false 0001464423 0001464423 2025-01-30 2025-01-30 0001464423 us-gaap:CommonStockMember 2025-01-30 2025-01-30 0001464423 us-gaap:SeriesAPreferredStockMember 2025-01-30 2025-01-30 0001464423 us-gaap:SeriesBPreferredStockMember 2025-01-30 2025-01-30 0001464423 us-gaap:SeriesCPreferredStockMember 2025-01-30 2025-01-30 0001464423 us-gaap:SeniorNotesMember 2025-01-30 2025-01-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): January 30, 2025

PennyMac Mortgage Investment Trust

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| Maryland |

|

001-34416 |

|

27-0186273 |

| (State or other jurisdiction of incorporation) |

|

(Commission File Number) |

|

(IRS Employer Identification No.) |

|

|

|

|

|

| 3043 Townsgate Road, Westlake Village, California |

|

91361 |

| (Address of principal executive offices) |

|

(Zip Code) |

(818) 224-7442

(Registrant’s telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☐ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

| Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

| Common Shares of Beneficial Interest, $0.01 par value |

|

PMT |

|

New York Stock Exchange |

| 8.125% Series A Cumulative Redeemable Preferred Shares of Beneficial Interest, $0.01 par value |

|

PMT/PA |

|

New York Stock Exchange |

| 8.00% Series B Cumulative Redeemable Preferred Shares of Beneficial Interest, $0.01 par value |

|

PMT/PB |

|

New York Stock Exchange |

| 6.75% Series C Cumulative Redeemable Preferred Shares of Beneficial Interest, $0.01 par value |

|

PMT/PC |

|

New York Stock Exchange |

| 8.50% Senior Note Due 2028 |

|

PMTU |

|

New York Stock Exchange |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 2.02 |

Results of Operations and Financial Condition. |

On January 30, 2025, PennyMac Mortgage Investment Trust (the “Company”) issued a press release announcing its financial results for the fiscal quarter and year ended December 31, 2024. A copy of the press release and the slide presentation used in connection with the Company’s presentation of financial results were made available on January 30, 2025 and are furnished as Exhibits 99.1 and Exhibit 99.2, respectively. In addition, the Company has made available other supplemental financial information for the fiscal quarter and year ended December 31, 2024 on its website at pmt.pennymac.com.

The information in Item 2.02 of this report, including the exhibits hereto, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, or otherwise subject to the liabilities of Section 18, nor shall it be deemed incorporated by reference into any disclosure document relating to the Company, except to the extent, if any, expressly set forth by specific reference in such filing.

