UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT UNDER SECTION 13

OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended July 31, 2022

☐ TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 000-54546

AMERI METRO, INC.

(Exact name of registrant as specified in its charter)

| Delaware | | 45-1877342 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer

Identification No.) |

2575 Eastern Blvd. Suite 102

York, Pennsylvania 17402

(Address of principal executive offices) (zip

code)

Registrant’s telephone number, including area

code: 717-434-0668

Securities registered pursuant to Section 12(b)

of the Act: None

Securities registered pursuant to Section 12(g)

of the Exchange Act:

Common Stock, $0.000001 par value per share

(Title of class)

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act

☐ Yes ☒ No

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent

filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to

the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K.

☒ Yes ☐ No

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company.

See the definitions of “large accelerated filer”, “accelerated filer”, “non-accelerated filer”, “smaller

reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller

reporting company | ☒ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether

any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the

registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as

defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

State the aggregate market value of the voting

and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the

average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second

fiscal quarter.

$0

Indicate the number of shares outstanding of each of the registrant’s

classes of preferred stock and common stock as of the latest practicable date.

| Class | | Outstanding at January 31, 2024 |

| | | |

| Preferred Stock, par value $0.000001 | | 1,800,000 shares |

| Class A Common Stock, par value $0.000001 | | 1,684,000 shares |

| Class B Common Stock, par value $0.000001 | | 4,289,637,844 shares |

| Class C Common Stock, par value $0.000001 | | 191,051,320 shares |

| Class D Common Stock, par value $0.000001 | | 114,000,000 shares |

AMERI METRO, INC.

TABLE OF CONTENTS

INDEX

PART I

ITEMS 1, 1A, 1B, 2,

3 and 4

SEE NOTE 1

PART II

ITEMS 5, 6, 7, and 7A

SEE NOTE 1

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

AMERI METRO, INC.

CONSOLIDATED BALANCE SHEETS

SEE NOTE 1

AMERI METRO, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

SEE NOTE 1

AMERI METRO, INC.

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’

DEFICIT

FOR THE YEARS ENDED JULY 31, 2022 AND 2021

SEE NOTE 1

AMERI METRO, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

SEE NOTE 1

AMERI METRO, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

July 31, 2022 and 2021

NOTE 1 – LETTER FROM AMERI METRO, INC. CFO

April 16, 2024

To Whom this May Concern and for the Record:

Ameri Metro, Inc. (“ARMT”) Background:

ARMT filed its original S-1 on June 13, 2013.

ARMT is an infrastructure company specializing in highly technical toll roads, bridges, high-speed rails, and ports. Since 2013, ARMT

has solidified over 100 infrastructure contracts throughout the USA and the world. All these contracts will ultimately recognize well

more than $1,000,000,000 each averaging approximately $20,000,000,000 each. All contracts ultimately benefit State or Federal agencies.

ARMT has solidified funding of approximately $950,000,000,000 from large financial institutions. ARMT was formed to enhance the humanitarian

crisis everywhere and fund governments whereby the projects are otherwise not affordable without raising taxes.

Personal Background:

My name is Phillip M. (“Marty”) Hicks,

and I am the Co-Chief Executive Officer and Chief Financial Officer of Ameri Metro, Inc. My brief professional background is that I have

more than 40 years’ experience and have served throughout the USA as a forensic accountant, one of the most accredited forensic

accountants in America. I am a former Partner for Deloitte and a veteran professional Whistleblower for the Security Exchange Commission’s

(“SEC”) program since its inception in August of 2011. With respect to White Collar crimes, I have assisted various U.S. Attorney’s

offices and the local Federal Bureau of Investigation. I continue to work with former Federal agents. In this respect, I have extensive

regulatory experience and have assisted with more than 50 Federal indictments including but not limited to; Robert Bandfield, Gregg Mulholland,

Brian Sodi, Scott Key, Barry Honig and others.

Late Regulatory Filings:

We at Ameri Metro, Inc. are providing details resulting in our late

filing of the following:

| |

● |

All 10-Q’s and the 10-K due since January 31, 2022 |

Even though we have adequate books and records for all periods

questioned in the opinion of management, we are unable to file financial statements nor footnotes for these periods due to the following:

| |

1. |

A bogus lawsuit was filed before the financial periods in question by Andrew Lentz for more than $389,000,000. Mr. Lentz was a former consultant to a related entity of ARMT. Mr. Lentz was fully aware that this bogus lawsuit would cause significant damages to ARMT including, but not limited to, not being able to meet its financial reporting requirements. To date, his strategy has worked. |

| |

2. |

Andrew Lentz boasted to many ARMT affiliates about “blowing the whistle” on ARMT to the SEC. In fact, the SEC indeed accepted the Lentz TCR (complaint) and acted upon it by opening an investigation and issuing questionnaires to all but a few ARMT Stock Class B shareholders. Only an insider such as Andrew Lentz was privy to that very private information. ARMT is currently supporting a lawsuit against Lentz and the SEC on behalf of our Class B shareholders for violations of personal privacy, fraud and extortion. In that regard, Lentz was not in a position to file a lawsuit of this magnitude, notably having filed personal bankruptcy three times, thus fraudulent. |

| |

3. |

Even though Andrew Lentz clearly made materially false statements to a Federal agency (i.e. the SEC) causing serious damages to ARMT, the SEC has not pursued, to our knowledge, a criminal complaint against him via the Department of Justice. In fact, the SEC continues to pursue de-registration of ARMT regardless of merit. |

| |

4. |

The SEC has not issued its final position on accounting for digital currencies. The proposed SEC position remains in direct conflict with GAAP standards and the AICPA’s proposals. We agree with the AICPA’s position because the SEC’s position opens the door to massive financial statement manipulations. |

If these matters remain outstanding and the SEC

continues its course of action against ARMT, we have no choice but to do the following or any combination thereof to protect our interests:

| |

● |

File a complaint in Federal Court against the SEC and Andrew Lentz for numerous allegations involving damages of more than $1,000,000,000. |

| |

● |

Immediately tokenize ARMT so that the company is no longer regulated by the SEC because the company will no longer have equity positions. |

| |

● |

File our complaint against Andrew Lentz for consideration to the US Attorney’s office in Pennsylvania. |

We sincerely hope this clarifies our inability

to meet our regulatory filing requirements, several of which are directly a consequence of SEC negligence.

