BRISBANE, Australia, July

19, 2017 /CNW/ --

JUNE QUARTER 2017 KEY POINTS1

OLAROZ LITHIUM FACILITY (ORE 66.5%)2

- Production of 2,536 tonnes of lithium carbonate for June

Quarter 2017

- FY17 production of 11,862 tonnes of lithium carbonate, up 72%

year on year (YoY)

- Sales revenue of US$27.4 million

on total sales of 2,566 tonnes for June Quarter

- FY17 sales revenue totalling US$120

million

- Average FOB price received up 5% quarter on quarter (QoQ) to

US$10,696/tonne FOB with higher

priced contracts reflecting firmer market conditions

- Cash cost of sales of US$4,279/tonne, up 20% QoQ with lower production

volumes and lower brine concentrations

- Gross cash margins remain steady at US$6,417/tonne maintaining a high margin of

60%

- VAT refunds of approximately US$10.8

million received in the quarter with total VAT refunds

received to date of approximately US$23.5

million

- Production in 1H FY18 is expected to increase significantly

compared to 2H FY17 and will be skewed to the December quarter with

increased evaporation rates through Spring and early Summer. Formal

production guidance will be given in August

2017

- Pricing is expected to exceed US$10,000 per tonne FOB in the September 2017 quarter

- Test work successfully completed with two specialized

engineering firms to finalise the process engineering for a 10,000

tonne per annum battery grade lithium hydroxide plant. Capital cost

and operating estimates will be received from both contractors

during the September quarter 2017

- Sales de Jujuy ("SDJ") successful in arranging with it local

bankers an export credit facility capped at US$25 million. This has facilitated the release

of additional SBLCs

BORAX ARGENTINA

- Sales volume in the June quarter was up 18% on the March

quarter 2017 to 11,398 tonnes

- Lower sales prices, inflation and severe weather conditions

impacted financial performance

- Tincalayu Expansion Project on schedule for completion in the

September quarter

ADVANTAGE LITHIUM AND CAUCHARI

- Advantage Lithium (ORE 35%) commenced a 17 hole drilling

program at Cauchari with the aim of providing an updated resource

estimate by the end of 2017

CORPORATE

- As at 30 June 2017, Orocobre

Group had available cash of US$51.5

million, up from US$30.6

million at 31 March 2017. This

follows the release of Standby Letters of Credit (SBLCs) of

US$21.2 million (ORE's share) back to

the Company during the quarter

- Orocobre completed the sale of exploration tenure at Salinas

Grandes to LSC Lithium Limited (TSXV: LSC) and received

US$4 million. A further US$3 million will be paid in three annual

tranches

- Inflation during FY17 has been 11% higher than the

corresponding devaluation of the ARS peso against the USD which has

resulted in higher costs at Borax Argentina SA and to a lesser

extent SDJ

OLAROZ LITHIUM FACILITY

For more information on Olaroz please click here

The Olaroz Lithium Facility is located in the Jujuy province of

Argentina. Together with partners,

Toyota Tsusho Corporation (TTC) and Jujuy Energia y Mineria

Sociedad del Estado (JEMSE), Orocobre is now operating the

first large scale lithium brine plant to be commissioned in

approximately 20 years.

The Olaroz Lithium Facility joint venture is operated through

Argentine subsidiary SDJ. The effective equity interests are:

Orocobre 66.5%, TTC 25.0% and JEMSE 8.5%.

PRODUCTION, SALES AND OPERATIONAL UPDATE

PRODUCTION AND SALES

Production for the quarter was 2,536 tonnes. Operations

were impacted by weather conditions slowing pond evaporation

rates and preventing delivery of a soda ash, a key reagent in the

production process, which resulted in the cessation of operations

for three days.

For FY17, total production is up 72% on FY16 to 11,862

tonnes.

Sales revenue for the quarter was US$27.4

million on total sales of 2,566 tonnes with average sales

prices up 5% to US$10,696/tonne3. The cash cost

of sales was US$4,279/tonne, up 20%

QoQ due to lower production levels and higher soda ash consumption

from lower brine concentrations. Costs are expected to decrease as

brine concentration and production increases with accelerating

evaporation rates through Spring and Summer.

Gross cash margins for the quarter remained strong at

US$6,417/tonne with the increase in

sales prices offsetting the increase in costs. Overall gross

operating margins remain strong at 60%.

