UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT

INVESTMENT COMPANIES

Investment

Company Act file number: 811-21846

Clough

Global Opportunities Fund

(exact

name of Registrant as specified in charter)

1700

Broadway, Suite 1850

Denver, Colorado 80290

(Address

of principal executive offices) (Zip code)

Chris

Moore, Secretary

Clough

Global Opportunities Fund

1700

Broadway, Suite 1850

Denver,

Colorado 80290

(Name

and address of agent for service)

Registrant’s

telephone number, including area code: 855-425-6844

Date

of fiscal year end: October 31

Date

of reporting period: November 1, 2022 – October 31, 2023

| Item

1. | Reports

to Stockholders. |

(a)

CLOUGH

GLOBAL DIVIDEND AND INCOME FUND

CLOUGH

GLOBAL EQUITY FUND

CLOUGH

GLOBAL OPPORTUNITIES FUND

Annual

Report

October

31, 2023

Clough

Global Funds

SECTION

19(B) DISCLOSURE

October

31, 2023 (Unaudited)

Clough

Global Dividend and Income Fund, Clough Global Equity Fund, and Clough Global Opportunities Fund (each a “Fund” and

collectively, the “Funds”), acting pursuant to a Securities and Exchange Commission (“SEC”) exemptive

order and with the approval of each Fund’s Board of Trustees (the “Board”), have adopted a plan, consistent

with each Fund’s investment objectives and policies to support a level distribution of income, capital gains and/or return

of capital (the “Plan”). In accordance with the Plan, the Funds’ managed distribution policy sets the monthly

distribution rate at an amount equal to one twelfth of 10% of each Fund’s adjusted year-ending net asset value (“NAV”),

which is the average of the NAVs as of the last five business days of the prior calendar year.

Under

the Plan, each Fund will distribute all available investment income to its shareholders, consistent with each Fund’s primary

investment objectives and as required by the Internal Revenue Code of 1986, as amended (the “Code”). If sufficient

investment income is not available on a monthly basis, each Fund will distribute long-term capital gains and/or return of capital

to shareholders in order to maintain a level distribution.

Each

monthly distribution to shareholders is expected to be at the fixed amount established by the Board, except for extraordinary

distributions and potential distribution rate increases to enable each Fund to comply with the distribution requirements imposed

by the Code.

Shareholders

should not draw any conclusions about each Fund’s investment performance from the amount of these distributions or

from the terms of the Plan. Each Fund’s total return performance on net asset value is presented in its financial

highlights table.

Each

Board may amend, suspend or terminate each Fund’s Plan without prior notice. The suspension or termination of the Plan could

have the effect of creating a trading discount (if a Fund’s stock is trading at or above net asset value) or widening an

existing trading discount. Each Fund is subject to risks that could have an adverse impact on its ability to maintain level distributions.

Examples of potential risks include, but are not limited to, economic downturns impacting the markets, increased market volatility,

companies suspending or decreasing corporate dividend distributions and changes in the Code. Please refer to the Notes to Financial

Statements in the Annual Report to Shareholders for a more complete description of its risks.

Please

refer to Additional Information for a cumulative summary of the Section 19(a) notices for each Fund’s current fiscal

period. Section 19(a) notices for each Fund, as applicable, are available on the Clough Global Closed-End Funds website

www.cloughcefs.com.

TABLE

OF CONTENTS

Clough

Global Funds

SHAREHOLDER

LETTER

October

31, 2023 (Unaudited)

To

Our Investors:

Clough

Global Dividend and Income Fund

For

the fiscal year ending October 31, 2023, the Clough Dividend and Income Fund (“GLV” or the “Fund”) declined

8.45% on net asset value (“NAV”) and 18.27% on market price. The Fund’s benchmark, the Morningstar Global Allocation

Total Return Index, gained 6.93% over the same period.

Technology

stocks and fixed income securities performed the best over the period, while healthcare and financials lagged.

Among

the Fund’s top five performers for the fiscal year, Broadcom Inc., a semiconductor company, gained in part due to expectations

for its generative artificial intelligence (“AI”) offering to be accretive to future growth. Microsoft Corp., the

large technology company, gained due to strength in its cloud business and expectations for the company to be a category leader

in AI. Airbus SE, the commercial aerospace company, gained on improved visibility in its backlog. The commercial aircraft cycle

is in an expansion phase which we think could last most of the decade. Comcast Corp., a media company, increased due to positive

earnings results relative to expectations. Lam Research Corp., a semiconductor company, gained on what we believe were early signs

of a memory recovery.

Among

the Fund’s bottom five performers for the fiscal year, put options on the S&P 500 Index detracted as stocks rose

during the period. Advance Auto Parts Inc., an automotive parts retailer, fell as the company missed earnings expectations

and cut its dividend. We exited the position. An options and futures position in securities which reflect the behavior of the

Secured Overnight Financing Rate (“SOFR”), a replacement for the London Interbank Offered Rate

(“LIBOR”), detracted as rates increased over the period. Bank of America Corp., the large bank, declined in part

due to lower net interest income (“NII”) expectations for the year. Northrop Grumman Corp., a large defense

contractor, underperformed after an earlier run up, but it remains one of the most diversified manufacturers of defense

systems and a large holding in the Fund.

During

the fiscal year we paid down $37 million in leverage in GLV, in part due to the higher cost of borrowing. In June 2023, we announced

a share repurchase program. The Fund repurchased and retired 202,800 shares of its common stock during the fiscal period.

Clough

Global Equity Fund

For

the fiscal year ending October 31, 2023, the Clough Global Equity Fund (“GLQ” or the “Fund”) declined

4.78% on net asset value (“NAV”) and 15.34% on market price. The Fund’s benchmark, the MSCI World Index, gained

11.05% over the same period.

Technology

and consumer discretionary stocks performed the best over the period, while healthcare and financials lagged.

Among

the Fund’s top five performers for the fiscal year, Microsoft Corp., the large technology company, gained due strength in

its cloud business and expectations for the company to be a category leader in artificial intelligence (“AI”). Broadcom

Inc., a semiconductor company, gained in part due to expectations for its generative AI offering to be accretive to future growth.

Royal Caribbean Cruises Ltd., a global cruise company, was among the top contributors as it recovered from two years of largely

idled operations to experience very strong demand. The company reported earnings results and guidance well ahead of Wall Street

estimates. TransDigm Group Inc., the aerospace manufacturing company, increased on the back of positive earnings revisions. Boeing

Co., a commercial aircraft manufacturer, gained on improved visibility in its backlog. The commercial aircraft cycle is in an

expansion phase which we think could last most of the decade.

Among

the Fund’s bottom five performers for the fiscal year, put options on the S&P 500 Index detracted as stocks rose

during the period. Crowdstrike Holdings Inc., a software company focused on cybersecurity, declined on a weak earnings report

as macroeconomic headwinds slowed growth. An options and futures position in securities which reflect the behavior of the

SOFR, a replacement for the LIBOR, detracted as rates increased over the period. Tesla Inc., a manufacturer of electric

vehicles, declined due to concerns over its reduced vehicle prices and implications on margins. Northrop Grumman Corp., a

large defense contractor, underperformed after an earlier run up, but it remains one of the most diversified manufacturers of

defense systems and a large holding in the Fund.

During

the fiscal year we paid down $81 million in leverage in GLQ, in part due to the higher cost of borrowing. In June 2023, we announced

a share repurchase program. The Fund repurchased and retired 284,700 shares of its common stock during the fiscal period.

Clough

Global Opportunities Fund

For

the fiscal year ending October 31, 2023, the Clough Global Opportunities Fund (“GLO” or the “Fund”) declined

4.49% on net asset value (“NAV”) and 16.38% on market price. The Fund’s benchmark, the Morningstar Global Allocation

Total Return Index, gained 6.93% over the same period.

Technology

and consumer discretionary stocks performed the best over the period, while healthcare and financials lagged.

Among

the Fund’s top five performers for the fiscal year, Broadcom Inc., a semiconductor company, gained in part due to expectations

for its generative artificial intelligence (“AI”) offering to be accretive to future growth and profitability. Microsoft

Corp., the large technology company, gained due strength in its cloud business and expectations for the company to be a category

leader in AI. Royal Caribbean Cruises Ltd., a global cruise company, was among the top contributors as it recovered from two years

of largely idled operations to experience very strong demand. The company reported earnings results and guidance well ahead of

Wall Street estimates. TransDigm Group Inc., the aerospace manufacturing company, increased on the back of positive earnings revisions.

Boeing Co., a commercial aircraft manufacturer, gained on improved visibility in its backlog. The commercial aircraft cycle is

in an expansion phase which we think could last most of the decade.

Among

the Fund’s bottom five performers for the fiscal year, put options on the S&P 500 Index detracted as stocks rose

during the period. Crowdstrike Holdings Inc., a software company focused on cybersecurity, declined on a weak earnings report

as macroeconomic headwinds slowed growth. An options and futures position in securities which reflect the behavior of the

SOFR, a replacement for the LIBOR, detracted as rates increased over the period. Centrexion Therapeutics Corp., a private

clinical stage biotechnology company, detracted in a challenging biotechnology market. Northrop Grumman Corp., a large

defense contractor, underperformed after an earlier run up, but it remains one of the most diversified manufacturers of

defense systems and a large holding in the Fund.