| Item 9.01 |

Financial Statements and Exhibits. |

(d) Exhibits.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

|

|

|

|

|

|

|

|

|

|

|

|

|

PENNYMAC MORTGAGE INVESTMENT TRUST |

|

|

|

|

| Dated: January 30, 2025 |

|

|

|

|

|

/s/ Daniel S. Perotti |

|

|

|

|

|

|

Daniel S. Perotti Senior Managing Director and Chief Financial Officer |

Exhibit 99.1

PennyMac Mortgage Investment Trust Reports

Fourth Quarter and Full-Year 2024 Results

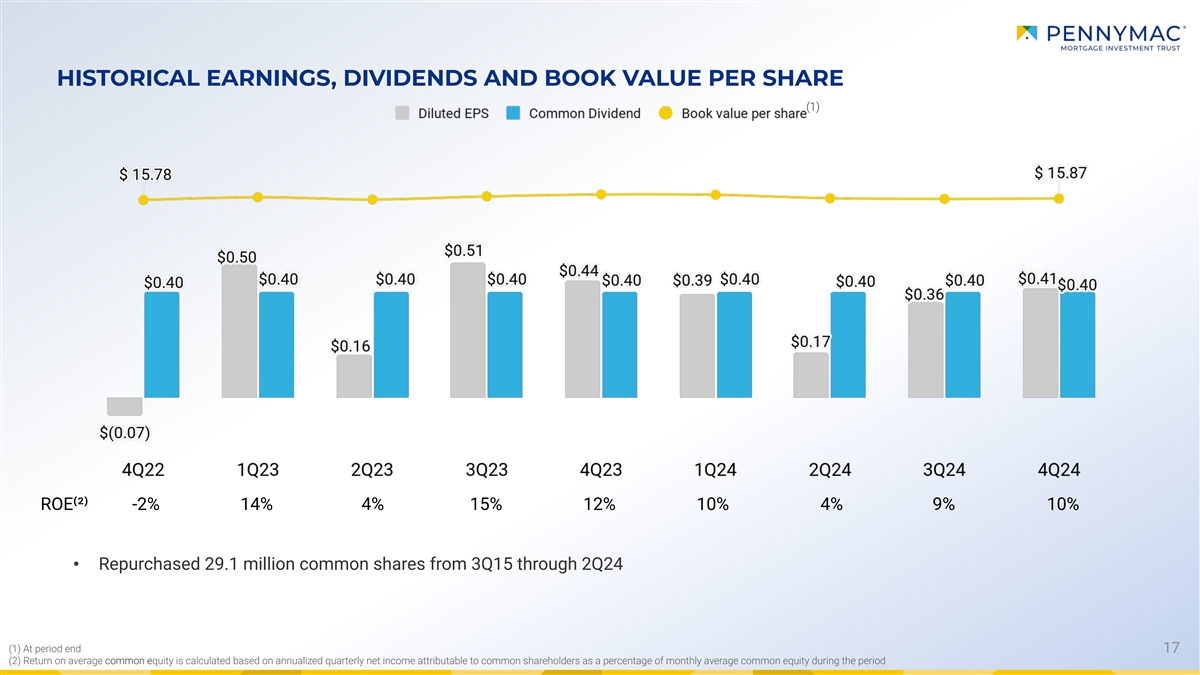

WESTLAKE VILLAGE, Calif. – January 30, 2025 – PennyMac Mortgage Investment Trust (NYSE: PMT) today reported net income

attributable to common shareholders of $36.1 million, or $0.41 per common share on a diluted basis for the fourth quarter of 2024, on net investment income of $107.9 million. PMT previously announced a cash dividend for the fourth quarter

of 2024 of $0.40 per common share of beneficial interest, which was declared on December 13, 2024, and paid on January 24, 2025, to common shareholders of record as of December 27, 2024.

Fourth Quarter 2024 Highlights

Financial results:

| |

• |

|

Net income attributable to common shareholders of $36.1 million; annualized return on average common equity

of 10%1 |

| |

• |

|

Results driven by strong levels of income excluding market driven value changes |

| |

• |

|

Book value per common share increased to $15.87 at December 31, 2024, from $15.85 at September 30, 2024

|

Other investment highlights:

| |

• |

|

Investment activity driven by correspondent production volumes |

| |

• |

|

Correspondent loan production volumes for PMT’s account totaled $3.5 billion in unpaid principal

balance (UPB), down 41 percent from the prior quarter as a result of the sale of a large percentage of conventional loans to PennyMac Financial Services, Inc. (NYSE: PFSI), and up 41 percent from the fourth quarter of 2023 as a result of

higher overall volumes |

| |

• |

|

Resulted in the creation of $60 million in new mortgage servicing rights (MSRs) |

| 1 |

Return on average common equity is calculated based on net income attributable to common shareholders as a

percentage of monthly average common equity during the quarter |

1

| |

• |

|

Closed two Agency-eligible investor loan securitizations with combined UPB of $822 million

|

| |

• |

|

Generated $52 million of net new investments in non-Agency

subordinate bonds |

Other highlights:

| |

• |

|

Renewed management and services agreement with PFSI for five years |

Notable activity after quarter end

| |

• |

|

Closed an additional Agency eligible investor loan securitization with UPB of $341 million

|

| |

• |

|

Generated $21 million of net new investments in non-Agency

subordinate bonds |

Full-Year 2024 Highlights

Financial results:

| |

• |

|

Net income of $161.0 million, versus $199.7 million in 2023 |

| |

• |

|

Net income attributable to common shareholders of $119.2 million, versus $157.8 million in 2023;

diluted earnings per share of $1.37 versus $1.63 in 2023 |

| |

• |

|

Dividends of $1.60 per common share |

| |

• |

|

Book value per share decreased slightly from $16.13 to $15.87 |

| |

• |

|

Net investment income of $334.2 million, down from $429.0 million in 2023 |

| |

• |

|

Return on average common equity of 8%2

|

| |

• |

|

Issued $1.3 billion in term debt to address or refinance upcoming maturities |

| 2 |

Return on average common equity is calculated based on net income attributable to common shareholders as a

percentage of monthly average common equity during the year |

2

“PMT produced strong results in the fourth quarter with a 10 percent annualized return on equity

primarily driven by strong levels of income excluding market driven value changes and excellent performance across all three investment strategies,” said Chairman and CEO David Spector. “Importantly, the fourth quarter marked a return to

organic creation of credit investments as we leveraged the strength of our correspondent production and securitization expertise to complete two securitizations of Agency-eligible investor loans and retained $52 million of net new credit

subordinate bond investments. With a growing pipeline of loans available for private label securitization and strong investor demand, we expect similar levels of activity well into 2025, with the potential for increased activity and securitizations

of other loan products as the origination market grows.”

