Filed

pursuant to Rule 424(b)(5)

Registration

No. 333-277230

Prospectus

Supplement

(To

Prospectus dated March 1, 2024)

10,380,000

Ordinary Shares

Lichen

China Limited

This

is an offering of the securities of Lichen China Limited (the “Company”, “we”, “our”, “us”,

“Lichen China”, “Lichen China Limited”), a Cayman Islands exempted company with limited liability. This is a

self-underwritten offering of up to 10,380,000 Class A ordinary shares (the “Class A ordinary shares”), par value $0.00004

per share of the Company, directly to select investors pursuant to this prospectus and the accompanying prospectus at an offering price

of US$0.70 per Class A ordinary share.

Our

Class A ordinary shares are listed on The Nasdaq Capital Market, or Nasdaq, under the symbol “LICN.” On May 1, 2024, the

last reported sale price of our Class A ordinary shares on Nasdaq was US$1.33 per share.

The

aggregate market value of our outstanding Class A ordinary shares held by non-affiliates, or public float, as of May 1, 2024, was approximately

US$36.7 million, which was calculated based on 18,060,000 Class A ordinary shares held by non-affiliates as of May 1, 2024 and a per

share price of US$2.03, which was the closing price of our Class A ordinary shares on Nasdaq on April 29, 2024. Pursuant to General Instruction

I.B.5 of Form F-3, in no event will we sell the securities covered hereby in a public primary offering with a value exceeding more than

one-third of the aggregate market value of our ordinary shares in any 12-month period so long as the aggregate market value of our outstanding

ordinary shares held by non-affiliates remains below US$75,000,000. During the 12 calendar months prior to and including the date of

this prospectus supplement, we have not sold any securities pursuant to General Instruction I.B.5 of Form F-3.

Investors

are cautioned that you are not buying shares of a China-based operating company but instead are buying shares of a Cayman Islands

holding company with operations conducted by our subsidiaries based in China and that this structure involves unique risks to investors.

This

is an offering of the ordinary shares of the Cayman Islands holding company. We conduct our business through the PRC subsidiaries. You

will not and may never have direct ownership in the operating entity based in China. We do not use a Variable Interest Entity (“VIE”)

structure.

Throughout

this prospectus, unless the context indicates otherwise, references to “Lichen China”, “Lichen China Limited”,

“we,” “us,” the “Company,” “our company” refer to Lichen China Limited, a holding company.

References to “Subsidiaries,” “Operating Subsidiaries,” or “PRC subsidiaries” refer to the Lichen

China Limited’s subsidiaries established under the laws of the People’s Republic of China. References to “Group”

are to Lichen China Limited and its consolidated subsidiaries collectively.

Lichen

China Limited is a Cayman Islands holding company and is not a Chinese operating company. As a holding company with no material operations

of its own, it conducts all of its operations and operates its business in China through its PRC subsidiaries. Because of our corporate

structure as a Cayman Islands holding company with operations conducted by our PRC subsidiaries, it involves unique risks to investors.

Furthermore, Chinese regulatory authorities could change the rules and regulations regarding foreign ownership in the industry in which

the Company operates, which would likely result in a material change in our operations and/or a material change in the value of the securities

we are registering for sale, including that it could cause the value of such securities to significantly decline or become worthless.

Investors in our ordinary shares should be aware that they do not directly hold equity interests in the Chinese operating entities, but

rather are purchasing equity solely in Lichen China Limited, our Cayman Islands holding company, which indirectly owns 100% equity interests

in the PRC subsidiaries. Our ordinary shares offered in this offering are shares of our Cayman Islands holding company instead of shares

of our subsidiaries in China. See “Risk Factors — Risks Related to Doing Business in China — The

filing, approval or other administration requirements of the Chinese Securities Regulatory Commission (the “CSRC”) or other

PRC government authorities may be required in connection with our future offshore offering under PRC law, and, if required, we cannot

predict whether or for how long we will be able to complete the filing procedure with the CSRC and obtain such approval or complete such

filing, as applicable.” on page 14 of the accompanying prospectus and our most recent annual report on Form 20-F.

Investing

in our ordinary shares involves a high degree of risk. Before buying any ordinary shares, you should carefully read the discussion of

material risks of investing in our ordinary shares in “Risk Factors” beginning on page 13 of the accompanying prospectus

and our most recent annual report on Form 20-F.

The

Chinese government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through

regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those

relating to taxation, environmental regulations, land use rights, property and other matters. The central or local governments of these

jurisdictions may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures

and efforts on our part to ensure our compliance with such regulations or interpretations. Accordingly, government actions in the future,

including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional

or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular

regions thereof, and could require us to divest ourselves of any interest we then hold in Chinese properties. See “Risk Factors — Risks

Related to Doing Business in China — Uncertainties with respect to the PRC legal system, including uncertainties regarding

the enforcement of laws, and sudden or unexpected changes in laws and regulations in China with little advance notice could adversely

affect us and limit the legal protections available to you and us” on page 13 of the accompanying prospectus, “Any actions

by the Chinese government to exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based

issuers could significantly limit or completely hinder our ability to offer or continue to offer our Class A ordinary shares to investors

and cause the value of our Class A ordinary shares to significantly decline or be worthless. The M&A Rules and certain other PRC

regulations establish complex procedures for some acquisitions of Chinese companies by foreign investors, which could make it more difficult

for us to pursue growth through acquisitions in China” on page 16 of the accompanying prospectus, and “We may lose the ability

to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless

if the Chinese government may exert more oversight and control over offerings that are conducted overseas and/or foreign investment in

China-based issuers” on page 20 of the accompanying prospectus and our most recent annual report on Form 20-F.

In

particular, as substantially all of our operations are conducted through the PRC subsidiaries, we are subject to certain legal and operational

risks associated with our operations in China, including those changes in the legal, political and economic policies of the Chinese government,

the relations between China and the United States, or Chinese or United States regulations may materially and adversely affect

our business, financial condition and results of operations. PRC laws and regulations governing our current business operations are sometimes

vague and uncertain, and therefore, these risks could result in a material change in our operations and/or the value of our ordinary

shares or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause

the value of our ordinary shares to significantly decline or be worthless. Recently, the PRC government initiated a series of regulatory

actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities

in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure,

adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

As

confirmed by our PRC counsel, Tianyuan Law Firm, we will not be subject to cybersecurity review with the Cyberspace Administration of

China, or the “CAC,” after the Cybersecurity Review Measures became effective on February 15, 2022, since we currently

do not have over one million users’ personal information and do not anticipate that we will be collecting over one million users’

personal information in the foreseeable future, which we understand might otherwise subject us to the Cybersecurity Review Measures;

we are also not subject to network data security review by the CAC if the Draft Regulations on the Network Data Security Administration

are enacted as proposed, since we currently do not have over one million users’ personal information and do not collect data that

affects or may affect national security and we do not anticipate that we will be collecting over one million users’ personal information

or data that affects or may affect national security in the foreseeable future, which we understand might otherwise subject us to the

Security Administration Draft. See “Risk Factors — Risks Related to Doing Business in China.”

