0001675634false--08-31FY202300500000000.000103583337500000000.00015073832139003583331300000.01400000.0027690001255000P5Y11800000.0P7Y2M12D0.000146733213586752200000700000300000110000055000013.2035.680.000167400000.01250520331250000035833317500.0050.00013328.0037620004210.80288.002880.0037203720.000.00011.005208334840837570590000012000000.00.00013150P10Y2000001100000P1Y10M24D800000.00200000.03700000.03800000.0100000.00379780003900000.0P3Y00016756342022-09-012023-08-3100016756342022-12-080001675634us-gaap:SubsequentEventMember2023-10-050001675634us-gaap:SubsequentEventMember2023-10-012023-10-050001675634us-gaap:SubsequentEventMember2023-10-012023-10-170001675634us-gaap:SubsequentEventMember2023-11-012023-11-220001675634us-gaap:SubsequentEventMember2023-12-012023-12-140001675634pixy:JohnStephenHolmesBankruptcyLitigationMember2022-11-012022-11-080001675634pixy:VensureLitigationMemberus-gaap:PendingLitigationMember2021-11-040001675634pixy:VensureLitigationMember2019-12-252020-01-030001675634pixy:VensureLitigationMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2021-09-070001675634pixy:VensureLitigationMemberpixy:WithdrawnClaimMember2021-04-012021-08-310001675634pixy:FoundryASVRFSawgrassLLCMember2022-09-012023-08-310001675634pixy:CapistranoCateringIncMember2022-09-012023-08-310001675634pixy:VensureLitigationMember2021-03-012021-03-120001675634pixy:OtherMattersMember2023-06-012023-06-050001675634pixy:OtherMattersMember2022-09-012023-08-310001675634pixy:GoldenWestWingsLLCMember2022-09-012023-08-310001675634pixy:SunzLitigationMember2021-03-012021-03-190001675634pixy:EverestLitigatonMember2022-09-012023-08-310001675634pixy:EverestLitigatonMember2020-12-012020-12-180001675634pixy:IndustrialHumanCapitalIncMemberus-gaap:IPOMember2021-10-012021-10-220001675634pixy:IndustrialHumanCapitalIncMemberus-gaap:IPOMember2022-09-012023-08-310001675634pixy:SpecialPurposeAcquisitionCompany2Member2023-08-310001675634pixy:SpecialPurposeAcquisitionCompany2Member2021-10-220001675634pixy:IndustrialHumanCapitalIncMemberus-gaap:IPOMember2021-10-220001675634pixy:SpecialPurposeAcquisitionCompany2Member2021-10-012021-10-310001675634pixy:SpecialPurposeAcquisitionCompanyOneMember2021-04-290001675634pixy:SpecialPurposeAcquisitionCompanyOneMember2021-04-012021-04-290001675634pixy:SpecialPurposeAcquisitionCompany2Member2022-09-012023-08-310001675634pixy:SpecialPurposeAcquisitionCompany2Member2021-04-290001675634pixy:ShiftPixyLabsFacilityMember2020-09-282020-10-010001675634pixy:IrvineFacilityMember2022-05-012022-05-020001675634pixy:SunriseFacilityMember2021-06-012021-06-070001675634pixy:SecondIrvineFacilityMember2022-09-012023-08-310001675634pixy:MiamiVerifoneFacilityMember2021-06-070001675634pixy:IrvineFacilityMember2022-09-012023-08-310001675634pixy:ShiftPixyLabsFacilityMember2021-09-012022-08-310001675634pixy:SunriseFacilityMember2022-09-012023-08-310001675634pixy:IrvineFacilityMember2021-09-012022-08-310001675634pixy:SunriseFacilityMember2021-09-012022-08-310001675634pixy:MiamiOfficeSpaceFacilityMember2021-09-012022-08-310001675634pixy:MiamiVerifoneFacilityMember2022-09-012023-08-310001675634pixy:MiamiOfficeSpaceFacilityMember2023-08-310001675634pixy:MiamiOfficeSpaceFacilityMember2022-08-310001675634pixy:MiamiOfficeSpaceFacilityMember2022-09-012023-08-310001675634us-gaap:StateAndLocalJurisdictionMember2023-08-310001675634us-gaap:DomesticCountryMember2023-08-310001675634pixy:DirectorsMember2022-08-310001675634pixy:DirectorsMember2023-08-310001675634pixy:ScottAbsherMember2021-09-012022-08-310001675634pixy:ScottAbsherMember2022-09-012023-08-310001675634pixy:ScottAbsherMember2022-08-310001675634pixy:ScottAbsherMember2023-08-310001675634pixy:DirectorsMember2022-09-012023-08-310001675634pixy:DirectorsMember2021-09-012022-08-310001675634pixy:ScottAbsherMember2022-08-012022-08-120001675634pixy:ScottAbsherMember2022-03-012022-03-310001675634pixy:ScottAbsherMember2021-10-220001675634pixy:ScottAbsherMember2022-07-310001675634pixy:ScottAbsherMember2021-10-012021-10-220001675634pixy:AmandaMurphyMember2022-08-310001675634pixy:AmandaMurphyMember2022-09-012023-08-310001675634pixy:AmandaMurphyMember2021-09-012022-08-310001675634pixy:ConnieAbsherElizabethEastvoldAndHannahAbsherMember2021-09-012022-08-310001675634pixy:ConnieAbsherElizabethEastvoldAndHannahAbsherMember2022-09-012023-08-310001675634pixy:JasonAbsherMember2021-09-012022-08-310001675634pixy:JasonAbsherMember2022-09-012023-08-310001675634pixy:PhilEastvoldMember2022-09-012023-08-310001675634pixy:PhilEastvoldMember2021-09-012022-08-310001675634pixy:DavidMayMember2021-09-012022-08-310001675634pixy:DavidMayMember2022-09-012023-08-310001675634pixy:MarkAbsherMember2021-09-012022-08-310001675634pixy:MarkAbsherMember2022-09-012023-08-310001675634pixy:RelatedPartiesMember2023-08-310001675634pixy:RelatedPartiesMember2022-09-012023-08-3100016756342021-09-012022-05-3100016756342023-03-012023-05-310001675634pixy:GrantedPriorToJuly12020Memberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2022-09-012023-08-310001675634pixy:OptionsGrantedOnOrAfterJuly12020Memberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-09-012023-08-310001675634pixy:GrantedPriorToJuly12020Memberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-09-012023-08-310001675634pixy:MarchSixTwoZeroTwentyThreeMember2023-03-060001675634pixy:MarchSixTwoZeroTwentyThreeMember2023-03-050001675634pixy:ExercisePriceRangeFiveMember2022-09-012023-08-310001675634pixy:ExercisePriceRangeFiveMember2023-08-310001675634pixy:ExercisePriceRangeFourMember2022-09-012023-08-310001675634pixy:ExercisePriceRangeFourMember2023-08-310001675634pixy:ExercisePriceRangeThreeMember2022-09-012023-08-310001675634pixy:ExercisePriceRangeThreeMember2023-08-310001675634pixy:ExercisePriceRangeTwoMember2022-09-012023-08-310001675634pixy:ExercisePriceRangeTwoMember2023-08-310001675634pixy:ExercisePriceRangeOneMember2022-09-012023-08-310001675634pixy:ExercisePriceRangeOneMember2023-08-310001675634srt:MaximumMemberpixy:ExercisePriceRangeFiveMember2022-09-012023-08-310001675634srt:MinimumMemberpixy:ExercisePriceRangeFiveMember2022-09-012023-08-310001675634srt:MaximumMemberpixy:ExercisePriceRangeFourMember2022-09-012023-08-310001675634srt:MinimumMemberpixy:ExercisePriceRangeFourMember2022-09-012023-08-310001675634srt:MaximumMemberpixy:ExercisePriceRangeThreeMember2022-09-012023-08-310001675634srt:MinimumMemberpixy:ExercisePriceRangeThreeMember2022-09-012023-08-310001675634srt:MaximumMemberpixy:ExercisePriceRangeTwoOneMember2022-09-012023-08-310001675634srt:MinimumMemberpixy:ExercisePriceRangeTwoMember2022-09-012023-08-310001675634srt:MaximumMemberpixy:ExercisePriceRangeOneMember2022-09-012023-08-310001675634srt:MinimumMemberpixy:ExercisePriceRangeOneMember2022-09-012023-08-3100016756342021-06-0400016756342022-01-012022-01-2600016756342022-07-012022-07-1800016756342021-09-012021-09-300001675634us-gaap:PrivatePlacementMember2021-05-012021-05-170001675634pixy:May2021CommonWarrantsMemberus-gaap:PrivatePlacementMember2021-05-310001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-07-180001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-07-250001675634pixy:ExistingWarrantsMember2022-07-012022-07-250001675634pixy:NewWarrantsMember2022-07-012022-07-250001675634pixy:NewWarrantsMember2022-07-250001675634pixy:NewWarrantsMember2022-07-180001675634pixy:InvestorWarrantsMember2022-07-180001675634pixy:October2020CommonWarrantsMemberpixy:CommonShareUnitsMember2020-10-080001675634pixy:PlacementWarrantsMemberus-gaap:IPOMemberpixy:IndustrialHumanCapitalIncMember2021-10-220001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-01-280001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2021-09-030001675634srt:ChiefExecutiveOfficerMember2022-08-012022-08-120001675634us-gaap:IPOMemberpixy:IHCMember2021-10-2200016756342023-07-012023-07-1200016756342023-07-120001675634pixy:SecuritiesPurchaseAgreementMember2023-07-1200016756342021-05-170001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-07-280001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-09-200001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2023-08-310001675634pixy:CommonStockWarrantsMemberus-gaap:PrivatePlacementMember2023-08-310001675634pixy:CommonStockWarrantsMemberus-gaap:PrivatePlacementMember2021-05-170001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2021-05-170001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2022-08-310001675634pixy:September2021PrefundedWarrantsMemberus-gaap:PrivatePlacementMember2021-09-300001675634us-gaap:PrivatePlacementMember2021-09-030001675634pixy:September2021CommonWarrantsMember2021-09-030001675634pixy:September2021PrefundedWarrantsMemberus-gaap:PrivatePlacementMember2021-09-030001675634us-gaap:PrivatePlacementMember2021-09-012021-09-300001675634pixy:May2021PrefundedWarrantsMemberus-gaap:PrivatePlacementMember2021-05-310001675634pixy:CommonStockWarrantsMemberus-gaap:PrivatePlacementMember2022-09-200001675634pixy:CommonShareUnitsMember2022-09-012022-09-200001675634pixy:September2021ModifiedWarrantsMember2022-09-012023-08-3100016756342022-08-092022-09-020001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2020-06-012020-06-050001675634pixy:CommonShareUnitsMember2021-10-012021-10-220001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2020-06-012020-06-050001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2020-01-042020-06-040001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-07-012022-07-250001675634pixy:September2021ModifiedWarrantsMember2022-07-012022-07-250001675634pixy:July2022CommonWarrantsMember2022-09-012023-08-310001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-01-260001675634pixy:ExistingWarrantsMember2022-09-012023-08-310001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-01-012022-01-260001675634pixy:JanuaryTwoZeroTwoTwoCommonWarrantsMember2022-09-012023-08-310001675634pixy:OptionAgreementMember2023-10-012023-10-1700016756342022-09-012022-09-200001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2022-08-120001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2023-08-3100016756342022-01-012022-01-280001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2022-08-012022-08-1200016756342023-05-310001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2022-07-012022-07-140001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2022-08-310001