Mr. Spector concluded, “While I am pleased with PMT’s performance in 2024, I

am even more excited by the opportunity ahead. Given our expectations for PMT to be a consistent issuer and investor in private label securitizations alongside its seasoned portfolio of MSRs and CRT with strong underlying fundamentals, I am

confident the company will continue to deliver attractive risk-adjusted returns in 2025 and beyond.”

3

The following table presents the contributions of PMT’s operating segments, consisting of Credit

Sensitive Strategies, Interest Rate Sensitive Strategies, and Correspondent Production, as well as non-segment activities in our corporate operations:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Quarter ended December 31, 2024 |

|

Credit sensitive

strategies |

|

|

Interest rate sensitive

strategies |

|

|

Correspondent

production |

|

|

Reportable

segment total |

|

|

Corporate |

|

|

Total |

|

| |

|

(in thousands) |

|

| Net investment income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net loan servicing fees |

|

$ |

— |

|

|

$ |

207,421 |

|

|

$ |

— |

|

|

$ |

207,421 |

|

|

$ |

— |

|

|

$ |

207,421 |

|

| Net gains on loans acquired for sale |

|

|

— |

|

|

|

— |

|

|

|

26,387 |

|

|

|

26,387 |

|

|

|

— |

|

|

|

26,387 |

|

| Net gains (losses) on investments and financings |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Mortgage-backed securities |

|

|

(292 |

) |

|

|

(130,856 |

) |

|

|

— |

|

|

|

(131,148 |

) |

|

|

— |

|

|

|

(131,148 |

) |

| Loans at fair value |

|

|

(4,016 |

) |

|

|

4,957 |

|

|

|

— |

|

|

|

941 |

|

|

|

— |

|

|

|

941 |

|

| CRT investments |

|

|

24,552 |

|

|

|

— |

|

|

|

— |

|

|

|

24,552 |

|

|

|

— |

|

|

|

24,552 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20,244 |

|

|

|

(125,899 |

) |

|

|

— |

|

|

|

(105,655 |

) |

|

|

— |

|

|

|

(105,655 |

) |

| Net interest income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest income |

|

|

21,114 |

|

|

|

106,117 |

|

|

|

32,478 |

|

|

|

159,709 |

|

|

|

3,426 |

|

|

|

163,135 |

|

| Interest expense |

|

|

20,679 |

|

|

|

135,733 |

|

|

|

29,531 |

|

|

|

185,943 |

|

|

|

1,177 |

|

|

|

187,120 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

435 |

|

|

|

(29,616 |

) |

|

|

2,947 |

|

|

|

(26,234 |

) |

|

|

2,249 |

|

|

|

(23,985 |

) |

| Other |

|

|

(282 |

) |

|

|

— |

|

|

|

4,041 |

|

|

|

3,759 |

|

|

|

— |

|

|

|

3,759 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20,397 |

|

|

|

51,906 |

|

|

|

33,375 |

|

|

|

105,678 |

|

|

|

2,249 |

|

|

|

107,927 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earned by PennyMac Financial Services, Inc.: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loan servicing fees |

