0001642365

false

0001642365

2023-01-01

2023-03-31

0001642365

2023-03-31

0001642365

2022-12-31

0001642365

2021-12-31

0001642365

2022-01-01

2022-03-31

0001642365

2022-01-01

2022-12-31

0001642365

2021-01-01

2021-12-31

0001642365

us-gaap:PreferredStockMember

2020-12-31

0001642365

us-gaap:CommonStockMember

2020-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2020-12-31

0001642365

us-gaap:RetainedEarningsMember

2020-12-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2020-12-31

0001642365

2020-12-31

0001642365

us-gaap:PreferredStockMember

2021-12-31

0001642365

us-gaap:CommonStockMember

2021-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2021-12-31

0001642365

us-gaap:RetainedEarningsMember

2021-12-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-12-31

0001642365

us-gaap:PreferredStockMember

2022-03-31

0001642365

us-gaap:CommonStockMember

2022-03-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2022-03-31

0001642365

us-gaap:RetainedEarningsMember

2022-03-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-03-31

0001642365

2022-03-31

0001642365

us-gaap:PreferredStockMember

2022-12-31

0001642365

us-gaap:CommonStockMember

2022-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2022-12-31

0001642365

us-gaap:RetainedEarningsMember

2022-12-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-12-31

0001642365

us-gaap:PreferredStockMember

2021-01-01

2021-12-31

0001642365

us-gaap:CommonStockMember

2021-01-01

2021-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2021-01-01

2021-12-31

0001642365

us-gaap:RetainedEarningsMember

2021-01-01

2021-12-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2021-01-01

2021-12-31

0001642365

us-gaap:PreferredStockMember

2022-01-01

2022-03-31

0001642365

us-gaap:CommonStockMember

2022-01-01

2022-03-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-03-31

0001642365

us-gaap:RetainedEarningsMember

2022-01-01

2022-03-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-01-01

2022-03-31

0001642365

us-gaap:PreferredStockMember

2022-04-01

2022-12-31

0001642365

us-gaap:CommonStockMember

2022-04-01

2022-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2022-04-01

2022-12-31

0001642365

us-gaap:RetainedEarningsMember

2022-04-01

2022-12-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2022-04-01

2022-12-31

0001642365

2022-04-01

2022-12-31

0001642365

us-gaap:PreferredStockMember

2023-01-01

2023-03-31

0001642365

us-gaap:CommonStockMember

2023-01-01

2023-03-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2023-01-01

2023-03-31

0001642365

us-gaap:RetainedEarningsMember

2023-01-01

2023-03-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-01-01

2023-03-31

0001642365

us-gaap:PreferredStockMember

2022-01-01

2022-12-31

0001642365

us-gaap:CommonStockMember

2022-01-01

2022-12-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2022-01-01

2022-12-31

0001642365

us-gaap:RetainedEarningsMember

2022-01-01

2022-12-31

0001642365

us-gaap:PreferredStockMember

2023-03-31

0001642365

us-gaap:CommonStockMember

2023-03-31

0001642365

us-gaap:AdditionalPaidInCapitalMember

2023-03-31

0001642365

us-gaap:RetainedEarningsMember

2023-03-31

0001642365

us-gaap:AccumulatedOtherComprehensiveIncomeMember

2023-03-31

0001642365

us-gaap:SeriesAPreferredStockMember

2022-02-09

0001642365

us-gaap:SeriesAPreferredStockMember

2022-02-01

2022-02-09

0001642365

altb:NHILMember

2023-02-01

2023-02-20

0001642365

altb:NHILMember

2023-02-20

0001642365

altb:ElectronicEquipmentMember

srt:MinimumMember

2023-03-31

0001642365

altb:ElectronicEquipmentMember

srt:MaximumMember

2023-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:NationalHoldingGroupCoLtdMember

2023-01-01

2023-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:NationalHoldingGroupCoLtdMember

2022-01-01

2022-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:NationalHoldingGroupCoLtdMember

2022-01-01

2022-12-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:NationalHoldingGroupCoLtdMember

2021-01-01

2021-12-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:GuoaoHainanNewEnergyCoLtdMember

2023-01-01

2023-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:GuoaoHainanNewEnergyCoLtdMember

2022-01-01

2022-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:GuoaoHainanNewEnergyCoLtdMember

2022-01-01

2022-12-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:GuoaoHainanNewEnergyCoLtdMember

2021-01-01

2021-12-31

0001642365

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2023-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2023-01-01

2023-03-31

0001642365

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2022-03-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2022-01-01

2022-03-31

0001642365

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2022-12-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2022-01-01

2022-12-31

0001642365

us-gaap:AccountsReceivableMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2021-12-31

0001642365

us-gaap:SalesRevenueNetMember

us-gaap:CustomerConcentrationRiskMember

altb:PusiboEnterpriseManagementConsultingCoLtdMember

2021-01-01

2021-12-31

0001642365

us-gaap:CashAndCashEquivalentsMember

2023-03-31

0001642365

us-gaap:CashAndCashEquivalentsMember

2022-12-31

0001642365

us-gaap:CashAndCashEquivalentsMember

2021-12-31

0001642365

altb:Mr.ZonghanWuMember

2023-03-31

0001642365

altb:Mr.ZonghanWuMember

2022-12-31

0001642365

altb:Mr.ZonghanWuMember

2021-12-31

0001642365

altb:TechnicalServiceMember

2023-01-01

2023-03-31

0001642365

altb:TechnicalServiceMember

2022-01-01

2022-03-31

0001642365

altb:TechnicalServiceMember

2022-01-01

2022-12-31

0001642365

altb:TechnicalServiceMember

2021-01-01

2021-12-31

0001642365

us-gaap:SeriesAPreferredStockMember

2023-03-31

0001642365

us-gaap:SeriesAPreferredStockMember

2022-12-31

0001642365

us-gaap:SeriesAPreferredStockMember

2021-12-31

0001642365

altb:MetaVerseInvestmentGroupMember

2022-02-01

2022-02-18

0001642365

altb:CustodianVenturesMember

2021-11-01

2021-11-16

0001642365

altb:CustodianVenturesMember

2021-11-16

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

xbrli:pure

As filed with the Securities and Exchange Commission on July 5, 2023

Registration No. ____________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Alpine Auto Brokers Inc.

(Exact name of Registrant as specified in its charter)

| Nevada |

|

6770 |

|

38-3970138 |

| (State or other jurisdiction of |

|

(Primary Standard Industrial |

|

(I.R.S. Employer |

| incorporation or organization) |

|

Classification Code Number) |

|

Identification No.) |

46 Reeves Road, Pakuranga 2010, New Zealand

Tel: +61 405223877

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Copies to:

McMurdo Law Group, LLC

1185 Avenue of the Americas, 3rd Floor

New York, NY 10036

(917) 318-2865

Approximate date of commencement of proposed sale to the public: As soon as practicable after the registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| |

Large Accelerated Filer |

☐ |

Accelerated Filer |

☐ |

| |

Non-accelerated Filer |

☐ |

Smaller reporting company |

☒ |

| |

|

Smaller reporting company |

☐ |

If an smaller reporting company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

WE HEREBY AMEND THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL WE SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT, OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE SECURITIES AND EXCHANGE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(a), MAY DETERMINE.

The information in this prospectus (this “Prospectus”) is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission (the “SEC”) is effective. This Prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state or other jurisdiction where offers or sales are not permitted.

