UNITED STATES

SECURITIES AND

EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-CSRS

Investment Company Act file number: 811-06041

The Central

and Eastern Europe Fund, Inc.

(Exact Name of Registrant

as Specified in Charter)

875 Third Avenue

New York, NY 10022-6225

(Address of Principal

Executive Offices) (Zip Code)

Registrant’s

Telephone Number, including Area Code: (212) 454-4500

Diane Kenneally

100 Summer Street

Boston, MA 02110

(Name and Address of

Agent for Service)

| Date of fiscal year end: |

10/31 |

| |

|

| Date of reporting period: |

4/30/2023 |

| ITEM 1. |

REPORT TO STOCKHOLDERS |

| |

|

| |

(a) |

| |

|

April 30, 2023

Semiannual Report

to Shareholders

The Central and Eastern Europe Fund, Inc.

Ticker Symbol: CEE

Contents

The Central and Eastern Europe Fund, Inc. (“the Fund”)

seeks long-term capital appreciation through investment primarily in equity and equity-linked securities of issuers domiciled in Central and Eastern Europe.

Investments in funds involve risks, including the loss of principal.

The shares of

most closed-end funds, including the Fund, are not continuously offered. Once issued, shares of closed-end funds are bought and sold in the open market. Shares of closed-end funds frequently trade at a discount to net asset value. The price of the Fund’s shares is determined by a number of factors, several of which are beyond the control of the Fund. Therefore, the Fund

cannot predict whether its shares will trade at, below, or above net asset value.

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its

subsidiaries such as DWS Distributors, Inc. which offers investment products or DWS Investment Management Americas, Inc. and RREEF America L.L.C. which offer advisory services.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE

NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

|

|

|

|

|

|

|

| 2 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

|

|

Investing in foreign securities presents certain risks, such as currency fluctuations, political and economic changes, and

market risks. Emerging markets tend to be more volatile and less liquid than the markets of more mature economies, and generally have less diverse and less mature economic structures and less stable political systems than those of developed

countries. Any fund that focuses in a particular segment of the market or region of the world will generally be more volatile than a fund that invests more broadly. This Fund is non-diversified and can take larger positions in fewer issuers,

increasing its potential risk.

The United States, the European Union, the United Kingdom and other countries have imposed sanctions on Russia, Russian companies,

and Russian individuals in response to actions taken by Russia in recent years, including its February 2022 invasion of Ukraine and subsequent activities. In turn Russia has imposed sanctions on Western individuals, businesses and products, and the

Russian central bank has taken actions that have effectively frozen investments by Western entities, including the Fund, in Russian companies. Sanctions have adversely affected not only the Russian economy but also the economies of many countries in

Europe, including countries in Central and Eastern Europe, and the continuation of sanctions, or the imposition of new sanctions, may have further adverse effects on the Russian and European economies. As a result of Russia’s invasion of

Ukraine and resulting dislocations, the Western sanctions and the retaliatory measures, the value and liquidity of the Fund’s portfolio assets have been severely adversely affected, and its Russian investments (some of which are in companies

that are subject to sanctions) have been fair valued at zero since March 14, 2022 except Polymetal International PLC, an Anglo-Russian precious metals mining company registered in the British Crown Dependency of Jersey which continues to trade on

the London Stock Exchange. It is not known if the situation will improve.

War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises and

related geopolitical events have led, and, in the future, may lead to significant disruptions in U.S. and world economies and markets, which may lead to increased market volatility and may have significant adverse effects on the Fund and its

investments. In the case of the Fund, Russia’s invasion of Ukraine has materially adversely affected, and may continue to materially adversely affect, the value and liquidity of the Fund’s portfolio.

|

|

|

|

|

|

|

|

|

|

|

The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

3 |

|

|

|

|

| Letter to the Shareholders |

|

(Unaudited) |

Dear Shareholder,

For its most recent semiannual

period ended April 30, 2023, The Central and Eastern Europe Fund, Inc. (the ”Fund”) posted a total return in U.S. dollars (“USD”) of 37.16% based on net asset value (“NAV”) and 18.18% based on market price. The

Fund’s benchmark, the MSCI Emerging Markets Eastern Europe Index, returned 42.69% during the same period. The Fund traded at an average premium to NAV of 18.76% for the period in review, compared with an average premium of 1.00% for the same

period a year earlier.

After the removal of Russia from the benchmark in March of 2022, Poland is now by far the biggest country in our Central and Eastern Europe

(CEE) market investment universe, followed by Hungary and the Czech Republic. All three markets recovered significantly over the reporting period as investors began to price in a frozen conflict in Ukraine and expectations for higher energy prices

moderated. Sentiment with respect to the Polish equity market was additionally supported by the expectation of increased E.U. financial support. Inflation remained elevated, pushing out the timeline for interest rate cuts by central banks.

The overall resilient macroeconomic environment has supported consistently strong bank earnings. With a positive corporate earnings backdrop, fears of asset quality

issues at regional banks eased over the period while higher interest rates boosted the net interest income of these institutions. These supportive factors were reflected in the

|

|

|

|

|

|

|

|

|

| Country Breakdown (As a % of Net Assets) |

|

4/30/23 |

|

|

10/31/22 |

|

| Poland |

|

|

56% |

|

|

|

50% |

|

| Hungary |

|

|

18% |

|

|

|

19% |

|

| Czech Republic |

|

|

10% |

|

|

|

12% |

|

| Austria |

|

|

4% |

|

|

|

3% |

|

| United Kingdom |

|

|

4% |

|

|

|

2% |

|

| Moldova |

|

|

3% |

|

|

|

4% |

|

| France |

|

|

1% |

|

|

|

2% |

|

| Russia |

|

|

1% |

|

|

|

1% |

|

| Cash* |

|

|

3% |

|

|

|

7% |

|

| |

|

|

100% |

|

|

|

100% |

|

| * |

Includes Cash Equivalents and Other Assets and Liabilities, Net. |

|

|

|

|

|

|

|

| 4 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

|

|

performance of financial stocks, which rallied sharply from very depressed valuations. Due to the Fund’s fundamental concentration policy, which provided that the Fund may not invest more

than 25% of its total assets in the securities of any one industry, the Fund was significantly underweight in diversified banks as compared to its benchmark, and did not participate fully in this rally, which constrained performance relative to the

benchmark. Within financials, the Fund’s increased allocation and subsequent overweight to insurance companies contributed positively to performance on the back of supportive domestic trends for insurers in Poland, the segment’s strong

pricing power and some indirect exposure to the banking industry.