On

February 17, 2023, the China Securities Regulatory Commission, or the CSRC, announced the Circular on the Administrative Arrangements

for Filing of Securities Offering and Listing by Domestic Companies, or the Circular, and released a set of new regulations which consists

of the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, and five

supporting guidelines. On the same date, the CSRC also released the Notice on the Arrangements for the Filing Management of Overseas

Listing of Domestic Companies, or the Notice. The Trial Measures came into effect on March 31, 2023. The Trial Measures refine the

regulatory system by subjecting both direct and indirect overseas offering and listing activities to the CSRC filing-based administration.

Requirements for filing entities, time points and procedures are specified. A PRC domestic company that seeks to offer and list securities

in overseas markets shall fulfill the filing procedure with the CSRC per the requirements of the Trial Measures. Where a PRC domestic

company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity,

which shall, as the domestic responsible entity, file with the CSRC. The Trial Measures also lay out requirements for the reporting

of material events. Breaches of the Trial Measures, such as offering and listing securities overseas without fulfilling the filing procedures,

shall bear legal liabilities, including a fine between RMB 1.0 million (approximately $150,000) and RMB 10.0 million (approximately

$1.5 million), and the Trial Measures increase the cost for offenders by enforcing accountability with administrative penalties

and incorporating the compliance status of relevant market participants into the Securities Market Integrity Archives.

According

to the Circular, since the date of effectiveness of the Trial Measures on March 31, 2023, PRC domestic enterprises falling within

the scope of filing that have been listed overseas or met the following circumstances are “existing enterprises”: before

the effectiveness of the Trial Measures on March 31, 2023, the application for indirect overseas issuance and listing has been approved

by the overseas regulators or overseas stock exchanges (such as the registration statement has become effective on the U.S. market),

it is not required to perform issuance and listing supervision procedures of the overseas regulators or overseas stock exchanges, and

the overseas issuance and listing will be completed by September 30, 2023. Existing enterprises are not required to file with the

CSRC immediately, and filings with the CSRC should be made as required if they involve refinancings and other filing matters. PRC domestic

enterprises that have submitted valid applications for overseas issuance and listing but have not been approved by overseas regulatory

authorities or overseas stock exchanges at the date of effectiveness of the Trial Measures on March 31, 2023 can reasonably arrange

the timing of filing applications with the CSRC and shall complete the filing with the CSRC before the overseas issuance and listing.

In

addition, an overseas-listed company must also submit the filing with respect to its follow-on offerings, issuance of convertible corporate

bonds and exchangeable bonds, and other equivalent offering activities, within the time frame specified by the Trial Measures. As a result,

we will be required to file with the CSRC within three business days after the completion of the offerings in connection with this

registration statement. We will begin the process of preparing a report and other required materials in connection with the CSRC filing,

which will be submitted to the CSRC in due course. However, if we do not maintain the permissions and approvals of the filing procedure

in a timely manner under PRC laws and regulations, we may be subject to investigations by competent regulators, fines or penalties, ordered

to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering,

and these risks could result in a material adverse change in our operations, limit our ability to offer or continue to offer securities

to investors, or cause such securities to significantly decline in value or become worthless. As the Circular and Trial Measures were

newly published, there exists uncertainty with respect to the filing requirements and their implementation. Any failure or perceived

failure of us to fully comply with such new regulatory requirements could significantly limit or completely hinder our ability to offer

or continue to offer securities to investors, cause significant disruption to our business operations, and severely damage our reputation,

which could materially and adversely affect our financial condition and results of operations and could cause the value of our securities

to significantly decline or be worthless. See “Risk Factors — Risks Related to Doing Business in China — The

filing, approval or other administration requirements of the Chinese Securities Regulatory Commission (the “CSRC”) or other

PRC government authorities may be required in connection with our future offshore offering under PRC law, and, if required, we cannot

predict whether or for how long we will be able to complete the filing procedure with the CSRC and obtain such approval or complete such

filing, as applicable” on page 14 of the accompanying prospectus and our most recent annual report on Form 20-F.

As

of the date of this prospectus, according to our PRC counsel, Tianyuan Law Firm, although we are required to complete the filing procedure

in connection with our offerings under the Trial Measures, no relevant PRC laws or regulations in effect require that we obtain permission

from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice, warning, sanction, or

any regulatory objection to this offering from the CSRC, the CAC, or any other PRC authorities that have jurisdiction over our operations.

The

Standing Committee of the National People’s Congress, or the SCNPC, or other PRC regulatory authorities may in the future promulgate

laws, regulations or implementing rules that requires our company or any of our subsidiaries to obtain regulatory approval from Chinese

authorities before listing in the U.S. In other words, although the Company has not received any denial to list on the U.S. exchange,

our operations could be adversely affected, directly or indirectly; our ability to offer, or continue to offer, securities to investors

would be potentially hindered and the value of our securities might significantly decline or be worthless, by existing or future laws

and regulations relating to its business or industry or by intervene or interruption by PRC governmental authorities, if we or our subsidiaries

(i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals

are not required, (iii) applicable laws, regulations, or interpretations change and we are required to obtain such permissions or

approvals in the future, or (iv) any intervention or interruption by PRC governmental with little advance notice. See “Risk

Factors — Risks Related to Doing Business in China” beginning on page 13 of the accompanying prospectus and

our most recent annual report on Form 20-F for a discussion of these legal and operational risks and information that should be considered

before making a decision to purchase our ordinary shares.

In

addition, since 2021, the Chinese government has strengthened its anti-monopoly supervision, mainly in three aspects: (1) establishing

the National Anti-Monopoly Bureau; (2) revising and promulgating anti-monopoly laws and regulations, including: the Anti-Monopoly

Law (draft Amendment published on October 23, 2021 for public opinions), the anti-monopoly guidelines for various industries, and

the detailed Rules for the Implementation of the Fair Competition Review System; and (3) expanding the anti-monopoly law enforcement

targeting Internet companies and large enterprises. As of the date of this prospectus, the Chinese government’s recent statements

and regulatory actions related to anti-monopoly concerns have not impacted our ability to conduct business, accept foreign investments,

or list on a U.S. or other foreign exchange because neither the Company nor its PRC subsidiaries engage in monopolistic behaviors

that are subject to these statements or regulatory actions.