SUBJECT

TO COMPLETION, DATED JULY 5, 2023

Alpine Auto Brokers Inc.

120,000,000 Shares of Common Stock, $0.001 par value per share

This is a public offering of Alpine Auto Brokers Inc. (“ALTB,” or the “Company”). We are offering 120,000,000 Common Shares at $0.01 per share (the “Shares”), in a best effort, direct public offering, solely by our Chief Executive Officer, Yufeng Zhang, for the Company. There is no minimum proceeds threshold for the offering. The offering will terminate within 360 days from the date of this prospectus. The Company will retain all proceeds received from the shares sold on their account in this offering. The Company has not made any arrangements to place the proceeds in an escrow or trust account. Any proceeds received in this offering may be immediately used by the Company in its sole discretion. There are no minimum purchase requirements for each investor. All proceeds retained by the Company may not be sufficient to continue operations.

Our Shares are not currently traded on any national securities exchange, but are quoted on any over-the-counter market, under the symbol “ALTB.”

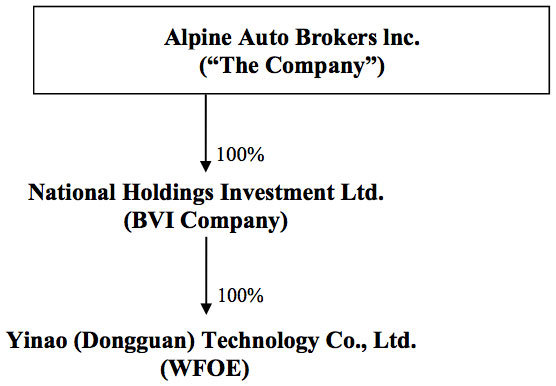

On February 20, 2023, the Company entered into a Definitive Share Exchange Agreement with National Holdings Investment Ltd., a British Virgin Islands corporation (“NHIL”), whereunder the Company acquired 100% ownership interest in NHIL for the issuance of 10,000,000 shares of the Company’s common stock. NHIL through its China based subsidiary, Yinao (Dongguan) Technology Co., Ltd., is mainly engaged in the planning and design service consulting business of new energy charging piles. The transaction closed effective February 24, 2023 and has been treated as a business combination, resulting in NHIL becoming a wholly-owned subsidiary of the Company. As such, the Company recognized the assets and liabilities of NHIL acquired in the reorganization, at their historical carrying amounts.

Investing in our Shares involves a high degree of risk. See “Risk Factors” for a detailed discussion of certain risks that you should consider in connection with an investment in our Shares.

ALTB is a holding company and we operate our business through Yinao (Dongguan) Technology Co., Ltd. (“YDTC”)

YDTC is formed and operating the Peoples Republic of China (“Material PRC Company”) has been duly established and is validly existing as a limited liability company under the laws of the Peoples Republic of China (“PRC Laws”),and has received all authorizations required by the Peoples Republic of China (the “Governmental Authorizations”) for its establishment to the extent such Governmental Authorizations are required under applicable PRC Laws, and its business license is in full force and effect. The Material PRC Company has the capacity and authority to own assets, to conduct business, and to sue and be sued in its own name under PRC Laws. The articles of association, business license and other constitutional documents (if any) of the Material PRC Company complies with the requirements of applicable PRC Laws and are in full force and effect. The Material PRC Company has not taken any corporate action, nor has any legal proceedings commenced against it, for its liquidation, winding up, dissolution, or bankruptcy, for the appointment of a liquidation committee, team of receivers or similar officers in respect of its assets or for any adverse suspension, withdrawal, revocation or cancellation of its business license.

All of the equity interests of the Material PRC Company are owned by NHIL, a BVI company, and (ii) the Material PRC Company has obtained all Governmental Authorizations for the ownership interest owned by NHIL The equity interests of the Material PRC Company are owned by NHIL free and clear of any pledge or other encumbrance under PRC Laws, and there are no outstanding rights, warrants or options to acquire, or instruments convertible into or exchangeable for, any equity interest in the Material PRC Company under PRC Laws, except for such encumbrance that would not be reasonably expected to have a Material Adverse Effect. “Material Adverse Effect,” as used herein, means a material adverse effect on the assets, liabilities, properties or business of the Company.

All of our operations are conducted by our subsidiaries and through our wholly-foreign-owned entity (“WFOE”) based in China which involves unique risks to investors. Our WFOE structure is used to provide investors with exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies. Investors may never hold equity interests in the Chinese operating company. The WFOE structure is not as stable as some have imagined. The senior management and the shareholders of the domestic company play a very important role in the WFOE structure. Once there are changes to such positions involving interests, potential risks of the WFOE structure will appear. Chinese regulatory authorities could disallow this structure, which would likely result in a material change in our operations and/or a material change in the value of the securities we are registering for sale, including that it could cause the value of such securities to significantly decline or become worthless.

The legal and operational risks associated with being based in or having the majority of the Company’s operations in China could result in a material change in the value of the securities we are registering for sale or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Please see the Risk Factor titled “We are faced with risks and uncertainties as a foreign enterprise under PRC laws” on page 14.

Recently, Beijing revamped its rules for overseas listings after ride-hailing Didi Global launched its initial public offering despite warnings from regulators. That triggered a data security investigation led by the Cyberspace Administration of China (“CAC”), which recently culminated with the firm announcing plans to delist in the US in favor of Hong Kong. This shows how recent statements and regulatory actions by China’s government, such as those related to the use of variable interest entities and data security or anti-monopoly concerns, have or may impact the company’s ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange.

Trading securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB determines that it cannot inspect or fully investigate our auditor, and that as a result an exchange may determine to delist your securities.

Investing in our Common Stock involves a high degree of risk. See “Risk Factors” on page 10 for a detailed discussion of certain risks that you should consider in connection with an investment in our Common Stock.

The Company will settle amounts owed under the WFOE structure by transferring dividends, or distributions between the holding company and its subsidiaries, or to investors, which have not yet occurred. We rely primarily on dividends paid by the WFOE for our cash needs, including the funds necessary to pay dividends and other cash distributions, if any, to our shareholders, to service any debt we may incur and to pay our operating expenses. We have made no such distributions to date and we have no current cash management policies in place. We will look to implement one in the near future.

There are no legal, arbitral or governmental proceedings, regulatory investigations or other governmental decisions, rulings, orders, or actions before any Governmental Agencies in progress or pending in the PRC to which the Company or any Material PRC Company is a party or to which any assets of any Material PRC Company is a subject which, if determined adversely against any of the Company and the Material PRC Company, would be reasonably expected to have a material adverse effect.

All dividends declared and payable upon the equity interests in the WFOE may be converted into foreign currency and freely transferred out of the PRC free of any deductions in the PRC, provided that (i) the declaration and payment of such dividends complies with applicable PRC Laws and the constitutional documents of the WFOE, and (ii) the remittance of such dividends out of the PRC complies with the procedures required by the relevant PRC Laws relating to foreign exchange administration.

We face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies. Despite the above, based on our current structure, these risks remain immaterial, regardless of the recent statements and regulatory actions by China’s government.

Adverse changes in economic and political policies of the PRC government could have a material and adverse effect on overall economic growth in China, which could materially and adversely affect our business. General macroeconomic conditions may materially and adversely affect our business, prospects, results of operations and financial position. The PRC government’s control over foreign currency conversion may adversely affect our business and results of operations and our ability to remit dividends. PRC regulation of loans to and direct investments in PRC entities by offshore holding companies may delay or prevent us from using the proceeds of this offering to make loans or additional capital contributions to our operating subsidiary in China, which could materially and adversely affect our liquidity and our ability to fund and expand business.