The Fund continued to increase its overweight to the energy sector, which had a positive impact on

performance. We viewed the sector as attractive on the basis of depressed valuations and solidly underpinned dividend payouts, despite concerns around the imposition of taxes on excess earnings (measured relative to a normal industrial cycle). While

supported by strong underlying trends, energy stocks experienced significant volatility over the period driven by pronounced swings in the price of oil as investors appeared to overlook the exposure of these companies to a wider range of factors.

Within Poland, the Fund has increased its exposure to companies within the industrials sector positioned to benefit from a stabilization in the Ukrainian economy,

particularly in the infrastructure sphere. More broadly, the Fund increased its exposure to Poland over the period while trimming positions in the Czech Republic and reducing its cash position.

Market Outlook

While inflation appears to be peaking, we do not expect

significantly lower inflation and central bank rate cuts until 2024. The outlook for Poland to access E.U. pandemic recovery funds has improved given the

|

|

|

|

|

|

|

|

|

| Sector Diversification (As a % of Equity Securities) |

|

4/30/23 |

|

|

10/31/22 |

|

| Financials |

|

|

32% |

|

|

|

33% |

|

| Energy |

|

|

24% |

|

|

|

22% |

|

| Consumer Discretionary |

|

|

11% |

|

|

|

10% |

|

| Consumer Staples |

|

|

9% |

|

|

|

10% |

|

| Utilities |

|

|

9% |

|

|

|

7% |

|

| Materials |

|

|

6% |

|

|

|

3% |

|

| Health Care |

|

|

5% |

|

|

|

6% |

|

| Communication Services |

|

|

2% |

|

|

|

8% |

|

| Industrials |

|

|

2% |

|

|

|

1% |

|

| Information Technology |

|

|

— |

|

|

|

0% |

|

| |

|

|

100% |

|

|

|

100% |

|

|

|

|

|

|

|

|

|

|

|

|

The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

5 |

|

country’s strong support for Ukraine and recent steps toward satisfying E.U. requirements around judicial independence and green energy. The recent meeting between the Polish Prime Minister

and Ukrainian President Zelensky underscored the potential structural importance of the relationship between the two nations from an economic standpoint once the conflict with Russia has been resolved.

From a sector perspective, while operating results for Polish financials have been strong, windfall taxation and loss provisions related to legacy mortgages, denominated

in the Swiss franc and underwritten before the Great Financial Crisis of 2007-2008, have weighed on bank profitability. As these headwinds ease, sentiment with respect to the sector should benefit. We do not see significant risks to asset quality

for CEE banks broadly in the short term as the overall business environment is supportive, even with the prospect of interest rates easing from current high levels. With respect to consumer-related sectors, with labor markets still tight and wages

gradually increasing, disposable income could benefit as inflation ultimately recedes. That said, we prefer value/discount retailers relative to general apparel or consumer staples companies which are experiencing margin pressures.

While the timeline is difficult to forecast, we have been increasing exposure to companies which stand to benefit from a recovery of

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ten Largest Equity Holdings at April 30, 2023

(64.0% of Net Assets) |

|

Country |

|

Percent |

|

| |

1. |

|

|

Polski Koncern Naftowy ORLEN SA |

|

Poland |

|

|

13.7 |

% |

| |

2. |

|

|

Powszechny Zaklad Ubezpieczen SA |

|

Poland |

|

|

8.3 |

% |

| |

3. |

|

|

MOL Hungarian Oil & Gas PLC |

|

Hungary |

|

|

6.5 |

% |

| |

4. |

|

|

CEZ AS |

|

Czech Republic |

|

|

6.4 |

% |

| |

5. |

|

|

Bank Polska Kasa Opieki SA |

|

Poland |

|

|

5.7 |

% |

| |

6. |

|

|

OTP Bank Nyrt |

|

Hungary |

|

|

5.6 |

% |

| |

7. |

|

|

Richter Gedeon Nyrt |

|

Hungary |

|

|

4.8 |

% |

| |

8. |

|

|

KGHM Polska Miedz SA |

|

Poland |

|

|

4.6 |

% |

| |

9. |

|

|

Dino Polska SA |

|

Poland |

|

|

4.6 |

% |

| |

10. |

|

|

Allegro.eu SA |

|

Poland |

|

|

3.8 |

% |

Portfolio holdings and characteristics are subject to change and not

indicative of future portfolio composition.

For more details about the Fund’s investments, see the Schedule of Investments commencing on page 10. For additional

information about the Fund, including performance, dividends, presentations, press releases, market updates, daily NAV and shareholder reports, please visit dws.com.

|

|

|

|

|

| 6 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

Ukraine’s economy. Many of these companies have had operating units in Ukraine or still have these units and would quickly benefit from an uptick in business activity there. Banks would be

among the beneficiaries of this trend as it would stimulate higher corporate loan demand.

From a valuation standpoint, both the Polish and Hungarian equity markets

are trading at significant discounts to the overall global emerging markets average, whereas the Czech equity market is trading at a premium, predominately due to one stock. We continue to closely monitor developments affecting foreign investors in

Russian securities. No assurances can be given that the extreme adverse environment for U.S. investors, such as the Fund, will improve.

Sincerely,

|

|

|

|

|

|

|

|

|

|

| Christian Strenger |

|

Sebastian Kahlfeld |

|

Hepsen Uzcan |

| Chairman |

|

Portfolio Manager |

|

Interested Director, President and Chief Executive Officer |

The views expressed in the preceding discussion regarding portfolio management matters are only through the end of the period of the

report as stated on the cover. Portfolio management’s views are subject to change at any time based on market and other conditions and should not be construed as recommendations. Past performance is no guarantee of future results.

Current and future portfolio holdings are subject to risk, including geopolitical and other risks.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

7 |

|

|

|

|

| Performance Summary |

|

April 30, 2023 (Unaudited) |

All performance shown is historical, assumes reinvestment of all dividend and capital gain distributions, and does not guarantee

future results. Investment return and net asset value fluctuate with changing market conditions so that, when sold, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data

quoted. Please visit dws.com for the most recent performance of the Fund.