During

the fiscal year we paid down $152 million in leverage in GLO, in part due to the higher cost of borrowing. In June 2023, we announced

a share repurchase program. The Fund repurchased and retired 679,602 shares of its common stock during the fiscal period.

Clough

Global Funds

SHAREHOLDER

LETTER

October

31, 2023 (Continued) (Unaudited)

Market

Commentary

Inflation

has come down at one of the fastest rates in history, yet because of the economy’s resilience, real interest rates have

moved substantially higher. The combination of intensive fiscal stimulus and the consumer’s use of COVID savings supported

consumption and have impacted the positive effects of improvement on the inflation and wage fronts in the eyes of investors.

But

historically, when interest rates have risen this sharply, the economy has slowed, allowing the Federal Reserve (the “Fed”)

to ease, and equity returns in the following year have generally been strong. We believe signs of an interest rate peak would

rally stocks and it would not take much for equity returns to exceed even today’s high cash rate. In a weaker economy the

tradeoff would be between poor earnings and falling stocks in those parts of the economy where spending is vulnerable (largely

consumer stocks), and higher stock prices in sectors where growth would continue (largely companies which benefit from government

and corporate investment, including technology). We think large-capitalization technology stocks can go higher as AI takes hold,

but we also think the equity market can broaden out to smaller and midsize stocks. We are bullish on equities and bonds for the

following reasons:

Businesses

have been emphasizing free cash flow strategies and many have paid down debt. While Treasury yields rose during the fiscal year

ending October 31, 2023, prices of many high-yield corporate bonds held up well, quality credit spreads have come in. That suggests

the markets look at many businesses as being quite healthy.

The

Federal Reserve’s near $8 trillion balance sheet is flush with available reserves, enough we believe to handle any sudden

emergencies on the liquidity front— just note the quick resolution of the Silicon Valley and Signature Bank eruptions in

March 2023. With the Fed so liquidity rich and government and corporate investment spending supporting the economy, weaker consumer

spending alone is unlikely to cause recession but could slow the economy enough to cause the Fed to ease and the equity multiple

to rise.

There

are good values in equities. Seven large technology stocks plus Tesla Inc have dominated the rise in the S&P 500 Index and

NASDAQ Composite Index during the first 10 months of 2023, but the average S&P 500 Index stock is up much less on the year

and the Russell 2000 Index, an index of small- and medium-capitalization stocks, is down over the same period. We believe there

are many undervalued stocks in the equity marketplace. Investors hold trillions of dollars in cash, and we believe high interest

rates on cash will not last very long.

Bonds

have become attractive. Usually bond yields rise, and bond prices fall, when inflation is picking up, but that is not the case

today. All measures of inflation are falling; the Personal Consumption Expenditures Deflator, which the Fed follows, increased

at a 2.4% annual rate during Q3 2023. That is roughly where the Fed’s target is, suggesting it is finished raising interest

rates. As inflation falls further (rents are beginning to fall and they make up a large part of the Consumer Price Index (CPI)),

it threatens to bring on deflation in certain sectors, such as autos and airline fares.

Long-term

interest rates, as of October 31, 2023, should not stay this high for long. Foreigners continue to purchase large amounts of Treasury

bonds and with inflation declining demand from U.S. pension funds, insurance companies and endowments should rise. At these rates,

a life insurance company can fund a very profitable annuity flow and a pension or endowment fund can meet a 5% annual distribution

level without effort or risk. We see a huge potential demand for bonds once the economy slows and deflation becomes an increasing

likelihood.

The

consumer has been using COVID savings and aggressive use of installment credit to sustain spending. But those savings have seemingly

run out, credit card delinquencies are picking up and banks are restricting lending. Government spending and corporate investments

related to it are driving the economy and could help keep it stable, but once household spending slows, employment should decline

and that is what the Fed needs to see to ease.

We

hold a contrary view here, but once the Fed eases there are strong reasons to expect bank deposit rates to decline sharply. What

is new in this cycle is that money measures are declining, particularly M2, signaling bank deposits are falling and that is quite

unusual. This simply states that at current interest rates there are not enough assets banks can purchase to leverage the $20

trillion in deposits they hold. Without the Fed forcing interest rates higher, banks would be working overtime to reduce deposit

costs. Even today, simple checking account deposit rates yield 10 basis points, and that level is likely where deposit interest

rates would be if the Fed were not so aggressive.

As

always, please don’t hesitate to reach out to us with any questions or comments.

Sincerely,

Charles

I Clough, Jr.

William

Whelan

Clough

Global Funds

SHAREHOLDER

LETTER

October

31, 2023 (Continued) (Unaudited)

This

letter is provided for informational purposes only and is not an offer to purchase or sell shares. Clough Global Dividend and

Income Fund, Clough Global Equity Fund, and Clough Global Opportunities Fund (the “Funds”) are closed-end funds, which

are traded on the NYSE American LLC, and do not continuously issue shares for sale as open-end mutual funds do. The market price

of a closed-end fund is based on the market’s value.

Although

not generally stated throughout, the information in this letter reflects the opinions of the individual portfolio managers, which

opinion is subject to change, and is not intended to be a forecast of future events, a guarantee of future results or investment

advice.

The

Morningstar Global Allocation Index represents a multi-asset class portfolio of 60% global equities and 40% global bonds. The

asset allocation within each class is driven by Morningstar asset allocation methodology. To maintain broad global exposure and

diversification, the index consists of equities & fixed income and utilizes global, float-weighted index methodology to determine

allocation to U.S. and non-U.S.

The

MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance

of 23 developed markets countries. Effective July 31, 2010, the MSCI World Index returns prior to January 1, 2002 were revised

to reflect the total returns, with dividends reinvested, reported by MSCI. The MSCI information may only be used for your internal

use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments

or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or

refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not

be taken as an. indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided

on an “as is” basis and the user of this information assumes the entire risk of any use made of this information.

MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information

(collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties

of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with

respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any

direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages

(www.msci.com).

Both

indices referenced herein reflect the reinvestment of dividends. The performance of the indices referenced herein is used for

informational purposes only. One cannot invest directly in an index. Indices are not subject to any of the fees or expenses to

which the Funds are subject, and there are significant differences between the Funds’ investments and the components of

the indices referenced.

The

net asset value (“NAV”) of a closed-end fund is the market price of the underlying investments (i.e., stocks and bonds)

in the Funds’ portfolios, minus liabilities, divided by the total number of fund shares outstanding. However, the Fund also

has a market price; the value of which it trades on an exchange. This market price can be more or less than its NAV

RISKS

An

investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain an annual report

or semiannual report which contains this and other information visit www.cloughcefs.com or call 1-855-425-6844. Read them carefully

before investing.

The

Funds’ distribution policies will, under certain circumstances, have certain adverse consequences to the Funds and their

shareholders because it may result in a return of capital resulting in less of a shareholder’s assets being invested in

the Funds and, over time, increase the Funds’ expense ratios.

Distributions

may be paid from sources of income other than ordinary income, such as net realized short-term capital gains, net realized long-term

capital gains and return of capital. Based on current estimates, we anticipate the most recent distribution has been paid from

short-term and long-term capital gains. The actual amounts and sources of the amounts for tax reporting purposes will depend upon

the Funds’ investment experiences during the remainder of its fiscal year and may be subject to changes based on tax regulations.

If a distribution includes anything other than net investment income, the Funds provide a Section 19(a) notice of the best estimate

of its distribution sources at that time. These estimates may not match the final tax characterization (for the full year’s

distributions) contained in shareholders’ 1099-DIV forms after the end of the year.

The

Funds’ investments in securities of foreign issuers are subject to risks not usually associated with owning securities of

U.S. issuers. These risks can include fluctuations in foreign currencies, foreign currency exchange controls, social, political

and economic instability, differences in securities regulation and trading, expropriation or nationalization of assets, and foreign

taxation issues.

The

Funds’ investments in preferred stocks and bonds of below investment grade quality (commonly referred to as “high

yield” or “junk bonds”), if any, are predominately speculative because of the credit risk of their issuers.

An

investment by the Funds in real estate investment trusts (“REITs”) will subject it to various risks. The first, real

estate industry risk, is the risk that the REIT share prices will decline because of adverse developments affecting the real estate

industry and real property values. In general, real estate values can be affected by a variety of factors, including supply and

demand for properties, the economic health of the country or of different regions, and the strength of specific industries that

rent properties. The second, investment style risk, is the risk that returns from REITs—which typically are small or medium

capitalization stocks—will trail returns from the overall stock market. The third, interest rate risk, is the risk that

changes in interest rates may hurt real estate values or make REIT shares less attractive than other income-producing investments.

Credit risk is the risk that an issuer of a preferred or debt security will become unable to meet its obligation to make dividend,

interest and principal payments.

Interest

rate risk is the risk that preferred stocks paying fixed dividend rates and fixed-rate debt securities will decline in value

because of changes in market interest rates. When interest rates rise the value of such securities generally will fall.

