UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

SCHEDULE

14A

Proxy

Statement Pursuant to Section 14(a) of the Securities

Exchange

Act of 1934

Filed by the Registrant [X]

Filed by a Party other than

the Registrant [ ]

Check the appropriate box:

| [ ] | Preliminary

Proxy Statement. |

| [ ] | Confidential,

for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| [X] | Definitive

Proxy Statement |

| [ ] | Definitive

Additional Materials. |

| [ ] | Soliciting

Material Pursuant to §240.14a-12 |

ECOFIN

SUSTAINABLE AND SOCIAL IMPACT TERM FUND

(Name of

Registrant as Specified In Its Charter)

(Name of

Person(s) Filing Proxy Statement, if other than the Registrant)

Payment

of Filing Fee (Check the appropriate box):

| [ ] | Fee

paid previously with preliminary materials. |

| [ ] | Fee

computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and

0-11. |

TORTOISE

ENERGY INFRASTRUCTURE CORPORATION

TORTOISE POWER AND ENERGY INFRASTRUCTURE FUND, INC.

TORTOISE MIDSTREAM ENERGY FUND, INC.

TORTOISE PIPELINE & ENERGY FUND, INC.

TORTOISE ENERGY INDEPENDENCE FUND, INC.

ECOFIN SUSTAINABLE AND SOCIAL IMPACT TERM FUND

6363

College Boulevard, Suite 100A

Overland Park, Kansas 66211

July

8, 2024

Dear

Fellow Stockholder:

You

are cordially invited to attend the combined annual meeting of stockholders of each of Tortoise Energy Infrastructure Corporation

(“TYG”), Tortoise Power and Energy Infrastructure Fund, Inc. (“TPZ”), Tortoise Midstream

Energy Fund, Inc. (“NTG”), Tortoise Pipeline & Energy Fund, Inc. (“TTP”), Tortoise Energy

Independence Fund, Inc. (“NDP”) and Ecofin Sustainable and Social Impact Term Fund (“TEAF”)

(each a “Company” and collectively, the “Companies”) on Thursday, August 8, 2024

at 10:00 a.m., Central Time at 6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211.

At

the meeting, you will be asked:

| ● | For

all Companies: To elect one director of the Company; |

| ● | For

all Companies: To ratify the selection of Ernst & Young LLP as the independent

registered public accounting firm of the Company for its fiscal year ending November

30, 2024; |

| ● | For

all Companies: To consider and take action on a non-binding Stockholder Proposal

submitted by activist investor Saba Capital Master Fund, Ltd., through its investment

adviser Saba Capital Management, L.P. (the “Saba Proposal”) if properly

presented at the meeting in accordance with federal proxy rules; |

| ● | For

TPZ Only: To consider and take action on a non-binding stockholder proposal submitted

by activist investor Special Opportunities Fund, Inc., through its investment adviser,

Bulldog Investors, LLP (the “TPZ Bulldog Proposal”) if properly presented

at the meeting in accordance with federal proxy rules; |

| ● | For

NDP Only: To consider and take action on a non-binding stockholder proposal submitted

by activist investor Special Opportunities Fund, Inc., through its investment adviser,

Bulldog Investors, LLP (the “NDP Bulldog Proposal”) if properly presented

at the meeting in accordance with federal proxy rules; and |

| ● | For

all Companies: To consider and take action upon such other business as may properly come

before the meeting as permitted by federal proxy rules and by New York Stock Exchange (“NYSE”)

rules. |

Enclosed

with this letter are answers to questions you may have about the director election, the ratification of auditors, and the stockholder

proposals, the formal notice of the meeting, the Companies’ combined proxy statement, which gives detailed information about

the proposals and why each Company’s Board of Directors recommends that you vote “for” the approval of

each of the Company’s proposals, “against” the Saba Proposal (for the stockholders of each Company),

and “against” the TPZ Bulldog Proposal (for TPZ stockholders) and “against” the NDP Bulldog

Proposal (for NDP stockholders), as well as the actual WHITE proxy card for you to sign and return. If you have any questions

about the enclosed proxy or need any assistance in voting your shares, please contact the client relations department of Tortoise

Capital Advisors, L.L.C., the investment adviser to the Companies, by calling 1-866-362-9331.

Your

vote at the annual meeting is especially important this year, and we encourage you to vote on all agenda items. NDP stockholders

should also refer to additional information detailed below.

Please

vote your shares via the internet or by telephone, or complete, sign and date the enclosed WHITE proxy card (your ballot)

and mail it in the postage-paid envelope included in this package.

| |

Sincerely, |

| |

|

| |

Matthew

G.P. Sallee |

| |

Chief

Executive Officer of TYG, TPZ, NTG, TTP, NDP and TEAF |

NOTE:

Even if you plan to attend the meeting, stockholders are requested to fill in, sign, date and return the accompanying WHITE proxy

card in the enclosed envelope without delay. Stockholders may also authorize their proxies by telephone and internet as described

further in the enclosed materials.

For

NDP Stockholders Only:

Your

vote at the annual meeting is especially important this year. Gabriel D. Gliksberg, in his capacity as Manager of ATG

Capital Management, LLC, which provides investment management services to JID 2013 Trust Holdings LLLP (the “Nominating

Stockholder”) has delivered notice of the Nominating Stockholder’s intent to nominate himself and Aaron T. Morris

for election as directors of NDP at the 2024 annual meeting. The Nominating Stockholder’s nominees are NOT endorsed by the

Board of Directors for NDP and your Board is asking that NDP stockholders vote “for” the election of the Board’s

nominee, who is a current director and serves as Chairman of the Board’s Audit Committee. Following the previously announced

decision by Jennifer Paquette that she would not stand for re-election at this year’s Annual Meeting, the Board has elected

to reduce the total size of the Board of Directors for each Company to four directors, effective upon completion of this year’s

Annual Meeting. Accordingly, only one director nominee will be considered for election at the Annual Meeting and the stockholders

of each Company (including NDP stockholders) should vote for only one director candidate.

Returning

the Nominating Stockholder’s gold proxy card, or any other proxy card you may receive from the Nominating Stockholder, will

revoke any WHITE proxy card previously returned to NDP, even if you withhold votes for the Nominating Stockholder’s nominees

on the gold, or any other color, proxy card. Additionally, if the Nominating Stockholder does not, in the GOLD proxy card, solicit

authority to vote on Proposals 2, 3 and 4 for NDP, then any NDP stockholder who returns the GOLD proxy card will be granting a

proxy to vote only on Proposal 1 and not to vote on Proposals 2, 3 and 4. As a result, such an NDP stockholder would only be able

to vote on Proposals 2, 3 and 4 by attending the Annual Meeting and voting in person. Conversely, an NDP stockholder who returns the WHITE proxy card will be able to vote on Proposals 2, 3 and 4 by doing so, but will only

be able to vote on the Board of Directors’ nominee for director and would not be able to cast a vote on the Nominating Stockholder’s

nominees unless such stockholder were to attend the Annual Meeting and vote in person. The Board of Directors encourages you to PLEASE DISCARD ANY GOLD PROXY

CARD OR ANY OTHER PROXY CARD YOU RECEIVE FROM THE NOMINATING STOCKHOLDER, AND PLEASE VOTE USING ONLY THE ENCLOSED WHITE PROXY

CARD. SINCE THE BOARD HAS ELECTED TO REDUCE THE TOTAL SIZE OF THE BOARD OF DIRECTORS TO FOUR MEMBERS EFFECTIVE UPON COMPLETION

OF THE ANNUAL MEETING, ONLY ONE DIRECTOR NOMINEE WILL BE CONSIDERED FOR ELECTION AND YOU SHOULD VOTE FOR ONLY ONE DIRECTOR CANDIDATE.

TORTOISE

ENERGY INFRASTRUCTURE CORPORATION

TORTOISE

POWER AND ENERGY INFRASTRUCTURE FUND, INC.

TORTOISE

MIDSTREAM ENERGY FUND, INC.

TORTOISE

PIPELINE & ENERGY FUND, INC.

TORTOISE

ENERGY INDEPENDENCE FUND, INC.