Fund specific data and performance are provided for informational purposes only

and are not intended for trading purposes.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average Annual Total Returns as of 4/30/23 |

|

|

|

|

|

|

| |

|

6-Month‡ |

|

|

1-Year |

|

|

5-Year |

|

|

10-Year |

|

| Net Asset Value(a) |

|

|

37.16 |

% |

|

|

12.63% |

|

|

|

(18.94)% |

|

|

|

(10.58)% |

|

| Market Price(a) |

|

|

18.18 |

% |

|

|

(26.98)% |

|

|

|

(16.48)% |

|

|

|

(9.46)% |

|

| MSCI Emerging Markets Eastern Europe Index(b) |

|

|

42.69 |

% |

|

|

13.15% |

|

|

|

(22.54)% |

|

|

|

(11.77)% |

|

| Blended Index |

|

|

42.69 |

% |

|

|

13.15% |

|

|

|

(22.54)% |

(c) |

|

|

(12.81)% |

(c) |

|

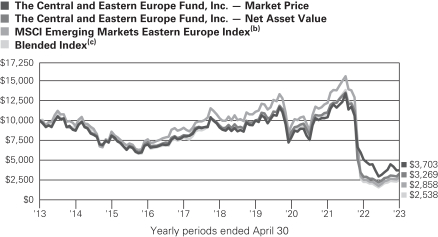

| Growth of an Assumed $10,000 Investment |

The growth of $10,000 is

cumulative.

| a |

Total return based on net asset value reflects changes in the Fund’s net asset value during each period. Total return

based on market value reflects changes in market value during each period. Each figure includes reinvestments of income and capital gain distributions, if any. Total returns based on net asset value and market price will differ depending upon the

level of any discount from or premium to net asset value at which the Fund’s shares trade during the period. Expenses of the Fund include investment advisory and administration fees and other fund expenses. Total returns shown take into

|

|

|

|

|

|

| 8 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

| |

account these fees and expenses. The annualized expense ratio of the Fund for the six months ended April 30, 2023 was 1.79%. |

| b |

The MSCI Emerging Markets Eastern Europe Index is a free-float weighted equity

index that is designed to capture large and mid cap representation across three emerging markets countries in Eastern Europe (Czech Republic, Hungary, and Poland). |

| |

Effective March 9, 2022, MSCI Inc. removed Russian securities from the MSCI Emerging Markets Eastern Europe Index.

|

| c |

Blended Index represents: MSCI Emerging Markets Europe Index from May 1, 2013 through February 29, 2016; MSCI

Emerging Markets Europe ex Greece Index from March 1, 2016 through July 31, 2017; and MSCI Emerging Markets Eastern Europe Index since August 1, 2017. |

| |

Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index.

|

| ‡ |

Total returns shown for periods less than one year are not annualized. |

|

|

|

|

|

|

|

|

|

| Net Asset Value and Market Price |

|

|

|

|

| |

|

As of 4/30/23 |

|

|

As of 10/31/22 |

|

| Net Asset Value |

|

$ |

7.98 |

|

|

$ |

5.96 |

|

| Market Price |

|

$ |

8.12 |

|

|

$ |

7.05 |

|

Prices and Net Asset Value fluctuate and are not guaranteed.

|

|

|

|

|

| Distribution Information |

|

Per Share |

|

| Six Months as of 4/30/23: |

|

|

|

|

| Income Distribution |

|

$ |

0.24 |

|

Distributions are historical, not guaranteed and will fluctuate. Distributions do not include return of capital or other non-income sources.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

9 |

|

|

|

|

| Schedule of Investments |

|

as of April 30, 2023 (Unaudited) |

|

|

|

|

|

|

|

|

|

| |

|

Shares |

|

|

Value ($) |

|

| Poland 55.9% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Banks 11.5% |

|

|

|

|

|

|

|

|

|

|

|

| Bank Polska Kasa Opieki SA |

|

|

125,000 |

|

|

|

2,890,755 |

|

|

|

|

| Powszechna Kasa Oszczednosci Bank Polski SA |

|

|

220,000 |

|

|

|

1,699,974 |

|

|

|

|

| Santander Bank Polska SA |

|

|

15,000 |

|

|

|

1,222,321 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5,813,050 |

|

|

|

|

| Broadline Retail 3.8% |

|

|

|

|

|

|

|

|

| Allegro.eu SA 144A* |

|

|

240,000 |

|

|

|

1,891,815 |

|

|

|

|

| Commercial Services & Supplies 0.6% |

|

|

|

|

|

|

|

|

| Mo-BRUK SA |

|

|

4,000 |

|

|

|

280,462 |

|

|

|

|

| Construction & Engineering 1.0% |

|

|

|

|

|

|

|

|

| Budimex SA |

|

|

5,500 |

|

|

|

485,025 |

|

|

|

|

| Consumer Staples Distribution & Retail 5.5% |

|

|

|

|

|

|

|

|

|

|

|

| Dino Polska SA 144A* |

|

|

22,500 |

|

|

|

2,295,376 |

|

|

|

|

| Eurocash SA* |

|

|

100,000 |

|

|

|

457,075 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,752,451 |

|

|

|

|

| Electric Utilities 2.0% |

|

|

|

|

|

|

|

|

| PGE Polska Grupa Energetyczna SA* |

|

|

600,000 |

|

|

|

994,338 |

|

|

|

|

| Entertainment 1.1% |

|

|

|

|

|

|

|

|

|

|

|

| 11 bit studios SA* |

|

|

1,000 |

|

|

|

150,833 |

|

|

|

|

| CD Projekt SA |

|

|

15,000 |

|

|

|

409,489 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

560,322 |

|

|

|

|

| Insurance 8.2% |

|

|

|

|

|

|

|

|

| Powszechny Zaklad Ubezpieczen SA |

|

|

450,000 |

|

|

|

4,152,712 |

|

|

|

|

| Metals & Mining 5.1% |

|

|

|

|

|

|

|

|

|

|

|

| Grupa Kety SA |

|

|

2,000 |

|

|

|

273,233 |

|

|

|

|

| KGHM Polska Miedz SA |

|

|

80,000 |

|

|

|

2,301,520 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2,574,753 |

|

|

|

|

| Oil, Gas & Consumable Fuels 13.7% |

|

|

|

|

|

|

|

|

| Polski Koncern Naftowy ORLEN SA |

|

|

450,000 |

|

|

|

6,876,370 |

|

|

|

|

| Textiles, Apparel & Luxury Goods 3.4% |

|

|

|

|

|

|

|

|

| LPP SA |

|

|

600 |

|

|

|

1,734,814 |

|

| Total Poland (Cost $25,121,018) |

|

|

|

|

|

|

28,116,112 |

|

|

|

|

| Hungary 17.9% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Banks 5.6% |

|

|

|

|

|

|

|

|

| OTP Bank Nyrt |

|

|

92,500 |

|

|

|

2,815,705 |

|

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

| 10 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

|

|

|

|

|

|

|

|

|

| |

|

Shares |

|

|

Value ($) |

|

|

|

|

| Diversified Telecommunication Services 1.0% |

|

|

|

|

|

|

|

|

| Magyar Telekom Telecommunications PLC (ADR)* |

|

|

400,000 |

|

|

|

503,591 |

|

|

|

|

| Oil, Gas & Consumable Fuels 6.5% |

|

|

|

|

|

|

|

|

| MOL Hungarian Oil & Gas PLC |

|

|

405,985 |

|

|

|

3,289,922 |

|

|

|

|

| Pharmaceuticals 4.8% |

|

|

|

|

|

|

|

|

| Richter Gedeon Nyrt |

|

|

100,000 |

|

|

|

2,414,516 |

|

| Total Hungary (Cost $8,038,342) |

|

|

|

|

|

|

9,023,734 |

|

|

|

|

| Czech Republic 9.7% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Banks 3.2% |