SDJ remains strongly operating cashflow positive.

|

Metric

|

June

quarter 2017

|

March

quarter 2017

|

Change QoQ

(%)

|

|

Production

(tonnes)

|

2536

|

2784

|

-9%

|

|

Sales

(tonnes)

|

2566

|

3142

|

-18%

|

|

Average price

received (US$/tonne)

|

10696

|

10211

|

5%

|

|

Cost of sales

(US$/tonne)4

|

4279

|

3565

|

20%

|

|

Revenue

(US$M)

|

27.4

|

32.1

|

-14%

|

|

Gross cash margin

(US$/tonne)

|

6417

|

6646

|

-3%

|

|

Gross cash margin

(%)

|

60%

|

65%

|

-8%

|

OPERATIONAL UPDATE

Operations during the quarter continued to focus on pond

management both from the perspective of inter-pond brine transfer

and operational controls and monitoring. During the quarter,

the design for the improved pumping system was finalised resulting

in the program being increased to six pumps, remote monitoring

systems and additional water cleaning lines to the pumps for a

revised capital cost of US$2.7m. This program will be undertaken in

two stages with the most important stage being completed by October

when evaporation rates increase in conjunction with the need to

increase inter-pond brine transfers. At a day to day

operational level additional management positions have been

established including Pond Operations Superintendent and Process

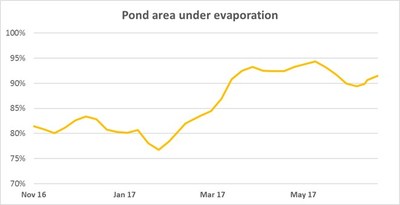

Manager. An indicator of improved pond management is the

increase in area under evaporation which maximises evaporation

efficiency. As can be seen in the chart below, the pond area under

evaporation has been maintained in excess of 90% since the initial

review in February 2017.

As previously advised at the half year results, the process of

re-establishing the correct inventory profile (volume and

concentration) would take approximately six months and is expected

to be completed in August. The six month duration is due to the

pond system having significant inertia and the process occurring

during the low evaporation time of the year.

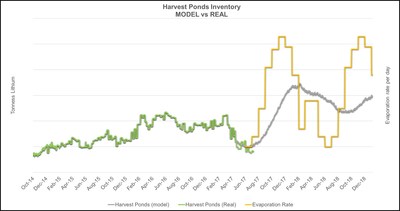

The chart below shows the seasonality of average evaporation

rates and the historical and forecast harvest pond inventory

profile. The inventory profile reaches the minimum level in

July prior to a rapid increase through September to December driven

by the corresponding increase in evaporation rates and movement of

inventory from earlier ponds. The actual pond profile deviates

slightly from that predicted due to the recent cloudy and snowy

weather conditions previously reported. It can also be seen that

the level of deviation of harvest pond inventory is relatively

insignificant compared to the increase that is modelled to occur

throughout the rest of the calendar year. The relative

performance is similar in primary and intermediate ponds and the

Company is encouraged that the measured data overall is correlating

well with predicted performance from the pond evaporation and

production model.

One of the key findings in the review of pond operating

practices has been that production reliability and resistance to

adverse weather conditions will be improved through maintaining a

higher level of inventory in the harvest ponds. As such, the

future lowest point of inventory will be significantly higher than

that experienced this past year and result in higher concentrations

to the plant throughout the cycle.

To enable production modelling and forecasting Orocobre

commenced a process of bathymetric surveys in April 2017.

However, strong winds severely slowed the process as flat surface

conditions are needed for the surveys. The work has been suspended

until October when wind conditions are normally more

favourable. To provide an alternative source of data the

focus has changed to more direct measurement and surveys of drained

areas. This work has highlighted that some further testing of

salt density is required prior to finalising the production model

and issuing formal production guidance which is now expected in

August 2017.

Prior to the pond issue, the purification circuit has achieved a

maximum throughput rate of 43 tonnes per day (tpd) and runs

consistently at 35-40 tpd (73-83% of nameplate). Recently

fitted hydrocyclones are expected to allow the purification circuit

to achieve nameplate capacity of approximately 48 tonnes per

day.

The primary circuit runs consistently above nameplate capacity

with a maximum achieved throughput of 66 tpd some 35% above design

rate of 48 tpd.

BRINE INVENTORY

At the end of the June quarter 2017, brine inventory was

approximately 38,300 tonnes of lithium carbonate equivalent.

MARKET AND SALES

Total volume of lithium carbonate sold in the June quarter

amounted to 2,566 tonnes. Lithium carbonate prices increased

5% to US$10,696/tonne (FOB) for the

quarter. The price achieved for the quarter is a result of higher

pricing in short term contracts compared to last quarter.