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberus-gaap:ConvertiblePreferredStockMember2022-09-012023-08-310001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2022-08-282022-09-030001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberus-gaap:ConvertiblePreferredStockMember2022-08-282022-09-0300016756342022-09-200001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberus-gaap:ConvertiblePreferredStockMember2022-08-120001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2023-12-080001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2023-08-012023-08-210001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberpixy:CommonShareUnitsMember2023-08-2100016756342023-01-012023-01-310001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMemberus-gaap:ConvertiblePreferredStockMember2022-07-1400016756342022-03-012022-05-3100016756342021-05-012021-05-170001675634pixy:OptionAgreementMember2023-08-2200016756342023-08-012023-08-210001675634pixy:OptionAgreementMember2023-08-012023-08-220001675634pixy:CEOMember2023-08-012023-08-2100016756342022-09-012022-09-300001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2022-07-140001675634pixy:ScottWAbsherMembersrt:ChiefExecutiveOfficerMember2021-08-130001675634pixy:June2018WarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:AmendedMarch2019NotesWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:May2020CommonWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:October2020CommonWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:June2018WarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:October2020CommonWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:AmendedMarch2019NotesWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:May2020CommonWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:October2020UnderwriterWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:October2020UnderwriterWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:May2020UnderwriterWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:May2020UnderwriterWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:March2019ServicesWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:March2019ServicesWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:June2018ServicesWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:June2018ServicesWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:March2020ExchangeWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:March2020ExchangeWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:May2021UnderwriterWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:May2021UnderwriterWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:September2021UnderwriterWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:September2021UnderwriterWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:July2023CommonWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:September2022CommonWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:September2022UnderwriterWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:July2022CommonWarrantsMemberus-gaap:WarrantMember2022-09-012023-08-310001675634pixy:July2022CommonWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:September2022UnderwriterWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:July2023CommonWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:September2022CommonWarrantsMemberus-gaap:WarrantMember2023-08-310001675634pixy:LeaseholdimprovementsMember2022-08-310001675634pixy:LeaseholdimprovementsMember2023-08-310001675634us-gaap:EquipmentMember2022-08-310001675634us-gaap:EquipmentMember2023-08-310001675634pixy:FurniturefixturesMember2022-08-310001675634pixy:FurniturefixturesMember2023-08-310001675634pixy:IHCMember2022-09-012023-08-310001675634pixy:IHCMember2023-02-012023-02-070001675634pixy:IHCMember2023-02-070001675634pixy:IHCMember2022-10-140001675634pixy:PublicSharesMemberpixy:IHCMember2022-10-1400016756342022-10-1400016756342021-04-2900016756342021-10-220001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2021-03-120001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:PEOBusinessMember2020-01-030001675634pixy:IncomeTaxExpenseMember2021-09-012022-08-310001675634pixy:IncomeTaxExpenseMember2022-09-012023-08-310001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2021-09-012022-08-310001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2022-09-012023-08-310001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2022-08-310001675634us-gaap:DiscontinuedOperationsDisposedOfBySaleMemberpixy:OverallBusinessMember2023-08-310001675634pixy:IndustrialHumanCapitalIncMember2022-09-012023-08-310001675634pixy:IndustrialHumanCapitalIncMember2023-02-012023-02-070001675634us-gaap:OtherIncomeMember2023-02-012023-02-070001675634pixy:IndustrialHumanCapitalIncMember2023-02-070001675634pixy:NoncontrollingInterestVIEMember2023-02-012023-02-070001675634pixy:PlacementWarrantsMemberus-gaap:IPOMemberpixy:IndustrialHumanCapitalIncMember2021-10-012021-10-2200016756342023-06-012023-06-300001675634us-gaap:OtherIncomeMember2023-08-310001675634srt:MaximumMember2022-09-012023-08-310001675634srt:MinimumMember2022-09-012023-08-310001675634pixy:PlacementWarrantsMemberus-gaap:IPOMemberpixy:IndustrialHumanCapitalIncMember2021-10-310001675634pixy:CommonWarrantsMemberus-gaap:SubsequentEventMemberpixy:PublicOfferingMember2023-10-050001675634us-gaap:SubsequentEventMemberpixy:PublicOfferingMember2023-10-050001675634us-gaap:SubsequentEventMemberpixy:PublicOfferingMember2023-10-012023-10-050001675634pixy:CommonWarrantsMemberus-gaap:SubsequentEventMemberpixy:PublicOfferingMember2023-10-012023-10-050001675634us-gaap:SoftwareDevelopmentMember2022-08-310001675634us-gaap:SoftwareDevelopmentMember2023-08-310001675634us-gaap:StockCompensationPlanMember2022-09-012023-08-310001675634us-gaap:WarrantMember2021-09-012022-08-310001675634us-gaap:WarrantMember2022-09-012023-08-310001675634pixy:EmployeeStockOptionTwoMember2021-09-012022-08-310001675634pixy:EmployeeStockOptionTwoMember2022-09-012023-08-310001675634pixy:FixedAssetsMember2022-09-012023-08-310001675634pixy:FixedAssetsMember2023-08-310001675634us-gaap:LeaseholdImprovementsMember2022-09-012023-08-310001675634srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2022-09-012023-08-310001675634srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2022-09-012023-08-310001675634us-gaap:EquipmentMember2022-09-012023-08-310001675634pixy:ClientTwoMemberpixy:GrossRevenuesMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientTwoMemberpixy:GrossRevenuesMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientOneMemberpixy:GrossRevenuesMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientOneMemberpixy:GrossRevenuesMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientFourMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientFiveMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientFiveMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientFourMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientThreeMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientThreeMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientTwoMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientTwoMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:ClientOneMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2021-09-012022-08-310001675634pixy:ClientOneMemberus-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-09-012023-08-310001675634pixy:NewMexicoMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2021-09-012022-08-310001675634pixy:WashingtonMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2021-09-012022-08-310001675634pixy:NewMexicoMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2022-09-012023-08-310001675634pixy:WashingtonMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2022-09-012023-08-310001675634us-gaap:CaliforniaFranchiseTaxBoardMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2021-09-012022-08-310001675634us-gaap:CaliforniaFranchiseTaxBoardMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:GeographicConcentrationRiskMember2022-09-012023-08-310001675634pixy:StaffingServicesMember2022-09-012023-08-310001675634pixy:StaffingServicesMember2021-09-012022-08-310001675634pixy:HumanCapitalManagementServicesMember2021-09-012022-08-310001675634pixy:HumanCapitalManagementServicesMember2022-09-012023-08-310001675634pixy:NoncontrollingInterestVIEMember2023-08-310001675634pixy:TotalStockholdersDeficitShoftPixyIncMember2023-08-310001675634us-gaap:RetainedEarningsMember2023-08-310001675634us-gaap:AdditionalPaidInCapitalMember2023-08-310001675634pixy:ConvertiblesPreferredStocksMember2023-08-310001675634us-gaap:CommonStockMember2023-08-310001675634pixy:ConvertiblesPreferredStocksMember2022-09-012023-08-310001675634pixy:NoncontrollingInterestVIEMember2022-09-012023-08-310001675634pixy:TotalStockholdersDeficitShoftPixyIncMember2022-09-012023-08-310001675634us-gaap:RetainedEarningsMember2022-09-012023-08-310001675634us-gaap:AdditionalPaidInCapitalMember2022-09-012023-08-310001675634us-gaap:CommonStockMember2022-09-012023-08-310001675634pixy:NoncontrollingInterestVIEMember2022-08-310001675634pixy:TotalStockholdersDeficitShoftPixyIncMember2022-08-310001675634us-gaap:RetainedEarningsMember2022-08-310001675634us-gaap:AdditionalPaidInCapitalMember2022-08-310001675634pixy:ConvertiblesPreferredStocksMember2022-08-310001675634us-gaap:CommonStockMember2022-08-310001675634pixy:ConvertiblesPreferredStocksMember2021-09-012022-08-310001675634pixy:NoncontrollingInterestVIEMember2021-09-012022-08-310001675634pixy:TotalStockholdersDeficitShoftPixyIncMember2021-09-012022-08-310001675634us-gaap:RetainedEarningsMember2021-09-012022-08-310001675634us-gaap:AdditionalPaidInCapitalMember2021-09-012022-08-310001675634us-gaap:CommonStockMember2021-09-012022-08-3100016756342021-08-310001675634pixy:NoncontrollingInterestVIEMember2021-08-310001675634pixy:TotalStockholdersDeficitShoftPixyIncMember2021-08-310001675634us-gaap:RetainedEarningsMember2021-08-310001675634us-gaap:AdditionalPaidInCapitalMember2021-08-310001675634pixy:ConvertiblesPreferredStocksMember2021-08-310001675634us-gaap:CommonStockMember2021-08-3100016756342021-09-012022-08-3100016756342022-08-3100016756342023-08-3100016756342023-12-1100016756342023-02-28iso4217:USDxbrli:sharesiso4217:USDxbrli:sharesxbrli:pureutr:sqft