ECOFIN

SUSTAINABLE AND SOCIAL IMPACT TERM FUND

ANSWERS

TO SOME IMPORTANT QUESTIONS

| Q. | WHAT

AM I BEING ASKED TO VOTE “FOR” ON THIS PROXY? |

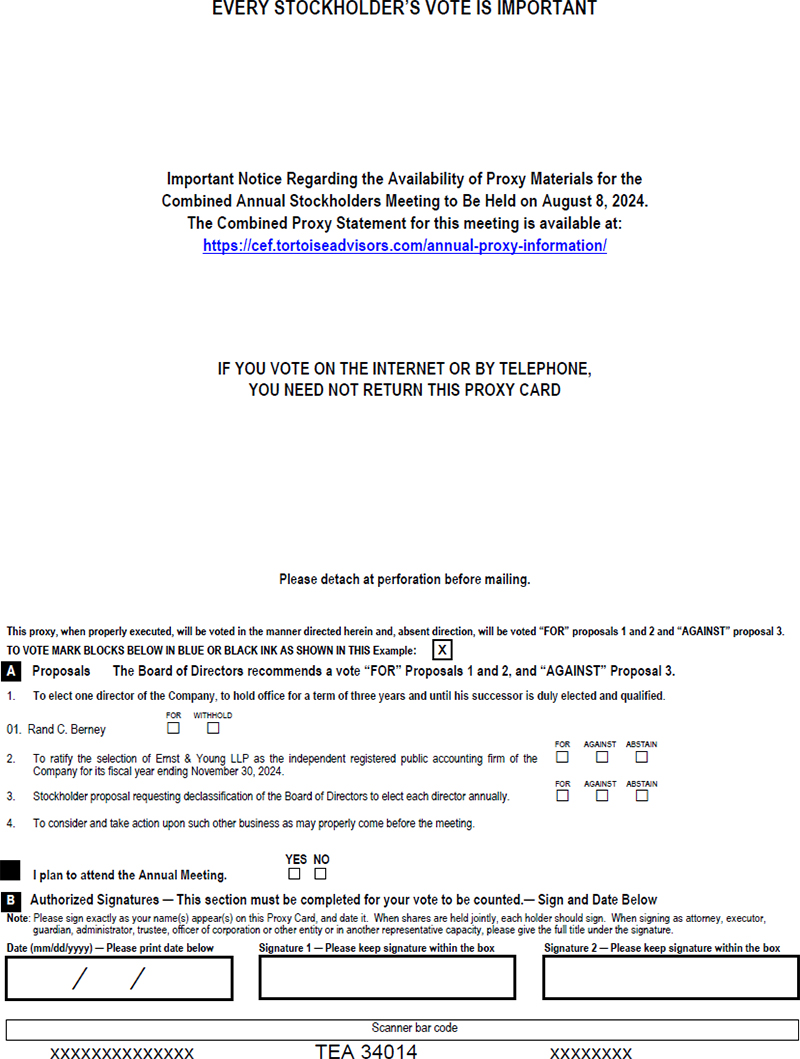

A. This

proxy contains three proposals for each Company to: (i) elect one director to serve until the 2027 Annual Stockholder Meeting;

(ii) ratify Ernst & Young LLP as the Company’s independent registered public accounting firm; and (iii) consider

and take action upon such other business as may properly come before the meeting, including the adjournment or postponement thereof.

In addition, stockholders of each Company are being asked to consider and vote upon a non-binding stockholder proposal submitted

by activist investor Saba Capital Master Fund, Ltd., through its investment adviser Saba Capital Management, L.P. (the “Saba

Proposal”), TPZ stockholders only are being asked to consider and vote upon a non-binding stockholder proposal submitted

by activist investor Special Opportunities Fund, Inc., through its investment adviser, Bulldog Investors, LLP (the “TPZ

Bulldog Proposal”) and NDP stockholders only are being asked to consider and vote upon a non-binding stockholder proposal

likewise submitted by activist investor Special Opportunities Fund, Inc., through its investment adviser, Bulldog Investors, LLP

(the “NDP Bulldog Proposal”).

| Q. | HOW

DOES THE BOARD OF DIRECTORS SUGGEST THAT I VOTE? |

A. The

Board of Directors of each of TYG, NTG, TTP, and TEAF unanimously recommends that you vote “FOR” the proposal to elect

Rand C. Berney to serve as a director of the Company until the 2027 Annual Meeting of Stockholders; “FOR” the proposal

to ratify Ernst & Young LLP as the Company’s independent registered public accounting firm for its fiscal year ended

November 30, 2024; and “AGAINST” the Saba Proposal.

The

Board of Directors of TPZ unanimously recommends that you vote “FOR” the proposal to elect Rand C. Berney to serve

as a director of the Company until the 2027 Annual Meeting of Stockholders; “FOR” the proposal to ratify Ernst &

Young LLP as the Company’s independent registered public accounting firm for its fiscal year ended November 30, 2024; “AGAINST”

the Saba Proposal; and “AGAINST” the TPZ Bulldog Proposal.

The

Board of Directors of NDP unanimously recommends that you vote “FOR” the proposal to elect Rand C. Berney to serve

as a director of the Company until the 2027 Annual Meeting of Stockholders; “FOR” the proposal to ratify Ernst &

Young LLP as the Company’s independent registered public accounting firm for its fiscal year ended November 30, 2024; “AGAINST”

the Saba Proposal; and “AGAINST” the NDP Bulldog Proposal.

A. Voting

is quick and easy. If you hold your shares directly as a stockholder of record, you may vote your shares via the internet, by

telephone (for internet and telephone voting, please follow the instructions on the enclosed WHITE proxy card), or by simply

completing and signing the enclosed WHITE proxy card, and mailing it in the postage-paid envelope included in this package.

You may also vote by attending and voting at the meeting. However, even if you plan to attend the meeting, we urge you to cast

your vote early. That will ensure your vote is counted should your plans change.

If

you hold your shares in “street name” through a broker, bank or other nominee, you should contact your nominee with

your instructions for voting in advance of the Annual Meeting, including any request that your nominee provide you with a legal

proxy. If you hold your shares in “street name,” you are strongly encouraged to vote your shares in advance of

the Annual Meeting, as you will not be able to vote during the Annual Meeting itself unless you request and provide to each applicable

Company a legal proxy from your nominee.

If

you hold your shares directly and intend to vote during the Annual Meeting, please let us know by calling 1-866-362-9331. Regardless

of whether you plan to vote during the Annual Meeting, you may be required to provide valid identification, such as your driver’s

license or passport, and satisfactory proof of ownership of shares in each applicable Company, such as your voting instruction

form (or a copy thereof) or a letter from your broker, bank or other nominee, or other nominee statement indicating ownership

as of the close of business on June 18, 2024.

For

NDP Stockholders Only:

Returning

the Nominating Stockholder’s gold proxy card, or any other proxy card you may receive from the Nominating Stockholder, will

revoke any WHITE proxy card previously returned to NDP, even if you withhold votes for the Nominating Stockholder’s nominees

on the gold, or any other color, proxy card. Likewise, if you have previously voted on the GOLD proxy card, executing and returning

the enclosed WHITE proxy card will revoke any votes you have previously cast using the GOLD proxy card.

Additionally,

it is important to note that, if you return the GOLD proxy card and the Nominating Stockholder does not, in the GOLD proxy card,

solicit authority to vote on Proposals 2, 3 and 4 for NDP, then any NDP stockholder who returns the GOLD proxy card will be granting

a proxy to vote only on Proposal 1 and not to vote on Proposals 2, 3 and 4. As a result, such an NDP stockholder would only be able

to vote on Proposals 2, 3 and 4 by attending the Annual Meeting and voting in person. Conversely, an NDP stockholder who returns the

WHITE proxy card will be able to vote on Proposals 2, 3 and 4 by doing so, but will only be able to vote on the Board of

Directors’ nominee for director and would not be able to cast a vote on the Nominating Stockholder’s nominees unless

such stockholder were to attend the Annual Meeting and vote in person. The Board of Directors encourages you to PLEASE DISCARD ANY

GOLD PROXY CARD OR ANY OTHER PROXY CARD YOU RECEIVE FROM THE NOMINATING STOCKHOLDER, AND PLEASE VOTE USING ONLY THE ENCLOSED WHITE

PROXY CARD. SINCE THE BOARD HAS ELECTED TO REDUCE THE TOTAL SIZE OF THE BOARD OF DIRECTORS TO FOUR MEMBERS EFFECTIVE UPON COMPLETION

OF THE ANNUAL MEETING, ONLY ONE DIRECTOR NOMINEE WILL BE CONSIDERED FOR ELECTION AND YOU SHOULD VOTE FOR ONLY ONE DIRECTOR

CANDIDATE.

| Q. | HOW DOES HOLDING MY SHARES THROUGH A BROKER, INSTEAD OF HOLDING

THEM DIRECTLY IN MY OWN NAME, IMPACT THE WAY THAT MY SHARES MAY BE VOTED ON EACH AGENDA ITEM AT THE ANNUAL MEETING UNDER NYSE RULES? |

A. If your

shares are owned directly in your name with the Company’s transfer agent, you are considered a registered holder of those shares.