Assuming no offer, issuance or sale of the Common Shares has been or will be made directly or indirectly within the PRC, a prior approval from the CSRC is not required for the Offering. However, there are substantial uncertainties regarding the interpretation and application of the M&A Rules, other PRC Laws and future PRC laws and regulations, and there can be no assurance that any Governmental Agency will not take a view that is contrary to or otherwise different from our opinions stated herein. Subject to any applicable administrative procedures required by PRC Laws, and provided that all required Governmental Authorizations have been duly obtained, the due application of the net proceeds to be received by the Company from the issue Common Shares as disclosed in the Prospectus under the caption “Use of Proceeds” does not and immediately after the Offering will not contravene any applicable PRC Laws, the articles of association or the business licenses of the Material PRC Company, except for such contravention or default which would not be reasonably expected to have a Material Adverse Effect.

There is no tax or duty payable by or on behalf of the Material PRC Company under applicable PRC Laws in connection with the creation, allotment and issuance Common Shares, provided that each person taking the aforementioned actions is not subject to PRC tax by reason of citizenship, permanent establishment, residence or otherwise subject to PRC tax imposed on or measured by net income or net profits.

Assuming no offer, issuance or sale of the Common Shares has been or will be made directly or indirectly within the PRC, it is not necessary that such documents be filed or recorded now with any Governmental Agency in the PRC.

There are no reporting obligations to any Governmental Agency under PRC Laws on those holders of Common Shares who are not deemed to be PRC residents as defined under applicable PRC Laws, to the extent that no reporting obligation is triggered by the purchase or holding of Common Shares under the PRC anti-monopoly laws, rules and regulations.

We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deem relevant, and subject to the restrictions contained in any future financing instruments.

On December 16, 2021, Public Company Accounting Oversight Board (PCAOB) issued a report on its determinations that PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, a Special Administrative Region of the People’s Republic of China (PRC), because of positions taken by PRC authorities in those jurisdictions. The PCAOB made these determinations pursuant to PCAOB Rule 6100, which provides a framework for how the PCAOB fulfils its responsibilities under the Holding Foreign Companies Accountable Act (HFCAA). The report further listed in its Appendix A and Appendix B, Registered Public Accounting Firms Subject to the Mainland China Determination and Registered Public Accounting Firms Subject to the Hong Kong Determination, respectively. The audit report included in this registration statement for the year ended December 31, 2022, was issued by Shandong Haoxin Certified Accountants Co., Ltd. (“HAOXIN”), an audit firm headquartered in PRC, a jurisdiction that the PCAOB has determined that the PCAOB may be unable to conduct inspections or investigate auditors, despite a recent treaty allowing the PCAOB to review the audit papers of firms in the PRC. Our auditors HAOXIN is among those listed by the PCAOB Mainland China Determination, a determination announced by the PCAOB on December 16, 2021 that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in PRC, because of a position taken by one or more authorities in PRC. As a result, we and investors in our common stock may be deprived of the benefits of such full PCAOB inspections, which could cause investors in our stock to lose confidence in our reported financial information and the quality of our financial statements. In addition, under the HFCAA, our securities may be prohibited from trading on the U.S. stock exchanges or in the over-the-counter trading market in the U.S. if our auditor is not inspected by the PCAOB for three consecutive years, and this ultimately could result in our common stock being delisted. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”), which, if enacted, would amend the HFCAA and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges or in the over-the-counter trading market in the U.S. if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. In the future, if we do not engage an auditor that is subject to regular inspection by the PCAOB, our common stocks may be delisted. See “Risk Factors – Risks associated with doing business in China – The audit report included in this Amendment is prepared by an auditor who is not inspected by the Public Company Accounting Oversight Board and as such, our investors are deprived of the benefits of such inspection. The Company could be delisted if it is unable to timely meet the PCAOB inspection requirements established by the Holding Foreign Companies Accountable Act.”

U.S shareholders may face difficulties in effecting service of process against the Company and officers and director, as they are both based in China. Even with proper service of process, the enforcement of judgments obtained in U.S. courts or foreign courts based on the civil liability provisions of the U.S. federal securities laws would be extremely difficult. Furthermore, there would be added costs and issues with bringing an original action in foreign courts to enforce liabilities based on the U.S. federal securities laws against the Company.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our Shares. As of the date of this prospectus, we do not have any PRC subsidiaries.

Cash dividends, if any, on our Shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

Investing in our Shares involves a high degree of risk. See “Risk Factors” for a detailed discussion of certain risks that you should consider in connection with an investment in our Shares. There are specific risks related to having operations in China that the Company has been organized to avoid.

The registered capital of the Material PRC Company has been duly paid in accordance with applicable PRC Laws and their respective articles of association, to the extent that such registered capital is required to be paid prior to the date hereof.

All of our business operations are conducted in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. Although the PRC economy has been transitioning from a planned economy to a more market-oriented economy since the late 1970s, the PRC government continues to exercise significant control over China’s economic growth through direct allocation of resources, monetary and tax policies, and a host of other government policies such as those that encourage or restrict investment in certain industries by foreign investors, control the exchange between the Renminbi and foreign currencies, and regulate the growth of the general or specific market. While the Chinese economy has experienced significant growth in the past 30 years, growth has been uneven, both geographically and among various sectors of the economy. As the PRC economy has become increasingly linked with the global economy, China is affected in various respects by downturns and recessions of major economies around the world. The various economic and policy measures enacted by the PRC government to forestall economic downturns or bolster China’s economic growth could materially affect our business. Any adverse change in the economic conditions in China, in policies of the PRC government or in laws and regulations in China could have a material adverse effect on the overall economic growth of China and market demand for our outsourcing services. Such developments could adversely affect our businesses, lead to reduction in demand for our services and adversely affect our competitive position.

The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since the late 1970s, the PRC government has been building a comprehensive system of laws and regulations governing economic matters in general. The overall effect has been to significantly enhance the protections afforded to various forms of foreign investments in China. We conduct our business primarily through our WFOE, the WFOE is established in China. These companies are generally subject to laws and regulations applicable to foreign investment in China. However, since these laws and regulations are relatively new and the PRC legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us. In addition, some regulatory requirements issued by certain PRC government authorities may not be consistently applied by other government authorities (including local government authorities), thus making strict compliance with all regulatory requirements impractical, or in some circumstances impossible. For example, we may have to resort to administrative and court proceedings to enforce the legal protection that we enjoy either by law or contract.

Alpine Auto Brokers Inc. is a holding company and we operate our business through our WFOE, YDTC in China. We exercise effective control over the operations of Beijing Kezhao pursuant to a series of contractual arrangements, under which we are entitled to receive substantially all of its economic benefits.

An

investment in our securities is highly speculative, involves a high degree of risk and should be considered only by persons who can

afford the loss of their entire investments. See “Risk Factors” beginning on page 10 of this prospectus.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Prospectus dated , 2023

TABLE OF CONTENTS

You should rely only on information contained in this prospectus. We have not authorized anyone to provide you with additional information or information different from that contained in this prospectus. Neither the delivery of this prospectus nor the sale of our securities means that the information contained in this prospectus is correct after the date of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy our securities in any circumstances under which the offer or solicitation is unlawful or in any state or other jurisdiction where the offer is not permitted.