Derivative transactions (such as futures contracts and options thereon, options, swaps, and short sales) subject the Funds to

increased risk of principal loss due to imperfect correlation or unexpected price or interest rate movements. Compared to

investment companies that focus only on large companies, the Funds’ share price may be more volatile because it also

invests in small and medium capitalization companies. Past performance is neither a guarantee, nor necessarily indicative, of

future results, which may be significantly affected by changes in economic and other conditions.

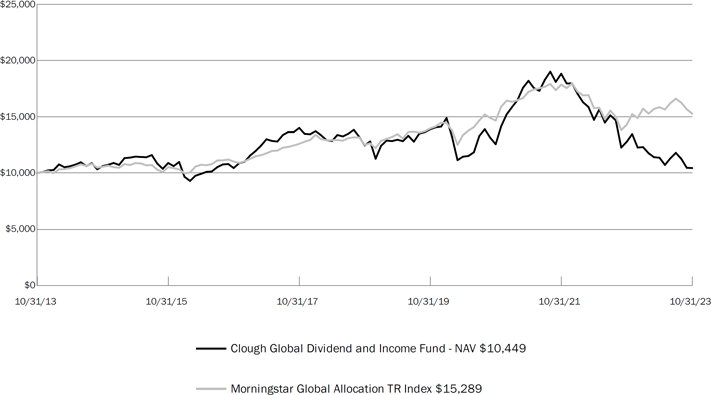

Clough

Global Dividend and Income Fund

PERFORMANCE

October

31, 2023 (Unaudited)

Growth

of $10,000 Investment

The

graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past

performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes

that a shareholder would pay on Fund distributions or the redemption of Fund shares

| Total Return as of October

31, 2023(a) |

|

|

|

|

|

| |

|

|

|

|

Since

Inception |

| |

1

Year |

3

Year(b) |

5

Year(b) |

10

Year(b) |

(7/28/2004)(b) |

| Clough

Global Dividend and Income Fund - NAV(c) |

-8.45% |

-5.17% |

-1.95% |

0.82% |

4.21% |

| Clough

Global Dividend and Income Fund - Market Price(d) |

-18.27% |

-5.88% |

-3.68% |

0.33% |

2.91% |

| Morningstar

Global Allocation TR Index |

6.93% |

1.35% |

4.09% |

4.34% |

5.98% |

| (a) | Total

returns assume reinvestment of all distributions. |

| (c) | Performance

returns are net of management fees and other Fund expenses. |

| (d) | Market

price is the value at which the Fund trades on an exchange. This market price can be more or less than its NAV. |

Distributions

to Common Shareholders

The

Fund intends to make monthly distributions to common shareholders according to its managed distribution policy. The Fund’s

managed distribution policy is to set the monthly distribution rate at an amount equal to one twelfth of 10% of the Fund’s

adjusted year-ending net asset value per share (“NAV”), which will be the average of the NAVs as of the last five

business days of the prior calendar year. The Board of Directors approve the distribution and may adjust it from time to time.

The monthly distribution amount paid from November 1, 2022 to December 31, 2022 was $0.0906 per share and the Fund paid $0.0597

per share monthly between January 1, 2023 and October 31, 2023. At times, to maintain a stable level of distributions, the Fund

may pay out less than all of its net investment income or pay out accumulated undistributed income, or return of capital, in addition

to current net investment income.

Clough

Global Dividend & Income Fund

FUND

ALLOCATION

October

31, 2023 (Unaudited)

| |

% of

Total |

| Global

Securities Holdings |

Portfolio(a) |

| United States of America |

57.79% |

| US Multinational(b) |

30.86% |

| South Korea |

3.01% |

| France |

2.44% |

| India |

2.13% |

| Sweden |

1.71% |

| Brazil |

1.55% |

| China |

1.45% |

| Ireland |

1.08% |

| Hong Kong |

0.28% |

| Spain |

-0.27% |

| Italy |

-0.61% |

| Germany |

-1.42% |

| TOTAL

INVESTMENTS |

100.00% |

| Asset

Allocation |

%

of Total Portfolio(a) |

| Common Stock - US |

45.28% |

| Common Stock - Foreign |

38.39% |

| Closed-End Funds |

0.24% |

| Preferred Stock |

1.32% |

| Exchange Traded Funds |

-0.91% |

| Total

Return Swap Contracts |

-0.27% |

| Total

Equities |

84.05% |

| |

|

| Corporate Bonds |

13.58% |

| Asset-Backed

Securities |

0.03% |

| Total

Fixed Income |

13.61% |

| |

|

| Money Market Funds |

2.31% |

| Purchased Options |

0.03% |

| Cash |

0.03% |

| Written

Options |

-0.03% |

| |

|

| TOTAL

INVESTMENTS |

100.00% |

| (a) | Percentages

calculated based on total portfolio, including securities sold short, cash balances, and notional value of return swaps. |

| (b) | U.S.

Multinationals includes companies organized or located in the United States that have more than 50% of revenues derived outside

of the United States. |

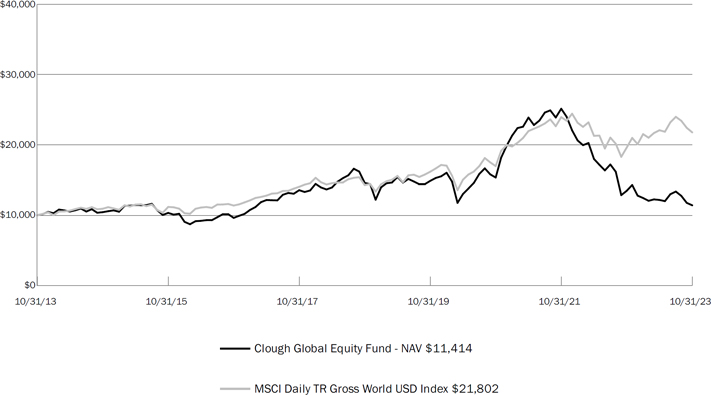

Clough

Global Equity Fund

PERFORMANCE

October

31, 2023 (Unaudited)

Growth

of $10,000 Investment

The

graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past

performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes

that a shareholder would pay on Fund distributions or the redemption of Fund shares

| Total Return as of October

31, 2023(a) |

|

|

|

|

|

| |

|

|

|

|

Since Inception |

| |

1

Year |

3

Year(b) |

5

Year(b) |

10

Year(b) |

(4/27/2005)(b) |

| Clough

Global Equity Fund - NAV(c) |

-4.78% |

-8.49% |

-1.35% |

2.16% |

4.66% |

| Clough

Global Equity Fund - Market Price(d) |

-15.34% |

-9.38% |

-5.11% |

1.17% |

3.17% |

| MSCI Daily

TR Gross World USD Index |

11.05% |

8.66% |

8.82% |

8.11% |

7.61% |

| (a) | Total

returns assume reinvestment of all distributions. |

| (c) | Performance

returns are net of management fees and other Fund expenses. |

| (d) | Market

price is the value at which the Fund trades on an exchange. This market price can be more or less than its NAV. |

Distributions

to Common Shareholders

The

Fund intends to make monthly distributions to common shareholders according to its managed distribution policy. The Fund’s

managed distribution policy is to set the monthly distribution rate at an amount equal to one twelfth of 10% of the Fund’s

adjusted year-ending net asset value per share (“NAV”), which will be the average of the NAVs as of the last five

business days of the prior calendar year. The Board of Directors approve the distribution and may adjust it from time to time.

The monthly distribution amount paid from November 1, 2022 to December 31, 2022 was $0.1162 per share and the Fund paid $0.0599

per share monthly between January 1, 2023 and October 31, 2023. At times, to maintain a stable level of distributions, the Fund

may pay out less than all of its net investment income or pay out accumulated undistributed income, or return of capital, in addition

to current net investment income.

Clough

Global Equity Fund

FUND

ALLOCATION

October

31, 2023 (Unaudited)

| |

% of

Total |

| Global

Securities Holdings |

Portfolio(a) |

| United States of America |

49.66% |

| US Multinational(b) |

36.94% |

| India |

4.34% |

| South Korea |

3.03% |

| China |

2.83% |

| France |

1.67% |

| Brazil |

1.62% |

| Hong Kong |

1.01% |

| Netherlands |

0.90% |

| Spain |

-0.29% |

| Italy |

-0.66% |

| Germany |

-1.05% |

| TOTAL

INVESTMENTS |

100.00% |

| Asset

Allocation |

%

of Total Portfolio(a) |

| Common Stock - Foreign |

50.41% |

| Common Stock - US |

46.97% |

| Closed-End Funds |

0.23% |

| Exchange Traded Funds |

0.12% |

| Total

Return Swap Contracts |

-0.29% |

| Total

Equities |

97.44% |

| |

|

| Convertible

Corporate Bonds |

0.03% |

| Total

Fixed Income |

0.03% |

| |

|

| Money Market Funds |

2.27% |

| Warrants |

0.24% |

| Purchased Options |

0.02% |

| Cash |

0.02% |

| Written

Options |

-0.02% |

| |

|

| TOTAL

INVESTMENTS |

100.00% |

| (a) | Percentages

calculated based on total portfolio, including securities sold short, cash balances, and notional value of return swaps. |

| (b) | U.S.

