portfolios

were larger. We understand that Standard & Poors has stated that at least 1,000 lives are required to achieve actuarial stability,

while A.M. Best concluded that at least 300 lives are necessary. Having fewer lives in a policy portfolio can cause the overall performance

of such portfolio to be unduly influenced by a relatively small number of “outliers” where the assets perform better or worse

than expected. The industry has sought to mitigate this risk by obtaining MRI coverage, which has the effect of accelerating cash flows

in cases where the assets underperform and reducing the volatility normally associated with a portfolio with fewer lives.

Increased

general market interests rates could increase the carrying costs of the life insurance policies and reduce the related cash flows.

If

general market interest rates increase, the value of life insurance portfolios would likely decrease. Some of the Holder’s carrying

costs associated with the life insurance policy portfolios (specifically interest payments on the MRI coverage outstanding balance) are

tied to interest rates. If interest rates increase, the Holder’s carrying costs will increase and the return on our investment

will decrease. Because the Holders pay all of the costs associated with the life insurance policy portfolios, an increase in the Holder’s

carrying costs will correspondingly decrease the amount cash flows.

In

addition, if the interest rates used to determine the market value of a life insurance policy change, the present value of the policy

may also change. Generally, as interest rates increase, the present value of a life insurance policy decreases. If a Holder is forced

to sell a policy in a higher interest rate environment, the market price for the policies may be less than the price at which such policy

was acquired. Furthermore, Holders are generally obligated under the senior loans financing the purchase of life insurance policies to

maintain certain loan to value ratios. If the present value of the life insurance policies decreases significantly, the Holder may be

in breach of such obligations, which could impair the Holder’s ability to obtain financing necessary to service existing life insurance

policies or acquire new policies. As a result, any life insurance portfolios may decline in value or become worthless.

Changes

to foreign banking laws and regulations or decreased lending capacity for life settlements could have a negative impact on the

ability of Holders to obtain loans with respect to purchases of life settlements.

Our

current business model relies on the availability to the Holders of senior loans from the Holders’ Lender or any other lender.

In the event of adverse regulatory changes or reduced capacity for life settlement lending, the Holders could experience the same liquidity

issues that have plagued other market participants. Changes to the Holders’ Lender’s loan to value requirements, compliance

with regulatory large exposure limits and changes to regulatory large exposure limits could also result in liquidity issues for the Holders

and corresponding liquidity issues for us. As mentioned above, changes in life expectancies could cause decreases in policy values, which

could result in loan to value violations and violations of large exposure limits.

Holders

may be required to obtain MRI coverage as a condition of our business model, which, if unavailable, could potentially increase our risk

of failure.

The

MRI is a relatively new product and there are no guarantees that the MRI provider will be able to meet the Holders’ coverage needs.