If you are the beneficial owner of shares held by a broker or other custodian, you hold those shares in “street name” and

are not a registered stockholder. Brokers or other custodians holding shares in “street name” for the benefit of their customers

and clients will request the instructions of such customers and clients on how to vote their shares on the proposals before the Annual

Meeting. The Companies understand that, under the rules of the NYSE, if you do not give specific voting instructions to your broker, generally

your broker will have discretion to vote your shares on routine matters but will not have discretion to vote your shares on non-routine

matters. Pursuant to these NYSE rules, Proposal No. 2 for each Company for this year’s Annual Meeting, ratification of the Board’s

selection of Ernst & Young LLP as the Company’s independent registered public accounting firm for the fiscal year ending November

30, 2024, qualifies as a “routine” matter, and all other agenda items for this year’s Annual Meeting qualify as “non-routine”

matters. When the broker exercises its discretion to vote on routine matters in the absence of voting instructions from you, a “broker

non-vote” occurs with respect to the non-routine matters since the broker will not have discretion to vote on such non-routine matters.

For a more detailed description of the

application of the votes required for approval of each agenda item at the Annual Meeting, and of the impact of abstentions and

broker non-votes (if any) on the outcome of each such vote and for purposes of determining the presence of a quorum as required for

conducting business at the Annual Meeting, please refer to the information presented under the subheading “Required Vote and

Directors’ Recommendation” with respect to each such item.

| Q. | HOW

WILL MY SHARES BE VOTED IF I RETURN THE ACCOMPANYING WHITE PROXY CARD? |

A. The

shares represented by the accompanying form of WHITE proxy will be voted in accordance with the specifications made on

the proxy if it is properly executed and received by the Company prior to or at the Meeting. Where a choice has been specified

on the WHITE proxy card accompanying this Proxy Statement with respect to the proposals, the shares represented by such

WHITE proxy card will be voted in accordance with the choice specified.

If

you return the accompanying WHITE proxy card that has been validly executed without indicating how your shares should be

voted on a matter and you do not revoke your proxy, your proxy will be voted FOR the election of Rand C. Berney (Proposal 1),

FOR the ratification and appointment of Ernst & Young LLP as the Company’s independent registered public accounting

firm for its fiscal year ended November 30, 2024 (Proposal 2), AGAINST the Saba Proposal (Proposal 3), AGAINST the TPZ Bulldog

Proposal for TPZ stockholders only (TPZ Proposal 4), AGAINST the NDP Bulldog Proposal for NDP stockholders only (NDP Proposal

4) and FOR, ABSTAIN, OR AGAINST any other matters acted upon at the meeting in the discretion of the persons named as proxies

and as permitted by federal proxy rules and by NYSE rules.

For

NDP Stockholders Only: Please note that, if you return the GOLD proxy card and the Nominating Stockholder does not, in the

GOLD proxy card, solicit authority to vote on Proposals 2, 3 and 4 for NDP, then any NDP stockholder who returns the GOLD proxy

card will be granting a proxy to vote only on Proposal 1 and not to vote on Proposals 2, 3 and 4. As a result, such an NDP stockholder

would only be able to vote on Proposals 2, 3 and 4 by attending the Annual Meeting and voting in person. Conversely, an NDP stockholder who returns the WHITE proxy card will be

able to vote on Proposals 2, 3 and 4 by doing so, but will only be able to vote on the Board of Directors’ nominee for director

and would not be able to cast a vote on the Nominating Stockholder’s nominees unless such stockholder were to attend the Annual

Meeting and vote in person. The Board of Directors encourages you to PLEASE DISCARD ANY GOLD PROXY CARD OR ANY OTHER PROXY CARD YOU RECEIVE

FROM THE NOMINATING STOCKHOLDER, AND PLEASE VOTE USING ONLY THE ENCLOSED WHITE PROXY CARD. SINCE THE BOARD HAS ELECTED TO REDUCE THE TOTAL

SIZE OF THE BOARD OF DIRECTORS TO FOUR MEMBERS EFFECTIVE UPON COMPLETION OF THE ANNUAL MEETING, ONLY ONE DIRECTOR NOMINEE WILL BE CONSIDERED

FOR ELECTION AND YOU SHOULD VOTE FOR ONLY ONE DIRECTOR CANDIDATE.

Q. WHO

ARE THE NOMINATING STOCKHOLDER (JID 2013 TRUST HOLDINGS LLLP) AND ITS INVESTMENT ADVISER (ATG CAPITAL MANAGEMENT, LLC), AND HOW

ARE THEY INVOLVED IN THE ANNUAL MEETING?

A. Gabriel

D. Gliksberg, in his capacity as Manager of ATG Capital Management, LLC, which provides investment management services to JID

2013 Trust Holdings LLLP (the “Nominating Stockholder”), has disclosed that the Nominating Stockholder has

acquired a position in NDP representing approximately 2.7% of NDP’s outstanding common stock as of the Record Date for the

Annual Meeting, and intends to nominate Gabriel D. Gliksberg and Aaron T. Morris for election as directors of NDP at the 2024

annual meeting.

| Q. | HOW

MANY DIRECTORS WILL BE ELECTED AT THE ANNUAL MEETING? |

A. Following

the previously announced decision by Jennifer Paquette that she would not stand for re-election at this year’s Annual Meeting,

the Board has elected to reduce the total size of the Board of Directors for each Company to four directors, effective upon completion

of this year’s Annual Meeting. Accordingly, only one director nominee will be considered for election at the Annual Meeting

and the stockholders of each Company (including NDP stockholders) should vote for only one director candidate.

Q. WHAT

SHOULD I DO IF I RECEIVE ANY PROXY MATERIALS OR A GOLD (OR ANY OTHER COLOR) PROXY CARDS FROM THE NOMINATING STOCKHOLDER?

A. In

the event you receive any proxy materials from the Nominating Stockholder or any of its affiliates, NDP urges you to discard and not

to sign, return or vote on any GOLD proxy card or any other proxy card that may be sent to you by or on behalf of the Nominating

Stockholder. As explained above, if you are an NDP stockholder and you return the GOLD proxy card, and the Nominating Stockholder

does not, in the GOLD proxy card, solicit authority to vote on Proposals 2, 3 and 4 for NDP, then any NDP stockholder who returns

the GOLD proxy card will be granting a proxy to vote only on Proposal 1 and not to vote on Proposals 2, 3 and 4. As a result, such

an NDP stockholder would only be able to vote on Proposals 2, 3 and 4 by attending the Annual Meeting and voting in person. Conversely, an NDP stockholder who returns the WHITE proxy card will be

able to vote on Proposals 2, 3 and 4 by doing so, but will only be able to vote on the Board of Directors’ nominee for director

and would not be able to cast a vote on the Nominating Stockholder’s nominees unless such stockholder were to attend the Annual

Meeting and vote in person.

If

you have already voted using a GOLD proxy card sent to you by the Nominating Stockholder, you can revoke it by voting using the

accompanying WHITE proxy card or by voting at the Annual Meeting. Only your latest dated proxy will count, and any proxy

may be revoked at any time prior to its exercise at the Annual Meeting. NDP is not responsible for the accuracy of any information

contained in any proxy materials filed or disseminated by, or on behalf of, the Nominating Stockholder or any of its affiliates

or any other statements that they may otherwise make. NDP reminds stockholders that only one director nominee will be considered

for election at the Annual Meeting and, accordingly, NDP stockholders should vote for only one director candidate.

This

information summarizes information that is included in more

detail

in the Proxy Statement. We urge you to

read

the entire Proxy Statement carefully.

If

you have questions, call 1-866-362-9331.

NOTICE

OF ANNUAL MEETING OF STOCKHOLDERS

| To

the Stockholders of: | Tortoise

Energy Infrastructure Corporation |

Tortoise

Power and Energy Infrastructure Fund, Inc.

Tortoise

Midstream Energy Fund, Inc.

Tortoise

Pipeline & Energy Fund, Inc.

Tortoise

Energy Independence Fund, Inc.

Ecofin

Sustainable and Social Impact Term Fund:

NOTICE

IS HEREBY GIVEN that the combined Annual Meeting of Stockholders of Tortoise Energy Infrastructure Corporation, Tortoise Power

and Energy Infrastructure Fund, Inc., Tortoise Midstream Energy Fund, Inc., Tortoise Pipeline & Energy Fund, Inc. and Tortoise

Energy Independence Fund, Inc., each a Maryland corporation, and Ecofin Sustainable and Social Impact Term Fund, a Maryland statutory

trust (each a “Company” and, collectively, the “Companies”), will be held on Thursday,

August 8, 2024 at 10:00 a.m. Central Time at 6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211 for the following

purposes:

| 1. | For

all Companies: To elect one director of the Company, to hold office for a term of

three years and until his successor is duly elected and qualified; |

| 2. | For

all Companies: To ratify the selection of Ernst & Young LLP as the independent

registered public accounting firm of the Company for its fiscal year ending November

30, 2024; |

| 3. | For

all Companies: To consider and take action on the non-binding Stockholder Proposal

submitted by Saba, if properly presented at the meeting in accordance with federal proxy

rules; |

| 4. | For

TPZ Only: To consider and take action on the non-binding Stockholder Proposal submitted

by Bulldog, if properly presented at the meeting in accordance with federal proxy rules;

and |

| 5. | For

NDP Only: To consider and take action on the non-binding Stockholder Proposal submitted

by Bulldog, if properly presented at the meeting in accordance with federal proxy rules;

and |

| 6. | For

all Companies: To consider and take action upon such other business as may properly

come before the meeting as permitted by federal proxy rules and by NYSE rules. |

The

foregoing items of business are more fully described in the Proxy Statement accompanying this Notice.