Multinationals includes companies organized or located in the United States that have more than 50% of revenues derived outside

of the United States. |

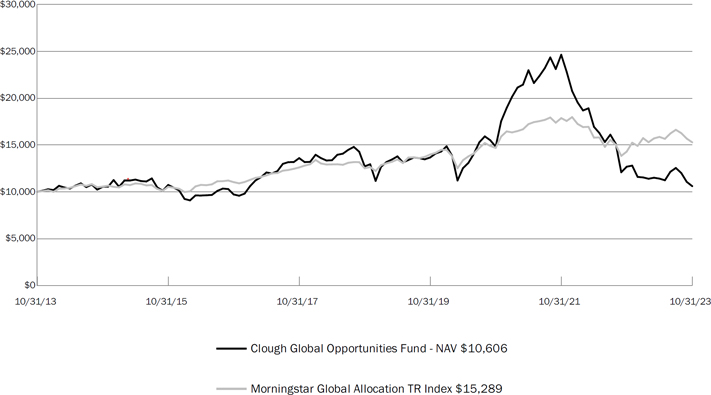

Clough

Global Opportunities Fund

PERFORMANCE

October

31, 2023 (Unaudited)

Growth

of $10,000 Investment

The

graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past

performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes

that a shareholder would pay on Fund distributions or the redemption of Fund shares

| Total Return as of October

31, 2023(a) |

|

|

|

|

|

| |

|

|

|

|

Since Inception |

| |

1

Year |

3

Year(b) |

5

Year(b) |

10

Year(b) |

(4/25/2006)(b) |

| Clough

Global Opportunities Fund - NAV(c) |

-4.49% |

-9.33% |

-1.51% |

1.34% |

2.93% |

| Clough

Global Opportunities Fund - Market Price(d) |

-16.38% |

-10.39% |

-3.45% |

0.65% |

1.46% |

| Morningstar

Global Allocation TR Index |

6.93% |

1.35% |

4.09% |

4.34% |

4.97% |

| (a) | Total

returns assume reinvestment of all distributions. |

| (c) | Performance

returns are net of management fees and other Fund expenses. |

| (d) | Market

price is the value at which the Fund trades on an exchange. This market price can be more or less than its NAV. |

Distributions

to Common Shareholders

The

Fund intends to make monthly distributions to common shareholders according to its managed distribution policy. The Fund’s

managed distribution policy is to set the monthly distribution rate at an amount equal to one twelfth of 10% of the Fund’s

adjusted year-ending net asset value per share (“NAV”), which will be the average of the NAVs as of the last five

business days of the prior calendar year. The Board of Directors approve the distribution and may adjust it from time to time.

The monthly distribution amount paid from November 1, 2022 to December 31, 2022 was $0.0943 per share and the Fund paid $0.0483

per share monthly between January 1, 2023 and October 31, 2023. At times, to maintain a stable level of distributions, the Fund

may pay out less than all of its net investment income or pay out accumulated undistributed income, or return of capital, in addition

to current net investment income.

Clough

Global Opportunities Fund

FUND

ALLOCATION

October

31, 2023 (Unaudited)

| |

% of

Total |

| Global

Securities Holdings |

Portfolio(a) |

| United States of America |

51.27% |

| US Multinational(b) |

34.54% |

| India |

3.87% |

| China |

2.53% |

| South Korea |

2.40% |

| Canada |

1.54% |

| Brazil |

1.53% |

| France |

1.48% |

| Ireland |

1.05% |

| Hong Kong |

0.95% |

| Netherlands |

0.84% |

| Spain |

-0.29% |

| Italy |

-0.66% |

| Germany |

-1.05% |

| TOTAL

INVESTMENTS |

100.00% |

| Asset

Allocation |

%

of Total Portfolio(a) |

| Common Stock - Foreign |

44.18% |

| Common Stock - US |

41.30% |

| Closed-End Funds |

0.22% |

| Exchange Traded Funds |

0.11% |

| Total

Return Swap Contracts |

-0.29% |

| Total

Equities |

85.52% |

| |

|

| Corporate Bonds |

12.60% |

| Convertible

Corporate Bonds |

0.03% |

| Total

Fixed Income |

12.63% |

| |

|

| Money Market Funds |

1.60% |

| Warrants |

0.23% |

| Purchased Options |

0.02% |

| Cash |

0.02% |

| Written

Options |

-0.02% |

| |

|

| TOTAL

INVESTMENTS |

100.00% |

| (a) | Percentages

calculated based on total portfolio, including securities sold short, cash balances, and notional value of return swaps. |

| (b) | U.S.

Multinationals includes companies organized or located in the United States that have more than 50% of revenues derived outside

of the United States. |

Clough

Global Dividend and Income Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023

| | |

Shares | | |

Value | |

| COMMON

STOCKS - 102.18% | |

| | | |

| | |

| Communication

Services - 3.99% | |

| | | |

| | |

| AT&T,

Inc.(a) | |

| 52,400 | | |

$ | 806,960 | |

| Comcast

Corp., Class A(a)(b) | |

| 42,200 | | |

| 1,742,438 | |

| Verizon

Communications, Inc.(a) | |

| 11,000 | | |

| 386,430 | |

| | |

| | | |

| 2,935,828 | |

| | |

| | | |

| | |

| Consumer

Discretionary - 15.00% | |

| | | |

| | |

| Autoliv,

Inc.(a) | |

| 14,250 | | |

| 1,306,012 | |

| BYD

Co. Ltd. | |

| 36,500 | | |

| 1,107,326 | |

| D.R.