LITHIUM MARKET

Contract prices for lithium carbonate remain above US$10,000/t after doubling in 2016. Market growth

rates have lifted from 10% p.a. to over 12% p.a. and are expected

to reach over 15% by 2020. The key driver for demand growth

has also shifted – the adoption of lithium-ion battery in personal

electronics such as laptops, tablets and phones which drove the

first demand surge has reached the mature phase of the product life

cycle (in developed economies at least). However, a more

significant growth catalyst in terms of potential lithium

consumption has emerged, being world-wide adoption of electric

vehicles (EV's) encouraged by government incentives and

infrastructure, falling costs of battery packs, improved

performance of rechargeable batteries and a greater range of EV

models to suit end-consumer needs.

In 2016 EV penetration was approaching 1% worldwide.

Several European countries however were ahead of the adoption curve

including Norway and the Netherlands having achieved EV shares of

25% and 10% respectively due to early introduction of government

incentives beginning in 1996 ("Global EV Outlook 2016",

OECD/International Energy Agency). Twenty years later

countries with much higher car ownership and fleet numbers have

begun to implement similar incentives and develop charging

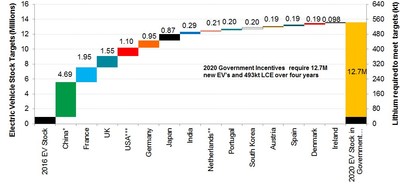

infrastructure. As of 2016 14 countries participating in EV

incentive programs had announced targets that would require 12.7

million new EVs between 2016 and 2020 and approximately 493,000

tonnes of lithium carbonate equivalent (LCE).

The rechargeable battery manufacturing industry has signalled a

confidence in the industry with worldwide manufacturing capacity

set to quadruple from ~75 GWh currently to over 305 GWh by 2020

(Benchmark Minerals). The vast majority of large scale car

manufacturers currently have, or will soon release, an EV model

encouraged by growing consumer demand, government manufacturer

incentives and decreasing li-ion battery pack costs, which have

fallen from US$600/kwh in 2012 to

~US$150/kwh just five years later

(Lux Research, 2016). Installed battery manufacturing

capacity was estimated to be operating above 90% utilisation in

2016 (Roskill, 2017) therefore additional battery capacity is

required to ensure continued EV growth at or above the current rate

of 40% p.a.

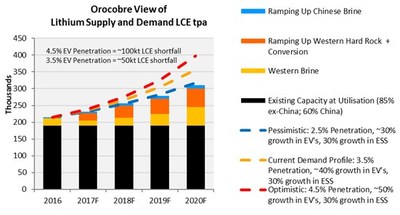

While there is much divergence between forecasts of EV

penetration rates the general consensus is growth rates will reach

at least 45% by 2020 resulting in EV penetration of approximately

4.5%. Similarly, forecast lithium demand from the energy

storage systems (ESS) segment varies widely as growth of between

20% to 25% p.a. has been recorded in the past three years

(Roskill). It is Orocobre's view that ESS development

will continue and exceed 30% p.a. growth by 2020 as renewable energy targets are more likely to

be achieved when renewable energy sources are combined with ESS as

exemplified by the South Australian government's plan to install a

100gWh battery factory. EV and ESS together with healthy

baseload demand in line with GDP growth, will require at least

350ktpa of LCE production by 2020.

These robust demand dynamics have compounded concern regarding a

significant lithium carbonate supply shortage given the current

market tightness. Slower than expected project ramp ups have

moderated supply expectations as the industry has become aware of

the challenges involved in ramping up lithium projects given scarce

industry experience and highly technical 'bespoke' operations with

unique and sometimes unpredictable challenges. As the risks

involved in raw material operations, processing, supply security

and financing become more apparent, strategic partnerships have

become a necessity. Vertical integration and/or strong partnerships

are particularly important for hard rock operations given the

additional capital required for spodumene mining, processing and

conversion as well as the broad technical skills required to

produce lithium carbonate or hydroxide.

The recent funding arrangements of hard rock projects

demonstrates that funding of new lithium production remains

challenging, high cost and an impediment to new production.

Given growth is not expected to slow in the foreseeable future

vertical integration is likely to continue. There is

significant potential for greater involvement and investment in

lithium projects from downstream participants including battery and

EV manufacturers, however widespread understanding of capital

intensity, project ramp-up challenges and supply chain lead times

(from lithium production to consumption in end-use segments) is

required to encourage the necessary

investment.