| Very Truly, | |

| | |

| /s/ Phillip M. Hicks. | |

Phillip M. (“Marty”) Hicks, Co-CEO, CFO

Cc: Resnick & Louis

Ameri Metro, Inc. | 2575

Eastern Blvd, Suite 102, York PA 17402 | Ameri-Metro.com

ITEMS 9, 9A and 9C

SEE NOTE 1

PART III

ITEMS 10, 11, 12, 13 and 14

SEE NOTE 1

PART IV

ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES

EXHIBITS

| 3.1 |

|

Articles

of Incorporation (filed with the Form 10 November 9, 2011) |

| 3.2 |

|

Amended

by-laws (filed as part of the Form 8-K/A filed January 18, 2013) |

| 3.3 |

|

Cert.

of Amendment Cert. of Incorporation of Ameri Metro |

| 5.1 |

|

Opinion of Counsel on legality of securities being registered* |

| 10.1 |

|

Master

Indenture Agreement of Alabama Toll Facilities, Inc. (filed with the Form 8-K January 18, 2013) |

| 10.2 |

|

Master

Indenture Agreement of Hi Speed Rail Facilities, Inc. (filed with the Form 8-K January 18, 2013) |

| 10.3 |

|

Master

Indenture Agreement of Hi Speed Rail Facilities Provider, Inc. (filed with the Form 8-K January 18, 2013) |

| 10.4 |

|

TEMS

engagement (filed as part of the Form 8-K/A filed January 18, 2013) |

| 10.5 |

|

Alabama

Indenture Agreement (filed as part of the Form 8-K/A filed January 18, 2013) |

| 10.6 |

|

High

Speed Rail Indenture Agreement (filed as part of the Form 8-K/A filed January 18, 2013) |

| 10.7 |

|

Damar

Agreement (filed as part of the Form 8-K/A filed January 18, 2013) |

| 10.8 |

|

Agreement

For Construction (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.9 |

|

Assignment

Agreement For Construction (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.10 |

|

Payment

Agreement to Penndel Land Co (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.11 |

|

Ameri

Metro Inc. / HSR Tech Inc. Licensing of Intellectual Property Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.12 |

|

HSR

Tech LOI Tech Use Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.13 |

|

Opportunity

License Agreement Entities (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.14 |

|

Master

Agreement for Construction Nonprofits (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.15 |

|

Master

Agreement for Construction Entities (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.16 |

|

Consulting

Agreement HSRFP Inc. (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.17 |

|

Consulting

Agreement HSRF Inc. (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.18 |

|

Company

Founder Emp. Agreement(filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.19 |

|

Directorship

Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.20 |

|

Letter

of Intent for Port Trajan property (filed with the Registration Statement on Form S-1 filed June 13, 2013) |

| 10.21 |

|

Port

De Ostia Inc. Agreement GTI (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.22 |

|

C-Bar

Marshall Rebar Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.23 |

|

Ameri

Metro & Jewell LOI (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.24 |

|

Master

Consulting Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.25 |

|

Master

Trustee Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.26 |

|

2015

Executive Incentive Compensation Program (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.27 |

|

Establishing

the Compensation Committee (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.28 |

|

Amendment

to Payment Agreement Penndel Land Co. (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.29 |

|

Amendment

to HSR Technologies Inc. Payment Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.30 |

|

Amendment

to Damar TruckDeck LLC Payment Agreement (filed as part of the Form 10-K/A filed November 6, 2019) |

| 10.31 |

|

TEMS

consent form letter (filed as part of the Form 10-K/A filed November 6, 2019) |

| 23.1 |

|

Consent of Counsel (included in Exhibit 5.1)* |

| 31.1 |

|

CERTIFICATION PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002* |

| 31.2 |

|

CERTIFICATION PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002* |

| 32.1 |

|

CERTIFICATION OF PRINCIPAL EXECUTIVE OFFICER TO 18 U.S.C. SECTION 1350, AS ADOPTED PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002* |

| 32.2 |

|

CERTIFICATION OF PRINCIPAL ACCOUNTING AND FINANCIAL OFFICER PURSUANT TO 18 U.S.C. SECTION 1350, AS ADOPTED PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002* |

| 99.1 |

|

ProAdvisor

Valuation report, dated November 1, 2016 (filed as Exhibit 99.1 to the registration statement on Form S-1, filed on November 23,

2016, and incorporated herein by reference) |

| 99.2 |

|

ProAdvisor

consent letter (filed as Exhibit 99.2 to the registration statement on Form S-1, filed on November 23, 2016) |

| 99.3 |

|

June

12, 2012 Agreement and Plan of Reorganization (filed as part of the Form 8-K/A filed January 18, 2013) |

| 99.4 |

|

Alabama

Legislative Act 506 (filed as part of the Form 8-K/A filed January 18, 2013) |

| 99.5 |

|

Form

of subscription agreement for sale of the shares (filed with the Registration Statement on Form S-1 filed June 13, 2013) |

| 99.6 |

|

Intended

use of Master Trust Indentures (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.7 |

|

Florida

Alabama TPO Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.8 |

|

Alabama

Toll Road Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.9 |

|

Appalachian

Region Commission Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.10 |

|

Atlantic

Energy & Utilities Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.11 |

|

High

Speed Rail Projects Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.12 |

|

Port

Freeport & Brazoria Fort Bend Rail District Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.13 |

|

High

Speed Rail & Ancillary Projects Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.14 |

|

Port

of Ostia Inc. @ KSJM International Airport Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.15 |

|

Portus

De Jewel Mexico Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.16 |

|

KSJM

International Airport Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.17 |

|

HSR

Freight Line Inc. / Phila. Port Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.18 |

|

HSR

Freight Line Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.19 |

|

HSR

Passenger Services Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.20 |

|

HSR

Technologies Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.21 |

|

Malibu

Homes Inc. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.22 |

|

Platinum

Media Inc. Bond Indenture (filed as part of the Form 10-Q filed December 30, 2019) |

| 99.23 |

|

Port

De Claudius Inc. & Port Trajan of Pa. Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.24 |

|

Panama

Canal – Alabama Port Partnership (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.25 |

|

Lord

Chauffeurs Inc. – Business Jet Center @ KSJM Airport Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.26 |

|

HSR

Freight Line Inc. & HSR Passenger Services Coast to Coast Rail Bond Indenture (filed as part of the Form 10-K/A filed November

6, 2019) |

| 99.27 |

|

New

York – Washington Rail Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.28 |

|

Ann

Charles International Cargo Airport Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.29 |

|

Texas

International Trade Corridor Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.30 |

|

Virginia

Crescent Line Rail Bond Indenture (filed as part of the Form 10-K/A filed November 6, 2019) |

| 99.31 |

|

Shah

Mathias transferred 102,600,000 Class B shares from his personal holdings, equally, to 20 related entities that Ameri Metro Inc.

holds a 25% interest in 19 of the related entities and a 10% interest in one of the related entities. (filed with the Form 8-K September

17,2020) |

| 99.32 |

|

2015

Equity Incentive Plan, the plan was funded with class B shares. According to the plan schedule. (filed with the form 8-K September

17, 2020) |

| 99.33 |

|

NorAsia

Consulting & Advisory Valuation Report (filed with the form 8-K September 4, 2020) |

| 99.34 |

|

Lord

Chauffeurs, LTD Amendment to Opportunity License Agreement (filed with the form 8-K September 4, 2020) |

| 99.35 |

|

Slater

& West, Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.36 |

|

Port of Ostia, Inc. Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.37 |

|

Port de Claudius, Inc.

Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.38 |

|

Platinum Media, Inc. Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.39 |

|

Penn Insurance Services

LLC. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.40 |

|

Natural Resources LLC.

Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.41 |

|

Malibu Homes, Inc. Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.42 |

|

KSJM International Airport,

Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.43 |

|

HSR Technologies, Inc.

Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.44 |

|

HSR Passenger Services,

Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.45 |

|

HSR Logistics, Inc. Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.46 |

|

HSR Freight Line, Inc.

Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.47 |

|

Eastern Development &

Design, Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.48 |

|

Cape Horn Abstracting Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.49 |

|

Atlantic Energy & Utility

Products, Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.50 |

|

Ann Charles International

Airport, Inc. Amendment to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.51 |

|

Ameri Cement Inc. Amendment

to Opportunity License Agreement (filed with the form 8-K August 14, 2020) |

| 99.52 |

|

Portus de Jewel Seaport

& Inland Port project Amendment to Opportunity License Agreement (filed with the form 8-K August 12, 2020) |

| 99.53 |

|

Susquehanna Mortgage Bankers

Corp. 25% non-controlling interest in SMBC (filed with the form 8-K August 12, 2020) |

| 99.54 |

|

HSR Technologies, Inc has

acquired intellectual property from NP&G Innovations, Inc. (filed with the form 8-K July 30, 2020) |

| 99.55 |

|

Platinum Media Inc. joint

venture agreement with Resurrection Media PlatJV, LLC. (filed with the form 8-K July 30, 2020) |

| 99.56 |

|

Platinum Media Inc. joint

venture agreement with Best of Times Productions. (filed with the form 8-K July 30, 2020) |

| 99.57 |

|

HSR Technologies, Inc.

acquired DAMAR TruckDeck bed liner intellectual property. (filed with the form 8-K July 30, 2020) |

| 99.58 |

|

HSR Technologies Inc. combat

COVID 19 exclusive right to use FDA Approved ozone equipment. (filed with the form 8-K July 22, 2020) |

| 99.59 |

|

HSR Logistics Inc. has

acquired an easement. (filed with the form 8-K July 22, 2020) |

| 99.60 |

|

Ann Charles International

Airport Inc. acquired Air Cyprus Aviation Limited, (filed with the form 8-K July 20, 2020) |

| 99.61 |

|

Norasia Valuation Report dated July 31, 2020* |

| 101.INS |

|

Inline XBRL Instance Document. |

| 101.SCH |

|

Inline XBRL Taxonomy Extension Schema Document. |

| 101.CAL |

|

Inline XBRL Taxonomy Extension Calculation Linkbase Document. |

| 101.DEF |

|

Inline XBRL Taxonomy Extension Definition Linkbase Document. |

| 101.LAB |

|

Inline XBRL Taxonomy Extension Label Linkbase Document. |

| 101.PRE |

|

Inline XBRL Taxonomy Extension Presentation Linkbase Document. |

| 104 |

|

Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101) |

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| Date: April 17, 2024 |

By: |

/s/ Shah Matthias |

| |

|

Shah Matthias |

| |

|

Founder, Chairman, and Chief Executive Officer |

| |

|

|

| Date: April 17, 2024 |

By: |

/s/ Phillip M Hicks |

| |

|

Phillip M Hicks |

| |

|

Co-CEO and CFO |

Pursuant to the Securities Exchange Act of 1934,

this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| NAME |

|

OFFICE |

|

DATE |

| |

|

|

|

|

| /s/ Debra Mathias |

|

|

|

|

| Debra Mathias |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ James Becker |

|

|

|

|

| James Becker |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Shahjahan C. Mathias |

|

|

|

|

| Shahjahan C. Mathias |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Donald E. (“Nick”) Williams, Jr. |

|

|

|

|

| Donald E. (“Nick”) Williams, Jr. |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Suhail Matthias |

|

|

|

|

| Suhail Matthias |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Bryan Elicker |

|

|

|

|

| Bryan Elicker |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Robert Choiniere |

|

|

|

|

| Robert Choiniere |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ Keith A. Doyle |

|

|

|

|

| Keith A. Doyle |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ James Kingsborough |

|

|

|

|

| James Kingsborough |

|

Director |

|

April 17, 2024 |

| |

|

|

|

|

| /s/ John Thompson |

|

|

|

|

| John Thompson |

|

Director |

|

April 17, 2024 |

14

N/A

N/A

9999

false

FY

0001534155

true

0001534155

2021-08-01

2022-07-31

0001534155

2022-01-31

0001534155

us-gaap:PreferredStockMember

2024-01-31

0001534155

us-gaap:CommonClassAMember

2024-01-31

0001534155

us-gaap:CommonClassBMember

2024-01-31

0001534155

us-gaap:CommonClassCMember

2024-01-31

0001534155

ck0001534155:CommonClassDMember

2024-01-31

iso4217:USD

xbrli:shares

Exhibit 5.1

April

17, 2024

Board

of Directors of Ameri Metro Inc

Mr. Shah Mathias, CEO

Topic:

Ameri Metro Inc.

Since management didn’t provide financials for the period ended October 31, 2022 we couldn’t perform a review for the financials.

Elkana

Amitai

Israel office +972-4-843-7373

| Mitzpe Netofa, Israel 1592500

New Hampshire office

+1-860-327-8708 | 500 Commercial Street, Suite 502 Manchester, NH 03101

Exhibit

31.1

OFFICER’S

CERTIFICATION PURSUANT TO SECTION 302 OF SARBANES OXLEY ACT

I,

Shah Mathias, certify that:

1.

I have reviewed this annual report on Form 10-K for the year ended July 31, 2022 of Ameri Metro, Inc.

2.

Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary

to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect

to the period covered by this report;

3.

Based on my knowledge, the financial statements, and other financial information included

in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the issuer

as of, and for, the periods presented in this report;

4.

The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls

and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control

over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the issuer and have:

a)

Designed such disclosure controls and procedures, or caused such disclosure controls

and procedures to be designed under our supervision, to ensure that material information relating

to the registrant, including its consolidated subsidiaries, is made known to us by others within

those entities, particularly during the period in which this report is being prepared;

b)

Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed

under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial

statements for external purposes in accordance with generally accepted accounting principles;

c)

Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report

our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the

period covered by this report based on such evaluation; and

d)

Disclosed in this report any change in the registrant’s internal control over financial reporting

that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth

fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the

registrant’s internal control over financial reporting; and

5.