Horton, Inc. | |

| 5,300 | | |

| 553,320 | |

| Home

Depot, Inc.(a)(b) | |

| 7,498 | | |

| 2,134,606 | |

| Lowe’s

Cos., Inc. | |

| 1,520 | | |

| 289,666 | |

| McDonald’s

Corp.(a)(b) | |

| 8,367 | | |

| 2,193,576 | |

| Meritage

Homes Corp. | |

| 1,700 | | |

| 193,834 | |

| PulteGroup,

Inc. | |

| 8,100 | | |

| 596,079 | |

| Starbucks

Corp.(a) | |

| 15,600 | | |

| 1,438,944 | |

| Wynn

Resorts, Ltd.(a) | |

| 14,210 | | |

| 1,247,354 | |

| | |

| | | |

| 11,060,717 | |

| | |

| | | |

| | |

| Consumer

Staples - 6.83% | |

| | | |

| | |

| Coca-Cola

Co.(a) | |

| 24,850 | | |

| 1,403,777 | |

| General

Mills, Inc.(a) | |

| 11,700 | | |

| 763,308 | |

| PepsiCo,

Inc.(a) | |

| 5,540 | | |

| 904,571 | |

| Procter

& Gamble Co.(a) | |

| 13,000 | | |

| 1,950,390 | |

| | |

| | | |

| 5,022,046 | |

| | |

| | | |

| | |

| Energy

- 5.76% | |

| | | |

| | |

| Chesapeake

Energy Corp.(a) | |

| 16,460 | | |

| 1,416,877 | |

| Chevron

Corp.(a) | |

| 8,300 | | |

| 1,209,559 | |

| Exxon

Mobil Corp.(a) | |

| 15,300 | | |

| 1,619,505 | |

| | |

| | | |

| 4,245,941 | |

| | |

| | | |

| | |

| Financials

- 8.70% | |

| | | |

| | |

| Bank

of America Corp.(a) | |

| 24,000 | | |

| 632,160 | |

| Charles

Schwab Corp. | |

| 10,400 | | |

| 541,216 | |

| HDFC

Bank Ltd. - ADR(a)(b) | |

| 15,500 | | |

| 876,525 | |

| ICICI

Bank Ltd. - Sponsored ADR(a)(b) | |

| 33,900 | | |

| 752,241 | |

| JPMorgan

Chase & Co.(a) | |

| 10,700 | | |

| 1,487,942 | |

| Morgan

Stanley(a) | |

| 18,550 | | |

| 1,313,711 | |

| Prudential

Financial, Inc.(a) | |

| 3,300 | | |

| 301,752 | |

| Starwood

Property Trust, Inc.(a)(b) | |

| 28,600 | | |

| 507,650 | |

| | |

| | | |

| 6,413,197 | |

| | |

Shares | | |

Value | |

| Health

Care - 14.50% | |

| | | |

| | |

| AbbVie,

Inc.(a)(b) | |

| 2,850 | | |

$ | 402,363 | |

| Amgen,

Inc.(a) | |

| 2,282 | | |

| 583,507 | |

| Encompass

Health Corp.(a) | |

| 15,300 | | |

| 957,168 | |

| Gilead

Sciences, Inc.(a) | |

| 6,300 | | |

| 494,802 | |

| HCA

Healthcare, Inc.(a) | |

| 3,230 | | |

| 730,432 | |

| Johnson

& Johnson(a) | |

| 12,007 | | |

| 1,781,118 | |

| Medtronic

PLC(a) | |

| 26,000 | | |

| 1,834,560 | |

| Merck

& Co., Inc.(a) | |

| 16,020 | | |

| 1,645,254 | |

| Sanofi(a) | |

| 13,200 | | |

| 597,300 | |

| Select

Medical Holdings Corp.(a) | |

| 32,700 | | |

| 743,271 | |

| Zimmer

Biomet Holdings, Inc.(a) | |

| 8,780 | | |

| 916,720 | |

| | |

| | | |

| 10,686,495 | |

| | |

| | | |

| | |

| Industrials

- 14.75% | |

| | | |

| | |

| Airbus

SE | |

| 19,794 | | |

| 2,644,813 | |

| Ferguson

PLC(a) | |

| 12,295 | | |

| 1,846,709 | |

| General

Dynamics Corp.(a) | |

| 10,060 | | |

| 2,427,579 | |

| Illinois

Tool Works, Inc.(a)(b) | |

| 1,793 | | |

| 401,847 | |

| Johnson

Controls International PLC | |

| 6,700 | | |

| 328,434 | |

| Lockheed

Martin Corp.(a) | |

| 815 | | |

| 370,532 | |

| Northrop

Grumman Corp.(a) | |

| 3,187 | | |

| 1,502,447 | |

| RTX

Corp.(a) | |

| 12,600 | | |

| 1,025,514 | |

| United

Parcel Service, Inc., Class B(a) | |

| 2,200 | | |

| 310,750 | |

| | |

| | | |

| 10,858,625 | |

| | |

| | | |

| | |

| Information

Technology - 22.59% | |

| | | |

| | |

| Accenture

PLC, Class A(a)(b) | |

| 3,097 | | |

| 920,088 | |

| Apple,

Inc.(a)(b) | |

| 13,880 | | |

| 2,370,288 | |

| Broadcom,

Inc.(a)(b) | |

| 1,475 | | |

| 1,241,021 | |

| Cisco

Systems, Inc.(a) | |

| 51,900 | | |

| 2,705,547 | |

| Lam

Research Corp.(a) | |

| 2,795 | | |

| 1,644,075 | |

| Microsoft

Corp.(a) | |

| 13,795 | | |

| 4,664,227 | |

| Samsung

Electronics Co., Ltd. | |

| 19,534 | | |

| 967,624 | |

| SK

Hynix, Inc. | |

| 15,515 | | |

| 1,336,044 | |

| Texas

Instruments, Inc.(a) | |

| 5,600 | | |

| 795,256 | |

| | |

| | | |

| 16,644,170 | |

| | |

| | | |

| | |

| Materials

- 5.26% | |

| | | |

| | |

| Dow,

Inc.(a) | |

| 31,200 | | |

| 1,508,208 | |

| Freeport-McMoRan,

Inc., Class B(a) | |

| 16,100 | | |

| 543,858 | |

| International

Paper Co.(a) | |

| 18,600 | | |

| 627,378 | |

| Vale

SA(a) | |

| 86,800 | | |

| 1,190,028 | |

| | |

| | | |

| 3,869,472 | |

| | |

| | | |

| | |

| Real

Estate - 1.35% | |

| | | |

| | |

| Simon

Property Group, Inc.(a) | |

| 4,800 | | |

| 527,472 | |

| VICI

Properties, Inc.(a) | |

| 16,500 | | |

| 460,350 | |

| | |

| | | |

| 987,822 | |

See

Notes to Financial Statements.

Clough

Global Dividend and Income Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023 (Continued)

| | |

| | |

| |

| | |

Shares | | |

Value | |

| Utilities

- 3.45% | |

| | | |

| | |

| Duke

Energy Corp.(a) | |

| 10,400 | | |

$ | 924,456 | |

| Exelon

Corp.(a)(b) | |

| 29,500 | | |

| 1,148,730 | |

| Hawaiian

Electric Industries, Inc. | |

| 35,900 | | |

| 465,982 | |

| | |

| | | |

| 2,539,168 | |

| | |

| | | |

| | |

| TOTAL

COMMON STOCKS | |

| | | |

| | |

| (Cost

$73,040,089) | |

| | | |

| 75,263,481 | |

| | |

| | | |

| | |

| CLOSED-END

FUNDS - 0.25% | |

| | | |

| | |

| BlackRock

Capital Allocation Trust(a)(b) | |

| 13,100 | | |

| 183,138 | |

| | |

| | | |

| | |

| TOTAL

CLOSED-END FUNDS | |

| | | |

| | |

| (Cost

$180,798) | |

| | | |

| 183,138 | |

| Description/Maturity

Date/Rate | |

| | |

| |

| PREFERRED

STOCKS - 1.37% | |

| | | |

| | |

| Gabelli Equity

Trust, Inc., Series K, Perpetual Maturity, 5.000%(a)(c) | |

| 21,200 | | |

| 448,168 | |

| Trinity

Capital, Inc., 1/16/2025, 7.000%(a) | |

| 22,400 | | |

| 565,600 | |

| | |

| | | |

| 1,013,768 | |

| | |

| | | |

| | |

| TOTAL

PREFERRED STOCKS | |

| | | |

| | |

| (Cost

$1,090,000) | |

| | | |

| 1,013,768 | |

| Underlying Security/Expiration Date/ | |

| | |

| |

| Exercise Price/Notional Amount | |

Contracts | | |

| |

| PURCHASED OPTIONS - 0.03% | |

| | | |

| | |

| Call Options Purchased - 0.03% | |

| | | |

| | |

| 3 Month SOFR | |

| | | |

| | |

| 12/15/2023, $97, $756,480,000 | |

| 3,200 | | |

| 20,000 | |

| | |

| | | |

| | |

| TOTAL PURCHASED OPTIONS | |

| | | |

| | |

| (Cost $1,351,732) | |

| | | |

| 20,000 | |

| | |

Principal | | |

| |

| Description/Maturity

Date/Rate | |

Amount | | |

| |

| CORPORATE

BONDS - 14.11% | |

| | | |

| | |

| Consumer

Discretionary - 2.56% | |

| | | |

| | |

| Carnival

Corp. | |

| | | |

| | |

| 3/1/2026,

7.625%(d)(e) | |

$ | 1,220,000 | | |

| 1,187,283 | |

| Melco

Resorts Finance Ltd. | |

| | | |

| | |

| 7/21/2028, 5.750%(a)(d)(e) | |

| 250,000 | | |

| 212,407 | |

| PulteGroup,

Inc. | |

| | | |

| | |

| 1/15/2027,

5.000%(a)(b) | |

| 500,000 | | |

| 486,124 | |

| | |

| | | |

| 1,885,814 | |

| | |

Principal | | |

| |

| Description/Maturity

Date/Rate | |

Amount | | |

Value | |

| Energy -

3.44% | |

| | | |

| | |

| NGL

Energy Operating LLC | |

| | | |

| | |

| 2/1/2026,

7.500%(d)(e) | |

$ | 940,000 | | |

$ | 918,437 | |

| Transocean,

Inc. | |

| | | |

| | |

| 2/1/2027,

8.000%(d)(e) | |

| 1,720,000 | | |

| 1,615,957 | |

| | |

| | | |

| 2,534,394 | |

| | |

| | | |

| | |

| Financials -

0.62% | |

| | | |

| | |

| Trinity

Capital, Inc. | |

| | | |

| | |

| 8/24/2026,

4.375%(a) | |

| 500,000 | | |

| 454,179 | |

| | |

| | | |

| | |

| Health

Care - 1.14% | |

| | | |

| | |

| Tenet

Healthcare Corp. | |

| | | |

| | |

| 10/1/2028,

6.125% | |

| 900,000 | | |

| 835,542 | |

| | |

| | | |

| | |

| Industrials -

5.01% | |

| | | |

| | |

| AerCap

Global Aviation Trust | |

| | | |

| | |

| 6/15/2045, 6.500%(d)(e) | |

| 840,000 | | |

| 824,927 | |

| Avis

Budget Car Rental, LLC | |

| | | |

| | |

| 7/15/2027, 5.750%(d)(e) | |

| 450,000 | | |

| 414,104 | |

| The

Hertz Corp. | |

| | | |

| | |

| 12/1/2026, 4.625%(d)(e) | |

| 390,000 | | |

| 327,046 | |

| TransDigm,

Inc. | |

| | | |

| | |

| 11/15/2027, 5.500%(a) | |

| 880,000 | | |

| 820,129 | |

| United

Airlines 2020-1 Class B Pass | |

| | | |

| | |

| Through

Trust | |

| | | |

| | |

| 1/15/2026, 4.875% | |

| 352,640 | | |

| 338,181 | |

| US

Airways 2012-2 Class A Pass | |

| | | |

| | |

| Through

Trust | |

| | | |

| | |

| 6/3/2025, 4.625%(a) | |

| 611,761 | | |

| 582,696 | |

| US

Airways 2013-1 Class A Pass | |

| | | |

| | |

| Through

Trust | |

| | | |

| | |

| 11/15/2025,

3.950%(a) | |

| 411,018 | | |

| 388,011 | |

| | |

| | | |

| 3,695,094 | |

| | |

| | | |

| | |

| Information

Technology - 1.34% | |

| | | |

| | |

| Apple,

Inc. | |

| | | |

| | |

| 5/6/2024,

3.450%(a) | |

| 1,000,000 | | |

| 989,752 | |

| | |

| | | |

| | |

| TOTAL

CORPORATE BONDS | |

| | | |

| | |

| (Cost

$10,668,105) | |

| | | |

| 10,394,775 | |

See

Notes to Financial Statements.

