LONCOR GOLD

ANNOUNCES ADUMBI PEA WITH 303,000 OZ/YEAR

OVER

A 10.3 YEAR LOM

-

Pre-tax NPV (5%

discount) of US$895 million and post-tax NPV of US$624 million for

HEP Hybrid case at a US$1,600 gold price

-

Using

a US$1,760 gold price, post-tax NPV (5% discount) of US$879 million

for HEP Hybrid case

-

Average annual

production of 303,000 ounces of gold over a 10.3 year life of mine

within proposed pit shell

-

Average total cash

costs of US$852 per ounce over life of mine and AISC of US$950 per

ounce for HEP Hybrid case

Toronto, Canada --

December 15, 2021 -- InvestorsHub NewsWire

-- Loncor

Gold Inc. ("Loncor"

or the "Company")

(TSX: "LN"; OTCQX: "LONCF"; FSE: "LO51") is pleased to

announce the results of the Preliminary Economic Assessment

("PEA")

for its Adumbi gold deposit within its 84.68%-owned Imbo Project in

the Democratic Republic of the Congo (the "DRC").

Project economics and

financial analysis was undertaken on two power options at Adumbi: a

Hydroelectric Power ("HEP")

Hybrid case and a Diesel Only case. The table below summarises the

PEA results for the HEP Hybrid and Diesel Only cases:

|

DESCRIPTION

|

Units

|

HEP

HYBRID CASE

|

DIESEL ONLY

CASE

|

|

PRE-TAX

|

AFTER

TAX

|

PRE-TAX

|

AFTER

TAX

|

|

Life of Mine ("LOM") Tonnage Ore

Processed

|

t (000)

|

49,771

|

49,771

|

49,771

|

49,771

|

|

LOM Feed Grade Processed

|

g/t

|

2.172

|

2.172

|

2.172

|

2.172

|

|

Production Period

|

yrs

|

10.3

|

10.3

|

10.3

|

10.3

|

|

LOM Gold Recovery

|

%

|

89.8%

|

89.8%

|

89.8%

|

89.8%

|

|

LOM Gold Production

|

oz (000)

|

3,121

|

3,121

|

3,121

|

3,121

|

|

LOM Payable Gold After Refining Losses

|

oz (000)

|

3,119

|

3,119

|

3,119

|

3,119

|

|

Gold Price

|

US$/oz

|

1,600

|

1,600

|

1,600

|

1,600

|

|

Revenue

|

US$ million

|

4,990

|

4,990

|

4,990

|

4,990

|

|

Total Cash Costs

|

US$/oz

|

852

|

852

|

908

|

908

|

|

AISC

|

US$/oz

|

950

|

950

|

1,040

|

1,040

|

|

Preproduction Capital Costs

|

US$ million

|

530

|

530

|

392

|

392

|

|

Sustaining Capital Costs

|

US$ million

|

305

|

305

|

411

|

411

|

|

Net Present Value ("NPV") (5% discount

rate)

|

US$ million

|

895

|

624

|

843

|

600

|

|

IRR

|

%

|

25.2%

|

20.7%

|

30.3%

|

25.2%

|

|

Discount Rate

|

%

|

5%

|

5%

|

5%

|

5%

|

|

Payback Period-from start of production

|

Years

|

4.16

|

4.98

|

3.16

|

4.06

|

|

Project Net Cash

|

US$ million

|

1,495.2

|

1,087.0

|

1,352.8

|

992.5

|

Note:

Total cash costs per payable ounce,

AISC (All-in Sustaining-Costs) per payable ounce and project net

cash are non-GAAP financial measures. Please see "Cautionary Note

Concerning Non-GAAP Measures". Total cash costs includes all on-site

mining costs, processing costs, mine level G&A, refining and

royalties. AISC includes all mining costs,

processing costs, mine level G&A, royalties, refining,

sustaining capital and closure costs. Project net cash is cash revenues

less selling costs, less all mining costs, processing costs, mine

level G&A, and royalties.

All financial figures in

this press release are in United States dollars, unless otherwise

noted.

The Adumbi PEA study was

prepared for Loncor by a number of independent mining and

engineering consultants led by New SENET (SENET), Johannesburg

(Processing and Infrastructure) and Minecon Resources and Services

Limited (Minecon), Accra (Mineral Resources, Mining and

Environmental and Social) and Maelgwyn South Africa

(MMSA), Johannesburg

(Metallurgical test work), Knight Piésold and Senergy, Johannesburg

(Power) and Epoch, Johannesburg (Tailings and Water Storage). SENET

undertook the financial and economic evaluation.

Cautionary

Statement:

The

Adumbi PEA is preliminary in nature and includes Inferred Mineral

Resources in the open pit outlines that are considered too

speculative geologically to have the economic considerations

applied to them that would enable them to be categorized as Mineral

Reserves. There

is no certainty that all the conclusions reached in the Adumbi PEA

will be realized. Mineral

Resources that are not Mineral Reserves do not have demonstrated

economic viability.

Commenting on today's

Adumbi PEA study, Loncor's President Peter Cowley said: "The

results from the Adumbi PEA demonstrates a robust project with an

average of +300,000 ounces of gold per annum over 10 years with low

total cash costs and AISC costs of US$852 and US$950 per ounce

respectively over the LOM for the HEP Hybrid power

case."

"There also remains

significant upside potential at Adumbi and environs to increase

mineral resources, gold production, reduce operating costs and

further improve the economics of the project. Excellent exploration

potential exists to further increase mineral resources at Adumbi,

within the Imbo permit and other permits held by Loncor in the

Ngayu greenstone belt. At Adumbi, the mineralized BIF host sequence

increases in thickness below the open pit shell and wide spaced

drilling has already intersected grades and thicknesses amenable to

underground mining. Further drilling is required to initially

outline a significant underground mineral resource which can then

be combined with the open pit mineral resource so that studies can

be undertaken for a combined open pit and underground mining

scenario at Adumbi. Besides increasing the resource base, a

combined open pit/underground project could increase grade

throughput and reduce strip ratios with the higher grade, deeper

mineral resources being mined by underground which could increase

annual gold production and reduce operating costs."