Pursuant

to the Holding Foreign Companies Accountable Act, or the HFCAA, if the Public Company Accounting Oversight Board, or the PCAOB, is unable

to inspect an issuer’s auditors for three consecutive years, the issuer’s securities are prohibited to trade on a U.S. stock

exchange. The PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate

completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because

of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency

of the PRC, because of a position taken by one or more authorities in Hong Kong. Furthermore, the PCAOB’s report identified

the specific registered public accounting firms which are subject to these determinations. On June 22, 2021, the U.S. Senate

passed the Accelerating Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated

Appropriations Act, 2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden, which contained,

among other things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act and amended the HFCAA by requiring

the SEC to prohibit an issuer’s securities from trading on any U.S stock exchanges if its auditor is not subject to PCAOB inspections

for two consecutive years instead of three, thus reducing the time period for triggering the prohibition on trading. On August 26,

2022, the PCAOB announced that it had signed a Statement of Protocol (the “SOP”) with the China Securities Regulatory Commission

and the Ministry of Finance of China. The SOP, together with two protocol agreements governing inspections and investigations (together,

the “SOP Agreement”), establishes a specific, accountable framework to make possible complete inspections and investigations

by the PCAOB of audit firms based in mainland China and Hong Kong, as required under U.S. law. On December 15, 2022, the

PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered

in mainland China and Hong Kong completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was

unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. However,

whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered

in mainland China and Hong Kong is subject to uncertainties and depends on a number of factors out of our and our auditor’s

control. The PCAOB continues to demand complete access in mainland China and Hong Kong moving forward and is making plans to resume

regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations

as needed. The PCAOB has also indicated that it will act immediately to consider the need to issue new determinations with the HFCAA

if needed.

Our

auditor, Enrome LLP, the independent registered public accounting firm, as an auditor of companies that are traded publicly in the United

States and a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections

to assess Enrome LLP’s compliance with applicable professional standards. Enrome LLP is headquartered in Singapore. As of the date

of this prospectus, Enrome LLP is not included in the list of PCAOB Identified Firms in the PCAOB Determination Report issued in December

2021. Our auditors, B&V for the fiscal year ended December 31, 2020 and TPS Thayer for the fiscal year ended December 31, 2021 and

2022, are both based in the U.S. B&V withdrew its registration from the PCAOB in January 2022. TPS Thayer is headquartered in Sugar

Land, Texas, and its registration with the PCAOB took effect in September 2020 and it is currently subject to PCAOB inspections. See

“Risk Factors — Risks Related to Doing Business in China — The recent joint statement by the SEC

and PCAOB, proposed rule changes submitted by Nasdaq, and the Holding Foreign Companies Accountable Act all call for additional and more

stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors

who are not inspected by the PCAOB. These developments could add uncertainties to our offering” on page 29 of the accompanying

prospectus and our most recent annual report on Form 20-F.

Our

management monitors the cash position of each entity within our organization regularly and prepare budgets on a monthly basis to ensure

each entity has the necessary funds to fulfill its obligation for the foreseeable future and to ensure adequate liquidity. In the event

that there is a need for cash or a potential liquidity issue, it will be reported to our Chief Financial Officer and subject to approval

by our board of directors, we will enter into an intercompany loan for the subsidiary in accordance with the applicable PRC laws and

regulations. However, the funds or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong

due to interventions in or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government

to transfer cash or assets. See “Risk Factors — Risks Related to Doing Business in China — To the

extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not

be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions

and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets.”

Under

existing PRC foreign exchange regulations, payment of current account items, such as profit distributions and trade and service-related

foreign exchange transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange,

or the SAFE, by complying with certain procedural requirements. Therefore, our PRC subsidiaries are able to pay dividends in foreign

currencies to us without prior approval from SAFE, subject to the condition that the remittance of such dividends outside of the PRC

complies with certain procedures under PRC foreign exchange regulations, such as the overseas investment registrations by our shareholders

or the ultimate shareholders of our corporate shareholders who are PRC residents. Approval from, or registration with, appropriate government

authorities is, however, required where the RMB is to be converted into foreign currency and remitted out of China to pay capital expenses

such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the

future to foreign currencies for current account transactions. Current PRC regulations permit our PRC subsidiaries to pay dividends to

the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations.

As of the date of this prospectus, there are no restrictions or limitations imposed by the Hong Kong government on the transfer

of capital within, into and out of Hong Kong (including funds from Hong Kong to the PRC), except for transfer of funds involving

money laundering and criminal activities. Cayman Islands law prescribes that a company may only pay dividends out of its profits or share

premium, and that a company may only pay dividends if, immediately following the date on which the dividend is paid, the company remains

able to pay its debts as they fall due in the ordinary course of business. Other than that, there is no restrictions on Lichen China

Limited’s ability to pay dividends to its shareholders. See “Prospectus Summary — Transfers of Cash to and

from Our Subsidiaries,” and “Risk Factors — Risks Related to Doing Business in China — To

the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may

not be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of

restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets,” “Risk

Factors — Risks Related to Doing Business in China — We are a holding company and we rely on our subsidiaries

for funding dividend payments, which are subject to restrictions under PRC laws,” and “Risk Factors — Risks

Related to Doing Business in China — Our PRC subsidiaries are subject to restrictions on paying dividends or making other

payments to us, which may have a material adverse effect on our ability to conduct our business.”

As

a holding company, we may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the

PRC, for our cash and financing requirements. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments

governing such debt may restrict their ability to pay dividends to us. Lichen China Limited is permitted under the laws of the Cayman

Islands to provide funding to our subsidiaries incorporated in Hong Kong through loans or capital contributions without restrictions

on the amount of the funds. Our subsidiaries are permitted under the respective laws of Hong Kong to provide funding to Lichen China

Limited through dividend distribution without restrictions on the amount of the funds. There are no restrictions on dividend transfers

from Hong Kong to the Cayman Islands. Current PRC regulations permit Fujian Province Lichen Management and Consulting Company Limited

(“Lichen WFOE” or “Lichen Zixun”) to pay dividends to the Company only out of its accumulated profits, if any,

determined in accordance with Chinese accounting standards and regulations. The transfer of funds among companies are subject to the

Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases

(2020 Revision, the “Provisions on Private Lending Cases”), which was implemented on August 20, 2020 to regulate the

financing activities between natural persons, legal persons and unincorporated organizations. As advised by our PRC counsel, Tianyuan

Law Firm, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund another subsidiary’s

operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’ ability to transfer cash

between PRC subsidiaries. During the fiscal years ended December 31, 2020, Lichen Zixun made dividend payments of RMB30 million (approximately

$4.3 million) to the then ultimate shareholders of Lichen Zixun, who are PRC individuals. The Company made no such dividend, distribution

or transfer during the fiscal year ended December 31, 2021. As of the date of this prospectus, except for the previously mentioned dividend

payments in fiscal year 2020, neither the Company nor its subsidiaries have made other transfers, dividends, or distributions to investors

and no investors have made transfers, dividends, or distributions to the Company or its subsidiaries. As of the date of this prospectus,

no dividends, distributions or transfers has been made between Lichen China Limited and any of its subsidiaries. We do not expect to

pay any cash dividends in the foreseeable future. Also, as of the date of this prospectus, no cash generated from one subsidiary is used

to fund another subsidiary’s operations and we do not anticipate any difficulties or limitations on our ability to transfer cash

between subsidiaries. See “Prospectus Summary — Transfers of Cash to and from Our Subsidiaries” on page 7

of the accompanying prospectus and “Consolidated Financial Statements” incorporated by reference into this prospectus.