Clough

Global Dividend and Income Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023 (Continued)

| | |

Principal | | |

| |

| Description/Maturity

Date/Rate | |

Amount | | |

Value | |

| ASSET-BACKED

SECURITIES - 0.03% | |

| | | |

| | |

| United

States Small Business Administration 12/1/2028, 6.220%(a) | |

| 21,658 | | |

$ | 21,423 | |

| | |

| | | |

| | |

| TOTAL

ASSET-BACKED SECURITIES | |

| | | |

| | |

| (Cost

$21,658) | |

| | | |

| 21,423 | |

| | |

Shares | | |

| |

| MONEY

MARKET FUNDS - 2.40% | |

| | | |

| | |

| BlackRock

Liquidity Funds, T-Fund Portfolio, Institutional Class, 5.240% (7-day yield) | |

| 1,767,307 | | |

| 1,767,307 | |

| | |

| | | |

| | |

| TOTAL

MONEY MARKET FUNDS | |

| | | |

| | |

| (Cost

$1,767,307) | |

| | | |

| 1,767,307 | |

| | |

| | | |

| | |

| TOTAL

INVESTMENTS - 120.37% | |

| | | |

| | |

| (Cost

$88,119,689) | |

| | | |

| 88,663,892 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| Other

Liabilities in Excess of Assets - (20.37)%(f) | |

| | | |

| (15,004,266 | ) |

| | |

| | | |

| | |

| NET

ASSETS - 100.00% | |

| | | |

$ | 73,659,626 | |

| SCHEDULE OF SECURITIES

SOLD | |

| | |

| |

| SHORT | |

Shares | | |

Value | |

| COMMON

STOCKS - (15.23)% | |

| | | |

| | |

| Consumer

Discretionary - (6.77)% | |

| | | |

| | |

| Asbury Automotive

Group, Inc.(g) | |

| (4,280 | ) | |

| (819,063 | ) |

| AutoNation, Inc.(g) | |

| (6,800 | ) | |

| (884,544 | ) |

| Brunswick Corp. | |

| (10,500 | ) | |

| (729,435 | ) |

| Ford Motor Co. | |

| (64,560 | ) | |

| (629,460 | ) |

| Group 1 Automotive, Inc. | |

| (1,590 | ) | |

| (401,205 | ) |

| Harley-Davidson, Inc. | |

| (26,800 | ) | |

| (719,580 | ) |

| Lithia Motors, Inc. | |

| (1,480 | ) | |

| (358,471 | ) |

| YETI

Holdings, Inc.(g) | |

| (10,200 | ) | |

| (433,704 | ) |

| | |

| | | |

| (4,975,462 | ) |

| | |

| | | |

| | |

| Financials -

(3.15)% | |

| | | |

| | |

| BNP Paribas | |

| (5,439 | ) | |

| (312,439 | ) |

| Credit Agricole S.A. | |

| (28,071 | ) | |

| (337,949 | ) |

| Deutsche Bank AG | |

| (98,400 | ) | |

| (1,083,384 | ) |

| Intesa Sanpaolo SpA | |

| (69,163 | ) | |

| (179,770 | ) |

| Societe Generale S.A. | |

| (5,689 | ) | |

| (127,283 | ) |

| UniCredit

SpA | |

| (11,616 | ) | |

| (290,372 | ) |

| | |

| | | |

| (2,331,197 | ) |

| | |

| | | |

| | |

| Health

Care - (0.39)% | |

| | | |

| | |

| Cross

Country Healthcare, Inc.(g) | |

| (12,500 | ) | |

| (289,500 | ) |

| | |

| | |

| |

| | |

Shares | | |

Value | |

| Industrials

- (1.60)% | |

| | | |

| | |

| American

Airlines Group, Inc.(g) | |

| (14,600 | ) | |

$ | (162,790 | ) |

| AMETEK,

Inc. | |

| (1,800 | ) | |

| (253,386 | ) |

| Honeywell

International, Inc. | |

| (1,300 | ) | |

| (238,238 | ) |

| Jacobs

Solutions, Inc. | |

| (2,200 | ) | |

| (293,260 | ) |

| Rockwell

Automation, Inc. | |

| (900 | ) | |

| (236,529 | ) |

| | |

| | | |

| (1,184,203 | ) |

| | |

| | | |

| | |

| Information

Technology - (2.68)% | |

| | | |

| | |

| International

Business Machines Corp. | |

| (13,620 | ) | |

| (1,969,997 | ) |

| | |

| | | |

| | |

| Materials

- (0.64)% | |

| | | |

| | |

| O-I

Glass, Inc.(g) | |

| (30,400 | ) | |

| (469,680 | ) |

| | |

| | | |

| | |

| TOTAL

COMMON STOCKS | |

| | | |

| | |

| (Proceeds

$11,027,760) | |

| | | |

| (11,220,039 | ) |

| | |

| | | |

| | |

| EXCHANGE-TRADED

FUNDS - (0.95)% | |

| | | |

| | |

| Consumer

Staples Select Sector SPDR Fund | |

| (10,300 | ) | |

| (698,958 | ) |

| | |

| | | |

| | |

| TOTAL

EXCHANGE-TRADED FUNDS | |

| | | |

| | |

| (Proceeds

$729,180) | |

| | | |

| (698,958 | ) |

| | |

| | | |

| | |

| TOTAL

SECURITIES SOLD SHORT | |

| | | |

| | |

| (Proceeds

$11,756,940) | |

| | | |

| (11,918,997 | ) |

Investment

Abbreviations:

ADR

- American Depository Receipt

SOFR

- Secured Overnight Financing Rate

FEDEF

Rates:

1D

FEDEF - 1 day effective Federal Funds Rate as of October 31, 2023 was 5.33%

| (a) | Pledged

security; a portion or all of the security is pledged as collateral for securities sold

short or borrowings. As of October 31, 2023, the aggregate value of those securities

was $69,764,423, representing 94.71% of net assets. |

| (b) | Loaned

security; a portion or all of the security is on loan as of October 31, 2023. |

| (c) | This

security has no contractual maturity date, is not redeemable and contractually pays an

indefinite stream of interest. |

| (e) | All

or a portion of the security is exempt from registration of the Securities Act of 1933.

These securities may be resold in transactions exempt from registration under Rule 144A,

normally to qualified institutional buyers. As of October 31, 2023, these securities

had an aggregate value of $5,500,161 or 7.46% of net assets. |

| (f) | Includes

cash which is being held as collateral for securities sold short. |

| (g) | Non-income

producing security. |

See

Notes to Financial Statements.

Clough

Global Dividend and Income Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023 (Continued)

For

Fund compliance purposes, the Fund’s sector classifications refer to any one of the sector sub-classifications used by one

or more widely recognized market indexes, and/or as defined by Fund management. This definition may not apply for purposes of

this report, which may combine sector sub-classifications for reporting ease. Sectors are shown as a percent of net assets. These

sector classifications are unaudited.

Call

Options Written

| | |

| |

| |

| | |

| | |

| | |

| | |

| |

| Underlying Security | |

Counterparty | |

Expiration Date | |

Strike Price | | |

Contracts | | |

Premiums Received | | |

Notional

Value | | |

Value | |

| 3 Month SOFR | |

Morgan Stanley | |

12/15/2023 | |

$ | 98 | | |

| (3,200 | ) | |

$ | (516,486 | ) | |

$ | (756,480,000 | ) | |

$ | (20,000 | ) |

| | |

| |

| |

| | | |

| | | |

$ | (516,486 | ) | |

$ | (756,480,000 | ) | |

$ | (20,000 | ) |

Total

Return Swap Contracts

| Reference Entity/Obligation | |

Counterparty | |

Floating

Rate Received

by the Fund(a) | |

Termination

Date | |

Notional Value | | |

Value | | |

Net

Unrealized Depreciation | |

| Banco Bilbao Vizcaya Argenta | |

Morgan Stanley | |

1D FEDEF - 50 bps | |

10/2/2024 | |

$ | (118,014 | ) | |

$ | (205,086 | ) | |

$ | (87,072 | ) |

| | |

| |

| |

| |

$ | (118,014 | ) | |

$ | (205,086 | ) | |

$ | (87,072 | ) |

| (a) | Payment

received when swap contract closes. |

See

Notes to Financial Statements.