The registrant’s other certifying officer(s) and I have disclosed, based on our most recent evaluation

of internal control over financial reporting, to the registrant’s auditors and the audit committee of the small business

registrant’s board of directors (or persons performing the equivalent functions):

a)

All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which

are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial

information; and

b)

Any fraud, whether or not material, that involves management or other employees who have a significant role in the

registrant’s internal control over financial reporting.

| Date:

April 17, 2024 |

By: |

/s/

Shah Mathias |

| |

|

Shah

Mathias |

| |

|

Chief

Executive Officer

(Principal

Executive Officer) |

Exhibit 31.2

OFFICER’S CERTIFICATION PURSUANT TO SECTION

302 OF SARBANES OXLEY ACT

I, Phillip M Hicks, certify that:

1.

I have reviewed this annual report on Form 10-K for the year ended July 31, 2022 of Ameri Metro, Inc.

2. Based on my knowledge, this report does not contain

any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the

circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial

statements, and other financial information included in this report, fairly present in all material respects the

financial condition, results of operations and cash flows of the issuer as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer(s)

and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules

13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in

Exchange Act Rules 13a-15(f) and 15d-15(f)) for the issuer and have:

a) Designed such disclosure controls

and procedures, or caused such disclosure controls and procedures to be designed under our supervision,

to ensure that material information relating to the registrant, including its consolidated

subsidiaries, is made known to us by others within those entities, particularly during the period in which

this report is being prepared;

b) Designed such internal control over financial

reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable

assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in

accordance with generally accepted accounting principles;

c) Evaluated the

effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about

the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such

evaluation; and

d) Disclosed in this report any

change in the registrant’s internal control over financial reporting that occurred during

the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual

report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control

over financial reporting; and

5. The registrant’s other certifying

officer(s) and I have disclosed, based on our most recent evaluation of internal control

over financial reporting, to the registrant’s auditors and the audit committee of the small

business registrant’s board of directors (or persons performing the equivalent functions):

a) All significant deficiencies and

material weaknesses in the design or operation of internal control over financial reporting which are reasonably

likely to adversely affect the registrant’s ability to record, process, summarize and report financial information;

and

b) Any fraud, whether or not material, that involves

management or other employees who have a significant role in the registrant’s internal control over financial reporting.

| Date: April 17, 2024 |

By: |

/s/ Phillip M Hicks |

| |

|

Phillip M Hicks |

|

|

Co-CEO and CFO |

Exhibit 32.1

CERTIFICATION PURSUANT TO 18 U.S.C. SECTION

1350

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the Annual Report of Ameri

Metro, Inc. (the “Company”) on Form 10-K for the year ended July 31, 2022 as filed with the Securities and Exchange Commission

on the date hereof (the “Report”), each of the undersigned, in the capacities and on the dates indicated below, hereby certifies

pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that to his knowledge:

1. The Report fully complies with the requirements

of Section 13(a) or 15(d) of the Securities Exchange Act of 1934; and

2. The information contained in the Report fairly

presents, in all material respects, the financial condition and results of operation of the Company.

3. A signed original of this written statement

required by Section 906 has been provided to the Company and will be retained by the Company and furnished to the Securities and Exchange

Commission or its staff upon request.

| Date: April 17, 2024 |

By: |

/s/ Shah Mathias |

| |

|

Shah Mathias |

|

|

Chief Executive Officer |

Exhibit 32.2

CERTIFICATION PURSUANT TO 18 U.S.C. SECTION

1350

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the Annual Report of Ameri

Metro, Inc. (the “Company”) on Form 10-K for the year ended July 31, 2022 as filed with the Securities and Exchange Commission

on the date hereof (the “Report”), each of the undersigned, in the capacities and on the dates indicated below, hereby certifies

pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that to his knowledge:

1. The Report fully complies with the requirements

of Section 13(a) or 15(d) of the Securities Exchange Act of 1934; and

2. The information contained in the Report fairly

presents, in all material respects, the financial condition and results of operation of the Company.

3. A signed original of this written statement

required by Section 906 has been provided to the Company and will be retained by the Company and furnished to the Securities and Exchange

Commission or its staff upon request.

| Date: April 17, 2024 |

By: |

/s/ Phillip M Hicks |

| |

|

Phillip M Hicks |

|

|

Co-CEO and CFO |

Exhibit 99.61

Valuation

Report Prepared by Ameri Metro, Inc. Management assisted by NorAsia Consulting & Advisory to the Board of Directors.

August 31, 2020

The Valuation Report provides an estimated

and expected range of potential Fair Market Values for Ameri Metro, Inc.’s common stock.

August 31, 2020,

To the Board of Directors of

Ameri Metro, Inc.

2575 Eastern Blvd, Suite 102

York, PA 17402

Re: Management’s Fair Market

Value for its Common Stock as of August 31, 2020

This valuation was performed for corporate

planning purposes; the resulting conclusion of value should not be used for any other purpose or by any other party for any purpose.

Based on our analysis we have determined

a range of values for Ameri Metro, Inc.’s (“AM” or “the Company”) by utilizing standard valuation metrics:

| B) Valuation per Share | |

| | |

| |

| | |

| | |

| |

| Net Asset Approach | |

| | |

| |

| i) Basic | |

$ | 301.03 | | |

$ | 220.66 | |

| ii) Diluted | |

$ | 299.78 | | |

$ | 220.66 | |

| | |

| | | |

| | |

| Discounted Future Net Income | |

| | | |

| | |

| i) Basic | |

$ | 238.20 | | |

$ | 174.61 | |

| ii) Diluted | |

$ | 237.21 | | |

$ | 174.08 | |

| | |

| | | |

| | |

| Discounted Future Cash Flows | |

| | | |

| | |

| i) Basic | |

$ | 142.07 | | |

$ | 104.14 | |

| ii) Diluted | |

$ | 141.48 | | |

$ | 103.82 | |

| | |

| | | |

| | |

| Market Value Approach | |

| | | |

| | |

| i) Basic | |

$ | 2,955.79 | | |

$ | 2,166.70 | |

| ii) Diluted | |

$ | 2,943.51 | | |

$ | 2,160.09 | |

The details for the calculations are

summarized in this report in various sections but the detailed calculations are summarized in the Excel file “Valuation Tables Ameri

Metro Final”.

The Company since July 2020 through

to August 2020 has completed 14 independent cash transactions for options to acquire Ameri Metro Inc. common stock with strike prices

from $3,000 to $4,100 per share. Total cash received for these transactions are $294,000. The July 2020 strike prices were in the $3,000

range and the August 2020 prices were last at $4,100 which could be a leading indicator for the true market value of Ameri Metro’s

stock once it has obtained appropriate liquidity in the market.