For investors outside the United States: We have not taken any action that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the securities covered hereby and the distribution of this prospectus outside of the United States.

The information in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since those dates.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the securities offered hereby or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us.

We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourself about, and to observe any restrictions relating to, this offering and the distribution of this prospectus.

Until July 5, 2023, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus.

Prospectus Summary

This summary highlights information that we present more fully elsewhere in this prospectus. This summary does not contain all of the information that you might wish to consider before buying Common Shares in this offering. You should read the entire prospectus carefully, including “Risk Factors” and the financial statements and accompanying notes.

Corporate Overview

Alpine Auto Brokers (the “Company”) was organized as Alpine Auto Brokers, LLC in the state of Utah in December 2010. The Company sold automobiles and provided dealer services, for a fee.

The Company was incorporated as Alpine Auto Brokers, Inc. on May 12, 2011, in the State of Nevada for the purpose of locating and purchasing used vehicles at auctions, from private individuals, from other dealers and selling these vehicles specifically to consumers in Salt Lake City, Utah. On January 1, 2014, the Company acquired 100 percent of the membership interests of Alpine Auto Brokers, LLC, a Utah Limited Liability Company formed on December 10, 2010. The Company operated through its wholly owned subsidiary Alpine Auto Brokers, LLC.

The acquisition was accounted for as a reverse recapitalization in which the operating entity’s historical financial statements become those of the “accounting acquirer” in which historical operating results are presented from inception.

The Company had been dormant since October 27, 2016.

On August 18, 2021, the Eight Judicial District Court in Clark County, Nevada Case No: A-20-816619-B appointed Custodian Ventures, managed by David Lazar as the Company’s Receiver.