"Additional deposits and

prospects occur close by to Adumbi and have the potential to add

mineral resources and feed for the Adumbi mine operation. Along

trend from Adumbi, the Manzako and Kitenge deposits have Inferred

Mineral Resources of 313,000 ounces (1.68 million tonnes grading

5.80 g/t Au) and remain open along strike and at depth. Further

along strike within the Imbo permit area, four priority prospects

have been identified with similar host lithologies to Adumbi and

will require drilling. Additional feed for the Adumbi processing

plant could also come from Loncor's 100%-owned high grade Makapela

deposit where Indicated Mineral Resources of 2.20 million tonnes

grading 8.66 g/t Au (614,200 ounces of gold) and Inferred Mineral

Resources of 3.22 million tonnes grading 5.30 g/t Au (549,600

ounces of gold) have been outlined to date with the high grade

material being able to be transported to Adumbi."

"Other opportunities are

being pursued to improve Adumbi's economics. The Company is already

in discussion with potential power suppliers with experience in the

DRC to project finance and build a hydroelectric facility at Adumbi

and then have an offtake agreement with Loncor to supply power for

the operation. Any hydroelectric power scheme could also have the

potential to obtain carbon credits."

Imbo Project

Containing the Adumbi Deposit

The Imbo Project which

contains the Adumbi deposit is situated at the eastern end of

the Ngayu Archean greenstone gold belt in

the Ituri Province of northeastern DRC and is approximately 220

kilometres from Africa's largest gold mine of Kibali, operated by Barrick Gold which in 2020 produced 808,134 ounces of gold.

This PEA was undertaken

on the Adumbi deposit, which is the main gold deposit on the

Company's 122 square kilometre Imbo Project. Loncor has a 84.68% interest in the

Imbo Project through its subsidiary Adumbi Mining S.A., with the

minority shareholders holding 15.32% (including a 10% free carried

interest held by the government of the DRC). The Imbo exploitation

permit is valid until February 2039.

Drilling commenced on the

Adumbi deposit in 2010 and to date 21,512 metres (74 core holes)

have been drilled (see Figure 1 below). Gold mineralization at Adumbi is

hosted in banded ironstone formation (BIF) and is similar to the

gold mineralization host lithologies of the major Kibali and Geita

mines in the DRC and Tanzania respectively. The main mineralized

host lithologies at Adumbi are BIF within which is a more altered,

higher sulfide RP ("replacement rock") lithology. As at Kibali and

Geita, significant underground mineral resource potential exists

below the Adumbi pit shell where the gold mineralization is open at

depth and where wide spaced drilling has already intersected

significant widths and grades with the BIF sequence thickening at

depth.

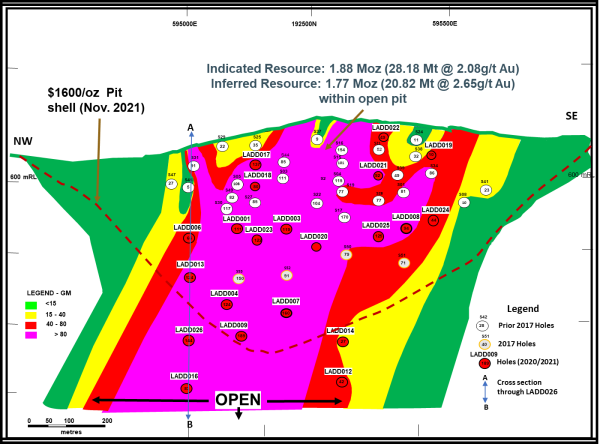

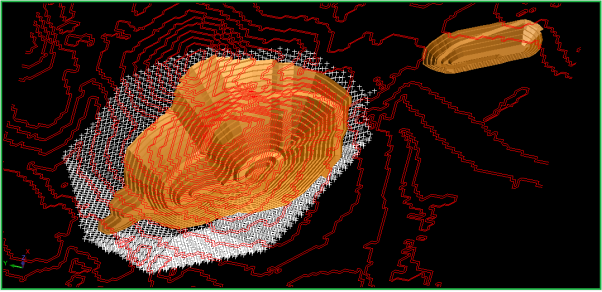

Figure

1:

Adumbi Deposit

Longitudinal Section Looking Northeast with Drill Hole Grade (g/t)

x True Thickness (Metre) Product Contours

Mineral

Resources

The mineral resource

assessment at Adumbi was undertaken by the Company's independent

geological consultants Minecon Resources and Services Limited

("Minecon").

Table I below summarises

the Adumbi indicated and inferred mineral resources based on

in-situ block cut-off grade at a 0.52 g/t Au for Oxide, 0.57 g/t Au

for Transition and 0.63 g/t Au for Fresh material and constrained

within a US$1,600 per ounce optimized pit shell.

84.68% of the Adumbi mineral

resources are attributable to Loncor via its 84.68% interest in the

Imbo Project.

Table

I:

Adumbi Deposit

Indicated and Inferred Mineral Resources

(effective date:

November 17, 2021)

|

Mineral

Resource Category

|

Tonnage

(Tonnes)

|

Grade

(g/t

Au)

|

Contained

Gold

(Ounces)

|

|

Indicated

|

28,185,000

|

2.08

|

1,883,000

|

|

Inferred

|

20,828,000

|

2.65

|

1,777,000

|

Note: Numbers may not add

up due to rounding.

Tables II below summarise

the indicated and inferred category mineral resources in terms of

material type.

Table

II: Adumbi Mineral Resources by Material Type

(effective date:

November 17, 2021)

|

|

INDICATED

MINERAL RESOURCE

|

INFERRED

MINERAL RESOURCE

|

|

Material

Type

|

Tonnage

|

Grade

|

Contained

Gold

|

Tonnage

|

Grade

|

Contained

Gold

|

|

(Tonnes)

|

(g/t

Au)

|

(Ounces)

|

(Tonnes)

|

(g/t

Au)

|

(Ounces)

|

|

Oxide

|

3,169,000

|

2.05

|

208,000

|

458,000

|

3.39

|

49,000

|

|

Transitional

|

3,401,000

|

2.51

|

274,000

|

280,000

|

2.74

|

24,000

|

|

Fresh

(Sulphide)

|

21,614,000

|

2.02

|

1,400,000

|

20,089,000

|

2.64

|

1,703,000

|

|

TOTAL

|

28,185,000

|

2.08

|

1,883,000

|

20,828,000

|

2.65

|

1,777,000

|

Note: Numbers may not add

up due to rounding.