Ameri Metro, Inc does have a ticker

symbol under (ARMT) which is on the OTC Markets, however there is no volume and this would not be an indicator of value.

Ameri Metro financial model is determined

based on all existing projects that have been identified and closed by the Company’s management. Ameri Metro’s valuation has

not considered the financing and growth factor in financing on going volume of projects through Susquehanna Mortgage Bankers, which is

in the process of re-registering as a financial institution and will become part of the United States of America Federal Reserve System.

Based

on our analysis, we believe that once the Ameri Metro shares are listed on the NYSE and sponsored by the appropriate market makers

that their value could trade between $2,160 and $4,100 per share given the significant earnings expectations and projects

identified.

This report is limited to the information

provided by management and any information that was not provided or is incorrect is the responsibility of management. We are not responsible

for any information provided after August 31, 2020 that could materially increase or decrease the expected valuation per share.

Respectfully submitted,

Ameri Metro, Inc. Management Assisted

by NorAsia Consulting & Advisory

| Table of Contents |

| |

|

|

|

| |

1) |

Introduction |

5 |

| |

|

|

|

| |

2) |

Definition of Fair Market Value |

5 |

| |

|

|

|

| |

3) |

Valuation Methodologies |

5 |

| |

|

|

|

| |

|

A) |

Going Concern Valuation |

5 |

| |

|

|

|

| |

|

|

i) |

The Market Approach |

6 |

| |

|

|

|

| |

|

|

ii) |

The Asset-Based Approach |

6 |

| |

|

|

|

| |

|

|

iii) |

The Income Approach |

6 |

| |

|

|

|

| |

|

|

|

Projected Net Income |

6 |

| |

|

|

|

| |

|

|

|

Projected Cash Flow |

6 |

| |

|

|

|

| |

4) |

Determine if Stock is Closely Held & Impact on Valuation |

6 |

| |

|

|

|

| |

5) |

The Nature of the Business and the History of the Enterprise from its Inception |

7 |

| |

|

|

|

| |

6) |

The Economic Outlook in General and the Condition and Outlook in General and the Condition and Outlook of the Specific Industry in Particular |

50 |

| |

|

|

|

| |

7) |

The Book Value of the Stock and the Financial Condition of the Business |

51 |

| |

|

|

|

| |

8) |

The Earning Capacity of the Company |

51 |

| |

|

|

|

| |

9) |

Enterprise Goodwill or Other Intangible Value |

52 |

| |

|

|

|

| |

10) |

Sales of the Stock and the Size of the Block of Stock to be Valued |

53 |

| |

|

|

|

| |

11) |

Valuation Calculations |

54 |

| |

|

|

|

| |

A) |

The Income Approach |

54 |

| |

|

|

|

| |

|

i) |

Projected Net Income |

54 |

| |

|

|

|

| |

|

ii) |

Projected Cash Flow |

55 |

| |

|

|

|

| |

B) |

The Market Approach |

56 |

| |

|

|

|

| |

C) |

The Asset-Based Approach |

57 |

| |

|

|

|

| |

|

i) |

Adjusted Book Values Method |

57 |

| |

|

|

|

| |

12) |

Other Items |

58 |

| |

|

|

|

| Appendix A: Other Calculations to Support Share Price Valuation |

60 |

This valuation was performed for corporate

planning purposes; the resulting conclusion of value should not be used for any other purpose or by any other party for any purpose.

The projections in the attached are

prepared based on a calendar year December 31 since Ameri Metro, Inc. is expecting to close on equity financing in the fourth quarter

of 2020 to commence project funding and the licensing for Susquehanna Mortgage Bankers should be completed in mid-November and the Bond

Issuances would commence in the fourth quarter 2020 and early 2021.

| 2) | Definition of Fair Market Value for this Report: |

The

definition of “Fair Market Value” for this Report is in line with which a stock market analyst would observe “Fair

Market Value”, which is typically the liquid trading price of the stock however many analysts will apply discounted cash flow and

discounted net income models to assess the reality of the stocks pricing1.

Fair

Value for financial reporting purposes is defined by ASC 820, “the price that would be received to sell an asset or paid

to transfer a liability in an orderly transaction between market participants at the measurement date.” This definition is similar

in many respects to “fair market value,” which is defined in IRS Revenue Ruling 59-602.

This analysis prepared by management

to present to Ameri Metro’s board of directors for the expected trading values of the company’s stock. The analysis is management’s

best estimate of the stock and is subject to significant interpretation, assumptions and expectations about the future that there can

be no guarantees that the realities can be met. Additionally, other third parties reviewing the same information could come to the same,

similar or very different conclusions than those provided in this report.

| 3) | Valuation Methodologies: |

| A) | Going Concern Valuation |

There are two fundamental bases on which a company may be

valued:

| 1. | As a going concern3,

and |

Ameri Metro, Inc. will be valued on a going concern basis,

as this is expected to be the highest value and best use to determine an expected share price for the Company.

| 1 | https://www.investopedia.com/articles/stocks/08/discounted-cash-flow-valuation.asp |

| 2 | https://gbq.com/measuring-fair-value-for-financial-reporting-

purposes/#:~:text=Accounting%20Standards%20Codification%20(ASC)%20Topic,market%20value%2C%E2%80%9D%20which%20

is%20defined |

| 3 | https://www.investopedia.com/terms/g/going_concern_value.asp |

The market approach is fundamental to

valuation as fair market value is determined by the markets. Management’s approach was to utilize gross projected net income and

gross projected cash flow and applying an industry market multiple for each business within Ameri Metro. The Company operates in a diverse

group of businesses from technology to entertainment to infrastructure, therefore using management’s best estimate we analyzed each

business independently.

| ii) | The Asset-Based Approach |

The asset based approach, sometimes

referred to as the cost approach, is an asset-oriented approach rather than a market oriented approach. Each component of a business is

valued separately.

Utilizing projected net income and cash

flows are acceptable methods to determine the fair market value of share price and assets. Since estimating the future income of a business

is at times considered to be speculative, historic data is used as a starting point, if it is available in the correct format and is accurate,

in several of the acceptable methods under the premised

For Ameri Metro, Inc. some of their

businesses have historical data and some do not, however, the future cannot be ignored as share valuations are based on market expectations

and performance.

Projected Net Income: standard

valuation parameters allow for five years of projected net income with a terminal value discounting the net income values back to present

day using the internal rate of return (or IRR), WACC or a reasonable discount rate. Additionally, management can apply a reasonable growth

rate based on expected growth of each business, the economy and inflation measures.