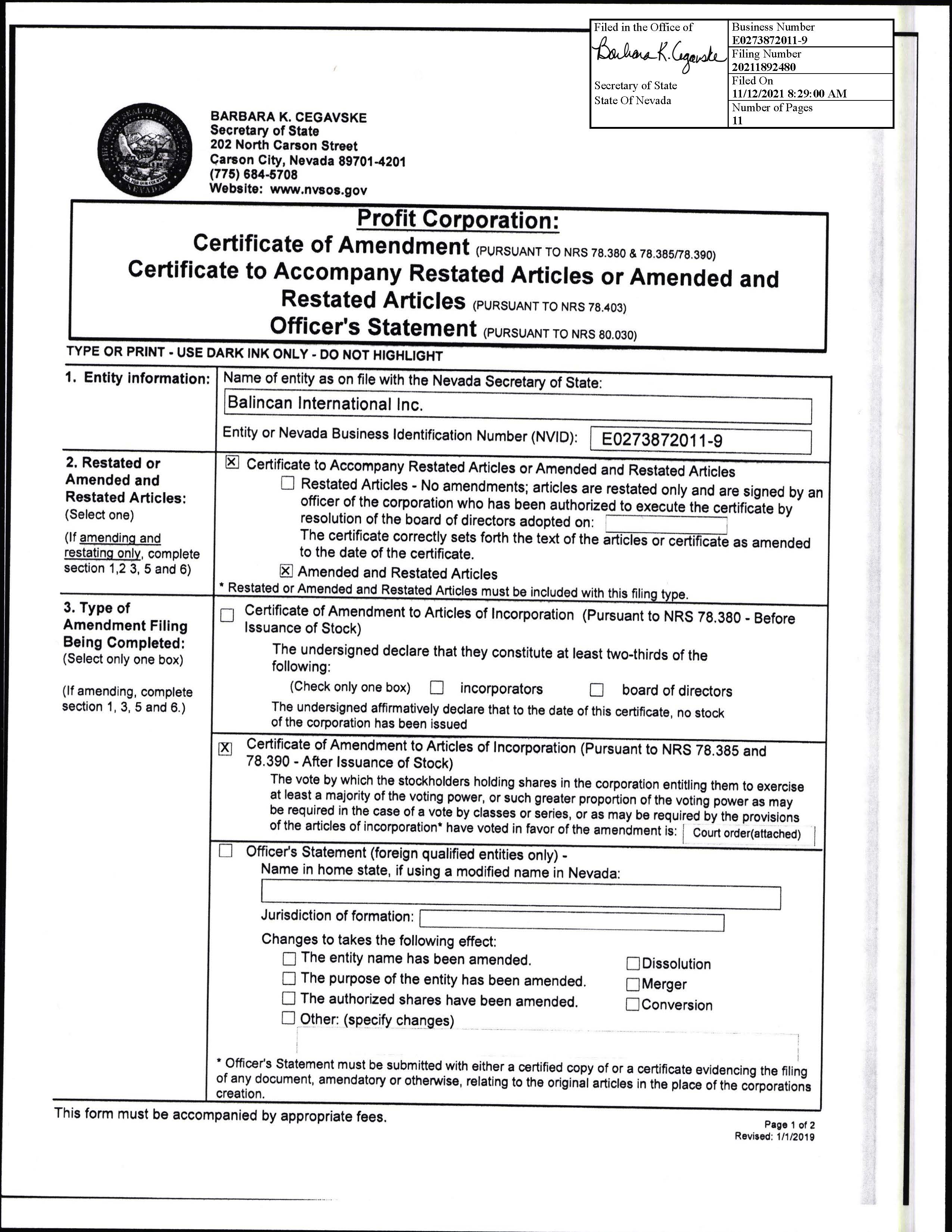

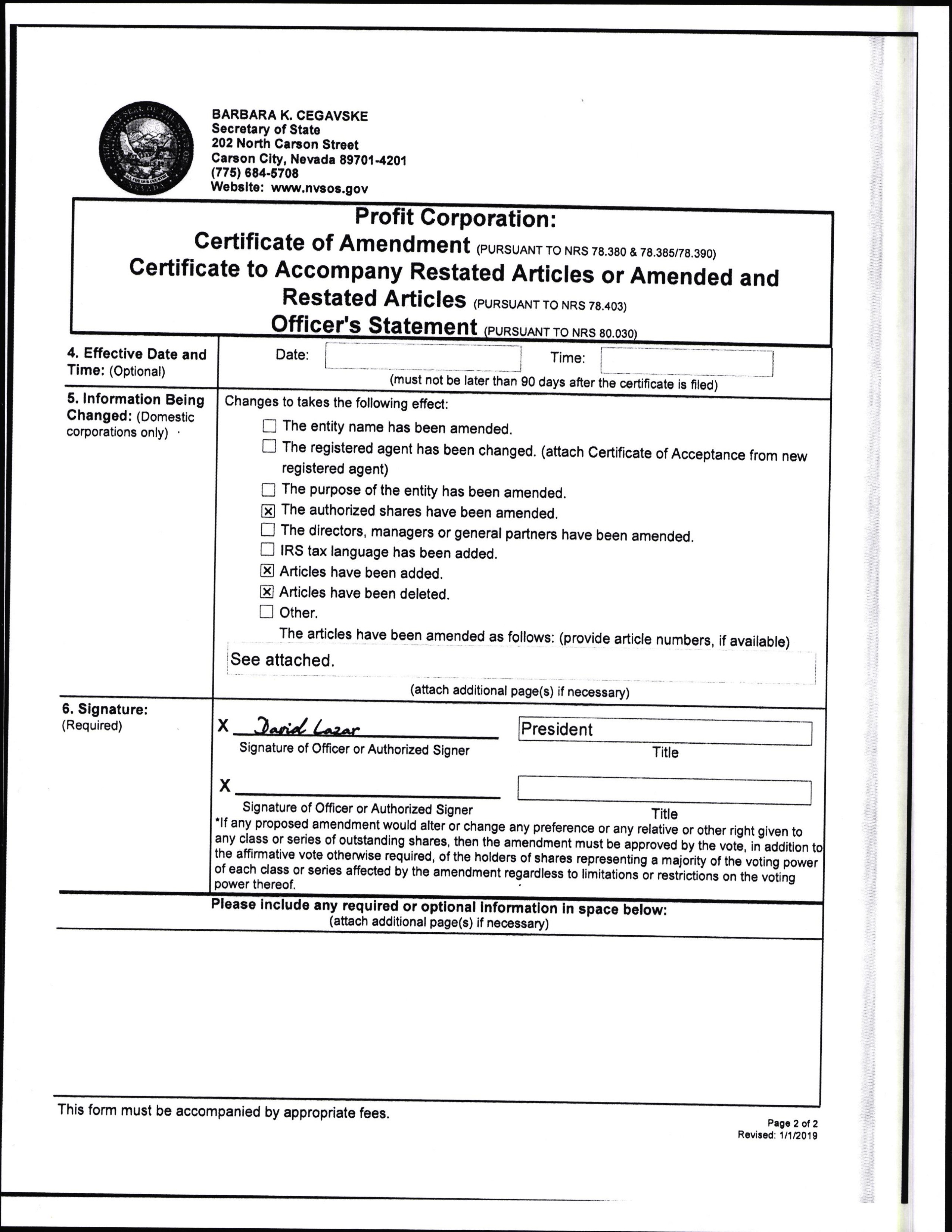

On January 28, 2022, the Company, amended its articles of incorporation change its name back to Alpine Auto Brokers Inc. The change was made because the Company failed to complete its prior name change with FINRA.

On February 9, 2022, as a result of a private transactions, 10,000,000 shares of Series A Preferred Stock, $0.001 par value per share (the “Shares”) of the “Company”, were transferred from Custodian Ventures, LLC to MetaVerse Investment Group (the “Purchaser”). As a result, the Purchaser became the holder of 90% of the voting rights of the issued and outstanding share capital of the Company on a fully-diluted basis of the Company, and became the controlling shareholder. The consideration paid for the Shares was $420,000, with $20,000 being held back pending certain public filings of the Company. The source of the cash consideration for the Shares was personal funds of the Purchaser. In connection with the transaction, David Lazar released the Company from all debts owed to him and/or Custodian Ventures, LLC.

On February 9, 2022, the existing director and officer resigned immediately. Accordingly, David Lazar, serving as a director and an officer, ceased to be the Company’s Chief Executive Officer, Chief Financial Officer, President, Treasurer, Secretary and a Director. At the effective date of the transfer, Zibin Xiao consented to act as the new Chief Executive Officer, President, and member of the Board of Directors. Also on February 9, 2022, Zonghan Wu consented to act as the new CFO, Treasurer, Secretary, and Chairman of the Board of Directors of the Company.

On June 27, 2022, Zibin Xiao resigned as the Chief Executive Officer, President, and member of the Board of Directors. Also on June 27, 2022, Yufeng Zhang consented to act as the new Chief Executive Officer, President, and member of the Board of Directors.

On February 20, 2023, the Company entered into a Definitive Share Exchange Agreement with National Holdings Investment Ltd., a British Virgin Islands corporation (“NHIL”), whereunder the Company acquired 100% ownership interest in NHIL for the issuance of 10,000,000 shares of the Company’s common stock. NHIL through its China based subsidiaries, Yinao (Dongguan) Technology Co., Ltd., is mainly engaged in the planning and design service consulting business of new energy charging piles. The transaction closed effective February 24, 2023 and has been treated as a business combination, resulting in NHIL becoming a wholly-owned subsidiary of the Company. As such, the Company recognized the assets and liabilities of NHIL acquired in the reorganization, at their historical carrying amounts.

As a result of the above transaction, the Company’s corporate structure which is set forth as follows:

Yinao (Dongguan) Technology Co., Ltd (YDTC) was organized in 2022 to engage in the business of constructing and operating charging stations for electric vehicles (“EV”). Our ambition is to build YDTC into a central participant in this growing industry.

In this, our first year of operation, we are focusing our efforts on building a group of consulting clients who are themselves distributors of charging stations. We are undertaking this top-down approach to the industry in part because we lack sufficient financial resources to compete directly with the major participant in the industry. But of equal importance is the opportunity for market impact that we will gain by positioning ourselves as leaders in the charging station industry. As those to whom we provide our services and guidance spread throughout the EV world, they will advertise our brand as their authoritative source for technological and commercial knowledge about the charging station industry, and so our brand will gain value among the relevant participants in the EV world. Our goal is that, when we have secured the financing necessary to compete in the charging station community, we will already be known and identified with quality and know-how related to charging stations.

Our main business at this time, therefore, is to provide consulting services relating to the planning and design of new energy charging piles to customer in Guangdong Province of the PRC. Our customers are enterprises that are either initiating their participation in this industry in general or expanding their operations to Guangdong. In either case, a customer who engages YDTC, will receive, among other things:

|

● |

a survey report on the distribution of new energy charging piles that have been built and are under construction in the district of Guangzhou City in which the customer intends to distribute its stations;, |

|

● |

a business plan based upon an analysis of the existing distribution of charging piles in the target market; |

|

● |

a site selection plan identifying prospective locations where charging piles can be built; |

|

● |

a plan of the electric equipment design plus the type of charging piles to be used; |

|

● |

a plan of the construction and the construction method; as well as |

|

● |

the design and sample drawings of the foundation for the piles, |

1. Corporate History and Structure

On January 10, 2022, Yinao (Dongguan) Technology Co., Ltd (YDTC) was incorporated pursuant to the PRC law.

On June 16, 2022, we established a holding company, National Holdings Investment Ltd (NHIL), under the laws of the British Virgin Islands (BVI).

On October 04, 2022, NHIL acquired 100% ownership interest in YDTC. YDTC becomes a wholly foreign owned enterprise pursuant to the PRC law.

On February 20, 2023, the Company entered into a Definitive Share Exchange Agreement with National Holdings Investment Ltd., a British Virgin Islands corporation (“NHIL”), whereunder the Company acquired 100% ownership interest in NHIL for the issuance of 10,000,000 shares of the Company’s common stock. NHIL through its China based subsidiaries, Yinao (Dongguan) Technology Co., Ltd., is mainly engaged in the planning and design service consulting business of new energy charging piles. The transaction closed effective February 24, 2023 and has been treated as a business combination, resulting in NHIL becoming a wholly-owned subsidiary of the Company.

2. Competitive Strengths

The following are the competitive strengths of Yinao (Dongguan) Technology Co., Ltd:

Top-down approach: The company’s strategy of targeting consulting clients who are themselves distributors of charging stations is a smart move, as it allows the company to establish itself as a leader in the industry while building its financial resources to compete directly with major participants. This approach will help the company gain valuable insights into the industry while building its brand reputation.

Technological and commercial knowledge: YDTC’s focus on providing its clients with technological and commercial knowledge about the charging station industry positions the company as a credible and authoritative source of information in the EV world. This knowledge base will be useful when the company is ready to enter the market as a direct competitor.

Brand reputation: By positioning itself as a leader in the charging station industry through its consulting services, YDTC is laying the foundation for a strong brand reputation. As clients spread the word about the quality of its services, the company’s brand value will increase, making it easier to compete with major players in the industry.