|

|

|

|

|

|

|

|

|

|

|

| Komercni Banka AS |

|

|

50,000 |

|

|

|

1,618,096 |

|

|

|

|

| Moneta Money Bank AS 144A |

|

|

1,000 |

|

|

|

3,681 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,621,777 |

|

|

|

|

| Electric Utilities 6.5% |

|

|

|

|

|

|

|

|

| CEZ AS |

|

|

60,000 |

|

|

|

3,234,783 |

|

| Total Czech Republic (Cost $3,779,937) |

|

|

|

|

|

|

4,856,560 |

|

|

|

|

| Austria 4.6% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Banks 2.0% |

|

|

|

|

|

|

|

|

| Erste Group Bank AG |

|

|

27,500 |

|

|

|

998,876 |

|

|

|

|

| Oil, Gas & Consumable Fuels 2.6% |

|

|

|

|

|

|

|

|

| OMV AG |

|

|

27,500 |

|

|

|

1,300,269 |

|

| Total Austria (Cost $2,038,358) |

|

|

|

|

|

|

2,299,145 |

|

|

|

|

| United Kingdom 3.6% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Broadline Retail 3.6% |

|

|

|

|

|

|

|

|

| Pepco Group NV (Registered) (Cost $1,853,050)* |

|

|

190,000 |

|

|

|

1,825,699 |

|

|

|

|

| Moldova 3.4% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Beverages 3.4% |

|

|

|

|

|

|

|

|

| Purcari Wineries PLC (Registered) (Cost $1,725,060) |

|

|

775,000 |

|

|

|

1,734,246 |

|

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

11 |

|

|

|

|

|

|

|

|

|

|

| |

|

Shares |

|

|

Value ($) |

|

| France 1.0% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Oil, Gas & Consumable Fuels 1.0% |

|

|

|

|

|

|

|

|

| TotalEnergies SE (Cost $354,903) |

|

|

7,500 |

|

|

|

479,613 |

|

|

|

|

| Russia 0.5% |

|

|

|

|

|

|

|

|

| Common Stocks |

|

|

|

|

|

|

|

|

|

|

|

| Banks 0.0% |

|

|

|

|

|

|

|

|

|

|

|

| Sberbank of Russia PJSC* (a) |

|

|

3,600,000 |

|

|

|

0 |

|

|

|

|

| TCS Group Holding PLC (GDR) (Registered)* (a) |

|

|

87,331 |

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

| Broadline Retail 0.0% |

|

|

|

|

|

|

|

|

| Ozon Holdings PLC (ADR)* (a) |

|

|

60,000 |

|

|

|

0 |

|

|

|

|

| Chemicals 0.0% |

|

|

|

|

|

|

|

|

|

|

|

| PhosAgro PJSC (GDR) (Registered)* (a) |

|

|

90,000 |

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

| Consumer Staples Distribution & Retail 0.0% |

|

|

|

|

|

|

|

|

|

|

|

| Fix Price Group PLC (GDR) (Registered)* (a) |

|

|

125,000 |

|

|

|

0 |

|

|

|

|

| Magnit PJSC* (a) |

|

|

63,909 |

|

|

|

0 |

|

|

|

|

| Magnit PJSC (GDR) (Registered)* (a) |

|

|

5 |

|

|

|

0 |

|

|

|

|

| X5 Retail Group NV (GDR) (Registered)* (a) |

|

|

137,884 |

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

| Interactive Media & Services 0.0% |

|

|

|

|

|

|

|

|

| Yandex NV ‘‘A’’* (a) |

|

|

188,000 |

|

|

|

0 |

|

|

|

|

| Metals & Mining 0.5% |

|

|

|

|

|

|

|

|

|

|

|

| Alrosa PJSC* (a) |

|

|

1,670,000 |

|

|

|

0 |

|

|

|

|

| Magnitogorsk Iron & Steel Works PJSC (GDR) (Registered)* (a) |

|

|

74,569 |

|

|

|

0 |

|

|

|

|

| MMC Norilsk Nickel PJSC (ADR)* (a) |

|

|

50,000 |

|

|

|

0 |

|

|

|

|

| Polymetal International PLC |

|

|

75,000 |

|

|

|

263,980 |

|

|

|

|

| Polyus PJSC (GDR) (Registered)* (a) |

|

|

20,000 |

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

263,980 |

|

|

|

|

| Oil, Gas & Consumable Fuels 0.0% |

|

|

|

|

|

|

|

|

|

|

|

| Gazprom PJSC** (a) |

|

|

5,000,000 |

|

|

|

0 |

|

|

|

|

| Lukoil PJSC** (a) |

|

|

209,500 |

|

|

|

0 |

|

|

|

|

| Novatek PJSC (GDR) (Registered)* (a) |

|

|

37,500 |

|

|

|

0 |

|

|

|

|

| Tatneft PJSC

(ADR)† * (a) |

|

|

100,000 |

|

|

|

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

|

|

|

|

| Wireless Telecommunication Services 0.0% |

|

|

|

|

|

|

|

|

| Mobile Telesystems PJSC (ADR)* (a) |

|

|

250,000 |

|

|

|

0 |

|

| Total Russia (Cost $65,914,090) |

|

|

|

|

|

|

263,980 |

|

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

| 12 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

|

|

|

|

|

|

|

|

|

| |

|

Shares |

|

|

Value ($) |

|

| Securities Lending Collateral 0.5% |

|

|

|

|

|

|

|

|

| DWS Government & Agency Securities Portfolio ‘‘DWS Government Cash Institutional