This

is a self-underwritten offering. See “Plan of Distribution” beginning on page S-28 of this prospectus supplement for

more information regarding these arrangements.

We

are an “emerging growth company” as defined under federal securities laws and, as such, will be subject to reduced public

company reporting requirements. See “Prospectus Summary — Implications of Being an Emerging Growth Company”

and “Prospectus Summary — Implications of Being a Foreign Private Issuer” on page 5 of the accompanying

prospectus for additional information.

Investing

in our securities being offered pursuant to this prospectus involves a high degree of risk. You should carefully read and consider the

‘‘Risk Factors’’ section of this prospectus, and risk factors set forth

in our most recent annual report on Form 20-F, in other reports incorporated herein by reference, and in the applicable prospectus

supplement before you make your investment decision.

Neither

the Securities and Exchange Commission, the Cayman Islands Monetary Authority, nor any state securities commission has approved or disapproved

of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| | |

Per

ordinary share | | |

Total | |

| Public offering price | |

$ | 0.70 | | |

$ | 7,266,000 | |

| Proceeds, before expenses, to us | |

$ | 0.70 | | |

$ | 7,266,000 | |

We

expect that delivery of the Class A ordinary shares being offered pursuant to this prospectus supplement and the accompanying prospectus

will be made on or about May 7, 2024, subject to customary closing conditions.

The

date of this prospectus supplement is May 2, 2024.

TABLE

OF CONTENTS

Prospectus

Supplement

Prospectus

ABOUT

THIS PROSPECTUS SUPPLEMENT

On

February 21, 2024, we filed with the U.S. Securities and Exchange Commission (the “SEC”) a registration statement on Form

F-3 (File No.333-277230), utilizing a shelf registration process relating to the securities described in this prospectus supplement,

which registration statement was declared effective by the SEC on March 1, 2024. Under this shelf registration process, we may, from

time to time, in one or more offerings, offer and sell up to US$100,000,000 of any combination, together or separately, of our Class

A ordinary shares, debt securities, warrants, rights, and units, or any combination thereof as described in the accompanying prospectus.

We are selling Class A ordinary shares in this offering.

This

document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering and also

adds to and updates information contained in the accompanying prospectus and the documents incorporated by reference into the prospectus

supplement. The second part, the accompanying prospectus, gives more general information, some of which does not apply to this offering.

You should read this entire prospectus supplement as well as the accompanying prospectus and the documents incorporated by reference

that are described under “Incorporation of Documents by Reference” and “Where You Can Find Additional Information”

in this prospectus supplement and the accompanying prospectus.

If

the description of the offering varies between this prospectus supplement and the accompanying prospectus, you should rely on the information

contained in this prospectus supplement. However, if any statement in one of these documents is inconsistent with a statement in another

document having a later date—for example, a document incorporated by reference in this prospectus supplement and the accompanying

prospectus—the statement in the document having the later date modifies or supersedes the earlier statement. Except as specifically

stated, we are not incorporating by reference any information submitted under any Report of Foreign Private Issuer on Form 6-K into this

prospectus supplement or the accompanying prospectus.

Any

statement contained in a document incorporated by reference, or deemed to be incorporated by reference, into this prospectus supplement

or the accompanying prospectus will be deemed to be modified or superseded for purposes of this prospectus supplement or the accompanying

prospectus to the extent that a statement contained herein, therein or in any other subsequently filed document which also is incorporated

by reference in this prospectus supplement or the accompanying prospectus modifies or supersedes that statement. Any such statement so

modified or superseded will not be deemed, except as so modified or superseded, to constitute a part of this prospectus supplement or

the accompanying prospectus.

We

further note that the representations, warranties, and covenants made by us in any agreement that is filed as an exhibit to any document

that is incorporated by reference in this prospectus supplement and the accompanying prospectus were made solely for the benefit of the

parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreements, and should

not be deemed to be a representation, warranty or covenant to you unless you are a party to such agreement. Moreover, such representations,

warranties, or covenants were accurate only as of the date when made or expressly referenced therein. Accordingly, such representations,

warranties, and covenants should not be relied on as accurately representing the current state of our affairs unless you are a party

to such agreement.

COMMONLY

USED DEFINED TERMS

Throughout

this prospectus, unless the context indicates otherwise, references to “Lichen China”, “Lichen China Limited”,

“we,” “us,” the “Company,” “our company” refer to Lichen China Limited, a holding company.

References to “Subsidiaries,” “Operating Subsidiaries,” or “PRC subsidiaries” refer to the Lichen

China Limited’s subsidiaries established under the laws of the People’s Republic of China. References to “Group”

are to Lichen China Limited and its consolidated subsidiaries collectively. Unless otherwise indicated, in this prospectus, references

to:

| ● | “China”

or the “PRC” are to the People’s Republic of China; |

| ● | “Class

A ordinary shares” are to a class of shares of Lichen China Limited called the “series A ordinary shares” with par

value $0.00004 per share; |

| ● | “Class

B ordinary shares” are to a class of shares of Lichen China Limited called the “series B ordinary shares” with par

value $0.00004 per share; |

| ● | “HKD”

are to the official currency of Hong Kong; |

| ● | “Lichen

China” or “LICN” are to Lichen China Limited, a Cayman Islands exempted company; |

| ● | “Legend

Consulting BVI” are to Legend Consulting Investments Limited, a British Virgin Islands exempted company and a wholly-owned subsidiary

of Lichen China; |

| |

●

|

“Legend

Consulting HK” are to Legend Consulting Limited (HK), a Hong Kong company and a wholly-owned subsidiary of Legend Consulting

BVI; |

| ● | “Lichen

WFOE” or “Lichen Zixun” are to Fujian Province Lichen Management and Consulting Company Limited, a wholly foreign-owned

company organized under the laws of the PRC and a wholly-owned subsidiary of Legend Consulting HK; |

| ● | “Lichen

Education” are to Xiamen City Legend Education Services Company Limited, a limited liability company organized under the laws of

the PRC and a wholly-owned subsidiary of Lichen WFOE; |

| ● | “RMB”

are to Renminbi, or the legal currency of the PRC; |

| ● | “U.S.

dollars,” “$,” and “USD” are to the legal currency of the United States; and |

| ● | “WFOE”

are to wholly foreign-owned enterprise. |

SPECIAL

NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This

prospectus supplement includes and incorporates forward-looking statements within the meaning of Section 27A of the Securities Act of

1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act. We intend such forward-looking statements to

be covered by the safe harbor provisions for forward-looking statements contained in the United States Private Securities Litigation