Growing industry: The electric vehicle market is expected to grow rapidly in the coming years, and the need for charging stations will increase accordingly. As a company focused solely on charging stations, YDTC is well-positioned to take advantage of this growth and establish itself as a significant player in the industry.

Strategic location: Dongguan is a key manufacturing hub in China, and the company’s location there gives it access to a large pool of skilled workers, suppliers, and potential customers. This strategic location could give YDTC an edge over competitors located in less advantageous areas.

3. The Charging Station Industry in China

In recent decades, China’s rapid economic growth has enabled more and more consumers to buy their own cars. The result has been the creation of the largest automotive market in the world—but also serious urban air pollution, high greenhouse gas emissions, and growing dependence on oil imports. To counteract those troubling trends, the Chinese government has imposed policies to encourage the adoption of plug-in electric vehicles (EVs). Since buying an EV costs more than buying a conventional internal combustion engine vehicle, in 2009 the government began to provide generous subsidies for EV purchases. As a result, China became the world’s largest market for EV’s, accounting for approximately 50% of global sales. In 2020 1.1 million EVs were produced and sold in China. The central government’s “New Energy Vehicle Industry Development Plan (2021 - 2035) predicted that sales of new energy vehicles would account for 20% of car sales in China in 2025. In fact, during 2022, EV sales represented 22% of new car sales.

As the number of EV purchases grew, paying for the subsidies became extremely costly for the government. As a result, beginning in 2020, China’s government began to phase out the subsidies and instead rely on a mandate imposed on car manufacturers. The mandate requires that a certain percent of all vehicles sold by a manufacturer each year must be battery-powered. To avoid financial penalties, every year manufacturers must earn a stipulated number of points, which are awarded for each EV produced based on a complex formula that takes into account range, energy efficiency, performance, and more. The requirements get tougher over time, with a goal of having EVs make up 40% of all car sales in China by 2030.

The mandate on vehicle manufacturers to produce EVs is supplemented by a number of Chinese government policies:

|

● |

Tax exemptions. The Chinese government exempts electric vehicles from consumption and sales taxes, which can save purchasers tens of thousands of RMB (equivalent to thousands of dollars). It also waives 50% of vehicle registration fees for electric vehicles. |

|

● |

Procurement. The Chinese government also uses its procurement power to promote electric vehicles. A May 2016 order required that half of new vehicles purchased by China’s central government be new energy vehicles within five years. |

|

● |

New auto factory requirements. Chinese regulations strongly discourage the construction of factories for manufacturing internal combustion engine vehicles only. Subject to exceptions that are difficult to satisfy, any new vehicle factory is required to include capacity for the construction of electric vehicles. |

Since EVs will be useless without charging stations, the Chinese central government has promoted the development of EV charging infrastructure as a matter of national policy. As the central government has withdrawn subsidies for purchase of EVs, it has redirected a significant portion of those funds to support the development of EV infrastructure, primarily charging stations. In November 2020, the General Office of the State Council promulgated its “Development Plan of the New Energy Vehicle Industry (2021 - 2035), in which it mandated financial support for the construction of charging stations and proposed preferential policies with respect to allocation of space in parking lots to charging stations. China State Grid and China Southern Grid, China’s two state-owned electric utilities, both have programs to promote the development of electric vehicle charging infrastructure.

Guangdong Province has also been aggressive in support of EVs and EV infrastructure. During 2022 the number of EVs sold in Guangdong Province doubled compared to sales in 2021, and now one-eighth of the EVs manufactured in the PRC are manufactured in Guangdong Province. To support this push toward EVs, Guangdong Province now has more charging stations than any other province in China – and three times as many charging facilities as are located in the entire United States. The Province subsidizes certain purchases of EVs, and encourages insurance companies to provide preferential premiums for EVs. The government of Guangdong Province gives every indication that it will continue to support the expansion of the charging station network indefinitely, with an ultimate goal of maximizing the conversion of vehicular traffic to electric.

4. Competition

The Company is operating in the growing market of new energy charging piles, which is becoming increasingly competitive due to the growing demand for electric vehicles and the government’s push towards cleaner energy. The competition the Company is facing can be broadly categorized into the following:

1. Established players: The new energy charging pile market is already populated with a number of established players such as State Grid, Southern Power Grid, and other major energy companies. These companies have a strong brand presence, financial resources, and expertise in the energy sector. They also have established relationships with customers and are likely to be strong competitors for the Company.

2. New entrants: The market for new energy charging piles is attracting a growing number of new entrants, ranging from start-ups to established companies diversifying into the market. These competitors are also likely to be aggressive in pursuing market share and have the potential to disrupt the market.

3. Technological changes: The charging technology for electric vehicles is constantly evolving, and competitors are investing heavily in developing new charging technologies such as wireless charging, fast charging, and ultra-fast charging. These technological changes could lead to new entrants and disrupt existing market players.

4. Regulatory environment: The regulatory environment for the new energy charging pile market is evolving rapidly, and competitors are likely to be affected by changes in regulations and policies related to the development of the new energy industry. These changes could favor some players and disadvantage others.

In summary, the Company is operating in a highly competitive market, facing competition from established players, new entrants, technological changes, and regulatory environment changes. The Company are developing a strong value proposition and endeavoring to build a competitive advantage to succeed in the market.

5. Marketing

The Company is developing a brand identity that reflects the Company’s values and mission. This includes developing a unique logo, website, and marketing materials that are visually appealing and clearly communicate the Company’s value proposition. The Company also plans to further strengthen our marketing efforts and improve our brand awareness through the following actions:

1. Leverage social media: Social media platforms such as WeChat, Weibo, and LinkedIn can be used to build awareness of our brand, share Company news and updates, and engage with potential customers. The Company can also consider partnering with influencers in the electric vehicle or sustainability space to reach a wider audience.

2. Attend industry events: The Company will attend industry events such as trade shows, conferences, and seminars to network with potential customers and partners. These events can also provide valuable insights into industry trends and customer needs.

3. Foster partnerships: The Company is seeking out partnerships with property developers, government agencies, and other companies in the new energy space. By partnering with these organizations, YDTC can expand its reach and access new customer segments.

4. Overall, by developing a brand identity, leveraging social media, attending industry events, and fostering partnerships, The Company can build awareness of its brand and generate leads in the highly competitive market.

6. PRC Laws and Regulations Affecting Our Business

There are several PRC laws and regulations that could affect the Company’s business, including:

1. Regulations on new energy vehicles: The Chinese government has implemented a number of regulations and policies aimed at promoting the development and adoption of new energy vehicles, including electric vehicles. These policies could create opportunities for the Company as demand for electric vehicle charging infrastructure increases.

2. Intellectual property laws: The Company may be subject to intellectual property laws related to patents, trademarks, and copyrights. This could impact the company’s ability to protect its intellectual property and may affect its competitive position.

It is important for YDTC to stay up-to-date with any changes or developments in these and other relevant laws and regulations in order to ensure compliance and mitigate any potential risks or challenges to its business operations.

7. Risks Related to Our Business

YDTC will face intense competition. It will not achieve market share and customers if it fails to compete effectively.