Shares’’, 4.74%

(Cost $257,400) (b) (c) |

|

|

257,400 |

|

|

|

257,400 |

|

|

|

|

| Cash Equivalents 3.4% |

|

|

|

|

|

|

|

|

| DWS Central Cash Management Government Fund, 4.81%

(Cost $1,689,548) (c) |

|

|

1,689,548 |

|

|

|

1,689,548 |

|

|

|

|

| |

|

% of Net

Assets |

|

|

Value ($) |

|

| Total Investment Portfolio (Cost $110,771,706) |

|

|

100.5 |

|

|

|

50,546,037 |

|

| Other Assets and Liabilities, Net |

|

|

(0.5 |

) |

|

|

(242,051 |

) |

| |

|

| Net Assets |

|

|

100.0 |

|

|

|

50,303,986 |

|

A summary of the Fund’s transactions with affiliated investments during the period ended April 30, 2023 are as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Value ($)

at

10/31/2022 |

|

Pur-

chases

Cost

($) |

|

|

Sales

Proceeds

($) |

|

|

Net

Real-

ized

Gain/

(Loss)

($) |

|

|

Net

Change

in

Unreal-

ized

Appreci-

ation/

(Depreci-

ation)

($) |

|

|

Income

($) |

|

|

Capital

Gain

Distri-

butions

($) |

|

|

Number of

Shares at

4/30/2023 |

|

|

Value ($)

at

4/30/2023 |

|

| Securities Lending Collateral 0.5% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| DWS Government & Agency Securities Portfolio ‘‘DWS Government Cash Institutional Shares’’, 4.74% (b) (c) |

|

| 1,444,172 |

|

|

— |

|

|

|

1,186,772 |

(d) |

|

|

— |

|

|

|

— |

|

|

|

10,027 |

|

|

|

— |

|

|

|

257,400 |

|

|

|

257,400 |

|

| Cash Equivalents 3.4% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| DWS Central Cash Management Government Fund, 4.81% (c) |

|

| 2,511,880 |

|

|

4,884,739 |

|

|

|

5,707,071 |

|

|

|

— |

|

|

|

— |

|

|

|

37,142 |

|

|

|

— |

|

|

|

1,689,548 |

|

|

|

1,689,548 |

|

| 3,956,052 |

|

|

4,884,739 |

|

|

|

6,893,843 |

|

|

|

— |

|

|

|

— |

|

|

|

47,169 |

|

|

|

— |

|

|

|

1,946,948 |

|

|

|

1,946,948 |

|

| * |

Non-income producing security. |

| ** |

Non-income producing security; due to applicable sanctions, dividend income was

not recorded. |

| † |

All or a portion of these securities were on loan. The value of all securities loaned at April 30, 2023 amounted to

$0.0, which is 0.0% of net assets. |

| (a) |

Investment was valued using significant unobservable inputs. |

| (b) |

Represents cash collateral held in connection with securities lending. Income earned by the Fund is net of borrower

rebates. |

| (c) |

Affiliated fund managed by DWS Investment Management Americas, Inc. The rate shown is the annualized seven-day yield at period end. |

| (d) |

Represents the net increase (purchases cost) or decrease (sales proceeds) in the amount invested in cash collateral for

the period ended April 30, 2023. |

The accompanying notes

are an integral part of the financial statements.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

13 |

|

144A: Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in

transactions exempt from registration, normally to qualified institutional buyers.

ADR: American Depositary Receipt (See Note E in the Notes to the Financial

Statements)

GDR: Global Depositary Receipt (See Note E in the Notes to the Financial Statements)

PJSC: Public Joint Stock Company

For purposes of its industry concentration policy,

the Fund classifies issuers of portfolio securities at the industry sub- group level. Certain of the categories in the above Schedule of Investments consist of multiple industry

sub-groups or industries.

Fair Value Measurements

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in three broad levels. Level 1 includes quoted prices in

active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds and credit risk). Level 3 includes significant unobservable

inputs (including the Fund’s own assumptions in determining the fair value of investments). The level assigned to the securities valuations may not be an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of April 30, 2023 in valuing the Fund’s investments.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Assets |

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

|

| Common Stocks (e) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Poland |

|

$ |

28,116,112 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

28,116,112 |

|

| Hungary |

|

|

9,023,734 |

|

|

|

— |

|

|

|

— |

|

|

|

9,023,734 |

|

| Czech Republic |

|

|

4,856,560 |

|

|

|

— |

|

|

|

— |

|

|

|

4,856,560 |

|

| Austria |

|

|

2,299,145 |

|

|

|

— |

|

|

|

— |

|

|

|

2,299,145 |

|

| United Kingdom |

|

|

1,825,699 |

|

|

|

— |

|

|

|

— |

|

|

|

1,825,699 |

|

| Moldova |

|

|

1,734,246 |

|

|

|

— |

|

|

|

— |

|

|

|

1,734,246 |

|

| France |

|

|

479,613 |

|

|

|

— |

|

|

|

— |

|

|

|

479,613 |

|

| Russia |

|

|

263,980 |

|

|

|

— |

|

|

|

0 |

|

|

|

263,980 |

|

| Short-Term Instruments (e) |

|

|

1,946,948 |

|

|

|

— |

|

|

|

— |

|

|

|

1,946,948 |

|

| Total |

|

$ |

50,546,037 |

|

|

$ |

— |

|

|

$ |

0 |

|

|

$ |

50,546,037 |

|

(e) See Schedule of Investments for additional detailed categorizations.

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

| 14 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

Statement of Assets and Liabilities

|

|

|

|

|

| as of April 30, 2023 (Unaudited) |

|

|

|

|

|

|

|

|

|

|

|

| Assets |

|

|

|

|

| Investments in non-affiliated securities, at value (cost $108,824,758) |

|

$ |

48,599,089 |

|

| Investment in DWS Central Cash Management Government Fund (cost $1,689,548) |

|

|

1,689,548 |

|

| Investment in DWS Government & Agency Securities Portfolio (cost $257,400)* |

|

|

257,400 |

|

| Foreign currency, at value (cost $54,212) |

|

|

50,606 |

|

| Receivable for investments sold |

|

|

396,976 |

|

| Dividends receivable |

|

|

121,018 |

|

| Foreign taxes recoverable |

|

|

178,192 |

|

| Interest receivable |

|

|

3,761 |

|

| Other assets |

|

|

21,152 |

|

| Total assets |

|

|

51,317,742 |

|

|

|

| Liabilities |

|

|

|

|

| Payable upon return of securities loaned |

|

|

257,400 |

|

| Payable for investments purchased |

|

|

496,934 |

|

| Payable for Directors’ fees and expenses |

|

|

57,668 |

|

| Investment advisory fee payable |

|

|

14,378 |

|

| Administration fee payable |

|

|

7,668 |

|

| Accrued expenses and other liabilities |

|

|

179,708 |

|

| Total liabilities |

|

|

1,013,756 |

|

| Net assets |

|

$ |

50,303,986 |

|

|

|

| Net Assets Consist of |

|

|

|

|

| Distributable earnings (loss) |

|

|

(129,850,600 |

) |

| Paid-in capital |

|

|

180,154,586 |

|

| Net assets |

|

$ |

50,303,986 |

|

|

|

| Net Asset Value |

|

|

|

|

|

|

Net assets value per share

($50,303,986 ÷ 6,300,392 shares of common stock issued and outstanding, $.001 par value, 80,000,000 shares authorized) |