LITHIUM HYDROXIDE PLANT

UPDATE ON PROGRESS

Olaroz industrial grade lithium carbonate and locally sourced

Japanese lime have been used as feedstock for testing of process

design to produce lithium hydroxide by two specialised engineering

firms. The test work demonstrated that a very high quality lithium

hydroxide could be produced from Olaroz lithium carbonate using a

customised process. The test work has also highlighted

opportunities to reduce lithium losses during conversion from

carbonate to hydroxide.

Lithium hydroxide currently sells at a significant premium

compared to lithium carbonate.

Contract negotiations are continuing with the two firms to

determine the preferred contractor. The selection criteria

for choice of engineering contractor includes turn-key

commissioning and personnel training with process, product quality

and performance guarantees.

Capital and operating costs for the lithium hydroxide plant in

Japan will be advised by the

engineering firms during the September quarter.

Subject to joint venture approvals and finalisation of financing

and permitting, construction could commence in November 2017 with commissioning 12 months later.

Orocobre does not anticipate the need to raise equity capital for

this project.

EXPANSION STUDY FOR OLAROZ

The Phase 2 expansion investment decision remains dependent on

achieving Phase 1 design production rates and the expansion being

funded without further equity capital (i.e. funded by project

finance and Phase 1 operating cashflow).

REVISED SCOPE OF PHASE 2 EXPANSION STUDIES

On 15 December 2016, Orocobre

announced the results of scoping studies into the expansion of

Olaroz and the proposed doubling of production at a cost of

US$190 million including US$25 million contingency. Subsequently,

these plans have been simplified to remove the purification circuit

from the incremental production. The resultant product mix is

17,500 tonne per annum Battery Grade lithium carbonate (>99.5%)

from the existing purification circuit and 17,500 tonne per annum

Industrial Grade lithium carbonate (avg. 99.0%) which will provide

feedstock for the planned lithium hydroxide plant in Japan.

This simplified strategy results in lower capital expenditure of

approximately US$160 million

including a US$25 million contingency

and lower implementation risk as the project is based around a

simple duplication of bores, ponds and primary circuit of Phase 1

at Olaroz. The full cost of the pond system contained within the

total capital expenditure estimate for Phase 2 is

US$75 million.

GHD has been appointed to oversee engineering design studies for

the Olaroz Phase 2 expansion. Arrangements were terminated

with Ausenco after they withdrew services from South America following a corporate

restructure. No significant delays are expected with this

change however progress against schedule is being actively

monitored.

The process to obtain necessary permits and approvals for Phase

2 continues to run concurrently with engineering, design and

selection of mechanical equipment such as centrifuges, filters and

reactors. Test work is continuing to allow further

optimisation of design and process beyond that already identified

from commissioning and operation of Phase 1.

The expansion studies are not managed by the SDJ operating team

but by consultants and a dedicated ORE study manager.

BORAX ARGENTINA

The focus in FY17 for Borax Argentina has been to increase

production rates and reduce unit costs at operations following

optimisation projects at Tincalayu and Campo Quijano, whilst building suitable

inventory levels. In sales and logistics, the focus has been

on developing new customers whilst improving response times and

delivery performance and thereby reinforcing Borax's value

proposition as the producer integral to a customer's security of

supply strategy.

OPERATIONS

Sales volumes in the June quarter 2017 were up 18% on the March

quarter to 11,398 tonnes of combined product. There were no tonnes

of tincal ore sold this quarter.

Operating conditions have been challenging during the last

quarter due to severe weather that saw heavy snowfall.

At Tincalayu, snow and freezing weather significantly affected

mining and the transport of water resulting in processing

operations being suspended for a cumulative 10 day period and the

loss of approximately 700 tonnes of decahydrate equivalent

production. Wet ore caused by the snow continued to impact on

production rate through to the end of the quarter. The Sijes

operations were less affected with approximately 200 tonnes of lost

concentrate production and delays in the export of

product.

COMBINED PRODUCT SALES VOLUME BY QUARTER

|

Previous Year

Quarters

|

Recent

Quarters

|

|

September

2015

|

8,124

|

September

2016

|

11,940

|

|

December

2015

|

10,078

|

December

2016

|

8,767

|

|

March 2016

|

8,006

|

March 2017

|

9,672

|

|

June 2016

|

9,274

|

June 2017

|

11,398

|

TINCALAYU EXPANSION STUDY

A study commenced in Q2 CY16 to evaluate a potential expansion

of the Tincalayu refined borates operation from its current

production capacity of 30,000 to 100-120,000 tonnes per annum and

an integrated 40,000 tonne boric acid plant.

It is anticipated that the potential expansion will further

enhance efficiencies in the production of refined borates at

Tincalayu and contribute to improved manufacturing unit costs.