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

| For the fiscal year ended August 31, 2023 |

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

| For the transition period from _____________ to _____________ |

SEC File No. 024-10557

SHIFTPIXY, INC. |

(Exact name of registrant as specified in its charter) |

Wyoming | | 47-4211438 |

(State of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

4101 NW 25th Street, Miami FL | | 33131 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number: (888) 798-9100

Securities to be registered pursuant to Section 12(b) of the Act:

Common Stock, par value $0.0001 per share | | Trading Symbol(s) | | The NASDAQ Stock Market LLC |

Title of each class registered | | PIXY | | Name of each exchange on which each class is registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

Emerging growth company | ☒ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. §7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes ☐ No ☒

As of February 28, 2023, the aggregate market value, based on the Nasdaq quoted closing price of $122.64 of the common stock held by non-affiliates of the registrant was approximately $7.0 million.

The number of outstanding shares of Registrant’s Common Stock, $0.0001 par value, was 5,397,698 shares as of December 11, 2023.

Auditor Name | | Auditor Location | | Auditor Firm ID |

Marcum LLP | | New York, NY | | (PCAOB NO 688) |

TABLE OF CONTENTS

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS AND INFORMATION

This Annual Report on Form 10-K ("Form 10-K"), the other reports, statements, and information that we have previously filed or that we may subsequently file with the Securities and Exchange Commission (“SEC”), and public announcements that we have previously made or may subsequently make, contain “forward-looking statements” within the meaning of the federal securities laws, including the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. Unless the context is otherwise, the forward-looking statements included or incorporated by reference in this Form 10-K and those reports, statements, information and announcements address activities, events or developments that ShiftPixy, Inc. (referred to throughout this Form 10-K as “we,” “us,” “our,” the “Company” or “ShiftPixy”), expects or anticipates will or may occur in the future. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “might,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Forward-looking statements contained in this Form 10-K include, but are not limited to, statements about:

| · | our future financial performance, including our revenue, costs of revenue and operating expenses; |

| | |

| · | our ability to achieve and grow profitability; |

| | |

| · | the sufficiency of our cash, cash equivalents and investments to meet our liquidity needs; |

| | |

| · | our predictions about industry and market trends; |

| | |

| · | our ability to expand successfully internationally; |

| | |

| · | our ability to manage effectively our growth and future expenses, including our growth and expenses associated with our sponsorship of various special purpose acquisition companies; |

| | |

| · | our estimated total addressable market; |

| | |

| · | our ability to maintain, protect and enhance our intellectual property; |

| | |

| · | our ability to comply with modified or new laws and regulations applying to our business; |

| | |

| · | the attraction and retention of qualified employees and key personnel; |

| | |

| · | our ability to be successful in defending litigation brought against us and |

| | |

| · | our ability to pay the outstanding delinquent payroll taxes, including penalties and interest. If the IRS or states and local jurisdictions pursues collection efforts beyond what the Company can afford to pay, the IRS can freeze our bank accounts and the Company may be forced to file for bankruptcy. |

We caution you that the forward-looking statements highlighted above do not encompass all of the forward-looking statements made in this Form 10-K.