Geological

Modelling and Grade Estimation

The Adumbi 3-dimensional

("3-D")

model was constructed by Minecon in collaboration with on-site

geologists using cross sectional and horizontal flysch plans of the

geology and mineralization and was used to assist in the

constraining of the 3-D geological model. The mineralization model was

constrained within a wireframe at 0.5 g/t Au cut-off grade. Grade

interpolation was undertaken using:

-

2 metre sample composites

capped at 18 g/t Au to improve the reliability of the block grade

estimates.

-

Ordinary Kriging to

interpolate grades into the block model.

-

Relative densities of

2.45 for oxide, 2.82 for transitional and 3.05 for fresh rock were

applied to the block model for tonnage estimation.

Pit

Optimisation Parameters

To constrain the depth

extent of the geological model and any mineral resources, an open

pit for the Adumbi deposit was constructed based on the following

pit optimisation parameters:

-

A gold price of US$1,600

per ounce.

-

Block size: 16 metres x

16 metres x 8 metres.

-

A thirty-two metres

minimum mining width and a maximum of four metres of internal waste

was applied.

-

Mining dilution of 100%

of the tonnes at 95% of the grade.

-

Ultimate slope angle of

minus 45 degrees.

-

Average mining cost of

US$3.29/tonne mined.

-

Metallurgical recoveries

of 91% for oxide, 88% for transitional and 90% for

fresh.

-

Average general and

administration cost of US$4.20/tonne.

-

Mineral resources were

estimated at a block cut-off grade of 0.52 g/t Au for oxide, 0.57

g/t Au for transition materials and 0.63 g/t Au for fresh material

constrained by a US$1,600 per ounce optimized pit

shell.

-

Transport of gold and

refining costs equivalent to 4.5% of the gold price.

-

No additional studies on

depletion by artisanal activity was undertaken since the RPA study

of 2014 and the same total amount of material was used by

Minecon.

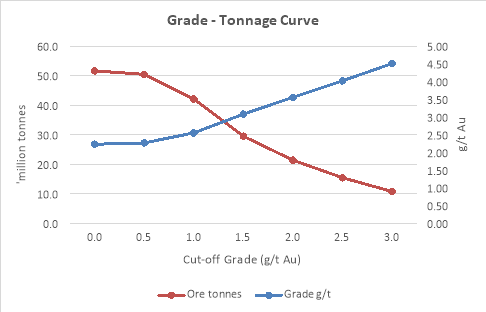

Tonnage/Grade

Curve

Grade/tonnage curves for

the Adumbi mineral resources at various gold cut-offs are

summarised in Table III and the graph below:

Table

III:

|

Block

Cut-off

|

Tonnage

|

Grade

|

Contained

Au

|

|

g/t

Au

|

million

tonnes

|

g/t

Au

|

million

ounces

|

|

0.0

|

51.60

|

2.23

|

3.70

|

|

0.5

|

50.10

|

2.29

|

3.68

|

|

1.0

|

41.15

|

2.61

|

3.45

|

|

1.5

|

29.07

|

3.17

|

2.97

|

|

2.0

|

21.76

|

3.66

|

2.56

|

|

2.5

|

16.06

|

4.17

|

2.15

|

|

3.0

|

12.12

|

4.63

|

1.80

|

Mining

The Adumbi deposit is

planned to be mined by conventional, contract, open pit mining

using truck and shovel mining fleet with drill and blasting for all

material types. Mining costs were broken down into reference and

incremental mining costs and were estimated from first principles

using knowledge of recent mining contracts operating in similar

gold mining operations in Africa. For the PEA, both Inferred and

Indicated Mineral Resources were included in the material to be

mined. Mining is planned to be carried out by a contractor on a

cost per tonne basis utilising a mining fleet consisting of 140

tonne rigid haul trucks with 8 cubic meter excavators.

Figure II:

Adumbi

Open Pit Design

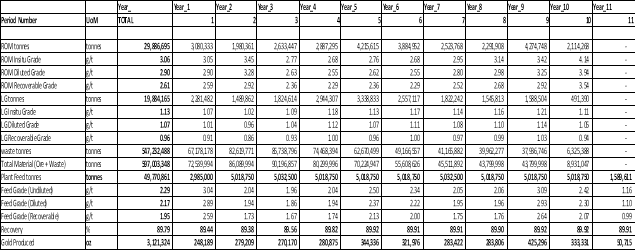

Table IV below summarises

the mining, processing and gold production schedules over Adumbi's

LOM.

Table

IV:

Mining, Processing

and Gold Production Schedules over Adumbi's LOM

Processing

Metallurgical

Testwork

Preliminary Economic

Assessment level metallurgical testwork (comminution and gold

recovery) was performed by Maelgwyn Mineral Services Laboratory on

the Adumbi ore to evaluate the process route required to treat the

ore and to obtain gold recoveries that can be achieved.

Table V below shows a

summary of the PEA Adumbi metallurgical testwork

results.

Table

V:

Adumbi

Metallurgical Testwork Results

|

Parameters

|

Units

|

Oxides

|

Transition

|

Fresh

|

|

Bond Rod Work

Index

|

kWh/t

|

12.7

|

13.6

|

14.6

|

|

Bond Ball Work

Index

|

kWh/t

|

11.8

|

13.7

|

14.2

|

|

Abrasion Index

|

|

0.19

|

0.25

|

0.34

|

|

Diagnostic Leach CIL

Recovery

|

%

|

90.76%

|

87.53%

|

89.9%

|

Average diagnostic leach

recovery for the fresh sulfide material was the weighted mean of RP

and BIF lithologies relative to their volume occurrence (20% RP:

80% BIF) in the fresh material. Diagnostic leach recoveries of 80.10%

for RP and 92.37% for BIF were realized for the fresh

sulfide.

Comminution results

indicated that both oxides and transition are medium-hard while

fresh material indicated that it is slightly

hard.

These results were taken

into account in the design of the comminution flowsheet.

In order to optimize gold

recovery further testwork was conducted on fresh and transitional

material whereby gravity was followed by flotation on gravity

tails. The results showed that most of the gold can be floated into

float concentrates as summarized in Table VI below.

Table

VI: Flotation Results

|

Sample

ID

|

Rougher

Concentrate

|

|

Gold

|

Sulphur

|

|

Grade (

g/t)

|

Rec.(%)

|

Grade

(%)

|

Rec.