Clough

Global Equity Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023

| | |

Shares | | |

Value | |

| COMMON STOCKS - 119.38% | |

| | | |

| | |

| Communication Services - 7.32% | |

| | | |

| | |

| Alphabet, Inc.(a)(b)(c) | |

| 71,000 | | |

$ | 8,896,300 | |

| | |

| | | |

| | |

| Consumer Discretionary - 23.62% | |

| | | |

| | |

| Amazon.com, Inc.(a)(c) | |

| 41,270 | | |

| 5,492,624 | |

| Booking Holdings, Inc.(a)(c) | |

| 350 | | |

| 976,346 | |

| BYD Co. Ltd. | |

| 103,000 | | |

| 3,124,782 | |

| Carnival Corp.(a)(c) | |

| 131,100 | | |

| 1,502,406 | |

| D.R. Horton, Inc.(c) | |

| 8,600 | | |

| 897,840 | |

| DraftKings, Inc.(a)(c) | |

| 149,400 | | |

| 4,126,428 | |

| Home Depot, Inc.(b)(c) | |

| 2,979 | | |

| 848,092 | |

| Lowe’s Cos., Inc.(c) | |

| 7,920 | | |

| 1,509,314 | |

| Marriott International, Inc.(c) | |

| 2,700 | | |

| 509,112 | |

| McDonald’s Corp. | |

| 9,930 | | |

| 2,603,348 | |

| Melco Resorts & Entertainment Ltd. - ADR(a)(c) | |

| 155,600 | | |

| 1,313,264 | |

| Meritage Homes Corp.(c) | |

| 2,900 | | |

| 330,658 | |

| PulteGroup, Inc.(c) | |

| 5,900 | | |

| 434,181 | |

| Royal Caribbean Cruises Ltd.(a)(b)(c) | |

| 27,940 | | |

| 2,367,356 | |

| Trip.com Group Ltd. - ADR(a)(c) | |

| 16,100 | | |

| 547,400 | |

| Wynn Resorts, Ltd.(c) | |

| 24,080 | | |

| 2,113,742 | |

| | |

| | | |

| 28,696,893 | |

| | |

| | | |

| | |

| Consumer Staples - 3.45% | |

| | | |

| | |

| Coca-Cola Co.(c) | |

| 10,400 | | |

| 587,496 | |

| General Mills, Inc.(b)(c) | |

| 9,700 | | |

| 632,828 | |

| Kroger Co.(b)(c) | |

| 15,000 | | |

| 680,550 | |

| Procter & Gamble Co.(b)(c) | |

| 15,300 | | |

| 2,295,459 | |

| | |

| | | |

| 4,196,333 | |

| | |

| | | |

| | |

| Energy - 11.94% | |

| | | |

| | |

| Cheniere Energy, Inc.(b)(c) | |

| 14,600 | | |

| 2,429,732 | |

| Chesapeake Energy Corp.(c) | |

| 29,280 | | |

| 2,520,422 | |

| Diamondback Energy, Inc.(c) | |

| 3,800 | | |

| 609,216 | |

| Exxon Mobil Corp.(c) | |

| 19,250 | | |

| 2,037,613 | |

| Noble Corp PLC(a) | |

| 25,500 | | |

| 1,190,595 | |

| Schlumberger N.V.(c) | |

| 22,400 | | |

| 1,246,784 | |

| Southwestern Energy Co.(a)(c) | |

| 401,200 | | |

| 2,860,556 | |

| Transocean Ltd.(a)(c) | |

| 244,000 | | |

| 1,615,280 | |

| | |

| | | |

| 14,510,198 | |

| | |

| | | |

| | |

| Financials - 8.85% | |

| | | |

| | |

| Berkshire Hathaway, Inc., Class A(a)(c) | |

| 3 | | |

| 1,553,475 | |

| HDFC Bank Ltd. - ADR(b)(c) | |

| 55,300 | | |

| 3,127,215 | |

| ICICI Bank Ltd. - Sponsored ADR(b)(c) | |

| 112,500 | | |

| 2,496,375 | |

| JPMorgan Chase & Co.(c) | |

| 15,800 | | |

| 2,197,148 | |

| Starwood Property Trust, Inc.(b)(c) | |

| 24,400 | | |

| 433,100 | |

| Visa, Inc., Class A(c) | |

| 3,955 | | |

| 929,821 | |

| | |

| | | |

| 10,737,134 | |

| | |

Shares | | |

Value | |

| Health Care - 16.08% | |

| | | |

| | |

| Acadia Healthcare Co., Inc.(a)(b)(c) | |

| 7,050 | | |

$ | 518,246 | |

| Amphivena Therapeutics, Inc. Series C(a)(d)(e)(f)(g)(h) | |

| 334,425 | | |

| 375,860 | |

| Arcellx, Inc.(a)(b)(c) | |

| 20,164 | | |

| 710,781 | |

| Argenx SE(a)(c) | |

| 2,485 | | |

| 1,166,881 | |

| Centrexion Therapeutics Corp.(a)(d)(e)(f)(g)(h) | |

| 4,336 | | |

| 8,009 | |

| Centrexion Therapeutics Corp. Series D Preferred(a)(d)(e)(f)(g)(h) | |

| 66,719 | | |

| 123,230 | |

| Cigna Group(c) | |

| 1,662 | | |

| 513,890 | |

| Dexcom, Inc.(a)(c) | |

| 18,400 | | |

| 1,634,472 | |

| Elevance Health, Inc.(c) | |

| 1,575 | | |

| 708,892 | |

| Encompass Health Corp.(c) | |

| 16,000 | | |

| 1,000,960 | |

| HCA Healthcare, Inc.(c) | |

| 5,580 | | |

| 1,261,861 | |

| Johnson & Johnson(c) | |

| 12,359 | | |

| 1,833,334 | |

| Karuna Therapeutics, Inc.(a)(c) | |

| 6,650 | | |

| 1,107,957 | |

| Merck & Co., Inc.(b)(c) | |

| 16,680 | | |

| 1,713,036 | |

| Roivant Sciences Ltd.(a) | |

| 115,900 | | |

| 1,001,376 | |

| Sanofi(c) | |

| 47,600 | | |

| 2,153,900 | |

| Select Medical Holdings Corp.(b)(c) | |

| 54,200 | | |

| 1,231,966 | |

| Surgery Partners, Inc.(a)(b)(c) | |

| 28,300 | | |

| 654,579 | |

| Tenet Healthcare Corp.(a)(b)(c) | |

| 9,970 | | |

| 535,389 | |

| Zimmer Biomet Holdings, Inc.(c) | |

| 12,520 | | |

| 1,307,213 | |

| | |

| | | |

| 19,561,832 | |

| | |

| | | |

| | |

| Industrials - 17.04% | |

| | | |

| | |

| Airbus SE | |

| 26,732 | | |

| 3,571,847 | |

| Boeing Co.(a)(b)(c) | |

| 19,115 | | |

| 3,571,064 | |

| Ferguson PLC(c) | |

| 20,220 | | |

| 3,037,044 | |

| General Dynamics Corp.(c) | |

| 18,040 | | |

| 4,353,232 | |

| Hertz Global Holdings, Inc.(a)(b)(c) | |

| 38,700 | | |

| 326,241 | |

| Northrop Grumman Corp.(c) | |

| 5,543 | | |

| 2,613,137 | |

| TransDigm Group, Inc.(a)(c) | |

| 3,909 | | |

| 3,237,004 | |

| | |

| | | |

| 20,709,569 | |

| | |

| | | |

| | |

| Information Technology - 22.93% | |

| | | |

| | |

| Accenture PLC, Class A(b)(c) | |

| 5,075 | | |

| 1,507,732 | |

| Amphenol Corp., Class A(c) | |

| 5,900 | | |

| 475,245 | |

| Apple, Inc.(c) | |

| 18,020 | | |

| 3,077,275 | |

| Broadcom, Inc.(b)(c) | |

| 2,581 | | |

| 2,171,576 | |

| Cisco Systems, Inc.(c) | |

| 4,300 | | |

| 224,159 | |

| Lam Research Corp.(b)(c) | |

| 6,011 | | |

| 3,535,791 | |

| Microsoft Corp.(c) | |

| 25,400 | | |

| 8,587,994 | |

| NVIDIA Corp.(c) | |

| 3,535 | | |

| 1,441,573 | |

| Palo Alto Networks, Inc.(a)(b)(c) | |

| 6,208 | | |

| 1,508,668 | |

| Samsung Electronics Co., Ltd. | |

| 33,183 | | |

| 1,643,732 | |

| ServiceNow, Inc.(a)(c) | |

| 2,411 | | |

| 1,402,840 | |

| SK Hynix, Inc. | |

| 26,581 | | |

| 2,288,972 | |

| | |

| | | |

| 27,865,557 | |

See

Notes to Financial Statements.

Clough

Global Equity Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023 (Continued)