|

$ |

7.98 |

|

| * |

Represents collateral on securities loaned. |

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

15 |

|

Statement of Operations

|

|

|

|

|

| for the six months ended April 30, 2023 (Unaudited) |

|

|

|

|

|

|

|

|

|

|

|

| Net Investment Income |

|

|

|

|

| Income: |

|

|

|

|

|

|

| Dividends (net of foreign withholding taxes of $41,911) |

|

$ |

235,322 |

|

| Income distributions — DWS Central Cash Management Government Fund |

|

|

37,142 |

|

| Securities lending income, net of borrower rebates |

|

|

10,027 |

|

| Total investment income |

|

|

282,491 |

|

| Expenses: |

|

|

|

|

|

|

| Investment advisory fee |

|

|

164,094 |

|

| Administration fee |

|

|

43,758 |

|

| Custody and accounting fee |

|

|

36,573 |

|

| Services to shareholders |

|

|

5,218 |

|

| Reports to shareholders and shareholder meeting expenses |

|

|

28,118 |

|

| Directors’ fees and expenses |

|

|

74,330 |

|

| Legal fees |

|

|

63,927 |

|

| Audit and tax fees |

|

|

26,064 |

|

| NYSE listing fee |

|

|

11,771 |

|

| Insurance |

|

|

9,497 |

|

| Miscellaneous |

|

|

14,197 |

|

| Total expenses before expense reductions |

|

|

477,547 |

|

| Expense reductions |

|

|

(82,047 |

) |

| Total expenses after expense reductions |

|

|

395,500 |

|

| Net investment loss |

|

|

(113,009 |

) |

|

|

| Realized and Unrealized Gain (Loss) |

|

|

|

|

| Net realized gain (loss) from: |

|

|

|

|

|

|

| Investments |

|

|

(2,115,535 |

) |

| Foreign currency |

|

|

4,051 |

|

| Net realized gain (loss) |

|

|

(2,111,484 |

) |

| Change in net unrealized appreciation (depreciation) on: |

|

|

|

|

|

|

| Investments |

|

|

16,182,291 |

|

| Foreign currency |

|

|

27,621 |

|

| Change in net unrealized appreciation (depreciation) |

|

|

16,209,912 |

|

| Net gain (loss) |

|

|

14,098,428 |

|

| Net increase (decrease) in net assets resulting from operations |

|

$ |

13,985,419 |

|

The accompanying notes are an integral part of the

financial statements.

|

|

|

|

|

| 16 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

Statements of Changes in Net Assets

|

|

|

|

|

|

|

|

|

| Increase (Decrease) in Net Assets |

|

Six Months

Ended

April 30, 2023

(Unaudited) |

|

|

Year Ended

October 31, 2022 |

|

|

|

|

|

|

|

|

|

|

| Operations: |

|

|

|

|

|

|

|

|

|

|

|

| Net investment income (loss) |

|

$ |

(113,009 |

) |

|

$ |

1,910,564 |

|

| Net realized gain (loss) |

|

|

(2,111,484 |

) |

|

|

(17,718,276 |

) |

| Change in net unrealized appreciation (depreciation) |

|

|

16,209,912 |

|

|

|

(160,619,446 |

) |

| Net increase (decrease) in net assets resulting from operations |

|

|

13,985,419 |

|

|

|

(176,427,158 |

) |

| Distributions to shareholders |

|

|

(1,484,719 |

) |

|

|

(5,946,582 |

) |

| Fund share transactions: |

|

|

|

|

|

|

|

|

|

|

|

| Net proceeds from reinvestment of distributions |

|

|

735,381 |

|

|

|

809,755 |

|

| Shares repurchased |

|

|

— |

|

|

|

(2,948,076 |

) |

| Net increase (decrease) in net assets from Fund share transactions |

|

|

735,381 |

|

|

|

(2,138,321 |

) |

| Total increase (decrease) in net assets |

|

|

13,236,081 |

|

|

|

(184,512,061 |

) |

| Net assets at beginning of period |

|

|

37,067,905 |

|

|

|

221,579,966 |

|

|

|

|

| Net assets at end of period |

|

$ |

50,303,986 |

|

|

$ |

37,067,905 |

|

|

|

|

| Other Information |

|

|

|

|

|

|

|

|

| Shares outstanding at beginning of period |

|

|

6,220,022 |

|

|

|

6,297,200 |

|

| Shares issued from reinvestment of distributions |

|

|

80,370 |

|

|

|

34,858 |

|

| Shares repurchased |

|

|

— |

|

|

|

(112,036 |

) |

|

|

|

| Shares outstanding at end of period |

|

|

6,300,392 |

|

|

|

6,220,022 |

|

The accompanying notes are an integral part of the

financial statements.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

17 |

|

Financial Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended 4/30/23 |

|

|

Years Ended October 31, |

|

| |

|

(Unaudited) |

|

|

2022 |

|

|

2021 |

|

|

2020 |

|

|

2019 |

|

|

2018 |

|

|

|

|

|

| Per Share Operating Performance |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net asset value, beginning of period |

|

|

|

|

|

|

$5.96 |

|

|

|

$35.19 |

|

|

|

$22.01 |

|

|

|

$31.60 |

|

|

|

$26.98 |

|

|

|

$27.58 |

|

| Income (loss) from investment operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income