Reform Act of 1995. All statements, other than statements of historical facts, included or incorporated by reference in this prospectus

supplement and the accompanying prospectus regarding our strategy, future operations, financial position, future revenues, projected

costs, prospects, plans and objectives of management, including, without limitation, the discussion of whether and when potential acquisition

transactions will close, expectations concerning our ability to increase our revenue, expectations with respect to operational efficiency,

expectations regarding financing, and expectations concerning our business strategy, under “Prospectus Supplement Summary - Recent

Developments,” are forward-looking statements. The words “anticipates,” “believes,” “estimates,”

“expects,” “intends,” “may,” “plans,” “projects,” “will,” “would”

and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these

identifying words. We cannot guarantee that we actually will achieve the plans, intentions or expectations disclosed in our forward-looking

statements and you should not place undue reliance on our forward-looking statements. There are a number of important factors that could

cause our actual results to differ materially from those indicated by these forward-looking statements. These important factors include

the factors that we identify in the documents we incorporate by reference in this prospectus supplement and the accompanying prospectus,

as well as other information we include or incorporate by reference in this prospectus supplement and the accompanying prospectus. See

“Risk Factors.” You should read these factors and other cautionary statements made in this prospectus supplement and the

accompanying prospectus, and in the documents we incorporate by reference as being applicable to all related forward-looking statements

wherever they appear in this prospectus supplement and the accompanying prospectus, and in the documents incorporated by reference herein

and therein. We do not assume any obligation to update any forward-looking statements made by us except to the extent required by law.

PROSPECTUS

SUPPLEMENT SUMMARY

This

summary highlights selected information about us, this offering and information contained in greater detail elsewhere in this prospectus

supplement, the accompanying prospectus, and in the documents incorporated by reference. This summary is not complete and does not contain

all of the information that you should consider before investing in our securities. You should carefully read and consider this entire

prospectus supplement, the accompanying prospectus and the documents, including financial statements and related notes, and information

incorporated by reference into this prospectus supplement, including the financial statements and “Risk Factors” starting

on pages S-13 of this prospectus supplement, before making an investment decision. If you invest in our securities, you are assuming

a high degree of risk.

Business

Overview

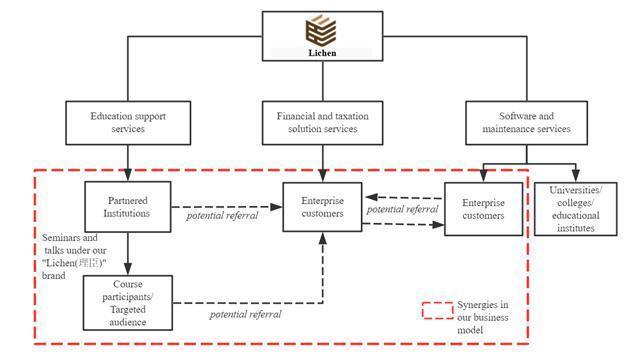

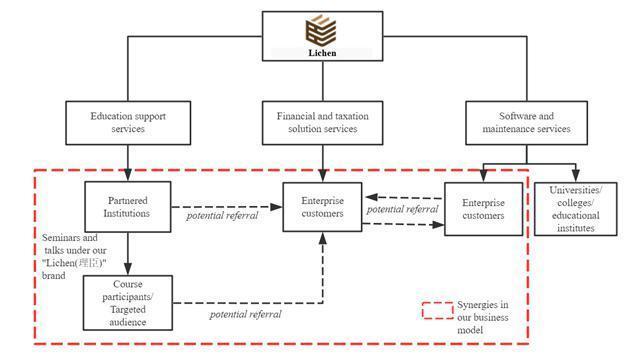

Through

our PRC subsidiaries, we provide (i) financial and taxation solution services; (ii) education support services; and (iii) software and

maintenance services in the PRC. The connections and synergies amongst our services are illustrated in the diagram below:

The

financial and taxation solution services provided to our corporate customers mainly comprise financial and taxation related management

consultation, internal control management consultation, annual or regular consultation, and internal training and general consultation.

The

education support services provided to our partnered institutions (“Partnered Institutions”) mainly comprise the provision

of marketing, operational and technical support and the sales of teaching and learning materials.

The

software and maintenance services provided to our corporate customers mainly comprise the sales of financial and taxation analysis software

and sales of financial and taxation training software.

Financial

and Taxation Solution Services

We

focus on our financial and taxation solution services to business companies in the PRC. We believe that every company, regardless of

its size, should adopt a sound financial and taxation management system for growth and sustainable development. With such philosophy

in mind as a guiding principle, our financial and taxation solution services are customized based on the specific needs and requirements

of individual customers.

Education

Support Services

Our

education support services are provided to our Partnered Institutions. As of the date of this prospectus, we collaborate with 23 Partnered

Institutions in 11 provinces or municipalities and 20 cities in the PRC. Partnered Institutions are education services providers

which mainly engage in organization of various seminars, talks and training courses to entrepreneurs, senior executives as well as financial

and taxation executives. From the personal and business networks of our management as well as our marketing initiatives (being our talks

and seminars hosted by the Partnered Institutions), potential customers who wish to set up education institutions may approach us and

initiate discussions with us, with an aim to becoming our Partnered Institutions.

Software

and Maintenance Services

Lichen

Zixun has been providing financial and taxation training software and academic affairs management system to our Partnered Institutions

as part of our services under the Partnership Agreements.

Leveraging

our understanding of corporate needs on financial and taxation management and analysis tools in daily operation of our enterprise customers,

we began to invest and develop our first financial and taxation analysis software, namely, Enterprise Financial Intelligence Analysis

System V1.0, in 2017 and have commercialized it for sale to our corporate customers since 2019.

With

respect to our Lichen Education Accounting Practice System V1.0, a financial and taxation training system that was developed in 2014,

it is focused on students’ or users’ practice experience by resembling, illustrating and providing practices on various accounting

tasks, such as bookkeeping, tax computation, filing tax returns and issuing valued-added tax invoices in actual business practices. Thereafter,

we updated and developed some new training systems based on Lichen Education Accounting Practice System V1.0. Lichen Education has eight

copyrights for financial and taxation training software to date.

As

of the date of this prospectus, we have not experienced any product recalls, liability claims or material complaints on our software

products.

After

Sales Services

Our

customers who engage us for our financial and taxation related consultation services may attend courses provided by our Partnered Institutions.

Continuous training can enhance the financial and taxation concepts of our customers and ensure the continuous implementation of the

financial and taxation solutions we provided to them. We also provide general customer care by responding to customer queries as they

arise, in order to resolve their problems on a timely basis.

From

time to time, the Partnered Institutions will also host talks and seminars, conducted by our experienced senior management personnel,

internal consultants or external experts, to which our customers are invited. As for our Partnered Institutions, we provide continuous

support to them, including operational and technical support in school management and operation and trainings to Partnered Institutions’

staff and employees to enhance their teaching quality. With respect to our software products, we offer software installation, training

and after sales technical and maintenance services, such as telephone, instant communication and remote support services, within one

year of purchase for our financial and taxation training software and financial and taxation analysis software.