|

|

19 |

|

|

|

20,467 |

|

|

|

— |

|

|

|

20,486 |

|

|

|

— |

|

|

|

20,486 |

|

| Management fees |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

7,149 |

|

|

|

7,149 |

|

| Loan fulfillment fees |

|

|

— |

|

|

|

— |

|

|

|

6,356 |

|

|

|

6,356 |

|

|

|

— |

|

|

|

6,356 |

|

| Professional Services |

|

|

— |

|

|

|

— |

|

|

|

3,508 |

|

|

|

3,508 |

|

|

|

2,533 |

|

|

|

6,041 |

|

| Loan Collection and Liquidation |

|

|

281 |

|

|

|

2,256 |

|

|

|

— |

|

|

|

2,537 |

|

|

|

— |

|

|

|

2,537 |

|

| Compensation |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

997 |

|

|

|

997 |

|

| Safekeeping |

|

|

— |

|

|

|

1,252 |

|

|

|

84 |

|

|

|

1,336 |

|

|

|

— |

|

|

|

1,336 |

|

| Mortgage Loan Origination Fees |

|

|

— |

|

|

|

— |

|

|

|

914 |

|

|

|

914 |

|

|

|

— |

|

|

|

914 |

|

| Other Expenses |

|

|

— |

|

|

|

2,464 |

|

|

|

— |

|

|

|

2,464 |

|

|

|

4,523 |

|

|

|

6,987 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

300 |

|

|

|

26,439 |

|

|

|

10,862 |

|

|

|

37,601 |

|

|

|

15,202 |

|

|

|

52,803 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pretax income (loss) |