The demand for charging stations in China is strong, and the barriers to entry into the supply market are not great. So there are many enterprises competing to meet the demand. YDTC’s competitors will include international giants such as Tesla, as well as several major Chinese suppliers of charging stations, as well as many low volume suppliers similar to YDTC. Increased competition may adversely affect its margins, market share and brand recognition, or result in significant losses. When YDTC sets prices for energy, it has to consider how competitors have set prices, since electricity is fungible. When they cut prices or offer additional benefits to compete with YDTC, YDTC may have to lower its own prices or offer additional benefits or risk losing market share, either of which could harm our financial condition and results of operations.

Some of the competitors will have longer operating histories, greater brand recognition, better supplier relationships, larger customer bases and greater financial, technical and marketing resources than YDTC has. These and other smaller companies may receive investment from or enter into strategic relationships with well-established and well-financed companies or investors, which would help enhance their competitive positions. Some of the competitors may be able to secure more favorable terms from suppliers, devote greater resources to marketing and promotional campaigns, adopt more aggressive pricing policies and devote substantially more resources to their website, mobile application and systems development. We cannot assure you that YDTC will be able to compete successfully against current or future competitors, and competitive pressures may have a material and adverse effect on its business, financial condition and results of operations.

For more information see Risk Factors below starting on page 10.

8. Growth Plan

The following is a growth plan for Yinao (Dongguan) Technology Co., Ltd:

Expand consulting services: YDTC should continue to expand its consulting services to attract more clients and establish itself as a top-tier consulting firm in the EV charging station industry. The company can do this by developing and offering new services such as feasibility studies, site selection, and project management.

Develop charging station technology: YDTC should invest in research and development to improve the technology used in its charging stations. By developing more efficient, user-friendly, and innovative charging stations, the company can differentiate itself from competitors and attract more clients. Additionally, YDTC could consider developing its own branded charging stations to sell directly to customers.

Form strategic partnerships: YDTC should form strategic partnerships with other players in the EV industry, such as EV manufacturers, energy providers, and other charging station companies. These partnerships could provide access to new markets, customers, and technology, as well as help the company to stay up-to-date with the latest industry trends.

Raise capital: To fund its expansion plans, YDTC should consider raising capital through various means, such as placement, venture capital, private equity, or debt financing. With adequate funding, YDTC can invest in research and development, expand its operations, and compete with major players in the EV charging station industry.

Overall, YDTC’s growth plan should focus on expanding its consulting services, improving its technology, forming strategic partnerships, and raising capital to achieve its goal of becoming a central participant in the growing EV charging station industry.

The Offering

| Common Shares offered |

|

120,000,000 Common Shares, $0.001 par value per share. |

| |

|

|

| Common Shares Outstanding before this Offering |

|

455,500,000 shares |

| |

|

|

| Common Shares to be Outstanding after this Offering |

|

575,500,000 shares |

| |

|

|

| Use of Proceeds; |

|

While there is no minimum number of shares that will be sold in this offering, if we were to sell the entire number of shares registered, we estimate that our net proceeds from this offering will be approximately $1,200,000, based on an initial public offering price of $0.01 per share, after deducting estimated offering expenses. We plan to use the net proceeds of this offering primarily for general corporate purposes, which may include hiring additional sales, marketing and management personnel, and investing in sales and marketing activities, capital expenditures, and other general and administrative matters. |

| |

|

|

| |

|

See Use of Proceeds. |

| |

|

|

| Minimum number of shares to be sold in this offering. |

|

None. |

| |

|

|

| Market for the shares |

|

There is a limited public market for the shares. The shares trade on the OTC Markets under the symbol “ALTB.” |

| |

|

|

| Risk Factors |

|

Investing in these securities involves a high degree of risk. You should be able to bear a complete loss of your investment and should carefully consider the information set forth in Risk Factors before deciding to invest in our common shares. While we face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies, based on our current structure, these risks remain immaterial, regardless of the recent statements and regulatory actions by China’s government. |

| |

|

|

| |

|

Adverse changes in economic and political policies of the PRC government could have a material and adverse effect on overall economic growth in China, which could materially and adversely affect our business. General macroeconomic conditions may materially and adversely affect our business, prospects, results of operations and financial position. The PRC government’s control over foreign currency conversion may adversely affect our business and results of operations and our ability to remit dividends. PRC regulation of loans to and direct investments in PRC entities by offshore holding companies may delay or prevent us from using the proceeds of this offering to make loans or additional capital contributions to our operating subsidiary in China, which could materially and adversely affect our liquidity and our ability to fund and expand business. |

| |

|

|

| |

|

The M&A Rules and certain other PRC regulations may make it more difficult for us to pursue growth through acquisitions. Under the Enterprise Income Tax Law, we may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders and have a material adverse effect on our results of operations and the value of your investment. The M&A Rules, among other things, purport to require CSRC approval prior to the listing and trading on an overseas stock exchange of the securities of an offshore special purpose vehicle established or controlled directly or indirectly by the Material PRC Company or individuals and formed for the purpose of overseas listing through the acquisition of PRC domestic interests held by such Material PRC Company or individuals. |

| |

|

Based on our understanding of the explicit provisions under PRC Laws, and assuming no offer, issuance or sale of the Common Shares has been or will be made directly or indirectly within the PRC, a prior approval from the CSRC is not required for the Offering. However, there are substantial uncertainties regarding the interpretation and application of the M&A Rules, other PRC Laws and future PRC laws and regulations, and there can be no assurance that any Governmental Agency will not take a view that is contrary to or otherwise different from our opinions stated herein. Subject to any applicable administrative procedures required by PRC Laws, and provided that all required Governmental Authorizations have been duly obtained, the due application of the net proceeds to be received by the Company from the issue Common Shares as disclosed in the Prospectus under the caption “Use of Proceeds” does not and immediately after the Offering will not contravene any applicable PRC Laws, the articles of association or the business licenses of the Material PRC Company, except for such contravention or default which would not be reasonably expected to have a Material Adverse Effect. |

| |

|

|

| |

|

The Company or our subsidiaries are required to obtain from Chinese authorities to operate our business and to offer the securities being registered to foreign investors. The Material PRC Company has obtained all material Governmental Authorizations necessary for its business operations as described in the Prospectus, and such Governmental Authorizations are in full force and effect and all required Governmental Authorizations have been duly obtained. |

| |

|

|

| |

|

The due application of the net proceeds to be received by the Company from the issue of Common Shares as disclosed in the Prospectus under the caption ‘Use of Proceeds’ does not, and immediately after the Offering, will not impact any applicable PRC Laws. |

| |

|

|

| |

|

Our WFOE takes invoices settles the Foreign Exchange with the banks, which pay in Renminbi. No transfer, dividend or distribution has been made to the holding company up to now. |

| |

|

|

| |

|

Earning Distributions |

| |

|

|

| |

|

We rely primarily on dividends paid by WFOE for our cash needs, including the funds necessary to pay dividends and other cash distributions, if any, to our shareholders, to service any debt we may incur and to pay our operating expenses. The Company settles amounts by transferring dividends, or distributions between the holding company and its subsidiaries, or to investors, which have not yet occurred between any of the above. The payment of dividends by entities organized in the PRC is subject to limitations as described herein. If we determine to pay dividends on any of our Common Shares in the future, as a holding company, we will be dependent on receipt of funds from WFOE. |

| |

|

|

| |

|

Our revenue, net income and cash flow are variable. We may experience fluctuations in our results, including our revenue and net income, from period to period, due to a number of other factors, including changes in management fees as well as changes in the amount of distributions, dividends, or interest paid in respect of investments; changes in our operating expenses; or the degree to which we encounter competition and general economic and market conditions. Such variability in the timing and amount of our accruals and management fees may lead to volatility in the trading price of our shares, and, therefore, our results and cash flow for a particular period may not be indicative of our performance in a future period. |