Projected Cash Flow: standard

valuation parameters allow for five years of projected net income with a terminal value discounting the cash flow values back to present

day using the internal rate of return (or IRR), WACC or a reasonable discount rate. Additionally, management can apply a reasonable growth

rate based on expected growth of each business, the economy and inflation measures.

| 4) | Determine if Stock is Closely Held & Impact on Valuation: |

Based

on the July 31, 2019 Form 10-K the board of directors, officers and the founder of Ameri Metro own 67.15% of the outstanding shares4.

Based on this there are still 32.85% of shares held by projects and independent parties that negotiated transactions with the Company’s

management.

| 4 | See July 31, 2019 Form 10-K Page 170 Item 12 on www.sec.gov. |

The Company is expected to issue shares

to large financial institutions as direct sales and is expecting large purchases of these shares therefore based on this analysis the

Company is not closely held and is not expected to be closely held once it begins trading its shares. There should be no impact on the

valuation due to the shares held by insiders, directors and officers of the Company.

| 5) | The Nature of the Business and the History of the Enterprise from its Inception: |

The Company was incorporated in the

State of Delaware and merged with Ameri Metro 2010 on June 12, 2012. The Company, and its wholly owned subsidiary Global Transportation

and Infrastructure, Inc., plan to use Private Public Partnerships (“PPP”) for funding of infrastructure projects and transportation

projects. The Company is a conduit to provide general contracting services for infrastructure projects and transportation projects. As

a conduit we identify infrastructure projects for both private and public end users. The Company will bring together private and public

entities, the end users, including the affiliate entities to organize the revenue bond offering, which will be the private debt vehicle

to build the infrastructure project for the end user. The Company’s ultimate role is providing general contracting services and

construction management services for the private and public entities.

The Company initially intends to develop

a Midwest high-speed rail system for passengers and freight. Currently the Company is engaged in raising capital and entering into relationships

to further its planned activities. These initial planned activities are “ATFI Roadway” and “Port Trajan”, a northeast

freight corridor.

Since its incorporation, the Company

has developed its business plan, appointed officers and directors, engaged initial project consultants, and had meetings with certain

agencies and groups related to potential future projects. Presently, the Company has not physically started any of the projects disclosed

in our business plan section. However, as disclosed in the “Projects” section, the Company has entered into agreements

with related and non-related parties. The Company will start these projects once capital is raised. The Company’s business model

and proceeds raised from financings will allow the Company to begin the ATFI Roadway and Port Trajan project as well as other projects.

The Company Founder, Shah Mathias,

has organized and established three related non-profit corporations and is an independent consultant of a fourth non-profit (ATFI) for

the purpose of funding projects of the Company identified by Transportation Economics Management Systems (TEMS), TEMS, a transportation/rail/sea

vessel consulting firm working for and with the Company has completed preliminary studies on behalf of the end user both public and private.

The Company can introduce related and non-related entities to the four non-profit entities for the purpose of funding projects they have.

These are the 4 Non-Profit entities

with the ability to officiate Master Bond Indentures when sponsored by a state end user:

| 1. | Alabama Toll Facilities, Inc. (ATFI) (A Non-Related Party) |

| 2. | Hi Speed Rail Facilities, Inc. (HSRF)(A Related Party) |

| 3. | Hi Speed Rail Facilities Provider, Inc. (HSFP)(A Related Party) |

| 4. | Global Infrastructure Finance & Development Authority

(GIF&DA)(A Related Party) |

These three non–profit related

entities will play a vital role in financing. The non-profits statutes provide a vehicle to issue bonds and help secure infrastructure

potential projects. The non-profit entities have the discretion to turn over the infrastructure of potential projects to the state, or

the governing body after it has successfully developed and paid for the potential projects.

With the funding raised from financings,

the Company will then be able to consult the end users, related and non-related entities, and non-profits (who will sponsor bond offerings

to fund the projects) and to contract with one or more of the largest construction firms in the United States who will carry out the actual

construction management on the large projects we plan on building. The Company does not have the work force, or expertise to perform the

actual physical work from start to finish. However, the Company anticipates engaging the largest construction management and construction

firms in the industry, such as AECOM, to meet the project’s needs. AECOM, as noted in its filings with the SEC, has over thirty

years of experience undertaking similar projects and produced $20 billion in revenue in 2018. They operate with a capacity of 87,000 employees,

and provide planning, consulting, architectural, and engineering design services to commercial and governmental clients across 7 continents.

AECOM also offers construction services, including building construction and energy, infrastructure and industrial construction. In addition,

they can provide program and facility management which entails maintenance, training, logistics, consulting, technical assistance, systems

integration, and information technology services.

The Company anticipates these firms

will want to be involved due to the scale of each project the Company has under contract, and those potential projects the Company can

engage in as a result of their relationship with the non-profit entities.

The Company also believes the economic

studies performed by TEMS will confirm that the cost of the projects will be supported by the usage and revenues generated by the project.

This will allow the Company, and the associated construction firms contracted with, to sustain profit. The types of projects the Company

is proposing to build have generally been successful in the United States over the last 200 years and will attempt to improve the way

passengers and freight are transported around the United States.

On December 1, 2010, the Company

formed its wholly-owned subsidiary, Global Transportation & Infrastructure, Inc. (“GTI”). GTI was formed to provide

development and construction consulting services for Alabama Toll Facilities, Inc. “ATFI” is a non-related, non-profit

company supported by the State of Alabama, to act as the exclusive entity, as set forth in House Joint Resolutions, H.J.R 459 and

H.J.R. 456, to finance the development of the 357 mile Alabama Toll Road (starting on the coastline of Alabama and running northward

to the boarder of Tennessee).

Pursuant to the executed agreement with

ATFI, “Assignment Agreement For Construction,” GTI will act as the consultant for such a toll road, including implementation

of the financing mechanism for the design, planning, engineering and related costs for its construction, and to engage in the construction

of freight transportation and related transportation projects by contracting with some of the largest construction firms in the industry.

ATFI is a non-related entity, and along with other related entity projects that are supported by the ATFI 357 mile toll road in Alabama,

the Company intends to act as the conduit to bring the ATFI toll roadway to completion. The ATFI toll roadway and other related potential

projects stemming from the ATFI toll roadway project, are at different stages, of a six-stage process supported by agreements and contracts.

The Company has a six stage process

for potential future project opportunities:

| 1. | Management’s Decision to take on a project |

| 2. | Enter into Letters of Intent, Agreements, Construction Contracts |

| 3. | Obtain State(s) sponsorship of the project through legislative actions (where applicable) |

| 4. | Engineering and Design Studies, Architectural Design, Feasibility Studies |

| 5. | Raise Capital through Bond Financing and/or Company stock offerings or other borrowings |

| 6. | Management of the physical construction as a general contractor |

The Company’s current list of

potential project opportunities is contained in the Business Plan Section. The common thread with all these future opportunities is that

the Company has not yet started Stage 5 or Stage 6, but continues to spend time, effort, and resources to advance each project. Each project

requires the raising of capital, which we expect to be accomplished through one or more of the non-profit entities mentioned on the previous

page.