Stockholders

of record as of the close of business on June 18, 2024 are entitled to notice of and to vote at the meeting (or any adjournment

or postponement of the meeting).

| |

By

Order of the Board of Directors of each Company, |

| |

|

| |

Diane

M. Bono |

| |

Secretary |

July

8, 2024

Overland Park, Kansas

All

stockholders are cordially invited to attend the meeting in person. Whether or not you expect to attend the meeting, please vote

your shares via the internet, by telephone or by completing, dating, signing and returning the enclosed WHITE proxy card as promptly

as possible in order to ensure your representation at the meeting. If you choose to vote using the enclosed WHITE proxy card,

a return envelope (which postage is prepaid if mailed in the United States) is enclosed for that purpose. Even if you have given

your proxy, you may still vote by attending and voting at the meeting. Please note, however, that if your shares are held of record

by a broker, bank or other nominee and you wish to vote at the meeting, you must obtain from the record holder a legal proxy issued

in your name.

For

NDP Stockholders Only: You may receive solicitation materials from the Nominating Stockholder, including an opposition proxy

statement and proxy card, seeking your proxy to vote for one or both of the individual nominees proposed by the Nominating Stockholder.

Your Board does NOT endorse the Nominating Stockholder’s nominees. NDP is not responsible for the accuracy of information

provided by or relating to the Nominating Stockholder or its nominees contained in solicitation material filed or disseminated

by or on behalf of the Nominating Stockholder, or any other statements that the Nominating Stockholder may make.

Additionally,

NDP stockholders should note that, since the Board has elected to reduce the total size of the Board of Directors to four members

effective upon completion of the Annual Meeting, ONLY ONE DIRECTOR NOMINEE WILL BE CONSIDERED FOR ELECTION AND YOU SHOULD VOTE

FOR ONLY ONE DIRECTOR CANDIDATE.

The

NDP Board urges you NOT to sign or return any proxy card sent to you by the Nominating Stockholder. Do NOT send back any proxy

card you may receive from the Nominating Stockholder, even to vote against one or both of the Nominating Stockholder’s nominees,

as this may cancel your prior vote for the Board’s nominee. Returning the Nominating Stockholder’s gold proxy card,

or any other proxy card you may receive from the Nominating Stockholder, will revoke any WHITE proxy card previously returned

to NDP, even if you withhold votes for the Nominating Stockholder’s nominees on the gold, or any other color, proxy card.

Therefore, PLEASE DISCARD ANY GOLD PROXY CARD OR ANY OTHER PROXY CARD YOU RECEIVE FROM THE NOMINATING STOCKHOLDER, AND PLEASE

VOTE USING ONLY THE ENCLOSED WHITE PROXY CARD.

Even

if you have previously returned a gold proxy card, or any other proxy card sent to you by the Nominating Stockholder, you can

change your vote by signing, dating and returning the enclosed WHITE proxy card in the postage-paid envelope, by recording your

voting instructions via telephone or the internet by following the instructions on the enclosed WHITE proxy card or by voting

in person at the meeting. Likewise, returning the gold proxy card, or any other proxy card you may receive from the Nominating

Stockholder, will revoke any WHITE proxy card previously returned to NDP, even if you withhold votes for the Nominating Stockholder’s

nominees. Only the latest dated proxy card you submit will be counted.

IT

IS IMPORTANT TO NOTE THAT, IF YOU RETURN THE GOLD PROXY CARD AND THE NOMINATING STOCKHOLDER DOES NOT, IN THE GOLD PROXY CARD,

SOLICIT AUTHORITY TO VOTE ON PROPOSALS 2, 3 AND 4 FOR NDP, THEN ANY NDP STOCKHOLDER WHO RETURNS THE GOLD PROXY CARD WILL BE GRANTING

A PROXY TO VOTE ONLY ON PROPOSAL 1 AND NOT TO VOTE ON PROPOSALS 2, 3 AND 4. AS A RESULT, SUCH AN NDP STOCKHOLDER WOULD ONLY BE

ABLE TO VOTE ON PROPOSALS 2, 3 AND 4 BY ATTENDING THE ANNUAL MEETING AND VOTING IN PERSON. CONVERSELY, AN NDP STOCKHOLDER WHO RETURNS THE WHITE PROXY CARD WILL BE

ABLE TO VOTE ON PROPOSALS 2, 3 AND 4 BY DOING SO, BUT WILL ONLY BE ABLE TO VOTE ON THE BOARD OF DIRECTORS’ NOMINEE FOR DIRECTOR

AND WOULD NOT BE ABLE TO CAST A VOTE ON THE NOMINATING STOCKHOLDER’S NOMINEES UNLESS SUCH STOCKHOLDER WERE TO ATTEND THE ANNUAL

MEETING AND VOTE IN PERSON.

TORTOISE

ENERGY INFRASTRUCTURE CORPORATION

TORTOISE POWER AND ENERGY INFRASTRUCTURE FUND, INC.

TORTOISE MIDSTREAM ENERGY FUND, INC.

TORTOISE PIPELINE & ENERGY FUND, INC.

TORTOISE ENERGY INDEPENDENCE FUND, INC.

ECOFIN SUSTAINABLE AND SOCIAL IMPACT TERM FUND

6363

College Boulevard, Suite 100A

Overland Park, Kansas 66211

1-866-362-9331

COMBINED

PROXY STATEMENT

ANNUAL

MEETING OF STOCKHOLDERS

August 8, 2024

This

combined proxy statement is being sent to you by the Boards of Directors of each of Tortoise Energy Infrastructure Corporation (“TYG”),

Tortoise Power and Energy Infrastructure Fund, Inc. (“TPZ”), Tortoise Midstream Energy Fund, Inc. (“NTG”),

Tortoise Pipeline & Energy Fund, Inc. (“TTP”), Tortoise Energy Independence Fund, Inc. (“NDP”)

and Ecofin Sustainable and Social Impact Term Fund (“TEAF”) (each a “Company” and collectively,

the “Companies”). The Board of Directors of each Company is asking you to complete and return the enclosed WHITE

proxy card, permitting your shares of the Company to be voted at the annual meeting of stockholders called to be held on August 8,

2024. The Board of Directors of each Company has fixed the close of business on June 18, 2024 as the record date (the “record

date”) for the determination of stockholders entitled to notice of and to vote at the meeting and at any adjournment thereof

as set forth in this combined proxy statement. This combined proxy statement and the enclosed proxy are first being mailed to stockholders

on or about, July 8, 2024.

Each

Company’s annual report can be accessed through its link on the closed-end fund section of its investment adviser’s

website (www.tortoiseadvisors.com) or on the Securities and Exchange Commission’s (“SEC”) website (www.sec.gov).

Important

Notice Regarding the Availability of Proxy Materials for the Annual Meeting of Stockholders to be Held on August 8, 2024:

This combined proxy statement is available on the internet at https://cef.tortoiseadvisors.com/annual-proxy-information/.

On this site, you will be able to access the proxy statement for the annual meeting and any amendments or supplements to the foregoing

material required to be furnished to stockholders.