(%)

|

|

Fresh - RP

|

9.57

|

95.06%

|

25.07

|

93.03%

|

|

Fresh - BIF

|

8.30

|

87.16%

|

17.90

|

85.13%

|

|

Transition

|

11.82

|

81.31%

|

15.80

|

95.52%

|

The concentrate samples

generated were not sufficient to enable further processing routes

such as:

-

Fine milling followed by

leaching with oxygen addition

-

Fine milling followed by

partial oxidation using high shear reactors and

leaching

-

Albion

process

-

Pressure

oxidation

-

Bio leaching

-

Roasting

These recovery processes

will be investigated during the next phase of the project to

optimize the gold recovery in the transitional and fresh ore

types.

Process

Plant

Based on the above

metallurgical testwork results, the Adumbi process plant design was

configured utilising well-known proven and established gravity and

carbon-in-leach (CIL) technologies to recover gold from blends of

oxide, transition and fresh ores that will be processed at a rate

of 5.0 million tonnes per annum.

The process plant

consists of the following sections:

-

Crushing

-

Milling

-

Gravity and concentrate

leach

-

Trash removal and

pre-leach thickener

-

CIL

-

Cyanide

detoxification

-

Arsenic

precipitation

-

Tails storage and return

water

-

Acid wash

-

Elution

-

Electrowinning

-

Gold room

-

Carbon

regeneration

-

Reagents

-

Air services

-

Water

services

Table VII below

summarises the key process design criteria for the process

plant.

Table

VII: Summary

of key process design criteria

|

ITEM

|

UNIT

|

OXIDE

|

TRANSITION

|

FRESH

|

|

Plant Throughput

|

Mt/a

|

5.0

|

5.0

|

5.0

|

|

Gold Head Grade

|

g Au/t

|

2.25

|

3.2

|

4.00

|

|

Design Gold Recovery

|

%

|

91.82

|

90.38

|

80.1 to 89.83

|

|

Crushing Plant Utilisation

|

%

|

65.0

|

65.0

|

65.0

|

|

Plant Availability

|

%

|

91.32

|

91.32

|

91.32

|

|

Comminution Circuit

|

|

1° Crush & SAB

|

1° Crush & SABC

|

1° Crush & SABC

|

|

Crush Size, P80

|

mm

|

180

|

180

|

180

|

|

Grind Size, P80

|

µm

|

75

|

75

|

75

|

|

Leach/CIL Residence Time

|

hrs

|

24

|

24

|

24

|

|

Leach Slurry Density

|

% w/w

|

40

|

40

|

50

|

|

Number of Pre-leach Tanks

|

#

|

1

|

1

|

1

|

|

Number of CIL Tanks/Stages

|

#

|

11

|

11

|

11

|

|

Cyanide Consumption

|

kg/t

|

0.99

|

1.32

|

1.31

|

|

Lime Consumption

|

kg/t

|

3.64

|

5.40

|

3.61

|

|

Elution Circuit Type

|

|

Pressure Zadra

|

Pressure Zadra

|

Pressure Zadra

|

|

Elution Circuit Size

|

t

|

12

|

12

|

12

|

|

|

|

|

|

|

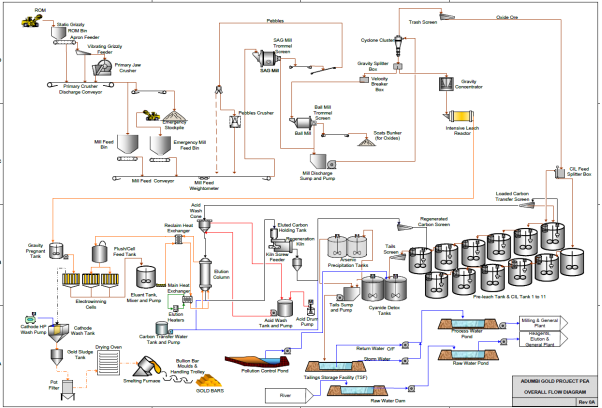

Figure III below shows

the proposed process plant flowsheet.

Figure III Proposed

Process Plant Flowsheet

Project

Infrastructure

A team of engineers from

SENET and Knight Piesold carried out a site investigation and, in

conjunction with the Loncor team, assessed the optimal positions

for key infrastructure components of the mine site. Preliminary

designs and layouts were done and positioned utilising the detailed

LIDAR survey which was previously commissioned by

Loncor.

Figure IV below

highlights the positions of key infrastructure for

Adumbi.

Figure IV:

Adumbi

Key Infrastructure and Site layout

Power

A desktop study was

undertaken by DRA Energy, South Africa assessing potential

hydroelectric, diesel and photovoltaic power sources for Adumbi.

Knight Piésold Ltd. from South Africa also undertook a desktop

study on a number of potential hydroelectric sites in and around

the Adumbi area and was part of the team of engineers from South

Africa who visited potential sites on the ground. The total

installed power required for Adumbi is estimated at 32

Megawatts (MW)

Table VIII below

indicates the different priority power generation options that were

investigated.

Table

VIII: Priority

Power Options for Adumbi

|

Option

|

Power

Option

|

Capex- Power

Plant

|

Power

Cost

|

Approximate

Distance from plant site (km)

|

|

USD

|

USD/kWh

|

|

1

|

Diesel Only 32 MW

|

15,708,000

|

0.2768

|

0

|

|

2

|

Hybrid, 32 MW Diesel, 20MW PV,

2.5MW/3.7MWh BESS

|

36,845,015

|

0.2459

|

0

|

|

3

|

Imbo Upper Site 3, 3.7MW HEP, 32 MW

Diesel, 20 MW PV, 12.4 MW/18.4MWh BESS

|

73,593,075

|

0.2133

|

5

|

|

4

|

Ngayu Confluence, 16.3 MW HEP, 32

MW Diesel, 20 MW PV, 12.4MW/18.4MWh BESS

|

138,593,075

|

0.1201

|

23

|

For the Adumbi PEA study,

two financial model cases were examined: the diesel only case of

generating power for essential processing plant equipment and

infrastructure; and the HEP Hybrid case option (Option 4)

which is a hybrid system consisting of HEP supplemented by diesel

and solar photovoltaic (PV) power generation with battery energy

storage. Although

capital costs are higher for the HEP Hybrid case, operating costs,

especially processing power costs are significantly reduced and

subsequent project economics are enhanced compared to the diesel

only powered generation case.