Approvals have been received for a new gas pipeline to supply the

expanded plant and initial cost estimates are under review.

The feasibility study will be completed during the September

quarter.

MARKET CONDITIONS

Market conditions remain difficult in the core South American

markets of Argentina and

Brazil. Borax Argentina continues to grow strong long term

relationships with key customers while expanding the customer base.

The continued focus on production efficiencies is required to

cushion the effect of market pricing remaining at the bottom of the

price cycle.

Prices of all borate products remain under pressure, in

particular boric acid pricing continues to decline.

In addition to price pressure the operations are seeing

inflation of costs which is exceeding devaluation of the Peso. FY17

has seen inflation of 21.8% while the Peso has only devalued by

10.8%.

The combination of low prices, inflationary costs and difficult

operating conditions have resulted in a disappointing financial

performance at Borax Argentina SA.

SAFETY AND COMMUNITY

SAFETY MILESTONE

The Olaroz site has recently achieved a significant milestone of

220 days of operation without a lost time injury.

At Borax, a new safety management system SICOP was installed

during the quarter which is expected to streamline access and

awareness of safety documentation. First aid training for staff was

conducted during the quarter.

An inspection by local Environmental Authorities noted that the

Tincalayu and Sijes sites were exemplary in waste management and

that Borax Argentina was one of the top four companies for

compliance with waste management regulations throughout the Salta

region.

SHARED VALUE PROGRAM

Sales de Jujuy received recognition from a forum hosted by Banco

Interamericano de Desarrollo (BID) for our Shared Value program.

Demetrio Nieva from the Olaroz Chico

community travelled to Buenos

Aires to share his community's experiences. Orocobre

was represented by Silvia Rodriguez

our Shared Value Manager.

BID is the main source of financing for development in

Latin America and has areas of

focus that include three development challenges - social inclusion

and equity, productivity and innovation and economic

integration.

ISO RE-CERTIFICATION

At Olaroz, audits have been completed for the Maintenance of

Certification (ISO 9000 Quality Standard) and Re-certification of

the Environmental Standard (ISO 14000). This follows the

audit in the March quarter of all Borax sites: Campo Quijano, Tincalayu, Sijes and

Porvenir.

ADVANTAGE LITHIUM

As previously announced, Orocobre completed the sale of a suite

of exploration assets to Advantage Lithium Corp (TSV: AAL) in the

March 2017 quarter. AAL is well

funded having raised C$20,000,000

capital in February 2017. Orocobre

holds 46,325,000 (35%) of the issued shares of AAL and 2,550,000

warrants exercisable at C$1.

Orocobre retains a 50% interest in the Cauchari Project and AAL

has the right to increase its interest to a total of 75% by the

expenditure of US$5,000,000 or

production of a Feasibility Study. AAL also took a 100% interest in

five other lithium properties that were previously held by Orocobre

totalling 85,543 hectares.

The AAL technical team is led by Callum

Grant. Callum is an engineer with broad experience from

exploration to production focusing on South America and in particular, Argentina.

The flagship Cauchari Property has an existing inferred resource

of 470,000 tonnes of Lithium Carbonate Equivalent and a large

exploration target to be tested with a 17 hole drill program.

Drilling commenced in May 2017 with

the successful casing of Hole CAU07, the first of the five-hole

Phase One program located in the North-West block of the Cauchari

property. Down-the-hole geophysical response in CAU07R

suggests brine conditions begin at a depth of 60-70m. Sampling and

testing of the fluid in the hole will be conducted once the drill

rig returns to CAU07R and at that time information will be

available on the chemical composition of the fluid5.

The drill program is on budget and initial sampling results are

expected to be available in July along with geophysical profiling

which will provide key information on target zones through the salt

lake sedimentary sequence.

The objective of work at Cauchari is to rapidly advance the

property through exploration and towards development by

2018/2019. A diamond drill program to complement the rotary

program will be conducted over the December half year. The overall

objective for 2017 remains an updated resource estimate combining

both NW and SE blocks of Cauchari moving into a Scoping Study in

early 2018. More advanced technical and engineering studies will

continue through 2018 and into 2019 leading to a Bankable

Feasibility Study with the required environmental permits for the

development phase.

CORPORATE AND ADMINISTRATION

SALINAS GRANDES

During the quarter Orocobre completed an agreement for the sale

of exploration tenure at Salinas Grandes to LSC Lithium Limited

(TSXV: LSC).