|

$ |

20,097 |

|

|

$ |

25,467 |

|

|

$ |

22,513 |

|

|

$ |

68,077 |

|

|

$ |

(12,953 |

) |

|

$ |

55,124 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

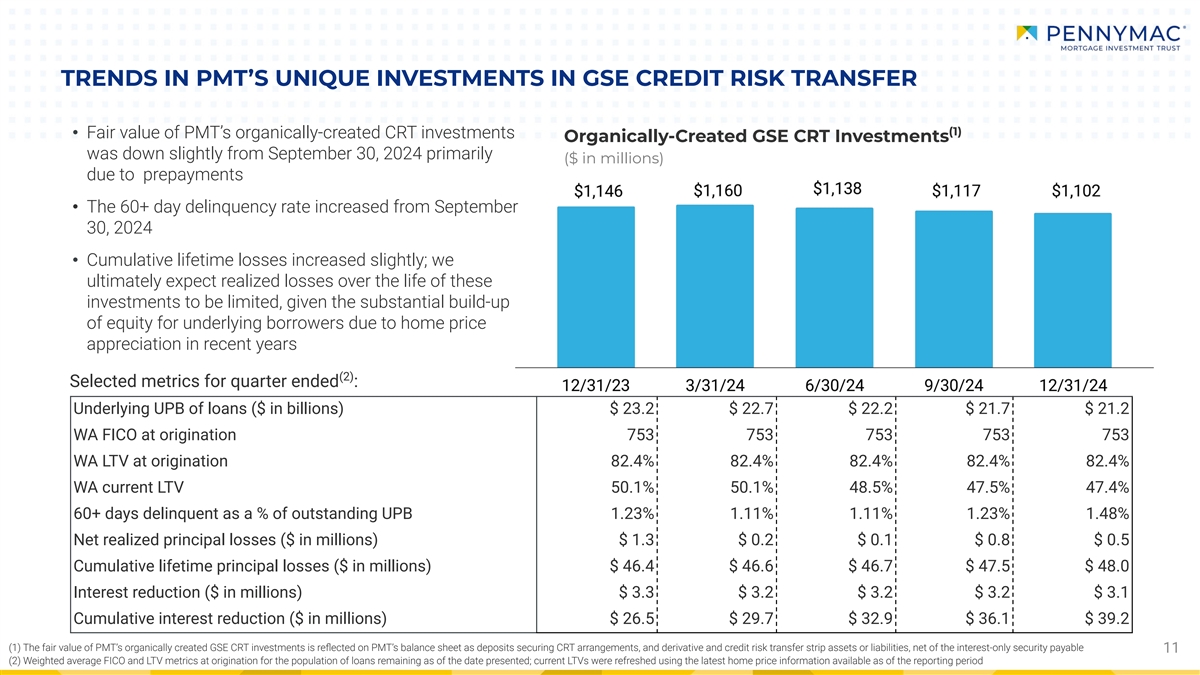

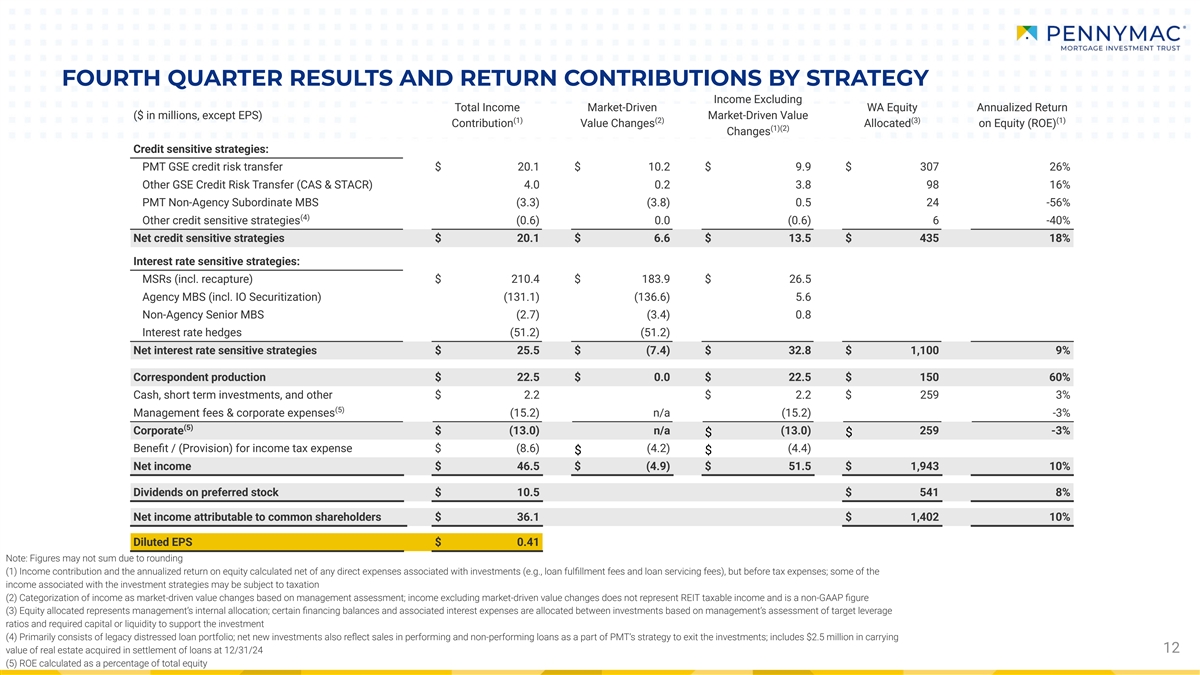

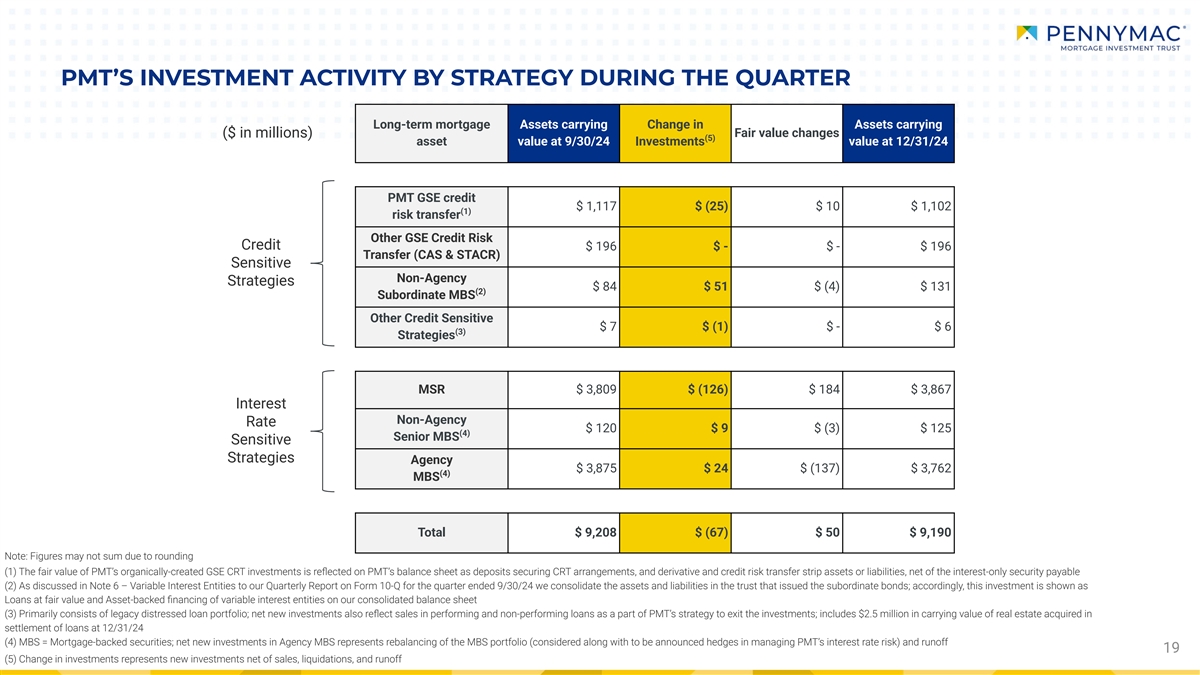

Credit Sensitive Strategies Segment

The Credit Sensitive Strategies segment primarily includes results from PMT’s organically-created GSE CRT investments, opportunistic investments in other

GSE CRT, investments in non-agency subordinate bonds from private-label securitizations of PMT’s production and legacy investments. Pretax income for the segment was $20.1 million on net investment

income of $20.4 million, compared to pretax income of $26.4 million on net investment income of $26.5 million in the prior quarter.