Sales

and Marketing

We

believe brand recognition of “Lichen” is critical to our ability to attract new customers and retain business collaboration

and relationship with our existing clientele, and our promotion and marketing efforts are designed to enhance our brand awareness and

reputations among them. Generally, we attract new customers with referrals from our Partnered Institutions and personal and business

networks of our executives and directors.

In

addition, we organize marketing activities, such as seminars, talks and consultation events with our Partnered Institutions, business

federations and business associations, leveraging our accumulated resources and connections. Through the business relationships with

our Partnered Institutions, we could, on the one hand, provide our education support services to them and, on the other hand, by leveraging

their business networks and their geographical coverage, promote our brand name and services to the participants of these seminars, talks

and courses organized by them. As of the date of this prospectus, we have deployed external experts and internal consultants to participate

in and deliver more than 1,000 talks, courses and seminars organized for their target audience.

Corporate

History and Structure

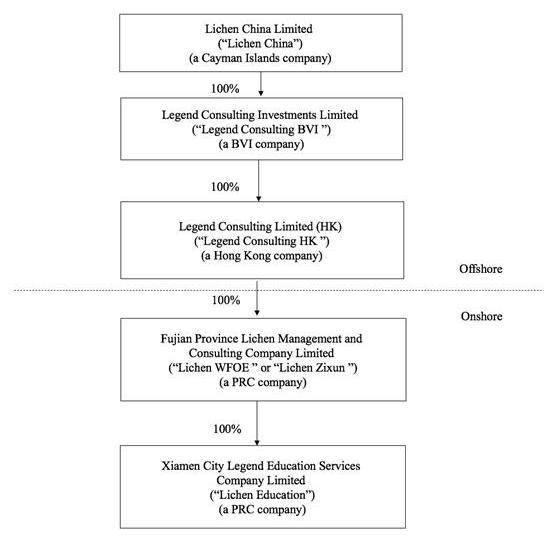

The

following diagram illustrates the corporate structure of Lichen China Limited and its significant subsidiaries as of the date of this

prospectus.

Holding

Company Structure

Lichen

China Limited was incorporated on April 13, 2016 under the laws of the Cayman Islands. As of the date of this prospectus, the authorized

share capital of the Company is US$50,000 divided into 1,000,000,000 Class A Ordinary Shares and 250,000,000 Class B Ordinary Shares,

of which 18,370,000 Class A Ordinary Shares and 9,000,000 Class B Ordinary Shares are issued and outstanding. The Company is a holding

company and is currently not actively engaging in any business. Lichen China Limited controls and receives the economic benefits of its

PRC subsidiaries’ business operation, if any, through equity ownership.

Legend

Consulting BVI was incorporated on December 20, 2013 under the laws of the British Virgin Islands with limited liability. Legend Consulting

BVI is a wholly owned subsidiary of the Company. Legend Consulting BVI is a holding company and is currently not actively engaging in

any business.

Legend

Consulting HK was formed on January 8, 2014 under the laws of Hong Kong. Legend Consulting HK is a wholly owned subsidiary of Legend

Consulting BVI. It is a holding company and is not actively engaging in any business.

Lichen

Zixun was established on April 14, 2004 under the laws of the PRC. Lichen Zixun is a wholly owned subsidiary of Legend Consulting HK

and is our main operating entity.

Lichen

Education was established on July 30, 2014 under the laws of PRC. Lichen Education is a wholly owned subsidiary of Lichen Zixun and is

our operating entity.

As

a result of our corporate structure, LICN’s ability to pay dividends may depend upon dividends paid by our Operating Subsidiaries.

If our existing Operating Subsidiaries or any newly formed ones incur debt on their own behalf in the future, the instruments governing

their debt may restrict their ability to pay dividends to us.

Implications

of Being an Emerging Growth Company

We

qualify as and elect to be an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, or

the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable

generally to public companies. These provisions include, but not limited to:

| |

● |

Reduced

disclosure about the emerging growth company’s executive compensation arrangements in our periodic reports, proxy statements

and registration statements; and |

| |

● |

an

exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to

the Sarbanes-Oxley Act of 2002. |

We

will remain an “emerging growth company” until the earliest to occur of (i) the last day of the fiscal year (a) following

the fifth anniversary of the closing of the Business Combination, (b) in which we have total annual gross revenue of at least $1.235 billion

or (c) in which we are deemed to be a large accelerated filer, which means the market value of equity securities held by our non-affiliates

exceeds $700 million as of the last business day of our prior second fiscal quarter, and (ii) the date on which we have issued more

than $1.0 billion in non-convertible debt during the prior three-year period.

Implication

of Being a Foreign Private Issuer

We

are a foreign private issuer within the meaning of the rules under the Securities Exchange Act of 1934, as amended (the “Exchange

Act”). As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

| |

● |

we

are not required to provide as many Exchange Act reports or provide periodic and current reports as frequently, as a domestic public

company; |

| |

● |

for

interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that

apply to domestic public companies; |

| |

● |

we

are not required to provide the same level of disclosure on certain issues, such as executive compensation; |

| |

● |

we

are exempt from provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; |

| |

● |

we

are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations

in respect of a security registered under the Exchange Act; and |

| |

● |

we

are not required to comply with Section 16 of the Exchange Act requiring insiders to file public reports of their share ownership

and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction. |

Implication

of Holding Foreign Companies Accountable Act

U.S. laws

and regulations, including the Holding Foreign Companies Accountable Act, or HFCAA, may restrict or eliminate our ability to complete

a business combination with certain companies, particularly those acquisition candidates with substantial operations in China.

On

March 24, 2021, the SEC adopted interim final rules relating to the implementation of certain disclosure and documentation requirements

of the HFCAA. An identified issuer will be required to comply with these rules if the SEC identifies it as having a “non-inspection”

year under a process to be subsequently established by the SEC. On June 22, 2021, the U.S. Senate passed the Accelerating

Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated Appropriations Act,

2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden, which contained, among other

things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act and amended the HFCAA by requiring the SEC

to prohibit an issuer’s securities from trading on any U.S stock exchanges if its auditor is not subject to PCAOB inspections for

two consecutive years instead of three, thus reducing the time period for triggering the prohibition on trading. On September 22,

2021, the PCAOB adopted a final rule implementing the HFCAA, which provides a framework for the PCAOB to use when determining, as contemplated

under the HFCAA, whether the PCAOB is unable to inspect or investigate completely registered public accounting firms located in a foreign

jurisdiction because of a position taken by one or more authorities in that jurisdiction.