For the HEP Hybrid case,

it was assumed the capital cost for the HEP option would be funded

by Loncor. However, the Company is already in discussion with

potential power suppliers with experience in the DRC to project

finance and build a hydroelectric facility at Adumbi and then have

an offtake agreement with Loncor to supply power for the operation.

Any hydroelectric power scheme could also have the potential to

obtain carbon credits.

Tailings Management

Facility (TMF)

EPOCH undertook a site

selection exercise to design a tailings management system to cater

for 50 million tonnes over the life of mine.

The following were

considered for the design of the TMF:

-

A new (tailings storage

facility) TSF

-

A new return water dam

(RWD) associated with the TSF

-

The storm water

management and associated infrastructure for the TSF comprising

slurry deposition pipeline, drainage, perimeter access road, and

boundary fencing.

-

The following

legislation, regulations and design standards were considered

during the PEA design of the TMF:

- International Cyanide Code Standard

of Practice

- Global Industry Standard for Tailings

Management (GISTM)

The site selection

process was based on a multi criteria analyses and qualitative risk

analysis, which aimed to determine the most favourable location for

the TSF footprint.

Water

Raw water for the project

will be abstracted from the rivers in the area, which have

significant flow throughout the year.

Accessibility and

Transport

A number of potential

access routes have been assessed from the major port of Mombasa in

Kenya via Uganda to the Imbo Project in the Ituri province of

northeastern DRC. In

comparison to the tarred roads in Kenya and Uganda, the roads in

northeastern DRC are lateritic in nature and can become difficult

during the rainy season.

Of the

three transport DRC border options from Mombasa to Adumbi, the

preferred route via Kenya and Uganda is Aru – Durba (location of

the Kibali gold mine) - Mungbere - Isiro -

Wamba -Adumbi based on

the following considerations:

-

It is

the shortest

itinerary in terms of distance and time.

-

The traffic is less

dense, which determines a lower rate of deterioration of the

roads.

-

The

security along the roads is good, Kibali mine having used this

route up to Durba for several years without any

incidents.

-

The 1,512

km long road from Mombasa to Araba is a good, tarred road and is

maintained by the Kenyan and Ugandan government

authorities.

-

From Arua

to Durba (Kibali mine), a distance of 189 km, the road is well

maintained with the support of Barrick/AngloGold

Ashanti.

-

The section of the route

from Durba to Wamba (451 km) is now being maintained by the

provincial authorities of Haut-Uele

-

Only the remaining

stretch of road from Wamba to Adumbi (64 km) will need to be

rehabilitated and maintained by Loncor.

-

Estimates for initial

rehabilitation/refurbishment of the route and ongoing maintenance

where required has been included in initial pre-production capital

costs and in annual maintenance costs.

The new airstrip at

Adumbi is expected to be commissioned in January 2022 and can

accommodate propeller aircraft with up to 8.1 tonne

payloads.

Environmental and

Social Considerations

Minecon is implementing

pre-feasibility level Environmental and Social Impact Assessment

(ESIA), in compliance with the DRC mining code, as part of the

ESIA/ESMP, including but not limited to ecological, hydrological,

geochemical monitoring and socio-economic assessment. The study

will include village-level socio-economic survey, which will

generate data on demography, lifestyles and household livelihoods.

This will provide the needed guidance for the formulation of a

Resettlement Policy Framework, that will form the basis for taking

the resettlement planning process to the level of a Resettlement

Action Plan. The social assessment, including public consultation,

will also serve to help generate a Community Development Plan and a

Stakeholder Engagement Plan which will be detailed and refined

during the study. An amount has been included in

pre-production capital costs for environmental and social

considerations under Owner's Costs.

Initial

Pre-Production and Sustaining Capital Cost Estimate

Summaries

The following Tables IX

to XII summarise the initial Adumbi pre-production and sustaining

capital costs for the two power case options: Diesel Only and HEP

Hybrid.

Table

IX: Adumbi

Pre-Production Capital Cost Estimate for Diesel Only Power

Case

|

Description

|

Capital

Cost

|

Contingency

|

Total

Capital Cost

|

|

US$(000)

|

US$(000)

|

US$(000)

|

|

Mining

|

49,988

|

9,998

|

59,986

|

|

Process Plant

|

143,655

|

27,714

|

171,369

|

|

Power Plant

|

12,004

|

2,401

|

14,405

|

|

Initial TSF

|

54,900

|

10,980

|

65,880

|

|

Infrastructure

|

22,675

|

4,785

|

27,461

|

|

Access Transport

Road

|

6,500

|

1,300

|

7,800

|

|

Owner's Costs

|

39,323

|

5,787

|

45,110

|

|

Total

Initial Capex

|

329,045

|

62,965

|

392,010

|

Table

X: Adumbi

Sustaining Capital Estimate for Diesel Only Power Case

|

Description

|

|

|

|

Total

Capital Cost

|

|

|

|

|

|

US$(000)

|

|

Mining Capitalized

Waste

|

|

|

|

328,215

|

|

Power Plant

|

|

|

|

14,122

|

|

TSF

|

|

|

|

66,329

|

|

Rehabilitation &

Closure Costs

|

|

|

|

30,678

|

|

Equipment Salvage

Value

|

|

|

|

-28,789

|

|

|

|

|

|

|

|

Total

Sustaining Capital

|

|

|

|

410,556

|

Table

XI: Adumbi

Pre-Production Capital Cost Estimate for HEP Hybrid Power

Case

|

Description

|

Capital

Cost

|

Contingency

|

Total

Capital Cost

|

|

|

US$(000)

|

US$(000)

|

US$(000)

|

|

Mining

|

49,988

|

9,998

|

59,986

|

|

Process Plant

|

143,655

|

27,714

|

171,369

|

|

HEP Hybrid Power

Plant

|

138,593

|

13,859

|

152,452

|

|

Initial TSF

|

54,900

|

10,980

|

65,880

|

|

Infrastructure

|

22,675

|

4,785

|

27,461

|

|

Access Transport

Road

|

6,500

|

1,300

|

7,800

|

|

Owner's Costs

|

39,323

|

5,787

|

45,110

|

|

Total

Initial Capex

|

455,634

|

74,423

|

530,058

|

Table

XII: Adumbi

Sustaining Capital Estimate for HEP Hybrid Power Case

|

Description

|

|

|

|

Total

Capital Cost

|

|

|

|

|

|

US$(000)

|

|

Mining Capitalized

Waste

|

|

|

|

328,215

|

|

Power Plant

|

|

|

|

0

|

|

TSF

|

|

|

|

66,329

|

|

Rehab & Closure

Costs

|

|

|

|

30,678

|

|

Equipment Salvage Value

(Process Plant &HEP)

|

|

|

-120,260

|

|

|

|

|

|

|

|

Total

Sustaining Capital

|

|

|

|

304,962

|

Adumbi Operating

Costs Summaries

The following Tables XIII

to XIV summarise LOM operating costs for the Diesel Only and HEP

Hybrid cases:

Table

XIII: Adumbi

LOM Operating Costs for the Diesel Only Case

|

Description

|

LOM

|

|

US$/t

processed

|

US$/oz

|

|

Mining

|

31.33

|

499.56

|

|

Processing

|

17.95

|

286.21

|

|

TSF

|

0.55

|

8.75

|

|

G & A

|

3.40

|

54.19

|

|

Refining &

Transport

|

0.22

|

3.50

|

|

Royalties

|

3.51

|

55.96

|

|

Total

Cash Costs

|

57.0

|

908

|

A diesel price of

US$0.90/litre was used based on supplier quotes.

Table

XIV: Adumbi

LOM Operating Costs for the HEP Hybrid Case

|

Description

|

LOM

|

|

US$/t

processed

|

US$/oz

|

|

Mining

|

31.33

|

499.56

|

|

Processing

|

14.44

|

230.22

|

|

TSF

|

0.55

|

8.75

|

|

G & A

|

3.40

|

54.19

|

|

Refining &

Transport

|

0.22

|

3.50

|

|

Royalties

|

3.51

|

55.96

|

|

Total

Cash Costs

|

53.4

|

852

|

Project Economics

and Financial Analysis

SENET has produced a cash

flow valuation model for the Adumbi deposit for the HEP Hybrid and

Diesel Only cases taking into account annual processed tonnages,

grades and recoveries, metal prices, site operating and total cash

costs including royalties and refining charges and initial

pre-production and sustaining capital expenditure estimates. The

financial assessment of Adumbi has been carried out on a "100%

equity" basis for both pre-tax and after-tax considerations. The

financial analysis assumed a base gold price of US$1,600 per ounce

of gold.

Table XV below summarises

the pre-tax and after-tax financial analysis for the HEP Hybrid and

Diesel Only cases:

Table

XV: Comparison

of HEP Hybrid vs Diesel power generation Financial

Models

|

DESCRIPTION

|

Units

|

HEP

HYBRID CASE

|

DIESEL ONLY

CASE

|

|

PRE-TAX

|

AFTER

TAX

|

PRE-TAX

|

AFTER

TAX

|

|

LOM Tonnage Ore Processed

|

t (000)

|

49,771

|

49,771

|

49,771

|

49,771

|

|

LOM Feed Grade Processed

|

g/t

|

2.172

|

2.172

|

2.172

|

2.172

|

|

Production Period

|

yrs

|

10.3

|

10.3

|

10.3

|

10.3

|

|

LOM Gold Recovery

|

%

|

89.8%

|

89.8%

|

89.8%

|

89.8%

|

|

LOM Gold Production

|

oz (000)

|

3,121

|

3,121

|

3,121

|

3,121

|

|

LOM Payable Gold After Refining Losses

|

oz (000)

|

3,119

|

3,119

|

3,119

|

3,119

|

|

Gold Price

|

US$/oz

|

1,600

|

1,600

|

1,600

|

1,600

|

|

Revenue

|

US$ million

|

4,990

|

4,990

|

4,990

|

4,990

|

|

Site Operating Costs

|

US$/oz

|

793

|

793

|

849

|

849

|

|

Total Cash Costs

|

US$/oz

|

852

|

852

|

908

|

908

|

|

AISC

|

US$/oz

|

950

|

950

|

1,040

|

1,040

|

|

Preproduction Capital Costs

|

US$ million

|

530

|

530

|

392

|

392

|

|

Sustaining Capital Costs

|

US$ million

|

305

|

305

|

411

|

411

|

|

NPV (5% discount rate)

|

US$ million

|

895

|

624

|

843

|

600

|

|

IRR

|

%

|

25.2%

|

20.7%

|

30.3%

|

25.2%

|

|

Discount Rate

|

%

|

5%

|

5%

|

5%

|

5%

|

|

Payback Period-from start of production

|

Years

|

4.16

|

4.98

|

3.16

|

4.06

|

|

Project Net Cash

|

US$ million

|

1,495.2

|

1,087.0

|

1,352.8

|

992.5

|

Note:

Total cash costs per payable ounce,

AISC (All-in Sustaining-Costs) per payable ounce and project net

cash are non-GAAP financial measures. Please see "Cautionary Note

Concerning Non-GAAP Measures". Total cash costs includes all on-site

mining costs, processing costs, mine level G&A, refining and

royalties. AISC includes all mining costs,

processing costs, mine level G&A, royalties, refining,

sustaining capital and closure costs. Project net cash is cash revenues

less selling costs, less all mining costs, processing costs, mine

level G&A, and royalties.

Sensitivity

Financial Analysis

Calculated sensitivities

to the Adumbi base case gold price of US$1,600/ounce show

significant upside leverage to the gold price and the robust nature

of the projected economics to the capital and operating

assumptions.