This

combined proxy statement sets forth the information that each Company’s stockholders should know in order to evaluate each

of the following proposals. The following table presents a summary of the proposals for each Company and the class of stockholders

of the Company being solicited with respect to each proposal.

| Proposals |

Class

of Stockholders of Each Company Entitled to Vote |

| For

Each Company |

|

1. To

elect one director of the Company, to hold office for a term of three years and until

his successor is duly elected and qualified. |

For

each of TYG, NTG and TTP – Preferred Stockholders only, voting as a class

For

each of TPZ, NDP and TEAF – Common Stockholders, voting as a class |

| For

Each Company: |

|

2. To

ratify the selection of Ernst & Young LLP as the independent registered public accounting

firm of the Company for the fiscal year ending November 30, 2024. |

For

each of TYG, NTG and TTP – Common Stockholders and Preferred Stockholders, voting

together as a single class

For

each of TPZ, NDP and TEAF – Common Stockholders voting as a class |

| For

Each Company: |

|

3. To

consider and take action on the non-binding Stockholder Proposal submitted by Saba, if

properly presented at the meeting in accordance with federal proxy rules. |

For

each of TYG, NTG and TTP – Common Stockholders and Preferred Stockholders, voting

together as a single class

For

each of TPZ, NDP and TEAF – Common Stockholders voting as a class |

| For

TPZ Only: |

|

4. To

consider and take action on the non-binding Stockholder Proposal submitted by Bulldog

(TPZ Proposal 4), if properly presented at the meeting in accordance with federal proxy

rules. |

For

TPZ – Common Stockholders voting as a class |

| For

NDP Only: |

|

5. To

consider and take action on the non-binding Stockholder Proposal submitted by Bulldog

(NDP Proposal 4), if properly presented at the meeting in accordance with federal proxy

rules. |

For

NDP – Common Stockholders voting as a class |

| For

Each Company: |

|

6. To

consider and take action upon such other business as may properly come before the meeting

as permitted by federal proxy rules and by NYSE rules. |

For

each of TYG, NTG and TTP – Common Stockholders and Preferred Stockholders, voting

together as a single class

For

each of TPZ, NDP and TEAF – Common Stockholders voting as a class |

PROPOSAL

ONE

ELECTION

OF ONE DIRECTOR

The

Board of Directors of each Company unanimously nominated Rand C. Berney, following a recommendation by the Nominating and Governance

Committee of each of TYG, TPZ, NTG, TTP, NDP and TEAF, for election as director at the combined annual meeting of stockholders

of the Companies, for a term that will expire on the date of the 2027 annual meeting of stockholders. Mr. Berney is currently

a director of each Company. Mr. Berney has consented to be named in this proxy statement and has agreed to serve if elected. The

Companies have no reason to believe that Mr. Berney will be unavailable to serve.

The

persons named on the accompanying proxy card intend to vote at the meeting (unless otherwise directed) “FOR” the election

of Mr. Berney as a director of each Company. Currently, each Company has five directors. Following the previously announced decision

by Jennifer Paquette that she would not stand for re-election at this year’s Annual Meeting, the Board has elected to reduce

the total size of the Board of Directors for each Company to four directors, effective upon completion of this year’s Annual

Meeting. In accordance with each Company’s Articles of Incorporation (or in the case of TEAF, its Declaration of Trust),

its Board of Directors is divided into three classes of approximately equal size. The terms of the directors of the different

classes are staggered. The term of each of H. Kevin Birzer and Alexandra A. Herger expires on the date of the 2025 annual meeting

of stockholders of each Company and the term of Conrad S. Ciccotello expires on the date of the 2026 annual meeting of stockholders

of each Company. Pursuant to the terms of each of TYG’s, NTG’s and TTP’s preferred shares, the preferred stockholders

of each of those Companies have the exclusive right to elect two directors to their Company’s Board. Following the decision

of Ms. Paquette not to stand for re-election, the Board of each of TYG, NTG and TTP has designated Mr. Berney as the director

the preferred stockholders of that Company shall have the right to elect at this year’s Annual Meeting.

Holders

of the preferred shares of each of TYG, NTG and TTP will vote as a class (with no voting by holders of common shares) on the election

of Mr. Berney as a director of each Company. Holders of common shares of each of TPZ, NDP and TEAF will vote as a class on the

election of Mr. Berney as a director of each Company. Stockholders do not have cumulative voting rights.

With

respect to each Company, if elected, Mr. Berney will hold office until the 2027 annual meeting of stockholders of each Company

and until his successor is duly elected and qualified. If Mr. Berney is unable to serve because of an event not now anticipated,

the persons named as proxies may vote for another person designated by the Company’s Board of Directors.

The

Board of Directors of NDP urges you to REJECT Messrs. Gliksberg and Morris as director nominees. The NDP Board believes

that Mr. Berney is best suited for service on the Board due to his familiarity with NDP as a result of his prior service as a

director. In addition, due to Mr. Berney’s extensive accounting and financial management expertise as a senior financial

executive of a large public company (ConocoPhillips) and, based on information offered by Messrs. Gliksberg and Morris, the Board

believes that Mr. Berney is more capable than either of Messrs. Gliksberg or Morris to lead NDP forward. The Board of Directors

notes that Mr. Berney serves as Chairman of the Audit and Valuation Committee and has been determined by the Board to be an “audit

committee financial expert” as defined by the Securities and Exchange Commission. While not directly related to NDP, the

Board has also taken note of the fact that Mr. Morris is an attorney who represents certain unrelated plaintiffs in litigation

filed against TYG and NTG, which is described in further detail herein under the heading “Additional Information Concerning

Certain Litigation.”

The

following table sets forth each Board member’s name, age and address; position(s) with the Companies and length of time

served; principal occupation during the past five years; the number of companies in the Fund Complex that each Board member oversees

and other public company directorships held by each Board member. Unless otherwise indicated, the address of each director is

6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211. The Investment Company Act of 1940, as amended (the “1940

Act”) requires the term “Fund Complex” to be defined to include registered investment companies advised

by the Company’s investment adviser, Tortoise Capital Advisors, L.L.C. (the “Adviser”). As of May 31,

2024, for each Director, the Fund Complex included TYG, TPZ, NTG, TTP, NDP, TEAF and for Mr. Ciccotello, the Fund Complex also

includes Ecofin Tax-Exempt Private Credit Fund, Inc. (“TSIFX”) whose investment adviser is the Adviser and

on whose board Mr. Ciccotello serves. The Adviser also serves as the investment adviser to three open end mutual funds.

| Nominee

For Director Who Is Independent: |

Name

and

Age |

Positions(s)

Held

With

The

Company

and

Length

of

Time

Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Director |

Other

Public

Company

Directorships

Held

by Director |

Rand

C. Berney

(Born 1955) |

Director

of TYG, NTG, TTP, NDP and TPZ since January 1, 2014; Director of TEAF since inception. |

Formerly

Executive-in- Residence, College of Business Administration, Kansas State University from 2012-2022; Formerly Senior Vice

President of Corporate Shared Services of ConocoPhillips from April 2009 to 2012, Vice President and Controller of ConocoPhillips

from 2002 to April 2009, and Vice President and Controller of Phillips Petroleum Company from 1997 to 2002; Member of the

Oklahoma Society of CPAs, the Financial Executive Institute, American Institute of Certified Public Accountants, the Institute

of Internal Auditors and the Institute of Management Accountants |

Six |

None |

| Remaining

Director Who is an Interested Person: |

Name

and

Age |

Positions(s)

Held

With

The

Company

and

Length

of

Time

Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Director |

Other

Public

Company

Directorships

Held

by Director |

H.

Kevin Birzer*

(Born 1959) |

Director

and Chairman of the Board of each Company since its inception. |

Chairman

of the Board of TortoiseEcofin Parent Holdco, LLC; Member of the Board of Directors of

the Adviser from 2002 through March 2024; Managing Director of the Adviser and member

of the Investment Committee of the Adviser from 2002 through April 1, 2024; Chartered

Financial Analyst (“CFA”) charterholder. |

Six |

None |

| Remaining

Directors Who Are Independent: |

Name

and

Age |

Positions(s)

Held

With

The

Company

and

Length

of

Time

Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Director |

Other

Public

Company

Directorships

Held

by Director |

Conrad

S. Ciccotello

(Born 1960) |

Director

of each Company since its inception. |

Professor

and the Director, Reiman School of Finance, University of Denver (faculty member since 2017); Senior Consultant to the finance

practice of Charles River Associates, which provides economic, financial, and management consulting services (since May 2020);

Formerly Associate Professor and Chairman of the Department of Risk Management and Insurance, Director of the Asset and Wealth

Management Program, Robinson College of Business, Georgia State University (faculty member from 1999 to 2017); Investment

Consultant to the University System of Georgia for its defined contribution retirement plan (2008-2017); Formerly Faculty

Member, Pennsylvania State University (1997-1999); Published a number of academic and professional journal articles on investment

company performance and structure, with a focus on MLPs. |

Seven |

CorEnergy

Infrastructure Trust, Inc.; Peachtree Alternative Strategies Fund |

| Remaining

Directors Who Are Independent: |

Name

and

Age |

Positions(s)

Held

With

The

Company

and

Length

of

Time

Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Director |

Other

Public

Company

Directorships

Held

by Director |

Alexandra

A. Herger

(Born 1957) |

Director

of TYG, NTG, TTP, NDP and TPZ since January 1, 2015; Director of TEAF since inception. |

Retired

in 2014; Previously interim vice president of exploration for Marathon Oil in 2014 prior to her retirement; Director of international

exploration and new ventures for Marathon Oil from 2008 to 2014; Held various positions with Shell Exploration and Production

Co. between 2002 and 2008; Member of the Society of Exploration Geophysicists, the American Association of Petroleum Geologists,

the Houston Geological Society and the Southeast Asia Petroleum Exploration Society; Member of the 2010 Leadership Texas/Foundation

for Women’s Resources since 2010; Director of Panoro Energy ASA, an international independent oil and gas company listed

on the Oslo Stock Exchange; Director of Tethys Oil (Stockholm) and member of PGS (Oslo) nomination committee. |

Six |

None |

| * | Mr.