We have based the forward-looking statements contained in this Form 10-K primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in the section of this Form 10-K entitled “Risk Factors” and elsewhere. Moreover, we operate in a very competitive and challenging environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Form 10-K. We cannot assure you that the results, events and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

The forward-looking statements made in this Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Form 10-K to reflect events or circumstances after the date of this Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, other strategic transactions or investments we may make or enter into.

The risks and uncertainties we currently face are not the only ones we face. New factors emerge from time to time, and it is not possible for us to predict which will arise. There may be additional risks not presently known to us or that we currently believe are immaterial to our business. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

The industry and market data contained in this Form 10-K are based either on our management’s own estimates or, where indicated, independent industry publications, reports by governmental agencies or market research firms or other published independent sources and, in each case, are believed by our management to be reasonable estimates. However, industry and market data are subject to change and cannot always be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares. We have not independently verified market and industry data from third-party sources. In addition, consumption patterns and customer preferences can and do change. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be verifiable or reliable.

PART I

Item 1. Business

Company Information

We were incorporated under the laws of the State of Wyoming on June 3, 2015. Our principal executive office is located at 4101 NW 25th Street, Miami, FL 33142, and our telephone number is (888) 798-9100. Our website address is www.shiftpixy.com. Our website does not form a part of this Form 10-K and listing of our website address is for informational purposes only.

Business Overview

We are a human capital management ("HCM") platform. We provide payroll and related employment tax processing, human resources and employment compliance, employment related insurance, and employment administrative services solutions for our business clients (“clients” or “operators”) and shift work or “gig” opportunities for worksite employees (“WSEs” or “shifters”). As consideration for providing these services, we receive administrative or processing fees as a percentage of a client’s gross payroll. The level of our administrative fees is dependent on the services provided to our clients, which ranges from basic payroll processing to a full suite of human resources information systems ("HRIS") technology. Our primary operating business metric is gross billings, consisting of our clients’ fully burdened payroll costs, which includes, in addition to payroll, workers’ compensation insurance premiums, employer taxes, and benefits costs.

Our goal is to be the best online fully-integrated workforce solution and employer services support platform for lower-wage workers and employment opportunities. We have built an application and desktop capable marketplace solution that allows for workers to access and apply for job opportunities created by our clients and to provide traditional back-office services to our clients as well as real-time business information for our clients’ human capital needs and requirements.

We have designed our business platform to evolve to meet the needs of a changing workforce and a changing work environment. We believe our approach and robust technology will benefit from the observed demographic workplace shift away from traditional employee/employer relationships towards the increasingly flexible work environment that is characteristic of the gig economy. We believe this change in approach began after the 2008 financial crisis and is currently being driven by the labor shortage created out of the COVID-19 economic crisis. We also believe that a significant problem underpinning the lower wage labor crisis is the sourcing of workers and matching temporary or gig workers to short-term job opportunities.

Figure 1

We have built our business on a recurring revenue model since our inception in 2015. Our focus has been to monetize a traditional staffing services business model, coupled with developed technology, to address underserved markets containing predominately lower wage employees with high turnover, including the light industrial, food service, restaurant, and hospitality markets.

Our primary focus was on clients in the restaurant and hospitality industries, market segments traditionally characterized by high employee turnover and low pay rates. We believe that these industries will be better served by our human resource information system (“HRIS”) technology platform and related mobile smartphone application that provides payroll and human resources tracking for our clients. The use of our HRIS platform should provide our clients with real-time human capital business intelligence and we believe will result in lower operating costs, improved customer experience, and revenue growth. All of our clients enter into service agreements with us or one of our wholly-owned subsidiaries to provide these services.

We believe that our value proposition is to provide a combination of overall net cost savings to our clients, for which they are willing to pay increased administrative fees that offset the costs of the services we provide, as follows:

| · | Payroll tax compliance and management services |

| | |

| · | Governmental HR compliance such as for Patient Protection and Affordable Care Act (“ACA”) compliance requirements; |

| | |

| · | Reduced client workers’ compensation premiums or enhanced coverage; |

| | |

| · | Access to an employee pool of potential qualified applicants to reduce turnover costs; |

| | |

| · | Ability to fulfill temporary worker requirements in a “tight” labor market with our intermediation (“job matching”) services; and |

| | |

| · | Reduced screening and onboarding costs due to access to an improved pool of qualified applicants who can be onboarded through a highly efficient, and virtually paperless technology platform. |

Our management believes that providing this baseline business, coupled with our technology solution, provides a unique, value-added solution to the HR compliance, staffing, and scheduling problems that businesses face. Over the past thirty-six months, in the face of the COVID-19 and post COVID-19 pandemic, we have instituted various growth initiatives described below that are designed to accelerate our revenue growth. These initiatives include the matching of temporary job opportunities between workers and employers under a fully compliant staffing solution through our HRIS platform. For this solution to be effective, we need to obtain a significant number of WSEs in concentrated geographic areas to fulfill our clients unique staffing needs and facilitate the client-WSE relationship.

Managing, recruiting, and scheduling a high volume of low-wage employees can be both difficult and expensive. Historically, the acquisition and recruiting of such an employee population has been a labor intensive and expensive process in part due to high onboarding costs and complex issues surrounding such matters as tax information capture or I-9 verification. Early in our history, we evaluated these costs and found that proper process flows that are automated with blockchain and cloud technology, coupled with access to lower cost workers’ compensation policies resulting from economies of scale, could result in a profitable and low-cost scalable business model.

Over the past five years, we have invested heavily in a robust, cloud-based HRIS platform to:

| · | reduce client WSE management costs; |

| | |

| · | automate new WSE and client onboarding; |

| | |

| · | accumulate a large pool of qualified WSEs across multiple geographical markets; |

| | |

| · | facilitate the intermediation (job matching) of WSEs with job opportunities; and |

| | |

| · | supply additional value-added services for our clients that generate additional revenue streams for us. |

We began to develop our HRIS platform in 2017, including our front-end desktop and mobile smartphone application to facilitate easier WSE and client onboarding processes, deliver additional client functionality, and provide enhanced opportunities for WSEs to find shift work. Beginning in March 2019, we transitioned the development of our mobile smartphone application from a third-party vendor to an in-house development team and launched an early version of the application several months later. As of August 31, 2019, we had completed the initial launch of our mobile application and we started to provide some of the HRIS and application services to select legacy customers on a pilot project basis. During our fiscal year ended August 31, 2021 ("Fiscal 2021"), our in-house engineers continued to implement additional HRIS functionality in employee fulfillment, delivery and scheduling services, and “gig” intermediation services through our mobile smartphone application. During Fiscal year ended August 31, 2022 ("Fiscal 2022"), our technology development efforts focused on supporting our growth initiatives with features such as bulk on-boarding, job matching intermediation, and qualified candidate pool vertical market integrations. We see these technology-based services as having potential to generate multiple streams of revenue from a variety of different markets.

Our cloud-based HRIS platform captures, holds, and processes HR and payroll information for our clients and WSEs through an easy-to-use customized front-end interface coupled with a secure, remotely hosted database. The HRIS system can be accessed by either a desktop computer or an easy-to-use mobile smartphone application designed with HR workflows in mind. Once fully implemented, we expect to reduce the time, expense, and error rate for onboarding our clients’ employees into our HRIS ecosystem. Upon being onboarded, these WSEs are listed as available for shift work within our business ecosystem. This allows our HRIS platform to serve as both a gig marketplace for WSEs for our opportunities and also allows for clients to better manage their staffing needs.

We see our technology platform and our ability to process gig workers as fully compliant W-2 employees as a key competitive advantage and differentiator to our market competitors that will facilitate expansion of our HCM services beyond our current concentration in low-wage restaurant employees and healthcare workers. We further believe that our accumulation of a significant number of WSEs on our platform, whether currently billed or not, will facilitate additional growth initiatives with the potential to generate significant value for our shareholders, as described below.