With the Alabama legislation Joint Resolution

HJR 459 and HJR 456 signed by the Governor, the ATFI project along with the ancillary projects are designed to support the sustainability

and to ensure the success of the ATFI project. The Company, pursuant to the construction agreements, is acting as Master General Contractor

for the building of the toll road. The Company will also build ancillary projects and related transportation systems, including but not

limited to rail and toll bridges, upon the successful issuance of the bond offering. The Company plans to improve port operations and

cargo facilities while building a 357 mile toll road from the coast of Alabama to the southern border of the State of Tennessee.

The contracts between ATFI and the Company

are in full force and effect under the House Joint Resolution HJR 459 and 456 unless new legislation is issued to rescind the current

HJR 459 and HJR 456. The related and non-related party contracts are in full force and effect in association with the projects.

The Company makes no guarantee we will

succeed in our business plan to help the United States by improving the infrastructure and changing the way cargo and the population travel,

but according to the United States Government it is a high priority to improve states’ infrastructure without taxing the American

public. The Company’s business model and ATFI legislative rights that are in place stand a reasonable chance of making a difference.

As Super Cargo ships increase in size, studies show that

the US ports do not have the sufficient water depth of fifty feet to berth these mega ships. The map below shows the Alabama Port which

ties to the ATFI toll road have the sufficient water depth of fifty feet. There are current studies taking place by US ports on how they

will solve the problem. The new challenge to US ports stems from the Panama Canal being widened and deepened to accommodate such ships.

Most US ports shown in the map below still lack the water depth to receive such ships substantiated by public reports found on the ASCE

American Society of Civil Engineers website under “Report Card For America’s Infrastructure”. The Panama Canal studies

below were completed by TEMS:

The

Company’s first project “Port Trajan” is directly connected to our current Alabama port potential project

“Port De Claudius, Inc.” through the new Alabama Toll Road (“ATFI”) connecting to Route 81 in Knoxville

Tennessee, which today is a major shipping corridor from Tennessee to Maine with South Central Pennsylvania (the location of Port

Trajan) becoming one of the current distribution locations for the north east. We believe that the ports of Mobile and Baltimore,

each with 50 feet of water depths, stand to be the ports used in making cargo movement to the north east corridor more efficient as

the size of cargo ships continues to increase. These ports, based on studies performed by TEMS, have the ability to be deepened and

the cost to do so will be offset by the economic impact they create according to studies performed to date by TEMS.

The Company’s funding plans include

stock offering and non-related and related parties officiating bond offerings to fund the projects identified.

The major elements of the infrastructure

for the projects as part of the Company’s planned activities are stated below:

Trade and Transportation Corridors

| ● | Development of container ports

for Class C, D and E ships |

| ● | Development of inland transportation

corridors including new greenfield highways and railroads |

| ● | Building of inland ports and

multimodal transportation centers |

| ● | Development of new urban centers

along the new infrastructure |

| ● | Development of ancillary facilities

including airport (express service), distribution centers, and logistics centers. |

High Speed Rail

| ● | Development of modern rail equipment

operating at speeds exceeding 250 mph |

| ● | Use rail to connect rural, small

urban and major metropolitan areas |

| ● | Track improvement, including

replacement and upgrades, additional sidings, signal and communications systems, and grade-crossing improvements |

| ● | Building of new greenfield routes |

| ● | Construction or improvement

of railroad grade crossings and passenger stations |

| ● | Acquiring new train equipment

including train sets and spares |

Transportation Infrastructure

Development of new road systems to

accommodate driverless cars and trucks, including electric cars and infrastructure to support the highway and rail systems that will be

used in Trade and Transportation Corridors and the High Speed Rail Systems.

Supporting Ancillary Development

| ● | Development or expansion of

a feeder bus system linking outlying areas to railroad stations |

| ● | Operation of a “hub-and-spoke”

passenger rail system providing service to and through one or more major hubs to locations throughout the United States |

| ● | Provision of multi-modal connections

to improve system access, hotels, retail, parking garages, sorting facilities / distribution facilities |

Supporting Transportation Systems

Ancillary development opportunities, airports, inland ports,

sea ports, toll roads and technology parks

As the US and World populations are

rapidly increasing, infrastructure is becoming inadequate and dilapidated as stated on the American Society of Civil Engineers website.

Government authorities are unable to keep up with preventative maintenance and replacement work because of the lack of funding. Studies

have consistently shown that the development of infrastructure promotes economic growth. However, the global financial crises have sent

governments into restructuring their budgets and reduced the possibility for funding new infrastructure development.

The Company’s management team

has recognized the need for a solution to limit the financial burden on governments and taxpayers alike. The Company plans to use Private

Public Partnerships to fund some or all of the capital requirements for the project opportunities. The Company’s use of proceeds

from the offering will potentially make it possible for the Company to fulfill its consulting agreements with ATFI and Related Parties

to begin immediately the feasibility studies and investment grade studies needed to officiate the bond offerings, specifically for the

“Port Trajan” project as detailed in the “project” section.

Once TEMS completes feasibility and

environmental studies, it will be the Company’s goal, through the financial markets to raise capital from bond offerings.

In

order to support the functionality of financial structure between the end user, whether public or private, and the non-profit,

whether related or non-related, Shah Mathias created the sixteen related entities listed below of which the Company owns 25% of each

via non-voting common shares, with the remaining 75% (and 100% voting control) owned by Mr. Mathias. The Company acting in its

Master Consulting role will be the conduit between one or more of the related entities who will secure by contract the project from

the end user and approach the non-profits for bond offering of the project. The construction management services will be performed

by one or more of the largest construction management firms in the United States by utilizing existing well-established construction

firms in or near the project location to perform the physical work on each project. The Company’s consulting staffing needs

are already in place and any additional needs can be met easily. Once a project is started, the consulting management team of the

Company would rely heavily on the work force of some of the largest construction management firms in the country. The seventeenth

related entity, HSRF Trust, was created to place the bond offering revenue in trust managed by agreements with ING (now Voya).

| 2. | HSR Passenger Services, Inc. |

| 5. | KSJM International Airport, Inc. |

| 7. | Port of De Claudius, Inc. |

| 8. | Atlantic Energy & Utility Products, Inc. |

| 12. | Penn Insurance Services LLC |

| 14. | Eastern Development & Design, Inc. |

| 17. | Ann Charles International Airport, Inc. |

| 18. | Dutch East India Logistics Co. |

| 19. | Natural Resources, LLC |

| 20. | Susquehanna Mortgage Bankers |

Presently, none of these related

entities recognized any revenue. These entities play a vital role in terms of becoming the entity that builds and owns the potential

project while the bond debt is being paid back. The ultimate beneficial owner of the project could be one of these entities or in the

case of State projects, the State would become the beneficial owner of the project built once the bond debt is retired. This business

model will control cost over runs and allow for more tightly managed projects during construction and then management of the operations

of the project until the debt is paid back.