On

December 2, 2021, the SEC issued amendments to finalize rules implementing the submission and disclosure requirements in the HFCAA. The

rules apply to registrants that the SEC identifies as having filed an annual report with an audit report issued by a registered public

accounting firm that is located in a foreign jurisdiction and that PCAOB is unable to inspect or investigate completely because of a

position taken by an authority in foreign jurisdictions. On December 16, 2021, the PCAOB issued a report on its determinations that

it is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong,

because of positions taken by PRC authorities in those jurisdictions. On August 26, 2022, the PCAOB announced that it had signed

a Statement of Protocol (the “SOP”) with the China Securities Regulatory Commission and the Ministry of Finance of China.

The SOP, together with two protocol agreements governing inspections and investigations (together, the “SOP Agreement”),

establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based

in mainland China and Hong Kong, as required under U.S. law. On December 15, 2022, the PCAOB announced that it was able

to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong

completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely

registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be

able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong

is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand

complete access in mainland China and Hong Kong moving forward and is making plans to resume regular inspections in early 2023 and

beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated

that it will act immediately to consider the need to issue new determinations with the HFCAA if needed.

Our

auditor, Enrome LLP, the independent registered public accounting firm, as an auditor of companies that are traded publicly in the United

States and a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections

to assess Enrome LLP’s compliance with applicable professional standards. Enrome LLP is headquartered in Singapore. As of the date

of this prospectus, Enrome LLP is not included in the list of PCAOB Identified Firms in the PCAOB Determination Report issued in December

2021. Our auditors, B&V for the fiscal year ended December 31, 2020 and TPS Thayer for the fiscal year ended December 31, 2021 and

2022, are both based in the U.S. B&V withdrew its registration from the PCAOB in January 2022. TPS Thayer is headquartered in Sugar

Land, Texas, and its registration with the PCAOB took effect in September 2020 and it is currently subject to PCAOB inspections.

However,

we cannot assure you whether Nasdaq or regulatory authorities would apply additional and more stringent criteria to us after considering

the effectiveness of our auditor’s audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency

of resources, geographic reach or experience as it relates to the audit of our financial statements. See “Risk Factors — Risks

Related to Doing Business in China — The recent joint statement by the SEC and PCAOB, proposed rule changes submitted

by Nasdaq, and the Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging

market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the

PCAOB. These developments could add uncertainties to our offering” on page 29 of the accompanying prospectus.

Transfers

of Cash to and from Our Subsidiaries

We

currently have not maintained any cash management policies that dictate the purpose, amount and procedure of cash transfers between the

Company, our subsidiaries, or investors. Rather, the funds can be transferred in accordance with the applicable PRC laws and regulations.

To the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not be

available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions

and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets.

Under

existing PRC foreign exchange regulations, payment of current account items, such as profit distributions and trade and service-related

foreign exchange transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange,

or the SAFE, by complying with certain procedural requirements. Therefore, our PRC subsidiaries are able to pay dividends in foreign

currencies to us without prior approval from SAFE, subject to the condition that the remittance of such dividends outside of the PRC

complies with certain procedures under PRC foreign exchange regulations, such as the overseas investment registrations by our shareholders

or the ultimate shareholders of our corporate shareholders who are PRC residents. Approval from, or registration with, appropriate government

authorities is, however, required where the RMB is to be converted into foreign currency and remitted out of China to pay capital expenses

such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the

future to foreign currencies for current account transactions. Current PRC regulations permit our PRC subsidiaries to pay dividends to

the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations.

As of the date of this prospectus, there are no restrictions or limitations imposed by the Hong Kong government on the transfer of capital

within, into and out of Hong Kong (including funds from Hong Kong to the PRC), except for transfer of funds involving money laundering

and criminal activities. Cayman Islands law prescribes that a company may only pay dividends out of its profits. Other than that, there

is no restrictions on Lichen China Limited’s ability to transfer cash to investors. See “Risk Factors - Risks Related to

Doing Business in China - To the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds

or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition

of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets,” “Risk

Factors - Risks Related to Doing Business in China - We rely on dividends and other distributions on equity paid by our PRC subsidiaries

to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to

us could have a material adverse effect on our ability to conduct our business,” and “Risk Factors - Risks Related to Doing

Business in China - Our PRC subsidiaries are subject to restrictions on paying dividends or making other payments to us, which may have

a material adverse effect on our ability to conduct our business.”

As

a holding company, we may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the

PRC, for our cash and financing requirements. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments

governing such debt may restrict their ability to pay dividends to us. Lichen China Limited is permitted under the laws of the Cayman

Islands to provide funding to our subsidiaries incorporated in the British Virgin Islands and Hong Kong through loans or capital

contributions without restrictions on the amount of the funds. Our subsidiaries are permitted under the respective laws of the British

Virgin Islands and Hong Kong to provide funding to Lichen China Limited through dividend distribution without restrictions on the amount

of the funds. There are no restrictions on dividends transfers from HK to BVI and BVI to the Cayman Islands. Current PRC regulations

permit our WFOE to pay dividends to the Company only out of its accumulated profits, if any, determined in accordance with Chinese

accounting standards and regulations.

The

PRC has currency and capital transfer regulations that require us to comply with certain requirements for the movement of capital. The

Company is able to transfer cash (US Dollars) to its PRC subsidiaries through an investment (by increasing the Company’s registered

capital in a PRC subsidiary). The Company’s subsidiaries within China can transfer funds to each other when necessary through the

way of current lending. The transfer of funds among companies are subject to the Provisions on Private Lending Cases, which was implemented

on August 20, 2020 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. As advised

by our PRC counsel, Tianyuan Law Firm, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary

to fund another subsidiary’s operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’

ability to transfer cash between PRC subsidiaries. The Company’s subsidiaries in the PRC have not transferred any earnings or cash

to the Company to date. As of the date of this prospectus, there has not been any assets or cash transfer between the holding company

and its subsidiaries. As of the date of this prospectus, there has not been any dividends or distributions made to US investors. The

Company’s business is primarily conducted through its subsidiaries. The Company is a holding company and its material assets consist

solely of the ownership interests held in its PRC subsidiaries. The Company relies on dividends paid by its subsidiaries for its working

capital and cash needs, including the funds necessary: (i) to pay dividends or cash distributions to its shareholders, (ii) to service

any debt obligations and (iii) to pay operating expenses. As a result of PRC laws and regulations (noted below) that require annual appropriations

of 10% of after-tax income to be set aside in a general reserve fund prior to payment of dividends, the Company’s PRC subsidiaries

are restricted in that respect, as well as in other respects noted below, in their ability to transfer a portion of their net assets

to the Company as a dividend.

With

respect to transferring cash from the Company to its subsidiaries, increasing the Company’s registered capital in a PRC subsidiary

requires the filing of the local commerce department, while a shareholder loan requires a filing with the State Administration of Foreign

Exchange or its local bureau. Aside from the declaration to the State Administration of Foreign Exchange, there is no restriction or

limitations on such cash transfer or earnings distribution.