Beginning in January 2020, we operated under a traditional staffing services business model, coupled with developed technology, to address underserved markets in the restaurant and hospitality industries, predominately consisting of lower wage employees with high turnover. At the same time, we continued our prior efforts to expand our services into other industries that utilize higher paid employees on a temporary or part-time basis, including the healthcare staffing industry. Our go-to-market approach was to use an inside sales force to market our services directly to clients to manage their human capital requirements and to form strategic relationships with business associations to gather WSEs. Until the COVID-19 pandemic, this approach was effective and resulted in substantial growth. However, the COVID-19 pandemic changed the landscape in HCM due to reduced employment in our core restaurant and hospitality markets.

We evaluated our prior growth initiatives and decided to change our focus considering the new market conditions. As part of our plan, we identified several growth initiatives designed to fully leverage our HRIS platform during the second half of Fiscal 2022 and year ended August 31, 2023 “Fiscal 2023”. These growth initiatives are focused on: seeking acquisition targets for growth, a recurring revenue base, significant gross profit conversion, margin expansion opportunities, a light industrial sector focus, a blue-chip client base, cyclical tailwinds, and a tenured management team willing and able to execute a comprehensive integration plan. The Company can give no assurance that it will be successful in implementing its business.

Figure 2

We have built our business on a recurring revenue model since our inception in 2015.

Staffing Solutions

The Company records gross billings as revenues for its staffing solutions clients. The Company is primarily responsible for fulfilling the staffing solutions services and has discretion in establishing price. The Company includes the payroll costs in revenues with a corresponding increase to cost of revenues for payroll costs associated with these services. As a result, we are the principal in this arrangement for revenue recognition purposes.

EAS Solutions / HCM

EAS solutions and Human Capital Management “HCM” revenues are primarily derived from the Company’s gross billings, which are based on (i) the payroll cost of the Company’s worksite employees (“WSEs”) and (ii) an administrative fee and (iii) if eligible, WSE can elect certain pass through benefits.

Gross billings are invoiced to each EAS and HCM client, concurrently with each periodic payroll. Revenues are offset by payroll cost component and pass through cost which are presented on a net basis for revenue recognition. WSEs perform their services at the client’s worksite. The Company assumes responsibility for processing and remitting payroll to the WSE and payroll related obligations, it does not assume employment-related responsibilities such as determining the amount of the payroll and related payroll obligations. Revenues that have been recognized but not invoiced are included in unbilled accounts receivable on the Company’s consolidated balance sheets were $1.8 million and $2.1 million, as of August 31, 2023 and August 31, 2022, respectively. Client who pay in advance of their invoice, the amount is recognized as a liability.

Our Services

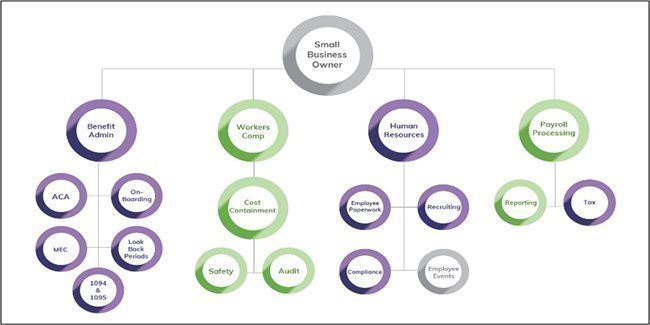

Figure 3

Our core business is to provide regular payroll processing services to clients under an employment administrative services (“EAS”) model in addition to individual services, such as payroll tax compliance, workers’ compensation insurance coverage related services, and employee HR compliance management. In addition, in November 2019, we launched our employee onboarding and employee scheduling functionalities to our customers through our mobile smartphone application. In Fiscal 2021, we began to operate under a direct staffing business model.

Our core EAS are typically provided to our clients for one-year renewable terms. We expect that our future service offerings, including technology-based services provided through our HRIS platform, will provide for additional revenue streams and support cost reductions for existing and future clients. We expect that our future services will be offered through “a la carte” pricing via customizable online contracts under our HCM services model as well as through our direct staffing business model. Our staffing services are typically provided to our clients under recurring revenue contracts with one of our subsidiaries.

We intend to use our growth initiatives to leverage our expansion by entering into client services agreements (“CSAs”) with national accounts at regional levels and the various restaurant brands that we are working to launch through ShiftPixy Labs. As such, these growth initiatives are expected to increase our core staffing services billings, revenues, gross profit, and operating leverage organically. We may also support our growth by performing new business acquisitions. Further, the new Gig Economy has given rise to controversy regarding the classification of many workers as “independent contractors”, rather than traditional employees, while the rising trend of predictive scheduling creates logistical issues for our clients’ management of their workers’ schedules. We provide solutions to businesses struggling with these compliance issues primarily by absorbing our clients’ workers, whom we refer to as WSEs (as well as “shift workers,” “shifters,” “gig workers,” or “assigned employees”). WSEs are included under our corporate employee umbrella as traditional employees who receive W-2s and are entitled to participate in a full array of benefits that we provide as part of our services for our clients. This arrangement benefits WSEs by providing additional work opportunities through access to our clients. WSEs further benefit from employee status and access to benefits through our plan offerings, including minimum essential health insurance coverage and 401(k) plans, as well as workers’ compensation coverage.

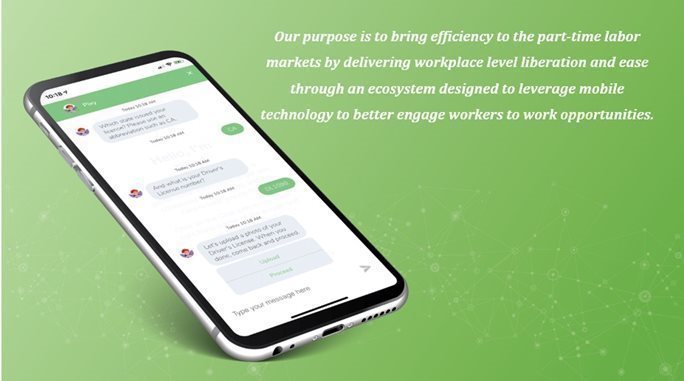

Technological Solution

At the heart of our EAS solution is a secure, cloud-based HRIS platform accessible by a desktop or mobile device through which our WSEs can onboard in a speedy, efficient and paperless manner, and then find available shift work at our client locations. We believe that this solution addresses effectively the dual issues of assisting WSEs seeking additional work and clients looking to fill open shifts. We believe that the easy-to-use onboarding functionality embedded in our HRIS platform will increase our pool of WSEs and provide a deep bench of worker talent for our business clients. The onboarding feature of our software enables us to capture all application process related data regarding our assigned employees and to introduce employees to and integrate them into the “ShiftPixy Ecosystem”. The mobile application features a chatbot that leverages artificial intelligence to aid in gathering the data from workers via a series of questions designed to capture all required information, including customer specific and governmental information. Final onboarding steps requiring signatures can also be prepared from the HRIS onboarding module. | | Figure 4 |

|

|

Our HRIS platform consists of a closed proprietary operating and processing information system that provides a tool for businesses needing staffing flexibility to schedule existing employees and to post open schedule slots to be filled by an available pool of shift workers (the “ShiftPixy Ecosystem”). The ShiftPixy Ecosystem provides the following benefits for our clients:

| 1. | Compliance: While our clients retain responsibility for compliance with labor and employment laws to the extent that such compliance depends upon their exclusive control over the worksite, we assume responsibility for a substantial portion of our clients’ wage and hour regulatory obligations through our role as legal employer of the WSEs. The ShiftPixy Ecosystem allows us to assist our clients in fulfilling their compliance obligations by providing a qualified pool of potential applicants as shift workers who are our legal employees. This serves to lessen the regulatory and compliance burden on our clients’ management, allowing them to focus more on the management of their business and less on legal issues. |

