| Copyright © 2023 First Foundation Inc. All Rights Reserved

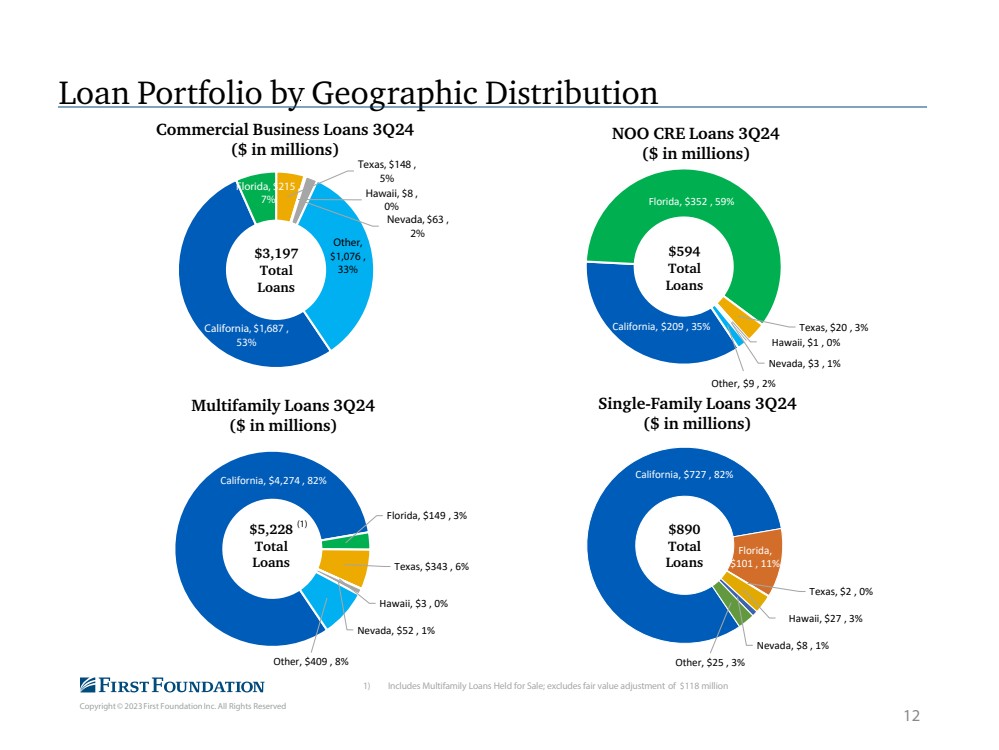

California, $727 , 82%

Florida,

$101 , 11%

Texas, $2 , 0%

Hawaii, $27 , 3%

Nevada, $8 , 1%

Other, $25 , 3%

Single-Family Loans 3Q24

($ in millions)

California, $4,274 , 82%

Florida, $149 , 3%

Texas, $343 , 6%

Hawaii, $3 , 0%

Nevada, $52 , 1%

Other, $409 , 8%

Multifamily Loans 3Q24

($ in millions)

California, $209 , 35%

Florida, $352 , 59%

Texas, $20 , 3%

Hawaii, $1 , 0%

Nevada, $3 , 1%

Other, $9 , 2%

NOO CRE Loans 3Q24

($ in millions)

California, $1,687 ,

53%

Florida, $215 ,

7%

Texas, $148 ,

5%

Hawaii, $8 ,

0%

Nevada, $63 ,

2%

Other,

$1,076 ,

33%

Commercial Business Loans 3Q24

($ in millions)

Loan Portfolio by Geographic Distribution

$5,228

Total

Loans

12

$594

Total

Loans

$890

Total

Loans

$3,197

Total

Loans

1) Includes Multifamily Loans Held for Sale; excludes fair value adjustment of $118 million

(1) |