Net

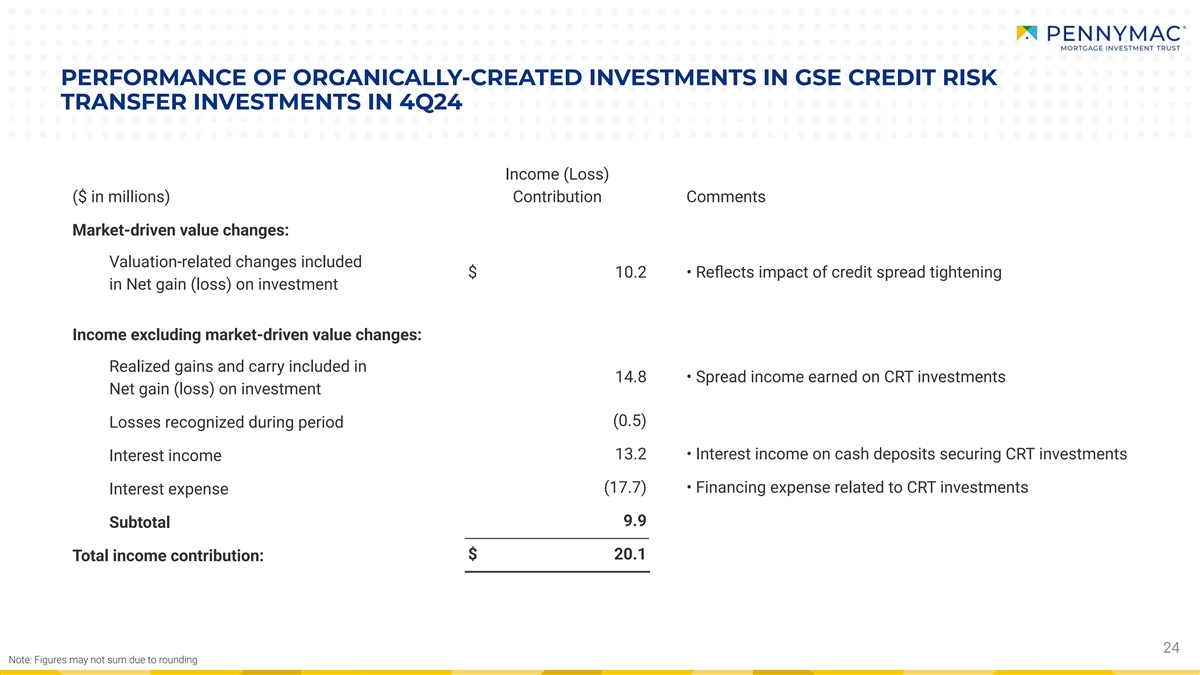

gains on investments in the segment were $20.2 million, compared to $27.1 million in the prior quarter. These net gains include $24.6 million of gains on PMT’s organically-created GSE CRT investments, $0.3 million in losses

on other acquired subordinate CRT mortgage-backed securities (MBS), and $4.0 million of losses on investments from non-agency subordinate bonds from PMT’s production.

4

Net gains on PMT’s organically-created CRT investments for the quarter were $24.6 million,

compared to $20.8 million in the prior quarter. These net gains include $10.2 million in valuation-related gains, which reflected the impact of credit spread tightening in the fourth quarter. The prior quarter included $6.6 million of

such gains. Net gains on PMT’s organically-created CRT investments also included $14.8 million in realized gains and carry, compared to $15.0 million in the prior quarter. Realized losses during the quarter were $0.5 million.

Net interest income for the segment totaled $0.4 million, compared to $0.5 million of net interest expense in the prior quarter. Interest

income totaled $21.1 million, down slightly from $21.4 million in the prior quarter. Interest expense totaled $20.7 million, down from $21.9 million in the prior quarter.