| | |

| 2. | Improved staffing fulfillment, recruiting, and retention: We believe that utilization of our HRIS platform reduces the impact of high work site employees “WSE” turnover, which is a consistent problem across the markets we serve. A significant issue at the end of Fiscal 2021 and part of Fiscal 2022 was the limited availability of WSEs in a “tight” labor market. Our platform provides an attractive avenue for pre-screened WSE applicants to find permanent positions that meet their needs through access to the ShiftPixy Ecosystem, which we believe results in a deeper potential labor pool for our clients to address their human capital needs. We also can function as a “flex” employer for WSEs who may be working full or part-time for other employers but want to have an additional source of income. |

| | |

| 3. | Cost Savings: The payroll and related costs associated with WSEs such as workers’ compensation and benefits are consolidated and charged, in effect, in conjunction with the shifters’ applicable rates of pay, allowing our clients to fund the employment related costs as the services are incurred, thereby avoiding various lump sum employment-related costs. We believe that our clients typically experience reductions in overhead costs related to HR compliance, payroll processing, WSE turnover and related costs, and elimination of non-compliance fines and related penalties, although the amount of cost savings realized varies from client to client. We exploit economies of scale in purchasing employer related solutions such as workers’ compensation and other benefits, which allows us to provide human capital services at a lower cost than we believe most businesses otherwise can typically staff a particular position. |

| | |

| 4. | Improved human capital management: Through access to our HRIS platform and our pool of human capital, our clients can scale up or down more rapidly, making it easier for them to contain and manage operational costs. We charge a fixed percentage on wages that allows our clients to budget and plan more accurately and efficiently without worrying about missteps arising from a wide range of legal and compliance issues for which we assume responsibility. |

During Fiscal 2019, we added a scheduling component to our application that enables our clients to schedule workers and to identify shift gaps that need to be filled. We use artificial intelligence (“AI”) to maintain schedules and fulfillment, using an active methodology to engage and move people to action. Included in this scheduling component is our “shift intermediation” functionality, which is designed to enable our WSEs to receive information and accept available shift work opportunities at multiple worksite locations. Our embedded AI is designed to monitor and accelerate the matching of WSEs with gig work opportunities. Our system monitors the capabilities of each WSE based on their work experience, needs, and training and provides messaging to clients and WSEs. The system matches worker requirements such as hours, position, and pay rate with client requirements such as experience, pay offered, hours offered and both employee and employer ratings. Similar to the way gig drivers are matched with gig riders through a smartphone app, our gig client opportunities are matched with WSEs for improved open job fulfillment. We believe this job fulfillment automation, using our HRIS platform, provides real-time human capital information to our clients and is a significant product differentiation feature.

Our goal is to have a mature and robust hosted cloud-based HRIS platform coupled with a seamless and technically sophisticated mobile smartphone application that will act as both a revenue generation system as well as a “viral” client acquisition engine through the combination of the scheduling, delivery, and intermediation features and interactions. We believe that once a critical mass of clients and WSEs is achieved, more shift opportunities will be created in the industries we serve. Our approach to achieving this critical mass is currently focused to build a national staffing footprint.

We expect our current business plan that focusses on acquisitions that is expected to be funded with either debt or stock, to be key drivers in supplying a significant number of WSEs across a national footprint and achieving the critical mass necessary for our technology to flourish. The development and integration of these vertical markets for our current business plan for bulk onboarding of WSEs is the focus of our growth. .

Opportunity

Shortly after the beginning of the pandemic, once it became clear that the business interruption would be prolonged and more extensive than originally contemplated, our management team began to make adaptations to our business strategy to capitalize on the pandemic related disruptions and what we believed to be the opportunities that would arise during a recovery. We realized that the COVID-19 pandemic created an employment shock that required a revised strategy and opened up opportunities to capitalize on a disrupted market. Our growth initiatives were created out of the changes underway in the early part of the pandemic and included new go-to-market strategies, and new service lines.

We see our opportunities to be multi-faceted. Our business strategy is to monetize our HRIS platform within observed and expected disruptions to the human capital market. We have designed our customer engagement to be agile in meeting the needs of a disrupted workforce and a rapidly changing work environment. The Company was founded, in part, with the goal to be properly positioned with a valuable service offering for the human capital marketplace and thereby ready to capitalize on the next wave of disruption.

According to an article from Forbes dated July 21, 2022 (“3 Reasons Businesses Are Tapping Into The Gig Economy”), The gig economy is booming, and business leaders are taking note. From the C-suite on down, Mercer’s 2022 Global Talent Trends report shows that gig is becoming a favored strategy, with six in 10 executives embracing this work model. The increase in preference for gig workers is not surprising considering the exponential growth the gig economy has seen in recent months. Ballooning by 30% during the pandemic, the gig workforce is now on track to surpass the full-time workforce in size by 2027. This phenomenon has prompted changes in business strategies that will assist organizations as they battle labor shortages, inflation, and prepare for the future of work.

According to an article from Zippia dated September 22, 2022 ("23 essential gig economy statistics 2022")

| · | At least 59 million American adults participated in the gig economy over 2020, roughly to 36% of the U.S. workforce. |

| | |

| · | 16% of U.S adults have earned money through an online gig platform at some point in their lives, and 9% earned income from online gig work in 2021. |

| | |

| · | Wages and participation for gig workers grew by 33% in 2020. |

| | |

| · | Gig workers contributed around $1.21 trillion to the U.S. economy in 2020, which is roughly 5.7% of the total U.S. GDP. |

| | |

| · | By the end of 2023, experts predict that 52% of the American workforce will have spent some time participating in the gig economy. |

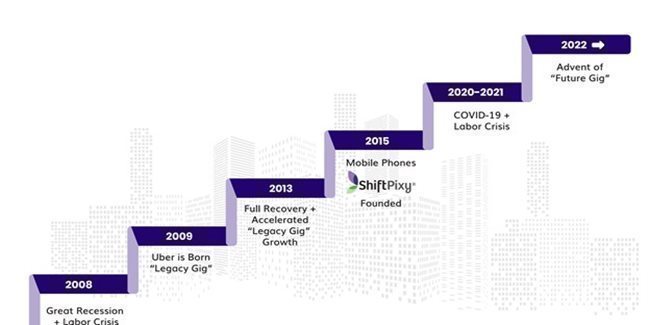

We have observed the following pattern in the development of the gig economy over the past fifteen years:

Figure 5

Each economic crisis creates chaos and disruption along with significant opportunities once recovery ensues. Our veteran management team has observed and learned from the technological and economic trends of the past 25 years, along with the resultant changes to the human capital markets, including the dot.com bubble, post 9/11 economic shocks, and the two more recent financial crises: the 2008 “Great Recession” and the 2020 COVID-19 crisis. We observed the creation of an entirely new approach to part time “gig” work after the 2008 economic crisis with the rise of companies that eschewed the traditional employer-employee relationship in favor of an “independent contractor” model, and which primarily focused on driver and delivery services. The resultant employment opportunities typically produced lower paying jobs that required a lower level of skill and expertise, and often deprived workers of health and welfare benefits that are typical, and often required, in the traditional employer-employee relationship. We call these early gig worker companies, like Uber and Postmates, “Legacy Gig” companies, which emerged in large numbers after the Great Recession. These companies experienced significant growth within five years of the 2008 crisis by capitalizing on a combination of factors, including the economic recovery itself, the companies’ ability to find a technological solution for the desire of the workforce to find more flexible work options, and the growing proliferation and sophistication of mobile smartphones. While these Legacy Gig providers have enjoyed great success, they are now facing significant pushback from regulatory authorities from their decision to embrace the independent contractor business model, which is under attack as a means of depriving employees of significant benefits and protections while evading traditional employer tax obligations.