Pursuant to the Orocobre-LSC Agreement, LSC acquired mining

properties located at Salinas Grandes in Salta and Jujuy provinces,

Argentina ("Salinas Grandes

Tenements"), which were held by Orocobre.

As consideration for the sale of the Salinas Grandes Tenements,

LSC:

- Paid Orocobre US$4 million;

- Transferred to Orocobre three properties located at Olaroz

("Olaroz Tenements") adjacent to current project properties

covering approximately 3,821 hectares thus strengthening Orocobre's

position at its flagship project; and

- Granted Orocobre a 2% royalty on the brine concentrate produced

from Salinas Grandes Tenements, calculated on the same basis as the

royalties paid by Sales de Jujuy at the Olaroz Lithium Facility to

the Jujuy Provincial Government.

LSC will pay a further US$3

million payable by way of three annual tranches of

US$1 million in June 2018, June

2019 and June 2020.

FINANCE

VAT

VAT refunds of approximately US$10.8

million have been received by SDJ during the quarter with

approximately US$23.5 million of VAT

refunds received to date.

Total remaining VAT refund entitlement amounts to US$20 million on an undiscounted basis. The

VAT balance outstanding takes into account the monthly debits and

credits and does not relate solely to construction VAT.

Post the end of the quarter, April's VAT presentation of

~US$1.2M was approved and such funds

are expected to be received in the coming weeks.

CASH BALANCE, DEBT POSITION AND STANDBY LETTERS OF

CREDIT

As at 30 June 2017, Orocobre Group

had available cash of US$51.5 million

following guarantee (SBLC) releases of approximately US$21.2 million (ORE's share) during the quarter

and payment received from the LSC transaction of US$4 million. During the quarter,

US$1.9 million was provided to Borax

Argentina due to the significant impact on production caused by

adverse weather conditions (as previously reported), low prices,

poor credit conditions and operating costs impacted by inflation

(see comments below).

At 30 June 2017, Orocobre had net

debt of US$65.3 million as detailed

below:

|

Loan

(US$M)

|

Lender

|

ORE

share

|

Facility

size

|

30 June 2017

balance

|

ORE share of

external debt

|

|

|

|

100%

|

(100% SDJ

SA)

|

(30 June

2017)

|

|

SDJ

|

|

Project level –

SDJ

|

Mizuho

Bank

|

66.50%

|

191.9

|

155.0

|

103.1

|

|

Working

Capital

|

HSBC

Argentina

|

72.68%

|

40.0

|

15.2

|

9.8

|

|

and Macro bank

Argentina

|

8.6

|

0.0

|

0.0

|

|

HSBC

Pre-Export

|

66.50%

|

25.0

|

22.0

|

14.6

|

|

Shareholders

loans

|

ORE / TTC

|

Internal

(75%)

|

54.7

|

54.7

|

0.0

|

|

Shareholders

loans

|

ORE

|

Internal

(100%)

|

18.0

|

18.0

|

0.0

|

|

|

|

|

|

|

Shareholders

loans

|

SDJ PTE

|

Internal

(72.68%)

|

1.0

|

1.0

|

0.0

|

|

Total

SDJ

|

|

|

339.2

|

265.9

|

127.5

|

|

|

|

|

|

|

|

Borax

|

|

|

|

|

|

|

Productive

loan

|

HSBC

Argentina

|

|

4.8

|

0.9

|

0.9

|

|

Pre-export

|

HSBC

Argentina

|

|

0.5

|

0.5

|

0.5

|

|

Working capital

facilities

|

Macro and

Patagonia

|

|

0.5

|

0.5

|

0.5

|

|

Total

Debt

|

|

|

344.9

|

267.7

|

129.3

|

|

Cash –

SDJ

|

|

66.50%

|

|

-4.0

|

-2.7

|

|

Cash – Orocobre

Group

|

|

|

|

-51.5

|

-51.5

|

|

Financial

Assets

|

|

|

|

-9.8

|

-9.8

|

|

(cash backing of

Working Capital facility

through SBLC's and guarantees)

|

|

|

|

|

Net Debt to

Orocobre

|

|

|

|

|

65.3

|

SDJ will make a further payment to Mizuho Bank in September

2017 of approximately US$14

million.

SDJ put in place a US$25 million

pre-export finance facility in the June quarter which allowed the

release of further SBLCs back to shareholders (ORE and Toyota

Tsusho Corporation). SDJ's working capital facilities were reduced

to US$37.2 million at 30 June of

which US$15.2 million is guaranteed

by SBLCs and the balance being the pre-export finance facility of

US$22 million.