(loss)a |

|

|

|

|

|

|

(.02 |

) |

|

|

.31 |

|

|

|

.90 |

|

|

|

1.00 |

d |

|

|

1.32 |

|

|

|

1.01 |

e |

| Net realized and unrealized gain (loss) on investments and foreign currency |

|

|

|

|

|

|

2.26 |

|

|

|

(28.64 |

) |

|

|

13.01 |

|

|

|

(9.21 |

) |

|

|

4.24 |

|

|

|

(1.24 |

) |

| Total from investment operations |

|

|

|

|

|

|

2.24 |

|

|

|

(28.33 |

) |

|

|

13.91 |

|

|

|

(8.21 |

) |

|

|

5.56 |

|

|

|

(.23 |

) |

| Less distributions from: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

|

|

|

|

(.24 |

) |

|

|

(.95 |

) |

|

|

(.92 |

) |

|

|

(1.46 |

) |

|

|

(1.01 |

) |

|

|

(.56 |

) |

| Increase (dilution) in net asset value from dividend reinvestment |

|

|

|

|

|

|

.02 |

|

|

|

(.02 |

) |

|

|

(.02 |

) |

|

|

(.03 |

) |

|

|

(.03 |

) |

|

|

(.01 |

) |

| Increase resulting from share repurchases |

|

|

|

|

|

|

— |

|

|

|

.07 |

|

|

|

.21 |

|

|

|

.11 |

|

|

|

.10 |

|

|

|

.20 |

|

| Net asset value, end of period |

|

|

|

|

|

|

$7.98 |

|

|

|

$5.96 |

|

|

|

$35.19 |

|

|

|

$22.01 |

|

|

|

$31.60 |

|

|

|

$26.98 |

|

| Market value, end of period |

|

|

|

|

|

|

$8.12 |

|

|

|

$7.05 |

|

|

|

$31.32 |

|

|

|

$18.33 |

|

|

|

$27.34 |

|

|

|

$22.96 |

|

|

|

|

| Total Investment Return for the Periodb |

|

|

|

|

|

|

|

|

|

| Based upon market value (%) |

|

|

|

|

|

|

18.18 |

** |

|

|

(76.57 |

) |

|

|

77.46 |

|

|

|

(29.42 |

) |

|

|

23.97 |

|

|

|

(4.49 |

) |

| Based upon net asset valuec (%) |

|

|

|

|

|

|

37.16 |

** |

|

|

(82.33 |

) |

|

|

65.86 |

|

|

|

(26.61 |

) |

|

|

21.90 |

|

|

|

(.18 |

) |

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

| 18 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

|

|

|

| Financial Highlights (continued) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Six Months

Ended 4/30/23 |

|

|

Years Ended October 31, |

|

| |

|

(Unaudited) |

|

|

2022 |

|

|

2021 |

|

|

2020 |

|

|

2019 |

|

|

2018 |

|

|

|

|

|

|

| Ratios to Average Net Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total expenses before expense reductions (%) |

|

|

|

|

|

|

2.16 |

* |

|

|

1.67 |

|

|

|

1.18 |

|

|

|

1.24 |

|

|

|

1.29 |

|

|

|

1.30 |

|

| Total expenses after expense reductions (%) |

|

|

|

|

|

|

1.79 |

* |

|

|

1.51 |

|

|

|

1.18 |

|

|

|

1.24 |

|

|

|

1.29 |

|

|

|

1.30 |

|

| Net investment income (loss) (%) |

|

|

|

|

|

|

(.25 |

)** |

|

|

2.12 |

|

|

|

2.95 |

|

|

|

3.71 |

d |

|

|

4.59 |

|

|

|

3.62 |

e |

| Portfolio turnover (%) |

|

|

|

|

|

|

22 |

** |

|

|

35 |

|

|

|

31 |

|

|

|

43 |

|

|

|

32 |

|

|

|

119 |

|

| Net assets at end of period ($ thousands) |

|

|

|

|

|

|

50,304 |

|

|

|

37,068 |

|

|

|

221,580 |

|

|

|

144,813 |

|

|

|

212,094 |

|

|

|

184,630 |

|

| a |

Based on average shares outstanding during the period. |

| b |

Total investment return based on net asset value reflects changes in the Fund’s net asset value during each period.

Total return based on market value reflects changes in market value during each period. Each figure includes reinvestments of dividend and capital gain distributions, if any. These figures will differ depending upon the level of any discount from or

premium to net asset value at which the Fund’s shares trade during the period. |

| c |

Total return would have been lower had certain expenses not been reduced. |

| d |

Net investment income per share includes $258,629 of non-recurring foreign dividend reclaims and $5,373 of non-recurring

related interest amounting to $0.04 per share. Excluding these non-recurring amounts, the net investment income ratio would have been 3.57%. |

| e |

Net investment income per share includes $981,033 of non-recurring foreign dividend reclaims and $348,133 of non-recurring

related interest amounting to $0.19 per share. Excluding these non-recurring amounts, the net investment income ratio would have been 2.94%. |

The accompanying notes are an integral part of the financial statements.

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

19 |

|

|

|

|

| Notes to Financial Statements |

|

(Unaudited) |

A. Accounting Policies

The Central and

Eastern Europe Fund, Inc. (the “Fund”) is a non-diversified, closed-end management investment company incorporated in Maryland. The Fund commenced investment operations on March 6, 1990.

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) requires

management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates. The Fund qualifies as an investment company under Topic 946 of Accounting

Standards Codification of U.S. GAAP. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements.

Security Valuation. The Fund calculates its net asset

value (“NAV”) per share for publication at the close of regular trading on Deutsche Börse XETRA, normally at 11:30 a.m., New York time.

The

Fund’s Board has designated DWS International GmbH (the “Advisor”) as the valuation designee for the Fund pursuant to Rule 2a-5 under the 1940 Act. The Advisor’s Pricing Committee (the “Pricing Committee”) typically

values securities using readily available market quotations or prices supplied by independent pricing services (which are considered fair values under Rule 2a-5). The Advisor has adopted fair valuation procedures that provide methodologies for fair

valuing securities.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in three broad levels. Level 1

includes quoted prices in active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds and credit risk). Level 3 includes

significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments). The level assigned to the securities valuations may not be an indication of the risk or liquidity associated with investing in

those securities.

Equity securities are valued at the most recent sale price or official closing price reported on the exchange (U.S. or foreign) or over-the-counter market on which they trade prior to the time of valuation. Securities for which no sales are reported are valued at the calculated mean between the most

recent bid and asked quotations on the relevant market or, if a mean cannot be determined, at the most recent bid quotation. Equity securities are generally categorized as Level 1.

|

|

|

|

|

| 20 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

Investments in open-end investment companies are valued and traded at their NAV

each business day and are categorized as Level 1.

Securities and other assets for which market quotations are not readily available or for which the above

valuation procedures are deemed not to reflect fair value are valued in a manner that is intended to reflect their fair value as determined in accordance with procedures approved by the Pricing Committee and are generally categorized as

Level 3. In accordance with the Fund’s valuation procedures, factors considered in determining value may include, but are not limited to, the type of the security; the size of the holding; the initial cost of the security; the existence of

any contractual restrictions on the security’s disposition; the price and extent of public trading in similar securities of the issuer or of comparable companies; quotations or evaluated prices from

broker-dealers and/or the appropriate stock exchange (for exchange-traded securities); an analysis of the company’s or issuer’s financial statements; an

evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold; and, with respect to debt securities, the maturity, coupon, creditworthiness, currency denomination, and the movement of the market in

which the security is normally traded. The value determined under these procedures may differ from published values for the same securities.