| | |

| | |

| |

| | |

Shares | | |

Value | |

| Materials

- 5.03% | |

| | | |

| | |

| Air

Products and Chemicals, Inc.(c) | |

| 2,537 | | |

$ | 716,550 | |

| Freeport-McMoRan,

Inc., Class B(c) | |

| 28,900 | | |

| 976,242 | |

| Linde

PLC(c) | |

| 4,287 | | |

| 1,638,320 | |

| Sherwin-Williams

Co.(b)(c) | |

| 2,887 | | |

| 687,712 | |

| Vale

SA(c) | |

| 152,900 | | |

| 2,096,259 | |

| | |

| | | |

| 6,115,083 | |

| | |

| | | |

| | |

| Real

Estate - 0.56% | |

| | | |

| | |

| Prologis,

Inc.(c) | |

| 3,200 | | |

| 322,400 | |

| Simon

Property Group, Inc.(c) | |

| 3,200 | | |

| 351,648 | |

| | |

| | | |

| 674,048 | |

| | |

| | | |

| | |

| Utilities

- 2.56% | |

| | | |

| | |

| Duke

Energy Corp.(b)(c) | |

| 10,800 | | |

| 960,012 | |

| Exelon

Corp.(c) | |

| 33,600 | | |

| 1,308,384 | |

| Hawaiian

Electric Industries, Inc.(c) | |

| 64,300 | | |

| 834,614 | |

| | |

| | | |

| 3,103,010 | |

| TOTAL

COMMON STOCKS | |

| | | |

| | |

| (Cost

$136,600,926) | |

| | | |

| 145,065,957 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| CLOSED-END

FUNDS - 0.25% | |

| | | |

| | |

| BlackRock

Capital Allocation Trust(c) | |

| 21,500 | | |

| 300,570 | |

| | |

| | | |

| | |

| TOTAL

CLOSED-END FUNDS | |

| | | |

| | |

| (Cost

$296,730) | |

| | | |

| 300,570 | |

| | |

| | | |

| | |

| | |

| | | |

| | |

| EXCHANGE-TRADED

FUNDS - 0.13% | |

| | | |

| | |

| United

States Natural Gas Fund, LP(a)(b)(c) | |

| 20,900 | | |

| 156,750 | |

| | |

| | | |

| | |

| TOTAL

EXCHANGE-TRADED FUNDS | |

| | | |

| | |

| (Cost

$406,467) | |

| | | |

| 156,750 | |

| | |

| | | |

| | |

| WARRANTS

- 0.25% | |

| | | |

| | |

| Hertz

Global Holdings, Inc. | |

| | | |

| | |

| Strike

Price $13.80, Expires | |

| | | |

| | |

| 6/30/2051(a)(c) | |

| 75,090 | | |

| 311,624 | |

| | |

| | | |

| | |

| TOTAL

WARRANTS | |

| | | |

| | |

| (Cost

$1,195,306) | |

| | | |

| 311,624 | |

| Underlying Security/Expiration

Date/ | |

| | |

| |

| Exercise

Price/Notional Amount | |

Contracts | | |

Value | |

| PURCHASED

OPTIONS - 0.02% | |

| | | |

| | |

| Call

Options Purchased - 0.02% | |

| | | |

| | |

| 3 Month SOFR | |

| | | |

| | |

| 12/15/2023,

$97, $1,182,000,000 | |

| 5,000 | | |

$ | 31,250 | |

| | |

| | | |

| | |

| TOTAL

PURCHASED OPTIONS | |

| | | |

| | |

| (Cost

$2,112,074) | |

| | | |

| 31,250 | |

| | |

| | | |

| | |

| | |

| Principal | | |

| | |

| Description/Maturity

Date/Rate | |

| Amount | | |

| | |

| CONVERTIBLE

CORPORATE BONDS - 0.03% | |

| | | |

| | |

| Health

Care - 0.03% | |

| | | |

| | |

| Amphivena

Convertible Note PP | |

| | | |

| | |

| 12/31/2049(a)(d)(e)(f)(g)(h) | |

| 108,750 | | |

| 32,625 | |

| | |

| | | |

| | |

| TOTAL

CONVERTIBLE CORPORATE BONDS | |

| | | |

| | |

| (Cost

$108,750) | |

| | | |

| 32,625 | |

| | |

| | | |

| | |

| | |

| Shares | | |

| | |

| MONEY

MARKET FUNDS - 2.42% | |

| | | |

| | |

| BlackRock

Liquidity Funds, T-Fund Portfolio, Institutional Class, 5.240% (7-day yield) | |

| 2,943,634 | | |

| 2,943,634 | |

| | |

| | | |

| | |

| TOTAL

MONEY MARKET FUNDS | |

| | | |

| | |

| (Cost

$2,943,634) | |

| | | |

| 2,943,634 | |

| | |

| | | |

| | |

| TOTAL

INVESTMENTS - 122.48% | |

| | | |

| | |

| (Cost

$143,663,887) | |

| | | |

| 148,842,410 | |

| | |

| | | |

| | |

| Other Liabilities in Excess of Assets - (22.48)%(i) | | |

| (27,323,300 | ) |

| |

| | | |

| | |

| NET ASSETS - 100.00% | |

| | | |

$ | 121,519,110 | |

| | |

| | | |

| | |

| SCHEDULE

OF SECURITIES SOLD | |

| | | |

| | |

| SHORT | |

| Shares | | |

| Value | |

| COMMON

STOCKS - (15.46)% | |

| | | |

| | |

| Consumer

Discretionary - (6.51)% | |

| | | |

| | |

| Asbury

Automotive Group, Inc.(a) | |

| (6,580 | ) | |

| (1,259,215 | ) |

| AutoNation,

Inc.(a) | |

| (10,450 | ) | |

| (1,359,336 | ) |

| Brunswick

Corp. | |

| (12,900 | ) | |

| (896,163 | ) |

| Ford

Motor Co. | |

| (128,280 | ) | |

| (1,250,730 | ) |

| Group

1 Automotive, Inc. | |

| (2,640 | ) | |

| (666,151 | ) |

| Harley-Davidson,

Inc. | |

| (44,400 | ) | |

| (1,192,140 | ) |

| Lithia

Motors, Inc. | |

| (2,450 | ) | |

| (593,414 | ) |

| YETI

Holdings, Inc.(a) | |

| (16,000 | ) | |

| (680,320 | ) |

| | |

| | | |

| (7,897,469 | ) |

See

Notes to Financial Statements.

Clough

Global Equity Fund

SCHEDULE

OF INVESTMENTS

October

31, 2023 (Continued)

| | |

Shares | | |

Value | |

| Financials

- (2.97)% | |

| | | |

| | |

| BNP

Paribas | |

| (9,800 | ) | |

$ | (562,954 | ) |

| Credit

Agricole S.A. | |

| (50,875 | ) | |

| (612,487 | ) |

| Deutsche

Bank AG | |

| (123,600 | ) | |

| (1,360,836 | ) |

| Intesa

Sanpaolo SpA | |

| (124,563 | ) | |

| (323,767 | ) |

| Societe

Generale S.A. | |

| (10,239 | ) | |

| (229,083 | ) |

| UniCredit

SpA | |

| (21,040 | ) | |

| (525,950 | ) |

| | |

| | | |

| (3,615,077 | ) |

| | |

| | | |

| | |

| Health

Care - (1.21)% | |

| | | |

| | |

| Cross

Country Healthcare, Inc.(a) | |

| (19,500 | ) | |

| (451,620 | ) |

| Danaher

Corp. | |

| (5,290 | ) | |

| (1,015,786 | ) |

| | |

| | | |

| (1,467,406 | ) |

| | |

| | | |

| | |

| Industrials

- (2.09)% | |

| | | |

| | |

| American

Airlines Group, Inc.(a) | |

| (24,500 | ) | |

| (273,175 | ) |

| AMETEK,

Inc. | |

| (2,800 | ) | |

| (394,156 | ) |

| Honeywell

International, Inc. | |

| (2,100 | ) | |

| (384,846 | ) |

| Jacobs

Solutions, Inc. | |

| (3,500 | ) | |

| (466,550 | ) |

| Paychex,

Inc. | |

| (6,000 | ) | |

| (666,300 | ) |

| Rockwell

Automation, Inc. | |

| (1,400 | ) | |

| (367,934 | ) |

| | |

| | | |

| (2,552,961 | ) |

| | |

| | | |

| | |

| Information

Technology - (2.07)% | |

| | | |

| | |

| International

Business Machines Corp. | |

| (17,370 | ) | |

| (2,512,397 | ) |

| | |

| | | |

| | |

| Materials

- (0.61)% | |

| | | |

| | |

| O-I

Glass, Inc.(a) | |

| (47,700 | ) | |

| (736,965 | ) |

| | |

| | | |

| | |

| TOTAL

COMMON STOCKS | |

| | | |

| | |

| (Proceeds

$18,669,892) | |

| | | |

| (18,782,275 | ) |

| | |

| | | |

| | |

| TOTAL

SECURITIES SOLD SHORT | |

| | | |

| | |

| (Proceeds

$18,669,892) | |

| | | |

| (18,782,275 | ) |

Investment

Abbreviations:

ADR

- American Depository Receipt

SOFR

- Secured Overnight Financing Rate

FEDEF

Rates:

1D

FEDEF - 1 day effective Federal Funds Rate as of October 31, 2023 was 5.33%

| (a) | Non-income

producing security. |

| (b) | Loaned

security; a portion or all of the security is on loan as of October 31, 2023. |

| (c) | Pledged

security; a portion or all of the security is pledged as collateral for securities sold

short or borrowings. As of October 31, 2023, the aggregate value of those securities

was $127,046,286, representing 104.55% of net assets. |

| (d) | All

or a portion of the security is exempt from registration of the Securities Act of 1933.

These securities may be resold in transactions exempt from registration under Rule 144A,

normally to qualified institutional buyers. As of October 31, 2023, these securities

had an aggregate value of $539,724 or 0.45% of net assets. |

| (e) | As

a result of the use of significant unobservable inputs to determine fair value, these

investments have been classified as Level 3 assets. |

| (g) | Fair

valued security; valued in accordance with procedures approved by the Board. As of October

31, 2023, these securities had an aggregate value of $539,724 or 0.45% of total net assets.

|

| (h) | Private

Placement; these securities may only be resold in transactions exempt from registration

under the Securities Act of 1933. As of October 31, 2023, these securities had an aggregate

value of $539,724 or 0.45% of net assets. |

| (i) | Includes

cash which is being held as collateral for securities sold short. |

For

Fund compliance purposes, the Fund’s sector classifications refer to any one of the sector sub-classifications used by one