Project sensitivities for

the NPV, IRR, cash cost, AISC and payback period have been

undertaken for varying gold price percentages from the

US$1,600/ounce base case and are summarised in Table XVI and XVII

below for the HEP Hybrid and Diesel Only cases:

Table

XVI: Gold

Price Sensitivities for the HEP Hybrid Case

|

Average Gold

Price (US$/oz)

|

|

Change in Gold Price

|

%

|

-15%

|

-10%

|

0%

|

10%

|

15%

|

|

Average Gold Price

|

US$/oz

|

1,360

|

1,440

|

1,600

|

1,760

|

1,840

|

|

NPV @ 5% -Pre-Tax

|

US$M

|

373

|

547

|

895

|

1,243

|

1,417

|

|

NPV @ 5% -Post-Tax

|

US$M

|

238

|

368

|

624

|

879

|

1,006

|

|

IRR- Pre-Tax

|

%

|

14.1%

|

18.0%

|

25.2%

|

31.9%

|

35.1%

|

|

IRR- Post -Tax

|

%

|

11.4%

|

14.7%

|

20.7%

|

26.4%

|

29.1%

|

|

Total Cash Costs

|

US$/oz

|

844

|

847

|

852

|

858

|

861

|

|

AISC

|

US$/oz

|

941

|

944

|

950

|

955

|

958

|

|

Payback Period– Pre-Tax

|

Years

|

7.88

|

6.26

|

4.16

|

3.00

|

2.64

|

|

Payback Period- Post-Tax

|

Years

|

8.28

|

7.10

|

4.98

|

3.76

|

3.30

|

Table

XVII: Gold Price Sensitivities for the Diesel Only

Case

|

Average Gold

Price (US$/oz)

|

|

Change in Gold Price

|

%

|

-15%

|

-10%

|

0%

|

10%

|

15%

|

|

Average Gold Price

|

US$/oz

|

1,360

|

1,440

|

1,600

|

1,760

|

1,840

|

|

NPV @ 5% -Pre-Tax

|

US$M

|

321

|

495

|

843

|

1,191

|

1,365

|

|

NPV @ 5% -Post-Tax

|

US$M

|

211

|

345

|

600

|

855

|

983

|

|

IRR- Pre-Tax

|

%

|

15.6%

|

20.8%

|

30.3%

|

39.0%

|

43.1%

|

|

IRR- Post-Tax

|

%

|

12.7%

|

17.2%

|

25.2%

|

32.6%

|

36.1%

|

|

Total Cash Costs

|

US$/oz

|

900

|

903

|

908

|

914

|

917

|

|

AISC

|

US$/oz

|

1,031

|

1,034

|

1,040

|

1,045

|

1,048

|

|

Payback Period - Pre-Tax

|

Years

|

7.53

|

5.46

|

3.16

|

2.18

|

1.93

|

|

Payback Period – Post-Tax

|

Years

|

8.02

|

6.28

|

4.06

|

2.77

|

2.39

|

Project

Opportunities

Loncor has identified and

will be pursuing a number of opportunities for enhancing and

increasing the economics and financial returns relating to the

Adumbi project. These include the

following:

-

Increasing Mineral

Resources

There is excellent

exploration potential to increase mineral resources at Adumbi,

within the Imbo Project and other permit areas held by Loncor in

the Ngayu greenstone belt. At Adumbi, the mineralized BIF host

sequence increases in thickness below the open pit shell and wide

spaced drilling has already intersected grades and thicknesses

amenable to underground mining. Further drilling is required to

initially outline a significant underground mineral resource which

can then be combined with the open pit mineral resource so that

studies can be undertaken for a combined open pit and underground

mining scenario at Adumbi. Besides increasing the resource base, a

combined open pit/underground project could increase grade

throughput and reduce strip ratios with the higher grade, deeper

mineral resources being mined by underground which could increase

annual gold production and reduce operating costs.

Additional deposits and

prospects occur close by to Adumbi and have the potential to add

mineral resources and feed to the Adumbi mine operation. Along

trend from Adumbi, the Manzako and Kitenge deposits have Inferred

Mineral Resources of 313,000 ounces of gold (1.68 million tonnes

grading 5.80 g/t Au) and remain open along strike and at depth.

Further along strike within the Imbo Project, four priority

prospects have been identified with similar host lithologies to

Adumbi and will require drilling.

Additional feed for the

Adumbi processing plant could also come from Loncor's 100%-owned

high grade Makapela deposit where Indicated Mineral Resources of

2.20 million tonnes grading 8.66 g/t Au (614,200 ounces of gold)

and Inferred Mineral Resources of 3.22 million tonnes grading 5.30

g/t Au (549,600 ounces of gold) have been outlined to date with the

high grade material being able to be transported to

Adumbi.

-

Additional geotechnical

investigations including drilling has the potential to optimize and

steepen pit slopes especially for the competent fresh BIF host rock

and thus reducing the strip ratio and thereby lowering mining

costs.

-

Further metallurgical

testwork to confirm recoveries, reagent consumptions and optimize

flowsheet design should be undertaken as the project advances into

pre-feasibility and full feasibility stages.

-

As mentioned previously,

hydroelectric sites have already been identified close to Adumbi

and further studies are required to optimize the power set for the

operation.

Qualified Persons

Mr. Philemon Bundo,

Senior Vice President of Process at New SENET (Pty) Ltd, and Mr.

Daniel Bansah, Chairman and Managing Director of Minecon, are the

"qualified persons" (as such term is defined in National Instrument

43-101) who are responsible for the technical information disclosed

in this press release. Mr. Bansah and Mr. Bundo have

reviewed and approved the contents of this press

release.

A technical report

relating to the Adumbi PEA reported in this press release will be

prepared in accordance with National Instrument 43- 101 and will be

filed on SEDAR and EDGAR within the period required by National

Instrument 43-101.

Technical Reports

Additional information

with respect to the Company's Imbo Project (which includes the

Adumbi deposit) is contained in the technical report of Minecon

Resources and Services Limited dated April 27, 2021 and entitled

"Updated Resource Statement and Independent National Instrument

43-101 Technical Report, Imbo Project, Ituri Province, Democratic

Republic of the Congo". A copy of the said report can be

obtained from SEDAR at

www.sedar.com and

EDGAR at

www.sec.gov.

Information with respect

to the Company's Makapela Project, and certain other properties of

the Company in the Ngayu gold belt, is contained in the technical

report of Venmyn Rand (Pty) Ltd dated May 29, 2012 and entitled

"Updated National Instrument 43-101 Independent Technical Report on

the Ngayu Gold Project, Orientale Province, Democratic Republic of

the Congo". A copy of the said report can be

obtained from SEDAR at www.sedar.com and EDGAR at

www.sec.gov.

About Loncor Gold Inc.

Loncor is a Canadian gold

exploration company focussed on the Ngayu Greenstone Gold Belt in

the northeast of the Democratic Republic of the Congo (the

"DRC").

The Loncor team has over

two decades of experience of operating in the

DRC.