| |

|

|

| |

|

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our Shares. |

| |

|

Pursuant to the Implementation Rules for the new Chinese enterprise income tax law, effective on January 1, 2008, dividends payable by a foreign investment entity to its foreign investors are subject to a withholding tax of up to 10%. Pursuant to Article 10 of the Arrangement Between the Mainland of China and the Hong Kong Special Administration Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income effective December 8, 2006, dividends payable by a foreign investment entity to its Hong Kong investor who owns 25% or more of the equity of the foreign investment entity is subject to a withholding tax of up to 5%. |

| |

|

|

| |

|

The payment of dividends by entities organized in the PRC is subject to limitations, procedures and formalities. Regulations in the PRC currently permit payment of dividends only out of accumulated profits as determined in accordance with accounting standards and regulations in China. WFOE is also required to set aside at least 10% of its after-tax profit based on PRC accounting standards each year to its compulsory reserves fund until the accumulative amount of such reserves reaches 50% of its registered capital. |

| |

|

|

| |

|

The transfer to this reserve must be made before distribution of any dividend to shareholders. The surplus reserve fund is non-distributable other than during liquidation and can be used to fund previous years’ losses, if any, and may be utilized for business expansion or converted into share capital by issuing new shares to existing shareholders in proportion to their shareholding or by increasing the par value of the shares currently held by them, provided that the remaining reserve balance after such issue is not less than 25% of the registered capital. |

| |

|

|

| |

|

Cash dividends, if any, on our Shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%. |

Risk Factors

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and the other information contained in this report before deciding to invest in our common stock.

Risks Related to our Business

If we are unable to hire, retain or motivate qualified personnel, consultants, and advisors, we may not be able to grow effectively.

At the present time, we have only three employees: our management team. Our ability to grow as a public company will be largely dependent on our ability to recruit highly skilled individuals. Future success depends on our continuing ability to identify, hire, develop, motivate and retain highly qualified personnel for all areas of our organization. Competition for such qualified employees is intense. If we do not succeed in attracting excellent personnel or in retaining or motivating them, we may be unable to grow effectively. In addition, all future success depends largely on our ability to retain key consultants and advisors. We cannot assure that any skilled individuals will agree to become an employee or consultant for the Company. Our inability to retain their services could negatively impact our business and our ability to execute our business strategy.

We may not be able to obtain additional funding to meet our requirements.

Our ability to enter into the business of constructing and distributing EV charging stations depends upon our ability to obtain financing through equity financing, debt financing (including credit facilities) or the sale or syndication of some or all of our interests in certain projects or other assets. If our access to existing credit facilities is not available, and if other funding does not become available, there could be a material adverse effect on our business.

The EV charging market is characterized by rapid technological change, which requires YDTC to continue to develop new products and product innovations. Any delays in such development could adversely affect market adoption of its products and YDTC’s financial results.

Continuing technological changes in battery and other EV technologies could adversely affect adoption of current EV charging technology and/or YDTC’s products. YDTC’s future success will depend upon its ability to develop and introduce a variety of new product offerings to address the changing needs of the EV charging market. As new products are introduced, gross margins tend to decline in the near term and improve as the product become more mature and with a more efficient manufacturing process.

As EV technologies change, YDTC may need to upgrade or adapt its charging station technology and introduce new products and services in order to serve vehicles that have the latest technology, in particular battery cell technology, which could involve substantial costs. Even if YDTC is able to keep pace with changes in technology and develop new products and services, its research and development expenses could increase, its gross margins could be adversely affected in some periods and its prior products could become obsolete more quickly than expected.

If YDTC is unable to devote adequate resources to develop products or cannot otherwise successfully develop products or services that meet customer requirements on a timely basis or that remain competitive with technological alternatives, its products and services could lose market share, its revenue will decline, it may experience higher operating losses and its business and prospects will be adversely affected.

Our success depends on our personnel. Loss of key personnel may adversely affect our business.

Our success depends to a significant extent on the performance of our management personnel. In particular, we will depend on the services of key persons. The loss of the services of key persons could have a material adverse effect on the Company’s business, operating results and financial condition.

If we are unable to implement and maintain effective internal control over financial reporting in the future, the accuracy and timeliness of our financial reporting may be adversely affected. In addition, because of our status as a smaller reporting company, you will not be able to depend on any attestation from our independent registered public accounting firm as to our internal control over financial reporting for the foreseeable future.

When we become a reporting company, the Sarbanes-Oxley Act requires, among other things, that we assess disclosure controls and procedures and internal control over financial reporting. In particular, as a public company, we will be required to perform system and process evaluations and testing of our internal control over financial reporting to allow management to report on the effectiveness of our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act. We will be required to furnish a report by management on, among other things, the effectiveness of our internal control over financial reporting for the first fiscal year beginning after the effective date of this offering. However, our independent registered public accounting firm will not be required to attest to the effectiveness of our internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act until the later of the year following our first annual report required to be filed with the SEC or the date we are no longer an “smaller reporting company” as defined in the JOBS Act. Accordingly, you will not be able to depend on any attestation concerning our internal control over financial reporting from our independent registered public accounting firm for the foreseeable future.

Our senior management lacks experience in managing a public company and complying with laws applicable to operating as a U.S. public company domiciled in the Nevada, and failure to comply with such obligations could have a material adverse effect on our business.

Prior to the completion of this offering, YDTC has been operated as a private company located in China. In connection with this offering, we acquired our company, ALTB, and NHIL, and YDTC, our subsidiary in China. In the process of taking these steps to prepare our company for this initial public offering, senior management of YDTC became the senior management of our company. None of senior management of our company has experience managing a public company or managing a Nevada company.

As a result of this offering, our company will become subject to laws, regulations and obligations that do not currently apply to it, such as the Exchange Act of 1934, and our senior management currently has no experience in complying with such laws, regulations and obligations. The senior management is only experienced in operating the business of YDTC in compliance with PRC laws. However, by virtue of this offering, our company will be required to file annual and current reports with the SEC in compliance with U.S. securities and other laws. These obligations can be burdensome and complicated, and failure to comply with such obligations could have a material adverse effect on our company.

The Public Company Accounting Oversight Board (PCAOB) issued a report on its determinations that the Board is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, a Special Administrative Region of the People’s Republic of China (PRC), because of positions taken by PRC authorities in those jurisdictions. The Board made these determinations pursuant to PCAOB Rule 6100, which provides a framework for how the PCAOB fulfils its responsibilities under the Holding Foreign Companies Accountable Act (HFCAA).

To protect investors and to carry out the PCAOB’s mandate, our inspectors and investigators need consistent access across all jurisdictions to the audit work performed for public companies in U.S. capital markets. Rule 6100 sets forth three factors that together reflect the access the PCAOB needs to completely execute its statutory mandate with respect to its inspections and investigations. The PCAOB’s determination report provides the PCAOB’s assessment of these factors based on positions taken by PRC authorities. As discussed in the report, PRC authorities assert that access by the Board to audit work papers and related information can be provided only under a cooperative agreement, but they persistently have taken positions that prevent the finalization of, or their full performance under, such agreements.

The PCAOB has issued its determination report to the U.S. Securities and Exchange Commission, which also has responsibilities under the HFCAA. The appendices to the report identify the PCAOB-registered firms subject to the determinations. Under Rule 6100, the Board will reassess its determinations at least annually.