With

respect to the payment of dividends, we note the following:

| |

1. |

PRC

regulations currently permit the payment of dividends only out of accumulated profits, as determined in accordance with accounting

standards and PRC regulations (an in-depth description of the PRC regulations is set forth below); |

| |

2. |

Our

PRC subsidiaries are required to set aside, at a minimum, 10% of their net income after taxes, based on PRC accounting standards,

each year as statutory surplus reserves until the cumulative amount of such reserves reaches 50% of their registered capital; |

| |

3. |

Such

reserves may not be distributed as cash dividends; |

| |

4. |

Our

PRC subsidiaries may also allocate a portion of their after-tax profits to fund their staff welfare and bonus funds; except in the

event of a liquidation, these funds may also not be distributed to shareholders; the Company does not participate in a Common Welfare

Fund; and |

| |

5. |

The

incurrence of debt, specifically the instruments governing such debt, may restrict a subsidiary’s ability to pay shareholder

dividends or make other cash distributions. |

If,

for the reasons noted above, our subsidiaries are unable to pay shareholder dividends and/or make other cash payments to the Company

when needed, the Company’s ability to conduct operations, make investments, engage in acquisitions, or undertake other activities

requiring working capital may be materially and adversely affected. However, our operations and business, including investment and/or

acquisitions by our subsidiaries within China, will not be affected as long as the capital is not transferred in or out of the PRC.

During

the fiscal years ended December 31, 2020, Lichen Zixun made dividend payments of RMB30 million (approximately $4.3 million) to the then

eventual shareholders of Lichen Zixun, who are PRC individuals. The Company made no such dividend, distribution or transfer during the

fiscal year ended December 31, 2021. As of the date of this prospectus, the Company or its subsidiaries have made no other transfers,

dividends, or distributions to investors and no investors have made transfers, dividends, or distributions to the Company or its subsidiaries.

As

of the date of this prospectus, no dividends, distributions or transfers has been made between Lichen China Limited and any of its subsidiaries.

For the foreseeable future, the Company intends to use the earnings for research and development, to develop new products and to expand

its production capacity. As a result, we do not expect to pay any cash dividends in the foreseeable future. Also, as of the date

of this prospectus, no cash generated from one subsidiary is used to fund another subsidiary’s operations and we do not anticipate

any difficulties or limitations on our ability to transfer cash between subsidiaries.

PRC

Regulations

In

accordance with PRC regulations, a domestic company is required to maintain a surplus reserve of at least 10% of its annual after-tax

profit until such reserve has reached 50% of its respective registered capital based on the enterprise’s PRC statutory accounts.

The aforementioned reserves can only be used for specific purposes and may not be distributed as cash dividends. Lichen Zixun and Lichen

Education were established as domestic companies; therefore, each is subject to the above-mentioned restrictions on distributable profits.

As

a result of PRC laws and regulations that require annual appropriations of 10% of after-tax income to be set aside, prior to payment

of dividends, in a general reserve fund, the Company’s PRC subsidiaries are restricted in their ability to transfer a portion of

their net assets to the Company as a dividend or otherwise.

Regulatory

Permissions

Our

Subsidiaries currently have obtained all material permissions and approvals required for our operations in compliance with the relevant

PRC laws and regulations in the PRC, including the business license and agency bookkeeping license. The business license is a permit

issued by Market Supervision and Administration that allows the company to conduct specific business within the government’s geographical

jurisdiction. The agency bookkeeping license is issued by the financial department to enterprises, allowing enterprises to accept entrusted

bookkeeping business. The business license and agency bookkeeping license are the only two permissions and approvals that our PRC subsidiaries

are required to obtain to conduct our business in China. In addition, Lichen China Limited, Legend Consulting BVI and Legend Consulting

HK are not required to obtain any permissions or approvals from any Chinese authorities to operate our business as of the date of this

prospectus. However, applicable laws and regulations may be tightened, and new laws or regulations may be introduced to impose additional

government approval, license and permit requirements. If we or our Subsidiaries inadvertently conclude that such permissions and approvals

relating to the operations of our business are not required, fail to obtain and maintain such approvals, licenses or permits required

for our business, or fail to respond to changes in the applicable laws, regulations, interpretations and regulatory environment, we or

our subsidiaries could be subject to liabilities, monetary penalties and even operational disruption, which may materially and adversely

affect our business, operating results, financial condition and the value of our Class A Ordinary Shares, significantly limit or completely

hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value

or become worthless.

As

confirmed by our PRC counsel, Tianyuan Law Firm, we and our Subsidiaries are not subject to cybersecurity review with the Cyberspace

Administration of China, or the “CAC,” after the Cybersecurity Review Measures became effective on February 15, 2022, since

we currently do not have over one million users’ personal information and do not anticipate that we will be collecting over one

million users’ personal information in the foreseeable future, which we understand might otherwise subject us to the Cybersecurity

Review Measures; we are also not subject to network data security review by the CAC if the Draft Regulations on the Network Data Security

Administration are enacted as proposed, since we currently do not have over one million users’ personal information and do not

collect data that affects or may affect national security and we do not anticipate that we will be collecting over one million users’

personal information or data that affects or may affect national security in the foreseeable future, which we understand might otherwise

subject us to the Network Data Security Administration Draft. However, the changing applicable laws, regulations or interpretations may

require us to do so in the future. Accordingly, any future failure to obtain prior approval of the CSRC, CAC, or any other Chinese authorities

for the listing and trading of our Class A Ordinary Shares on a foreign stock exchange could have a material adverse effect upon our

business. If we or our subsidiaries inadvertently conclude that such approval or permission is not required, fail to obtain and maintain

such approval or permission required, we or our subsidiaries may face sanctions by the CSRC, CAC or other PRC regulatory agencies for

failure to seek CSRC, CAC approval. These sanctions may include fines and penalties on our operations in China, limitations on our operations

in China, delays in or restrictions on the repatriation of the proceeds from this offering into the PRC, restrictions on or prohibition

of the payments or remittance of dividends by our subsidiaries in China, or other actions that could have a material adverse effect on

our business, financial condition, results of operations, reputation, prospects, the trading price of our Class A Ordinary Shares, and

the ability to offer the securities being registered to foreign investors.

On

August 8, 2006, six PRC regulatory agencies jointly adopted the Regulations on Mergers and Acquisitions of Domestic Enterprises

by Foreign Investors, or the M&A Rules, which came into effect on September 8, 2006 and were amended on June 22, 2009.

The M&A Rules requires that an offshore special purpose vehicle formed for overseas listing purposes and controlled directly or indirectly

by the PRC Citizens shall obtain the approval of the CSRC prior to overseas listing and trading of such special purpose vehicle’s

securities on an overseas stock exchange. Based on our understanding of the Chinese laws and regulations in effect at the time of this

prospectus, we will not be required to submit an application to the CSRC for its approval of this offering and the listing and trading

of our ordinary shares on the Nasdaq under the M&A Rules. However, there remains some uncertainty as to how the M&A Rules will