Loncor's growing resource

base in the Ngayu Belt currently comprises the Imbo and Makapela

Projects. At the Imbo Project, the Adumbi

deposit holds an indicated mineral resource of 1.88 million ounces

of gold (28.185 million tonnes grading 2.08 g/t gold), and the

Adumbi deposit and two neighbouring deposits hold an inferred

mineral resource of 2.090 million ounces of gold (22.508 million

tonnes grading 2.89 g/t Au), with 84.68% of these resources being

attributable to Loncor. Loncor has been carrying out a

drilling program at the Adumbi deposit with the objective of

outlining additional mineral resources. The Makapela Project (which is

100%-owned by Loncor and is located approximately 50 kilometres

from the Imbo Project) has an indicated mineral resource of 614,200

ounces of gold (2.20 million tonnes grading 8.66 g/t Au) and an

inferred mineral resource of 549,600 ounces of gold (3.22 million

tonnes grading 5.30 g/t Au).

Additional information

with respect to Loncor and its projects can be found on Loncor's

website at www.loncor.com

Cautionary

Note to U.S. Investors

National

Instrument 43-101 - Standards of Disclosure for Mineral Projects

("NI

43-101") is a rule of

the Canadian Securities Administrators which establishes standards

for all public disclosure an issuer makes of scientific and

technical information concerning mineral projects.

Unless

otherwise indicated, all resource estimates contained in this press

release have been prepared in accordance with NI 43-101 and the

Canadian Institute of Mining, Metallurgy and Petroleum

Classification System.

These

standards differ from the requirements of the U.S. Securities and

Exchange Commission, and resource information contained in this

press release may not be comparable to similar information

disclosed by U.S. companies.

Cautionary

Note Concerning Forward-Looking Information

This

press release contains forward-looking information.

All

statements, other than statements of historical fact, that address

activities, events or developments that the Company believes,

expects or anticipates will or may occur in the future (including,

without limitation, statements regarding estimates and/or

assumptions in respect of production, revenue, cash flow and costs,

estimated project economics, Adumbi project opportunities, mineral

resource estimates, potential underground mineral resources,

potential mineralization, potential gold discoveries, drill

targets, potential mineral resource increases, exploration results,

and future exploration and development plans) are forward-looking

information.

This

forward-looking information reflects the current expectations or

beliefs of the Company based on information currently available to

the Company.

Forward-looking

information is subject to a number of risks and uncertainties that

may cause the actual results of the Company to differ materially

from those discussed in the forward-looking information, and even

if such actual results are realized or substantially realized,

there can be no assurance that they will have the expected

consequences to, or effects on the Company.

Factors

that could cause actual results or events to differ materially from

current expectations include, among other things, uncertainty of

estimates of capital and operating costs, production estimates and

estimated economic return, the possibility that actual

circumstances will differ from the estimates and assumptions used

in the Adumbi PEA, the possibility that future exploration

(including drilling) or development results will not be consistent

with the Company's expectations, the possibility that drilling or

development programs will be delayed, activities of the Company may

be adversely impacted by the continued spread of the widespread

outbreak of respiratory illness caused by a novel strain of the

coronavirus ("COVID-19"), including the ability of the Company to

secure additional financing, risks related to the exploration stage

of the Company's properties, uncertainties relating to the

availability and costs of financing needed in the future, failure

to establish estimated mineral resources (the Company's mineral

resource figures are estimates and no assurances can be given that

the indicated levels of gold will be produced), changes in world

gold markets or equity markets, political developments in the DRC,

gold recoveries being less than those indicated by the

metallurgical testwork carried out to date (there can be no

assurance that gold recoveries in small scale laboratory tests will

be duplicated in large tests under on-site conditions or during

production), fluctuations in currency exchange rates, inflation,

changes to regulations affecting the Company's activities, delays

in obtaining or failure to obtain required project approvals, the

uncertainties involved in interpreting drilling results and other

geological data and the other risks disclosed under the heading

"Risk Factors" and elsewhere in the Company's annual report on Form

20-F dated March 31, 2021 filed on SEDAR at www.sedar.com and EDGAR

at www.sec.gov.

Forward-looking

information speaks only as of the date on which it is provided and,

except as may be required by applicable securities laws, the

Company disclaims any intent or obligation to update any

forward-looking information, whether as a result of new

information, future events or results or otherwise.

Although

the Company believes that the assumptions inherent in the

forward-looking information are reasonable, forward-looking

information is not a guarantee of future performance and

accordingly undue reliance should not be put on such information

due to the inherent uncertainty therein.

Cautionary

Note Concerning Mineral Resource Estimates

The

mineral resource figures referred to in this press release are

estimates and no assurances can be given that the indicated levels

of gold will be produced. Such estimates are expressions of

judgment based on knowledge, mining experience, analysis of

drilling results and industry practices. Valid

estimates made at a given time may significantly change when new

information becomes available. While

the Company believes that the mineral resource estimates included

in this press release are well established, by their nature mineral

resource estimates are imprecise and depend, to a certain extent,

upon statistical inferences which may ultimately prove

unreliable. If

such estimates are inaccurate or are reduced in the future, this

could have a material adverse impact on the Company.

Mineral

resources are not mineral reserves and do not have demonstrated

economic viability. There

is no certainty that mineral resources can be upgraded to mineral

reserves through continued exploration.

Due to

the uncertainty that may be attached to inferred mineral resources,

it cannot be assumed that all or any part of an inferred mineral

resource will be upgraded to an indicated or measured mineral

resource as a result of continued exploration. Confidence

in the estimate is insufficient to allow meaningful application of

the technical and economic parameters to enable an evaluation of

economic viability worthy of public disclosure (except in certain

limited circumstances). Inferred

mineral resources are excluded from estimates forming the basis of

a feasibility study.

Cautionary

Note Concerning Non-GAAP Measures

This

press release includes certain terms or performance measures

commonly used in the mining industry that are not defined under

International Financial Reporting Standards ("IFRS"), including

cash costs and AISC per payable ounce of gold sold. Non-GAAP

measures do not have any standardized meaning prescribed under IFRS

and, therefore, they may not be comparable to similar measures

employed by other companies. The

Company believes that, in addition to conventional measures

prepared in accordance with IFRS, certain investors use this

information to evaluate performance. The

data presented is intended to provide additional information and

should not be considered in isolation or as a substitute for

measures of performance prepared in accordance with IFRS.

For further information,

please visit our website at

www.loncor.com or

contact:

John Barker, CEO, +44

7547 159 521

Peter Cowley, President,

+44 7904 540 856

Arnold Kondrat, Executive

Chairman, +1 416 366 7300