In summary and for clear understanding

of the process:

The State who has a project to build

would be able to have the project built by sponsoring the bond offering on behalf of one of the related entities below. The related entities

would build and manage the project, assume the liability of the debt and then return the project back to the State upon retirement of

the bond debt. In the case of non-State projects, the related entity could be the beneficial owner of the project at the end of the bond

debt retirement.

1) HSR

Freight line, Inc. This company will handle all services related to the use of track time, train sets leases and freight forwarding

services. HSR Freight Line, Inc. intends to offer high speed rail, freight forwarding and parcel handling services to existing national

and global carriers. As opposed to independently developing a freight corridor, carriers will be able to lease train sets with their trade

logos and slogans in their own color schemes at various rates depending on the time frames, in addition to toll fees for track time. The

Company interfaces with the entity in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as

consultant for construction services for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in

post construction operations revenue.

2) HSR

Passenger Services, Inc. This company will handle all ticketing, booking, reservations, food & beverage services, hotel booking

and car rental booking services. HSR Passenger Service Inc. will offer concession space at the travel plazas, technology parks and develop

motels, hotels, fast food restaurant establishments and convenience stores. The Company interfaces with the entity in three separate stages:

Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction services for a fee and Stage 3 interface

– as a 25% non-controlling interest shareholder, sharing in post construction operations revenue.

3) HSR

Technologies, Inc. This company will handle all build to suit manufacturing facilities for train sets and centralized signalization

services along the rail road tracks and train stations. Within the technology parks HSR Technologies, Inc. will be a sole provider of

all fiber optics, telecommunication and all related technologies services including equipment maintenance.

A. Maintenance

for train engines, rail cars and rail track through a maintenance agreement with equipment lease holders.

B. Total

maintenance for all Industrial sites for assembly plants, train stations, train terminals, manufacturing plants, parts distribution centers,

rail roads, rail crossings, rail yards, cargo terminals, parking lot, parking garages, hotel, motels, food and beverage vending machines,

all retail shopping centers, office complexes and all on/off site improvements.

C. The

airline industry is congested throughout existing terminal space. The proposed KSJM International Airport in Alabama will offer services

to eliminate burden on existing terminal space for airline carriers. Federal Aviation Administration (FAA) certified inspection stations

will service the airline industry. This company will also provide marine services, oil platforms and petro chemical industry services

due to proximity to the Gulf of Mexico.

The Company interfaces with the entity,

in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction services

for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in post construction operations revenue.

4) HSR

Logistics, Inc. This company will handle coordination, delivery and movement of all machinery equipment, material goods and will operate

all warehousing facilities.

The Company interfaces with the entity

in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction services

for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in post construction operations revenue.

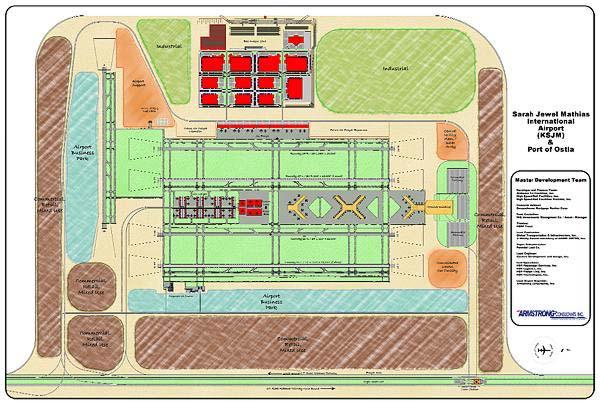

5) KSJM

International Airport, Inc. This company formed to serve as a master airport facility. It will provide four types of airport terminals

and one international airline inspection service terminal operated by HSR Technologies Inc.:

| a) | Passenger Terminals, operated by HSR Passenger Services Inc. |

| b) | Air Cargo Terminals, operated by Port of Ostia, Inc. |

| c) | Corporate Jet Center Terminal |

| d) | International Airline, FAA inspections maintenance service

terminals, operated by KSJM International Airport, Inc. |

| e) | Domestic Airline FAA inspection maintenance service terminals,

operated by HSR Technologies Inc. |

The Company interfaces with the entity

in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction services

for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in post construction operations revenue.

6) Port

of Ostia, Inc. This company will handle foreign and domestic Air Cargo, and while supporting ground services such as freight forwarding

services will be provided by HSR Freight Line, Inc. and air and ground logistics will be provided by HSR Logistics, Inc. The Company interfaces

with the entity in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction

services for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in post construction operations

revenue.

7) Port

of De Claudius, Inc. This company will handle foreign and domestic inbound / outbound sea container inland port operation and warehouse

distribution center. The Company interfaces with the entity in three separate stages: Stage 1 interface - as consultant for a fee, Stage

2 interface – as consultant for construction services for a fee and Stage 3 interface – as a 25% non-controlling interest

shareholder, sharing in post construction operations revenue.

8) Atlantic

Energy & Utility Products, Inc. This company will provide electric, gas, water, sanitary sewer service, trash removal, cable TV,

Dish network and internet services.

Petroleum

products and services will also be provided during and after construction, along with fuel services on the toll road, all industrial

and technology parks, including the airport, inland ports and incoming and outgoing vessels. The Company interfaces with the entity

in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction

services for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder, sharing in post construction

operations revenue.

9) Malibu

Homes, Inc. This company will provide residential home building services. The Company interfaces with the entity, in three separate

stages: Stage 1 interface - as consultant for a fee, Stage 2 interface – as consultant for construction services for a fee and Stage

3 interface – as a 25% non-controlling interest shareholder, sharing in post construction operations revenue.

10) Ameri

Cement, Inc. This company handles all cement needs for building (357 miles four lane) Alabama Toll Road “ATFl” and others

future projects. The Company interfaces with the entity in three separate stages: Stage 1 interface - as consultant for a fee, Stage 2

interface – as consultant for construction services for a fee and Stage 3 interface – as a 25% non-controlling interest shareholder,

sharing in post construction operations revenue.

11) Lord

Chauffeurs LID. This company operates all passenger ground transportation car service for passengers such as limo and taxi, as well

as the corporate jet center. The Company interfaces with the entity in three separate stages: Stage 1 interface - as consultant for a