Birzer, as a former principal of the Adviser from 2002 through April 1, 2024, is an “interested

person” of the Company, as that term is defined in Section 2(a)(19) of the 1940

Act. |

In

addition to the experience provided in the table above, each director possesses the following qualifications, attributes and skills,

each of which factored into the conclusion to invite them to join the Company’s Board of Directors: Mr. Ciccotello, experience

as a college professor, a Ph.D. in finance and expertise in energy infrastructure MLPs; Mr. Berney, experience as a college professor,

executive leadership and business experience; Ms. Herger, executive leadership and business experience; and Mr. Birzer, investment

management experience during his tenure as an executive, portfolio manager and leadership roles with the Adviser prior to April

1, 2024.

Other

attributes and qualifications considered for each director in connection with their selection to join the Board of Directors of

each Company were their character and integrity and their willingness and ability to serve and commit the time necessary to perform

the duties of a director for all of the Companies. In addition, as to each director other than Mr. Birzer, his or her status as

an Independent Director; and, as to Mr. Birzer, his roles with the Adviser were an important factor in his selection as a director.

No experience, qualification, attribute or skill was by itself controlling.

Mr.

Birzer serves as Chairman of the Board of Directors of each Company. Mr. Birzer is an “interested person” of the Companies

within the meaning of the 1940 Act. The appointment of Mr. Birzer as Chairman reflects each Board of Directors’ belief that

his experience, familiarity with each Company’s day-to-day operations and the individuals with responsibility for each Company’s

management and operations provides the Board of Directors with insight into each Company’s business and activities and,

with his familiarity with each Company’s administrative support, facilitates the efficient development of meeting agendas

that address each Company’s business, legal and other needs and the orderly conduct of meetings of the Board of Directors.

Mr. Ciccotello serves as Lead Independent Director. The Lead Independent Director will, among other things, chair executive sessions

of the four directors who are Independent Directors, serve as a spokesperson for the Independent Directors and serve as a liaison

between the Independent Directors and each Company’s management. The Independent Directors will regularly meet outside the

presence of management and are advised by independent legal counsel. The Board of Directors also has determined that its leadership

structure, as described above, is appropriate in light of each Company’s size and complexity, the number of Independent

Directors and the Board of Directors’ general oversight responsibility. The Board of Directors also believes that its leadership

structure not only facilitates the orderly and efficient flow of information to the Independent Directors from management, but

also enhances the independent and orderly exercise of its responsibilities.

Information

About Executive Officers

Mr.

Birzer is the Chairman of the Board of each Company. The preceding tables give more information about Mr. Birzer. The following

table sets forth each other executive officer’s name, age and address; position(s) held with the Company and length of time

served; principal occupation during the past five years; the number of portfolios in the Fund Complex overseen by each officer

and other public company directorships held by each officer. Unless otherwise indicated, the address of each officer is 6363 College

Boulevard, Suite 100A, Overland Park, Kansas 66211. Each officer serves until his or her successor is elected and qualified or

until his or her resignation or removal. As employees of the Adviser, each of the following officers are “interested persons”

of the Company, as that term is defined in Section 2(a)(19) of the 1940 Act.

Name

and

Age |

Position(s)

Held With

The

Company and

Length

of Time Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Officer(1) |

Other

Public

Company

Directorships

Held

by Officer |

Matthew

G.P. Sallee

(Born 1978) |

Chief

Executive Officer of each Company since June 7, 2024; President of TYG and NTG since June 30, 2015. |

Managing

Director of the Adviser since January 2014 and a member of the Investment Committee of the Adviser since June 30, 2015; Senior

Portfolio Manager of the Adviser since February 2019; Portfolio Manager of the Adviser from July 2013 to January 2019; CFA

designation since 2009. |

Six |

None |

Brian

A. Kessens

(Born 1975) |

President

of TTP and TPZ since June 30, 2015. |

Managing

Director of the Adviser since January 2015 and a member of the Investment Committee of the Adviser since June 30, 2015; Senior

Portfolio Manager of the Adviser since February 2019; Portfolio Manager of the Adviser from July 2013 to January 2019; CFA

designation since 2006. |

Two |

None |

Name

and

Age |

Position(s)

Held With

The

Company and

Length

of Time Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Officer(1) |

Other

Public

Company

Directorships

Held

by Officer |

Robert

J. Thummel, Jr.

(Born 1972) |

President

of NDP since June 30, 2015. |

Managing

Director of the Adviser since January 2014 and a member of the Investment Committee of the Adviser since June 30, 2015; Senior

Portfolio Manager of the Adviser since February 2019; Portfolio Manager of the Adviser from July 2013 to January 2019. |

One |

None |

Kate

Moore

(Born 1987) |

President

of TEAF since August 9, 2022 |

Managing

Director since March 29, 2021; Chief Operating Officer of TortoiseEcofin since March 1, 2023; Chief Development Officer of

TortoiseEcofin from March 29, 2021 to March 1, 2023; President of TSIFX since April 2021; Director – Head of Product

Development of the Adviser from July 2020 to March 2021; Director – Strategic Investment Group of the Adviser from July

2019 to July 2020; Vice President – Strategic Investment Group of the Adviser from June 2018 to July 2019; previously

served in various roles at Tradebot Systems, Inc. from July 2009 to June 2018, including most recently as Senior Equity Trader

and Director at Tradebot Ventures. |

Two |

None |

Name

and

Age |

Position(s)

Held With

The

Company and

Length

of Time Served |

Principal

Occupation

During

Past Five Years |

Number

of

Portfolios

in

Fund

Complex

Overseen

by

Officer(1) |

Other

Public

Company

Directorships

Held

by Officer |

Shobana

Gopal

(Born 1962) |

Vice

President of TYG, NTG, TPZ, TTP and NDP since June 30, 2015, and of TEAF since November 5, 2018. |

Managing

Director – Tax of the Adviser since July 2021; Director, Tax of the Adviser from January 2013 to July 2021; Tax Analyst

of the Adviser from September 2006 through December 2012; Vice President of TSIFX since February 2018. |

Seven |

None |

Sean

Wickliffe

(Born 1989) |

Principal

Financial Officer and Treasurer of each Company since April 1, 2024; Vice President and Assistant Treasurer of

each of TYG, NTG, TPZ, TTP, NDP and TEAF from July 14, 2021 to April 1, 2024; |

Vice

President – Financial Operations of the Adviser since January 2021; Senior Financial Operations Analyst of the Adviser

from January 2020 to January 2021; Financial Operations Analyst of the Adviser from December 2016 to January 2020; Junior

Financial Operations Analyst of the Adviser from November 2015 to December 2016. |

Six |

None |

Diane

Bono

(Born 1958) |

Chief

Compliance Officer of TYG since 2006 and of each of NTG, TPZ, TTP and NDP and TEAF since its inception; Secretary of TYG,

NTG, TPZ, TTP and NDP since May 2013 and of TEAF since November 5, 2018. |

Managing

Director of the Adviser since January 2018; Chief Compliance Officer of the Adviser since June 2006; Chief Compliance Officer

and Secretary of TSIFX since February 2018. |

Seven |

None |

| (1) | As

of May 31, 2024, for each executive officer, the Fund Complex included TYG, TPZ, NTG,

TTP, NDP and TEAF and for Mr. Sallee and Mses. Bono, Gopal and Moore, the Fund Complex

also includes TSIFX, for which they serve as officers. |

Committees

of the Board of Directors of each Company

Each

Company’s Board of Directors currently has four standing committees: (i) the Executive Committee; (ii) the Audit and Valuation

Committee; (iii) the Nominating and Governance Committee; and (iv) the Compliance Committee. Currently, all of the non-interested

directors, Messrs. Ciccotello and Berney and Mses. Herger and Paquette, are the only members of each of these committees, except

for the Executive Committee, for each Company. Each Company’s Executive Committee currently consists of Mr. Birzer

and Mr. Ciccotello.