The lessons learned from the Legacy Gig providers and the demographic shifts underpinning their success gave rise to the founding of ShiftPixy. In 2015, our founders Pixy evaluated the Legacy Gig businesses and believed that there was a need in the marketplace for a lower wage “gig” service provider to treat its workers as employees, with all of the traditional benefits and protections that employees have historically enjoyed, while also providing the flexibility that is the hallmark of the gig economy. The ShiftPixy Ecosystem and our HRIS platform were designed and continue to be enhanced with this goal in mind. The launch of ShiftPixy in 2015 coincided with the widespread adoption of smartphones throughout the population, making the marriage of WSEs and business on a distributed network on a grand scale possible.

Our business plan at inception was premised upon our belief that gig workers would eventually migrate away from an independent contractor to a more traditional employee/employer relationship that nonetheless provides the range of flexibility and choice commonly desired by workers in the gig economy. We also recognized a gap in the marketplace where traditional HR service providers were not providing a comprehensive services suite for gig workers on a level comparable to that typically provided to higher wage or salaried employees. We also came to recognize the likelihood that governmental regulators and tax authorities would ultimately object to the prevalent use of independent contractors by private businesses as a means to avoid paying certain taxes and avoid providing traditional employment benefits to their workers, and we believe that recent actions by federal, state and local governments have proved our predictions to be accurate. Therefore, as our business plan has evolved, we have avoided an independent contractor model, which we do not believe to be sustainable, in favor of a staffing model through which we employ our clients’ WSEs and provide them with a full range of traditional benefits.

Figure 6

More recently, there have been significant workplace shocks due to the COVID-19 pandemic. Increasingly and as is well documented in news media, those companies employing lower wage employees are experiencing significantly increased employee turnover and higher recruiting costs. We believe that the broader employment marketplace is undergoing a fundamental shift towards a new “Future Gig” workplace and further believe that ShiftPixy is well positioned to capitalize on the combination of a near term economic recovery and the longer-term demographic shift of younger and lower paid workers to a temporary and flexible work environment, as was seen with the early gig service provider business models. The financial markets have already recognized this opportunity in the growth and high value of companies focusing on the higher end salary or contract employment for professionals or creative personnel (as contractors and employees) and lower pay scale workers (as contractors) as well as significant investment in third party delivery. We believe that our commitment to a full employment staffing model, through which our WSEs are provided with a range of traditional employment benefits, uniquely positions us to attract Future Gig workers to our HRIS platform and the ShiftPixy Ecosystem.

Third party delivery constitutes an important part of our overall strategy to supply our clients with highly qualified WSEs at an affordable price while allowing them to regain control over their brands. Throughout the pandemic, many of our clients were forced to cede control over their brands to large third-party delivery services such as Postmates and UberEats to ensure their survival. The result was not only a dissipation of profits, but also a loss of control over the delivery experience and, in many cases, a decline in customer loyalty and goodwill. We believe that QSRs require more control over the delivery experience to ensure their future success which, in turn, requires more flexibility that can only be achieved through digital engagement. Our technology platform is designed with this goal in mind, focusing on real-time business intelligence for human capital while also providing additional key data capture that is critical to QSR success.

We had had made substantial investment that has been made in “ghost” kitchens, which we had believe to make significant changes in restaurant industry. We believe that our existing relationships with QSRs provide us with unique insight into the vulnerabilities and opportunities created by this third-party consumer disruption, and the primary work of ShiftPixy Labs is devoted to maximizing the monetization of this disruption through the creation and optimization of new vertical markets and opportunities, with the goal of creating additional shareholder value. However, we decided to delay the launch of the Ghost kitchen or Labs and the Company did not have enough capital to execute its business plans.

Markets and Marketing

Overview

Our products and services are designed primarily to help from the small to large sized businesses thrive in the gig economy by providing a cost-effective, legally compliant means to fulfill their staffing needs. As noted above, the worldwide trend toward a gig economy has been fueled largely by the widespread adoption of smartphones, which provide the technological means for remote office workers to move away from the traditional centralized workplace.

Most 18-to 30-year-old workers use a smartphone. This, in turn, has led to a significant disruption of the traditional employer-employee relationship, with supply management firm Ardent Partners reporting as far back as 2016 that nearly 42% of the world’s total workforce was considered “non-employee”, which includes temporary staff, gig workers, freelancers, and independent contractors.

We have designed our mobile application to take full advantage of this fundamental shift to the gig economy, which has been fueled by the near universal adoption of smartphones. Our initial marketing efforts focused on small and medium sized businesses struggling to find and maintain workers in the gig economy. In particular, we have targeted the restaurant and hospitality industries, which are characterized by high turnover and often use independent contractors to perform less than full-time gig engagements, primarily in the form of shift work. A significant problem for these businesses, along with many others in a wide variety of industries, involves compliance with employment related regulations imposed by federal, state and local governments. Requirements associated with workers’ compensation insurance, and other traditional employment compliance issues, including the employer mandate provisions of the ACA, create compliance challenges and increased costs. The compliance challenges are often complicated by “workaround” solutions to which many employers resort to avoid characterizing employees as “full-time” in an often futile attempt to avoid fines and penalties.

We believe that our services and HRIS platform provide a cost-effective, fully compliant solution for small businesses facing increasingly complex regulations and related litigation governing the classification and use of independent contractors. Recently in California, where most of our WSEs currently reside, legislation was passed that defines gig workers employed by Legacy Gig companies such as Lyft and Uber as employees rather than independent contractors, which we believe was a direct governmental response to a considerable loss of tax revenue derived from categorizing these WSEs as independent contractors. In November 2020, California voters passed Proposition 22, which nominally had the effect of repealing this legislation and restoring independent contractor status with respect to “app-based drivers.” Nevertheless, Proposition 22 also instituted various labor and wage policies that are specific to app-based drivers and their employers that do not apply to other independent contractors, including: (i) minimum wage requirements; (ii) working hours limitations; (iii) requiring companies to pay healthcare subsidies under certain circumstances; and (iv) requiring companies to provide or make available occupational accident insurance and accidental death insurance to their app-based drivers. We believe that there is an increasing likelihood that other states and municipalities will impose similar mandates in the near future, which will likely include, at a minimum, wage and benefit provisions similar to those guaranteed by Proposition 22.

Figure 7

Source: 11th Annual State of Independence in America, Data Highlights & Preview | August 2021 MBO Partners

Prior Focus and Marketing Efforts

Our business model provides a solution to this likely regulatory change by absorbing workers for these types of gig economy companies as our employees, significantly limiting the risk of litigation, fines and other related issues. Our early market focus was on the food service and hospitality industries, based primarily upon our understanding of the issues and challenges facing QSRs. Some of the key features incorporated in our mobile smartphone application to address these challenges include: (i) scheduling and intermediation functionality, which is designed to enhance the client’s experience through easy WSE scheduling and reducing turnover impact, and (ii) delivery functionality, which is designed to increase revenues through “in house” delivery fulfillment, thereby reducing delivery costs while creating a better customer experience and elevated engagement.

One of the most recent significant developments in the food and hospitality industry has been the rapid rise of third-party restaurant delivery Legacy Gig providers such as Uber EatsTM, GrubHubTM, and DoorDashTM. These providers have facilitated an increase in quick service restaurant or QSR sales in many local markets by providing food delivery to a wide-scale audience using independent contractor delivery drivers. Nevertheless, we have observed two significant issues negatively impacting on our clients as a result of their increased reliance upon third party delivery providers that have been widely reported. The first issue is the large revenue share typically being paid to third-party delivery providers as delivery fees. These additional costs erode QSR profits that would otherwise be generated by additional sales made through the delivery channel. The second issue is that our QSR clients have encountered logistical problems with food deliveries, including late deliveries, cold food, missing accessories, and unfriendly delivery people. This has caused significant “brand erosion”, causing these clients to reconsider third-party delivery.