INFLATION VERSUS DEVALUATION

The AR$/US$ exchange rate weakened by 8% during the quarter from

AR$15.39/US$ at 31 March 2017 to AR$16.63/US$ at 30 June 2017 whilst inflation for the same period

was 5.3%. For the financial year devaluation of the ARS$ against

the US$ was 10.8% versus inflation of 21.8%. This resulted in 11%

higher than expected US$ costs for ARS peso denominated expenses at

both SDJ and Borax Argentina SA.

The effect of inflation and devaluation over time generally

shows that they cancel each other out. When looking at specific

periods such as the financial year that has just passed, inflation

was 11% higher than devaluation, resulting in higher costs at both

Borax Argentina and to a much lesser extent SDJ.

FOR FURTHER INFORMATION PLEASE CONTACT:

Andrew Barber

Investor Relations Manager

Orocobre Limited

T: +61 7 3871 3985

M:+61 418 783 701

E:

abarber@orocobre.com

ABOUT OROCOBRE LIMITED

Orocobre Limited is listed on the Australian Securities Exchange

and Toronto Stock Exchange (ASX: ORE) (TSX: ORL), and is building a

substantial Argentinian-based industrial chemicals and minerals

company through the construction and operation of its portfolio of

lithium, potash and boron projects and facilities in the Puna

region of northern Argentina. The

Company has built, in partnership with Toyota Tsusho Corporation

and JEMSE, the first large-scale, greenfield brine based lithium

project in approximately 20 years at the Salar de Olaroz with

planned production of 17,500 tonnes per annum of low-cost lithium

carbonate.

The Olaroz Lithium Facility has a low environmental footprint

because of the following aspects of the process:

- The process is designed to have a high processing recovery of

lithium. With its low unit costs, the process will result in low

cut-off grades, which will maximise resource recovery.

- The process route is designed with a zero liquid discharge

design. All waste products are stored in permanent impoundments

(the lined evaporation ponds). At the end of the project life the

ponds will be capped and returned to a similar profile following

soil placement and planting of original vegetation types.

- Brine is extracted from wells with minimum impact on freshwater

resources outside the salar. Because the lithium is in sedimentary

aquifers with relatively low permeability, drawdowns are limited to

the salar itself. This is different from halite hosted deposits

such as Salar de Atacama, Salar de

Hombre Muerto and Salar de Rincon

where the halite bodies have very high near surface permeability

and the drawdown cones can impact on water resources around the

Salar affecting the local environment.

- Energy used to concentrate the lithium in the brine is solar

energy. The carbon footprint is lower than other processes.

- The technology developed has a very low maximum fresh water

consumption of <20 l/s, which is low by industry standards. This

fresh water is produced by reverse osmosis from non-potable

brackish water.

- Sales de Jujuy S.A. is also committed to the ten principles of

the sustainable development framework as developed by The

International Council on Mining and Metals. The company has an

active and well-funded "Shared Value" program aimed at the long

term development of the local people.

The Company continues to follow the community and shared value

policy to successfully work with suppliers and the employment

bureau to focus on the hiring of local people from the communities

of Olaroz, Huancar, Puesto Sey, Pastos Chicos, Catua, Susques,

Jama, El Toro, Coranzulí, San Juan and Abrapampa. The project

implementation is through EPCM (Engineering, Procurement and

Construction Management) with a high proportion of local

involvement through construction and supply contracts and local

employment. The community and shared value policy continues to be a

key success factor, training local people under the supervision of

high quality experienced professionals.

TECHNICAL INFORMATION, COMPETENT PERSONS' AND QUALIFIED

PERSONS STATEMENTS

The Company is not in possession of any new information or data

relating to historical estimates that materially impacts on the

reliability of the estimates or the Company's ability to verify the

historical estimates as mineral resources, in accordance with the

JORC Code. The supporting information provided in the initial

market announcement on 21/08/12

continues to apply and has not materially changed. Additional

information relating to the Company's Olaroz Lithium Facility is

available on the Company's website in "Technical Report – Salar de

Olaroz Lithium-Potash Project, Argentina" dated May 113, 2011 which was

prepared by John Houston, Consulting

Hydrogeologist, together with Mike

Gunn, Consulting Processing Engineer, in accordance with NI

43-101.