Executive

Committee. The Executive Committee of each Company has authority to exercise the powers of the Board (i) to address emergency

matters where assembling the full Board in a timely manner is impracticable, or (ii) to address matters of an administrative or

ministerial nature. Mr. Birzer is an “interested person” of each Company as defined by Section 2(a)(19) of the 1940

Act. In the absence of either member of the Executive Committee, the remaining member is authorized to act alone.

| ● | Audit

and Valuation Committee. The Audit and Valuation Committee of each of TYG, TPZ, NTG,

TTP, NDP and TEAF was established in accordance with Section 3(a)(58)(A) of the Securities

Exchange Act of 1934, as amended (the “Exchange Act”), and operates under

a written charter adopted and approved by the Board, a current copy of which is available

at the Company’s link on the Adviser’s website (www.tortoiseadvisors.com)

and in print to any stockholder who requests it from the Secretary of the Company at

6363 College Boulevard, Suite 100A, Overland Park, Kansas 66211. The Committee: (i) is

responsible for the appointment, compensation, retention or termination and oversight

of the independent registered public accounting firm (“auditors”); (ii) approves

services to be rendered by the auditors and monitors the auditors’ performance;

(iii) reviews the results of each Company’s audit; (iv) determines whether to recommend

to the Board that the Company’s audited financial statements be included in the

Company’s Annual Report; and (v) responds to other matters as outlined in the Committee

Charter. Each Committee member is “independent” as defined under the applicable

New York Stock Exchange listing standards, and none are “interested persons”

of the Company as defined in the 1940 Act. The Board of Directors of each company has

determined that Conrad S. Ciccotello and Rand C. Berney are each an “audit committee

financial expert.” In addition to his experience overseeing or assessing the performance

of companies or public accountants with respect to the preparation, auditing or evaluation

of financial statements, Mr. Ciccotello has a Ph.D. in Finance. |

| ● | Nominating

and Governance Committee. Each Nominating and Governance Committee member is “independent”

as defined under the New York Stock Exchange listing standards, and none are “interested

persons” of TYG, TPZ, NTG, TTP, NDP or TEAF as defined in the 1940 Act. The Nominating

and Governance Committee of each Company operates under a written charter adopted and

approved by the Board, a current copy of which is available at the Company’s link

on the Adviser’s website (www.tortoiseadvisors.com). The Committee: (i) identifies

individuals qualified to become Board members and recommends to the Board the director

nominees for the next annual meeting of stockholders and to fill any vacancies; (ii)

monitors the structure and membership of Board committees and recommends to the Board

director nominees for each committee; (iii) reviews issues and developments related to

corporate governance issues and develops and recommends to the Board corporate governance

guidelines and procedures, to the extent necessary or desirable; (iv) has the sole authority

to retain and terminate any search firm used to identify director candidates and to approve

the search firm’s fees and other retention terms, though it has yet to exercise

such authority; and (v) may not delegate its authority. The Nominating and Governance

Committee will consider stockholder recommendations for nominees for membership to the

Board so long as such recommendations are made in accordance with the Company’s

Bylaws. Nominees recommended by stockholders in compliance with the Bylaws of the Company

will be evaluated on the same basis as other nominees considered by the Committee. Stockholders

should see “Stockholder Proposals and Nominations for the 2025 Annual Meeting”

below for information relating to the submission by stockholders of nominees and matters

for consideration at a meeting of the Company’s stockholders. The Bylaws of each

Company (other than NDP, TPZ and TEAF) require all nominees for directors, at the time

of nomination, (1) to be at least 21 and less than 75 years of age and have substantial

expertise, experience or relationships relevant to the business of the Company, or (2)

to be a current director of the Company that has not reached 75 years of age. The Bylaws

of each of NDP and TPZ (but not TEAF) require all nominees for directors, at the time

of nomination, (1) to be at least 21 years of age and have substantial expertise, experience

or relationships relevant to the business of the Company, and also to have a master’s

degree in economics, finance, business administration or accounting, a graduate professional

degree in law from an accredited university or college in the United States or the equivalent

degree from an equivalent institution of higher learning in another country, or a certification

as a public accountant in the United States, or be deemed an “audit committee financial

expert” as such term is defined in Item 401 of Regulation S-K (or any successor

provision) promulgated by the Securities and Exchange Commission, or (2) to be a current

director of the Company. The Committee has the sole discretion to determine if an individual

satisfies the foregoing qualifications. The Committee also considers the broad background

of each individual nominee for director, including how such individual would impact the

diversity of the Board, but does not have a formal policy regarding consideration of

diversity in identifying nominees for director. |

| ● | Compliance

Committee. Each Compliance Committee member is “independent” as defined

under the New York Stock Exchange listing standards, and none are “interested persons”

of the Company as defined in the 1940 Act. Each Company’s Compliance Committee

operates under a written charter adopted and approved by the Board, a current copy of

which is available at the Company’s link on the Adviser’s website (www.tortoiseadvisors.com).

The committee reviews and assesses management’s compliance with applicable securities

laws, rules and regulations; monitors compliance with the Company’s Code of Ethics;

and handles other matters as the Board or committee chair deems appropriate. |

The

Board of Directors’ role in the Company’s risk oversight reflects its responsibility under applicable state law to

oversee generally, rather than to manage, the Company’s operations. In line with this oversight responsibility, the Board

of Directors will receive reports and make inquiry at its regular meetings and as needed regarding the nature and extent of significant

risks (including investment, compliance and valuation risks) that potentially could have a materially adverse impact on the Company’s

business operations, investment performance or reputation, but relies upon the Company’s management to assist it in identifying

and understanding the nature and extent of such risks and determining whether, and to what extent, such risks may be eliminated

or mitigated. In addition to reports and other information received from the Company’s management regarding its investment

program and activities, the Board of Directors as part of its risk oversight efforts will meet at its regular meetings and as

needed with the Adviser’s Chief Compliance Officer to discuss, among other things, risk issues and issues regarding the

Company’s policies, procedures and controls. The Board of Directors may be assisted in performing aspects of its role in

risk oversight by the Audit and Valuation Committee and such other standing or special committees as may be established from time

to time. For example, the Audit and Valuation Committee will regularly meet with the Company’s independent public accounting

firm to review, among other things, reports on internal controls for financial reporting.

The

Board of Directors believes that not all risks that may affect the Company can be identified, that it may not be practical or

cost-effective to eliminate or mitigate certain risks, that it may be necessary to bear certain risks (such as investment-related

risks) to achieve the Company’s goals and objectives, and that the processes, procedures and controls employed to address

certain risks may be limited in their effectiveness. Moreover, reports received by the directors as to risk management matters

are typically summaries of relevant information and may be inaccurate or incomplete. As a result of the foregoing and other factors,

the risk management oversight of the Board of Directors is subject to substantial limitations.

None

of the Companies currently has a standing compensation committee. None of the Companies has any employees and the New York Stock

Exchange does not require boards of directors of registered closed-end funds to have a standing compensation committee.

The

following table shows the number of Board and committee meetings held during the fiscal year ended November 30, 2023 for each

of the Companies:

| |

TYG |

TPZ |

NTG |

TTP |

NDP |

TEAF |

| Board

of Directors* |

15 |

15 |

15 |

15 |

15 |

15 |

| Executive

Committee |

0 |

0 |

0 |

0 |

0 |

0 |

| Audit

and Valuation Committee |

5 |

5 |

5 |

5 |

5 |

5 |

| Nominating

and Governance Committee |

2 |

2 |

2 |

2 |

2 |

2 |

| Compliance

Committee |

2 |

2 |

2 |

2 |

2 |

2 |

| * | The

number reflects meetings of the full Board. In addition, there were executive session

meetings of the independent directors as follows: 15 for each of TYG and NTG and 11 for

each of TPZ, TTP, NDP and TEAF. |

During

the 2023 fiscal year, for each of the Companies, all directors who were directors during the 2023 fiscal year attended at least

75% of the aggregate of (1) the total number of meetings of the Board and (2) the total number of meetings held by all committees

of the Board on which they served. None of the Companies has a policy with respect to Board member attendance at annual meetings.

All of the directors of each of TYG, TPZ, NTG, TTP, NDP and TEAF attended the Company’s 2023 annual meeting virtually.