Disclosure about the

classification of the fair value measurements is included in a table following the Fund’s Schedule of Investments.

Securities Transactions and Investment Income. Investment transactions are accounted for on a trade date plus one basis for daily NAV

calculation. However, for financial reporting purposes, investment security transactions are reported on trade date. Interest income is recorded on the accrual basis. Dividend income is recorded on the

ex-dividend date net of foreign withholding taxes. Certain dividends from foreign securities may be recorded subsequent to the ex-dividend date as soon as the Fund is

informed of such dividends. Due to the impact of sanctions and other regulations and requirements, dividend income may not be recorded. Realized gains and losses from investment transactions are recorded on an identified cost basis. Proceeds from

litigation payments, if any, are included in net realized gain (loss) for investments.

Securities

Lending. Brown Brothers Harriman & Co., as lending agent, lends securities of the Fund to certain financial institutions under the terms of its securities lending agreement. During

the term of the loans, the Fund continues to receive dividends generated by the securities and to participate in any changes in their market value. The Fund requires the borrowers of the securities to maintain collateral with the Fund consisting of

either cash and/or U.S. Treasury Securities having a value at least equal to the value of the securities loaned. When the collateral falls below

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

21 |

|

specified amounts, the lending agent will use its best effort to obtain additional collateral on the next business day to meet required amounts under the securities lending agreement. As of

period end, any securities on loan were collateralized by cash. During the six months ended April 30, 2023, the Fund invested the cash collateral into a joint trading account in DWS Government & Agency Securities Portfolio, an

affiliated money market fund managed by DWS Investment Management Americas, Inc. DWS Investment Management Americas, Inc. receives a management/administration fee (0.07% annualized effective rate as of April 30, 2023) on the cash collateral

invested in DWS Government & Agency Securities Portfolio. The Fund receives compensation for lending its securities either in the form of fees or by earning interest on invested cash collateral net of borrower rebates and fees paid to a

lending agent. Either the Fund or the borrower may terminate the loan at any time and the borrower, after notice, is required to return borrowed securities within a standard time period. There may be risks of delay and costs in recovery of

securities or even loss of rights in the collateral should the borrower of the securities fail financially. If the Fund is not able to recover securities lent, the Fund may sell the collateral and purchase a replacement investment in the market,

incurring the risk that the value of the replacement security is greater than the value of the collateral. The Fund is also subject to all investment risks associated with the reinvestment of any cash collateral received, including, but not limited

to, interest rate, credit and liquidity risk associated with such investments.

As of April 30, 2023, the Fund had securities on loan which were classified as common

stock in the Schedule of Investments. The value of the related collateral exceeded the value of the securities loaned at period end. As of period end, the remaining contractual maturity of the collateral agreements were overnight and continuous.

Foreign Currency Translation. The books and records

of the Fund are maintained in United States dollars.

Assets and liabilities denominated in foreign currency are translated into United States dollars at the

prevailing exchange rates at period end. Purchases and sales of investment securities, income and expenses are translated at the rate of exchange prevailing on the respective dates of such transactions. Net realized and unrealized gains and losses

on foreign currency transactions represent net gains and losses between trade and settlement dates on securities transactions, the acquisition and disposition of foreign currencies, and the difference between the amount of net investment income

accrued and the U.S. dollar amount actually received. The portion of both realized and unrealized gains and losses on investments that results from fluctuations in foreign currency exchange rates is not separately disclosed but is included with net

realized and unrealized gain/appreciation and loss/depreciation on investments.

|

|

|

|

|

| 22 |

|

| |

|

The Central and Eastern Europe Fund, Inc. |

Contingencies. In the normal course of business, the Fund

may enter into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not

yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

Taxes. The Fund’s policy is to comply with the

requirements of the Internal Revenue Code of 1986, as amended, which are applicable to regulated investment companies, and to distribute all of its taxable income to its shareholders.

Additionally, the Fund may be subject to taxes imposed by the governments of countries in which it invests. Such taxes are generally based on income and/or capital gains

earned or repatriated. Estimated tax liabilities on certain foreign securities are recorded on an accrual basis and are reflected as components of interest income or net change in unrealized gain/loss on investments. Tax liabilities realized as a

result of security sales are reflected as a component of net realized gain/loss on investments.

At October 31, 2022, the Fund had a net tax basis capital loss

carryforward of approximately $67,373,000, which may be applied against realized net taxable capital gains indefinitely, including short-term losses ($17,650,000) and

long-term losses ($49,723,000).

At April 30, 2023, the aggregate cost of investments for federal income tax purposes

was $110,514,376. The net unrealized depreciation for all investments based on tax cost was $60,225,749. This consisted of aggregate gross unrealized appreciation for all investments for which there was an excess of value over tax cost of $9,213,579

and aggregate gross unrealized depreciation for all investments for which there was an excess of tax cost over value of $69,439,328.

The Fund has reviewed the tax

positions for the open tax years as of October 31, 2022 and has determined that no provision for income tax and/or uncertain tax positions is required in the Fund’s financial statements. The Fund’s federal tax returns for the prior

three fiscal years remain open subject to examinations by the Internal Revenue Service.

Dividends and

Distributions to Shareholders. The Fund records dividends and distributions to its shareholders on the ex-dividend date. The timing and character of

certain income and capital gain distributions are determined annually in accordance with United States federal income tax regulations, which may differ from accounting principles generally accepted in the United States of America. These differences

primarily relate to certain securities sold at a loss. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for a reporting period may differ significantly from distributions during such

|

|

|

|

|

|

|

| The Central and Eastern Europe Fund, Inc. |

|

| |

|

|

23 |

|

period. Accordingly, the Fund may periodically make reclassifications among certain of its capital accounts without impacting the NAV of the Fund.

The tax character of current year distributions will be determined at the end of the current fiscal year.

B. Investment Advisory and Administration Agreements

The Fund is party to

an Investment Advisory Agreement with DWS International GmbH (“DWSI”). The Fund also has an Administration Agreement with DWS Investment Management Americas, Inc. (“DIMA”). DWSI and DIMA are affiliated companies.

Under the Investment Advisory Agreement with DWSI, DWSI directs the investments of the Fund in accordance with its investment objectives, policies and restrictions. DWSI

determines the securities, instruments and other contracts relating to investments to be purchased, sold or entered into by the Fund.

The Investment Advisory