CAUTION REGARDING FORWARD-LOOKING INFORMATION

This news release contains "forward-looking information" within

the meaning of applicable securities legislation. Forward-looking

information contained in this release may include, but is not

limited to, the completion of commissioning, the commencement of

commercial production and ramp up of the Olaroz Lithium Facility

and the timing thereof, the cost of construction relative to the

estimated capital cost of the Olaroz Lithium Facility, the meeting

of banking covenants contained in project finance documentation,

the design production rate for lithium carbonate at the Olaroz

Lithium Facility, the expected brine cost and grade at the Olaroz

Lithium Facility, the expected operating costs at the Olaroz

Lithium Facility and the comparison of such expected costs to

expected global operating costs, the estimation and conversion of

exploration targets to resources at the Olaroz Lithium Facility,

the viability, recoverability and processing of such resources, the

potential for an expansion at the Olaroz Lithium Facility and the

outcome of studies currently being undertaken into the proposed

expansion at Olaroz and elsewhere, the capital cost of an expansion

at the Olaroz Lithium Facility; the future performance of the

relocated borax plant and boric acid plant, including without

limitation the plants estimated production rates, financial data,

the estimates of mineral resources or mineralisation grade at Borax

Argentina mines, the economic viability of such mineral resources

or mineralisation, mine life and operating costs at Borax Argentina

mines, the projected production rates associated with the borax

plant and boric acid plant, the market price of borate products

whether stated or implied, demand for borate products and other

information and trends relating to the borate market, taxes

including recoveries of IVA, royalty and duty rate and the ongoing

working relationship between Orocobre and the Province of Jujuy,

TTC and Mizuho Bank.

Such forward-looking information is subject to known and unknown

risks, uncertainties and other factors that may cause actual

results to be materially different from those expressed or implied

by such forward-looking information, including but not limited to

the risk of further changes in government regulations, policies or

legislation; the possibility that required concessions may not be

obtained, or may be obtained only on terms and conditions that are

materially worse than anticipated; that further funding may be

required, but unavailable, for the ongoing development of the

Company's projects; changes in the scope and focus of studies

currently being undertaken with respect to the expansion of the

Company's production facilities, fluctuations or decreases in

commodity prices and market demand for product; uncertainty in the

estimation, economic viability, recoverability and processing of

mineral resources; risks associated with weather patterns and

impact on production rate; risks associated with commissioning and

ramp up of the Olaroz Lithium Facility to full capacity; unexpected

capital or operating cost increases; uncertainty of meeting

anticipated program milestones at the Olaroz Lithium Facility;

general risks associated with the further development of the Olaroz

Lithium Facility; general risks associated with the operation of

the borax plant or boric acid plant; the potential for an expansion

at the Tincalayu operations and the outcome of studies currently

being undertaken into the proposed expansion at Tincalayu a

decrease in the price for borates resulting from, among other

things, decreased demand or an increased supply of borates or

substitutes, as well as those factors disclosed in the Company's

Annual Report for the year ended June 30,

2016 filed at www.sedar.com.

The Company believes that the assumptions and expectations

reflected in such forward-looking information are reasonable.

Assumptions have been made regarding, among other things: the

timely receipt of required approvals and completion of agreements

on reasonable terms and conditions; the ability of the Company to

obtain financing as and when required and on reasonable terms and

conditions; the prices of lithium, potash and borates; market

demand for products and the ability of the Company to operate in a

safe, efficient and effective manner. Readers are cautioned that

the foregoing list is not exhaustive of all factors and assumptions

which may have been used. There can be no assurance that

forward-looking information will prove to be accurate, as actual

results and future events could differ materially from those

anticipated in such information. Accordingly, readers should not

place undue reliance on forward-looking information. The Company

does not undertake to update any forward-looking information,

except in accordance with applicable securities laws.

1 All figures presented in this report are

unaudited

2 All figures 100% Olaroz Project basis

3 Note: Orocobre reports price as "FOB" (Free On Board)

which excludes additional insurance and freight charges included in

"CIF" (Cost, Insurance and Freight or delivered to destination

port) pricing. The key difference between an FOB and CIF

agreement is the point at which responsibility and liability

transfer from seller to buyer. With a FOB shipment, this typically

occurs when the goods pass the ship's rail at the export port. With

a CIF agreement, the seller pays costs and assumes liability until

the goods reach the port of destination chosen by the buyer.

The Company's pricing is also net of TTC commissions.

The intention in reporting FOB prices is to provide clarity on the

sales revenue that flows back to SDJ, the joint venture company in

Argentina.

4 Excludes royalties and head office costs

5 The reader is cautioned that the interpretation of

brine is based on indirect geophysical methods and there is no

guarantee that brine would contain lithium at an economic

concentration.

View original content with

multimedia:http://www.prnewswire.com/news-releases/orocobre-quarterly-report-of-operations-for-period-ending-30-june-2017-300492174.html

SOURCE Orocobre Limited