ADDITIONAL

INFORMATION CONCERNING CERTAIN LITIGATION

On

May 12, 2023, plaintiffs Howard Nathanson and Gus Gordon, derivatively and on behalf of TYG and NTG, filed a suit against H. Kevin

Birzer, Conrad S. Ciccotello, Rand C. Berney, Jennifer Paquette, and Alexandra Herger, and against the Adviser, in the Circuit

Court for Baltimore City, Maryland. TYG and NTG also were named in the suit as Nominal Defendants. The complaint, among other

things, alleges derivative claims for breach of fiduciary duty related to the Adviser’s management of TYG and NTG and the

Director Defendants’ oversight thereof and for the adoption of amendments to the Bylaws of TYG and NTG in October 2020 which

the complaint alleges were illegal under the 1940 Act. The complaint seeks unspecified damages related to the alleged breaches

of fiduciary duty, rescission of the Adviser’s investment advisory contract for TYG and NTG pursuant to an alleged violation

of the Investment Advisers Act of 1940, and, on behalf of the plaintiffs in their individual capacities as shareholders of TYG

and NTG, recission of the allegedly illegal Bylaws provisions pursuant to the 1940 Act. The case is Howard Nathanson and Gus

Gordon, derivatively on behalf of Tortoise Energy Infrastructure Corp. and Midstream Energy Fund v. Tortoise Capital Advisors,

L.L.C. et al., Baltimore City Circuit Court, Maryland. Plaintiffs had filed a similar action in the U.S. District Court for

the District of Kansas in August 2022, which was dismissed without prejudice as a result of the forum selection clause in the

Bylaws of TYG and NTG. On February 16, 2024, the Baltimore City Circuit Court granted Defendants’ Motion to Dismiss this

case in its entirety with prejudice. Plaintiffs filed a timely notice of appeal of that decision on March 15, 2024. While management

of the Adviser and the Director Defendants are unable to predict the outcome of this matter, they believe that this case is without

merit and intend to defend against it vigorously, and do not believe the outcome would result in the payment of any monetary damages

by TYG or NTG.

Director

and Officer Compensation

None

of the Companies compensates any of its directors who are interested persons nor any of its officers. The following table sets

forth certain information with respect to the compensation paid by each Company and the Fund Complex for fiscal 2023 to each of

the current independent directors for their services as a director. None of the Companies has any retirement or pension plans.

Name

of

Person,

Position

|

Aggregate

Compensation from Company(1)

|

Pension

or

Retirement

Benefits

Accrued

as

Part of

Company

Expenses

|

Estimated

Annual

Benefits

Upon

Retirement

|

Total

Compensation

from

Company

and

Fund

Complex*

Paid

to

Director

|

| |

TYG

|

TPZ

|

NTG

|

TTP

|

NDP

|

TEAF

|

|

|

|

| Independent

Directors |

|

|

|

|

|

|

|

|

|

| Conrad

S. Ciccotello |

$22,000 |

$22,000 |

$22,000 |

$17,000 |

$17,000 |

$22,000 |

$0 |

$0 |

$156,000 |

| Rand

C. Berney |

$22,000 |

$22,000 |

$22,000 |

$17,000 |

$17,000 |

$22,000 |

$0 |

$0 |

$122,000 |

| Alexandra

A. Herger |

$21,000 |

$21,000 |

$21,000 |

$16,000 |

$16,000 |

$21,000 |

$0 |

$0 |

$116,000 |

| Jennifer

Paquette |

$21,000 |

$21,000 |

$21,000 |

$16,000 |

$16,000 |

$21,000 |

$0 |

$0 |

$116,000 |

| * | For

the fiscal year ended November 30, 2023, for each Director, the Fund Complex included

TYG, TPZ, NTG, TTP, NDP, and TEAF, and for Mr. Ciccotello, the Fund Complex also includes

TSIFX, on whose Board he serves. |

| (1) | No

amounts have been deferred for any of the persons listed in the table. |

For

the 2024 fiscal year, each independent director receives an annual retainer from each Company as set forth below. Additionally,

each independent director receives a fee of $1,000 for each meeting of the Board of Directors he or she attends in person, as

well as $200 for each meeting of the Board of Directors attended telephonically, and $200 for each committee meeting attended

in person or telephonically. The independent directors are reimbursed for expenses incurred as a result of attendance at meetings

of the Board of Directors and Board committees. The independent directors waived the meeting fees for each of TTP and NDP for

2024. The Lead Independent Director, the Chairman of the Audit and Valuation Committee, and each other committee chairman each

receives an additional annual retainer as set forth below. The independent directors are reimbursed for expenses incurred as a

result of attendance at meetings of the Board of Directors and Board committees.

| |

TYG |

TPZ |

NTG |

TTP |

NDP |

TEAF |

| Annual

Board Retainer |

$15,000 |

$15,000 |

$15,000 |

$15,000 |

$15,000 |

$15,000 |

| Lead

Independent Director Retainer |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

| Audit

and Valuation Committee Chairman Retainer |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

$2,000 |

| Other

Committee Chairman Retainer |

$1,000 |

$1,000 |

$1,000 |

$1,000 |

$1,000 |

$1,000 |

Required

Vote and Directors’ Recommendation

With respect to each of TYG,

NTG and TTP, Mr. Berney will be elected by the vote of a plurality of all the votes cast by shares of preferred stock of the Company

present at the meeting, in person or by proxy, to the exclusion of holders of common stock. With respect to TPZ, NDP and TEAF, Mr. Berney

will be elected by the vote of a plurality of all the votes cast by shares of common stock of the Company present at the meeting, in

person or by proxy. Stockholders do not have cumulative voting rights, and proxies cannot be voted for a greater number of persons than

the number of nominees named. A vote by plurality means the nominee with the highest number of affirmative votes, regardless of any votes

withheld, will be elected.

With

respect to TYG, NTG and TTP, each preferred share is entitled to one vote in the election of Mr. Berney. With respect to TPZ,

NDP and TEAF, each common share is entitled to one vote in the election of Mr. Berney.

If your shares are owned directly in your name with the Company’s transfer agent, you are considered a registered holder of those

shares. If you are the beneficial owner of shares held by a broker or other custodian, you hold those shares in “street name”

and are not a registered stockholder. Brokers or other custodians holding shares in “street name” for the benefit of their

customers and clients will request the instructions of such customers and clients on how to vote their shares on the proposals before

the Annual Meeting. The Companies understand that, under the rules of the New York Stock Exchange (“NYSE”), if you

do not give specific voting instructions to your broker, generally your broker will have discretion to vote your shares on routine matters

but will not have discretion to vote your shares on non-routine matters. Pursuant to these NYSE rules, Proposal No. 2 for each Company

for this year’s Annual Meeting, ratification of the Board’s selection of Ernst & Young LLP as the Company’s independent

registered public accounting firm for the fiscal year ending November 30, 2024, qualifies as a “routine” matter, and all

other agenda items for this year’s Annual Meeting qualify as “non-routine” matters. When the broker exercises its discretion

to vote on routine matters in the absence of voting instructions from you, a “broker non-vote” occurs with respect to the

non-routine matters since the broker will not have discretion to vote on such non-routine matters.

For

Stockholders Other Than NDP Stockholders: For the purposes of the vote on this proposal, for each Company, abstentions and

broker non-votes, if any, will not be counted as shares voted and will have no effect on the result of the vote, although they will be considered present for the purpose of determining

the presence of a quorum required to conduct business at the Annual Meeting.

For

NDP Stockholders Only: Abstentions, if any, will not be counted towards a nominee’s achievement of a plurality. However,

because of the contested nature of Proposal 1 for NDP stockholders, under the rules of the NYSE your broker may not vote your

shares on routine matters or non-routine matters. Therefore, due to the contested nature of Proposal 1 for NDP stockholders, we

do not expect broker non-votes to occur or to count towards the determination of whether a quorum of NDP stockholders is present

for purposes of conducting business at the Annual Meeting. We urge you to instruct your broker or other nominee to vote your shares

so that your votes may be counted. The Board unanimously recommends that shareholders vote using the WHITE proxy card.

BOARD

RECOMMENDATION

The

Board of Directors of each of TYG, NTG and TTP unanimously recommends that the preferred stockholders of each Company vote “for”

Mr. Berney as a director. The Board of Directors of each of TPZ, NDP and TEAF unanimously recommends that the common stockholders

of each Company vote “for” Mr. Berney as a director.

For

NDP Stockholders Only:

Please

note that, since the Board has elected to reduce the total size of the Board of Directors to four members effective upon completion

of the Annual Meeting, ONLY ONE DIRECTOR NOMINEE WILL BE CONSIDERED FOR ELECTION AND YOU SHOULD VOTE FOR ONLY ONE DIRECTOR CANDIDATE.

Please discard and do NOT send back the GOLD proxy card, or any other proxy card you may receive from the Nominating Stockholder,

even to withhold votes on Nominating Stockholder’s nominees, as this may cancel your prior vote for NDP’s nominee.

ADDITIONALLY,

PLEASE NOTE THAT, IF YOU RETURN THE GOLD PROXY CARD AND THE NOMINATING STOCKHOLDER DOES NOT, IN THE GOLD PROXY CARD, SOLICIT AUTHORITY

TO VOTE ON PROPOSALS 2, 3 AND 4 FOR NDP, THEN ANY NDP STOCKHOLDER WHO RETURNS THE GOLD PROXY CARD WILL BE GRANTING A PROXY TO