While some larger chain restaurants have mitigated these additional costs and risks by moving to either a centralized food fulfillment center (commissary) or a “ghost” kitchen solution for their third-party delivery system, our clients typically lack the resources to follow this example. Our ShiftPixy Labs growth initiative, (described in more detail, below), focuses on addressing this issue for these smaller QSR operators through the use of our technology. Our HRIS platform allows our QSR clients to manage food deliveries in a cost-effective manner by using their own WSEs, (for whom we serve as the legal employer), through a customized “white label” mobile application. Our delivery feature links this “white label” delivery ordering system to our delivery solution, thereby freeing our clients to showcase their brands throughout the mobile ordering process while retaining back-office delivery functionality on a par with that offered by the Legacy Gig providers, including scheduling, ordering, and delivery status pushed to a customer’s smart phone. The first development phase of this aspect of our platform focused on driver onboarding functionality, which we completed during our fiscal year ended August 31, 2019 ("Fiscal 2019"). Additional features currently under development or already implemented allow us to “micro meter” the essential commercial insurance coverages required by our operator clients on a delivery-by-delivery basis (workers’ compensation and auto coverages), thereby overcoming a significant obstacle encountered by QSRs seeking to provide their own delivery services without relying on a Legacy Gig provider.

Our technology platform and approach to human capital management also provides a unique window into the daily demands of quick server restaurants (“QSR) operators, giving us the ability to extend our technology and engagement to optimize this self-delivery proposition. We expect our most recent enhancements to our driver management layer for operators in the ShiftPixy Ecosystem to allow our clients to use their own team members to control the delivery process from start to finish, yielding a more positive customer experience. We believe that our mobile application already provides the HR compliance, management and insurance solutions necessary to support a delivery option and create a turnkey self-delivery opportunity for the individual QSR operator.

The impact of the COVID-19 pandemic on our marketing efforts, along with its broader impact on the gig economy, appears to be mixed. According to a recent report issued by AppJobs through its Future Work Institute, the pandemic has fueled an increase in global demand for remote services such as delivery, online surveys and market research, while the demand for positions requiring entry into the home, such as house-sitting, babysitting and cleaning, has declined by 36%. Our experience with the bulk of our clients during the height of the pandemic largely confirms this research. Specifically, we observed a significant decline in our food and hospitality billed WSEs located in our Southern California markets during mid-March 2020, which coincided with the shutdown of many of our quick QSR clients’ dining locations. We began to experience some recovery in early May 2020, as various lockdown measures were relaxed and many restaurant operators created “work-around” solutions to new health and safety regulations, including improved takeout and delivery, as well as limited in-person dining. The reimplementation of lockdowns from November 2020 through February 2021 negatively impacted our WSE billings, although this was tempered somewhat by the receipt of COVID-19 related government payments such as the PPP Loan program. As of August 31, 2023, we have seen a recovery, and it is clear to us that the commercial landscape in the restaurant industry has moved towards a mix between restaurant delivered meals compared to in-person dining. Our ShiftPixy Labs initiative is largely designed to address this shift in demand. However, the commercial launch of Labs has been delayed to a future date until there is enough capital and proper staffing.

Figure 8

Market expansion

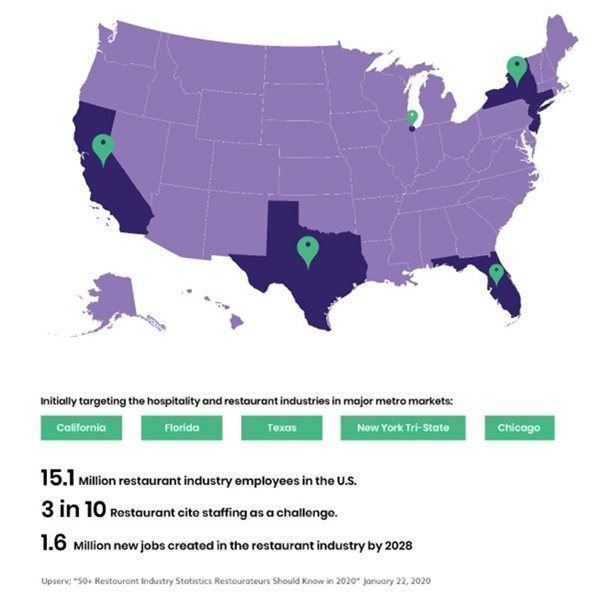

We view our ability to capture and utilize information pertaining to our target demographic to be integral to our future expansion and revenue growth. Although our clients were principally concentrated in Southern California, we believe that our expanded go-to-market strategy focused on building a national account portfolio managed by a newly-formed regional team of senior sales executives and ShiftPixy Labs initiatives have the potential, if successful, to result in the addition of a significant number of WSEs to the ShiftPixy ecosystem, covering a truly national footprint. Our current technology efforts are devoted to ensuring that our HRIS platform has the capacity to take full advantage of this projected future growth, which we believe is likely to result from the following factors:

| 1. | Large Potential Markets. |

| | |

| | Restaurant and Hospitality: Current statistics show that there are over 15.1 million WSEs in the restaurant and hospitality industries – representing over $300 billion in annual revenues – who are overwhelmingly working on a part-time basis. At our current monetization rate per WSE, this represents an annual gig economy revenue opportunity of over $9 billion per year for the United States. We believe that our ShiftPixy Labs initiative will position us to take full advantage of growth opportunities within this industry segment. |

| | Light Industrial Staffing: We project a target market approximating annual revenues $35 billion in North America derived from light industrial staffing, approximately 50% of which is currently consolidated in ten larger companies with the remainder divided amongst a multitude of smaller, regional entities. We believe that if our expanded go-to-market strategy focused on building a national account portfolio managed by a newly-formed regional team of senior sales executives, if successful in completing its business plan, it will make us a significant player in the light industrial staffing space with a nationwide footprint. We further believe that, if we are successful in entering into one or more CSAs with national account at regional levels, the resulting relationship will provide a nationwide outlet for our HRIS platform that will extend our geographic footprint dramatically, which in turn should result in significant increases to our revenues and earnings. |

| | |

| | Other Industries: Our present intention is to expand both our geographic footprint and our service offerings into other industries as well, particularly where part-time work is a significant component of the applicable labor force, including the retail, healthcare and technology sectors. |

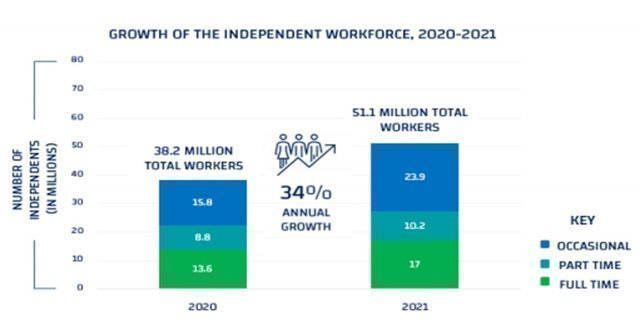

| 2. | Rapid Rise of Independent Workers. According to a recent study by Statista, the number of independent workers in the United States continues to increase significantly, regardless of the frequency of work. During Calendar 2021, there were approximately 23.9 million occasional independent workers in the United States, representing an increase from 12.9 million occasional independent workers estimated in Calendar 2017. |

| | |

| 3. | Technology Affecting Attitudes towards Employment Related Engagements. Gig economy platforms have changed the way that part-time and non-traditional WSEs identify and connect to work opportunities through the use of smartphone technology. Many demographic groups, including millennials, have embraced this technology as a means to secure short-term employment related engagements, as evidenced by the widespread adoption of smartphones. We believe that this demographic trend represents the “last mile” enabling technology solutions such as ours to provide superior worker engagement in the gig economy. |

| | |