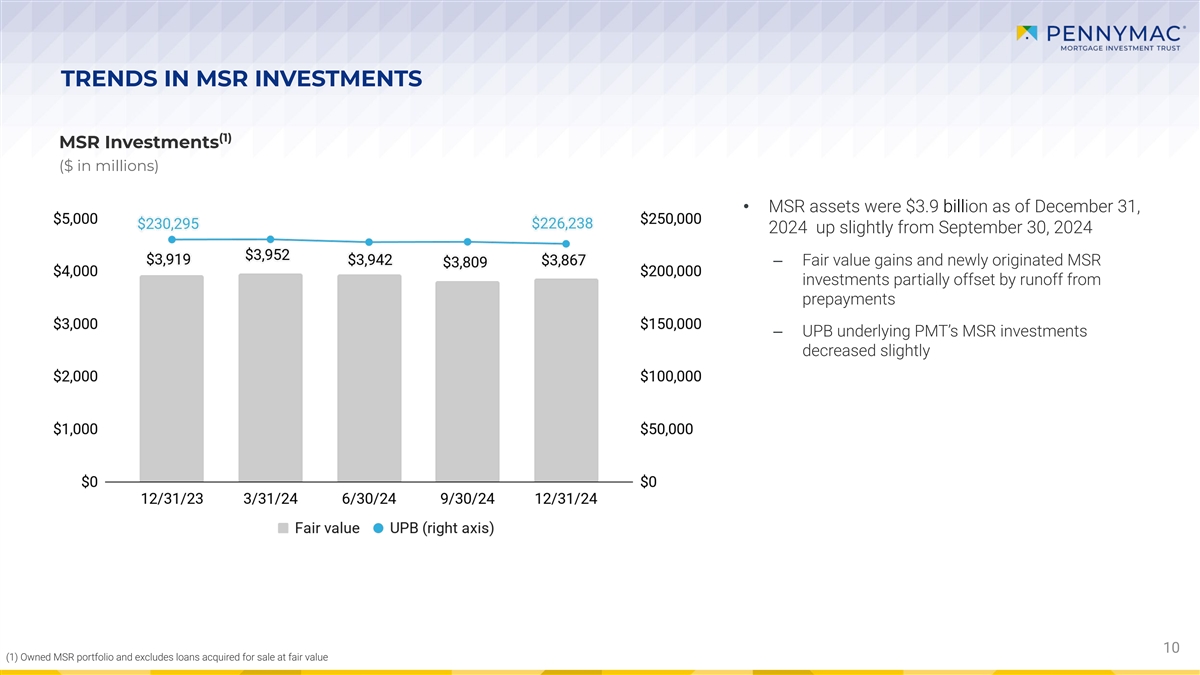

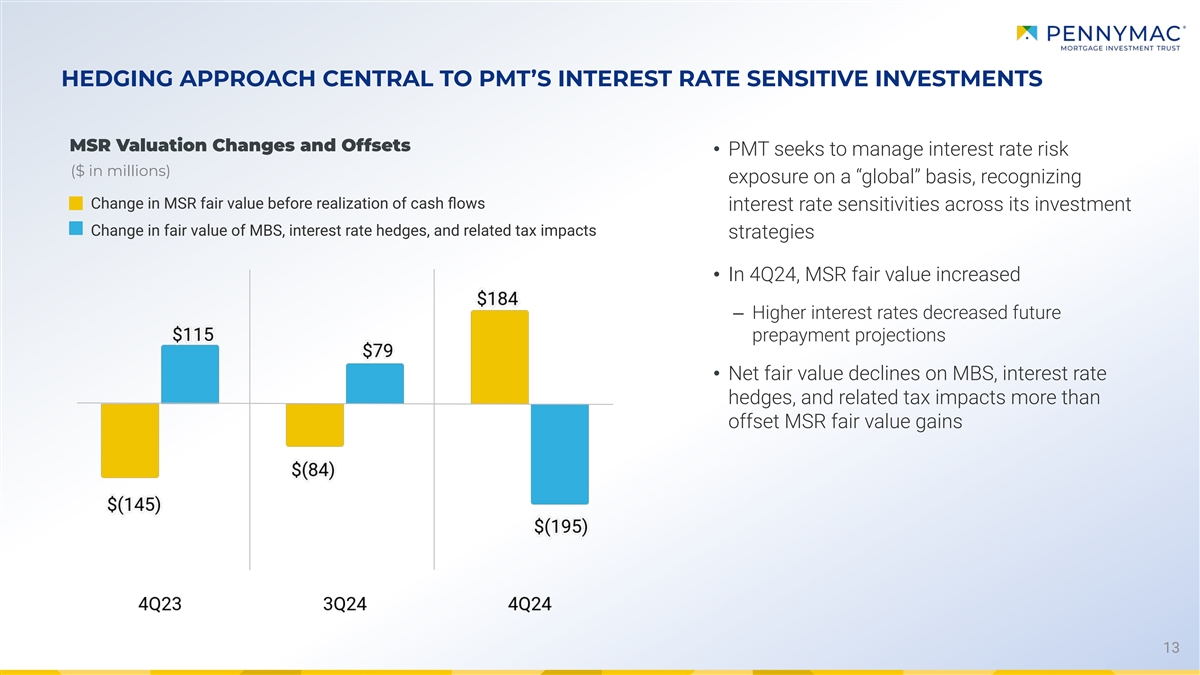

Interest Rate Sensitive Strategies Segment

The Interest

Rate Sensitive Strategies segment includes results from investments in MSRs, Agency MBS, non-Agency senior MBS and interest rate hedges. Pretax income for the segment was $25.5 million on net investment

income of $51.9 million, compared to pretax income of $0.5 million on net investment income of $26.1 million in the prior quarter. The segment includes investments that typically have offsetting fair value exposures to changes in

interest rates. For example, in a period with increasing interest rates, MSRs are expected to increase in fair value, whereas Agency pass-through and non-Agency senior MBS are expected to decrease in fair

value.

The results in the Interest Rate Sensitive Strategies segment consist of net gains and losses on investments, net interest income and net loan

servicing fees, as well as associated expenses.

Income from net loan servicing fees was $207.4 million, compared to losses of $85.1 million in

the prior quarter. Net loan servicing fees included contractually specified servicing fees of $159.6 million and $4.9 million in other fees, reduced by $90.6 million in realization of MSR cash flows, which was down from

$100.6 million in the prior quarter due to higher interest rates during the quarter. Net loan servicing fees also included $183.9 million in fair value gains on MSRs due to higher interest rates, $51.2 million in hedging losses, and

$0.9 million of MSR recapture income. PMT’s hedging activities are intended to manage its net exposure across all interest rate sensitive strategies, which include MSRs, MBS and related tax impacts.

5

Net losses on investments for the segment were $125.9 million, which primarily consisted of losses on

MBS due to higher interest rates.

The following schedule details net loan servicing fees:

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Quarter ended |

|

| |

|

December 31, 2024 |

|

|

September 30, 2024 |

|

|

December 31, 2023 |

|

| |

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

(in thousands) |

|

|

|

|

| From non-affiliates: |

|

|

|

|

|

|

|

|

|

|

|

|

| Contractually specified |

|

$ |

159,553 |

|

|

$ |

162,605 |

|

|

$ |

162,916 |

|

| Other fees |

|

|

4,884 |

|

|

|

4,012 |

|

|

|

2,487 |

|

| Effect of MSRs: |

|

|

|

|

|

|

|

|

|

|

|

|

| Change in fair value |

|

|

|

|

|

|

|

|

|

|

|

|

| Realization of cashflows |

|

|

(90,612 |

) |

|

|

(100,612 |

) |

|

|

(87,729 |

) |

| Market changes |

|

|

183,879 |

|

|

|

(84,306 |

) |

|

|

(144,603 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

93,267 |

|

|

|

(184,918 |

) |

|

|

(232,332 |

) |

| Hedging results |

|

|

(51,209 |

) |

|

|

(67,220 |

) |

|

|

(11,191 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

42,058 |

|

|

|

(252,138 |

) |

|

|

(243,523 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net servicing fees from non-affiliates |

|

|

206,495 |

|

|

|

(85,521 |

) |

|

|

(78,120 |

) |

| From PFSI—MSR recapture income |

|

|

926 |

|

|

|

441 |

|

|

|

290 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net loan servicing fees |

|

$ |

207,421 |

|

|

$ |

(85,080 |

) |

|

$ |

(77,830 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest expense for the segment was $29.6 million versus $8.4 million in the prior quarter. Interest income

totaled $106.1 million, down from $128.5 million in the prior quarter primarily due to lower interest income on MBS and earnings on custodial balances. Interest expense totaled $135.7 million, down slightly from $136.9 million in

the prior quarter.

Segment expenses were $26.4 million, up slightly from $25.6 million in the prior quarter.

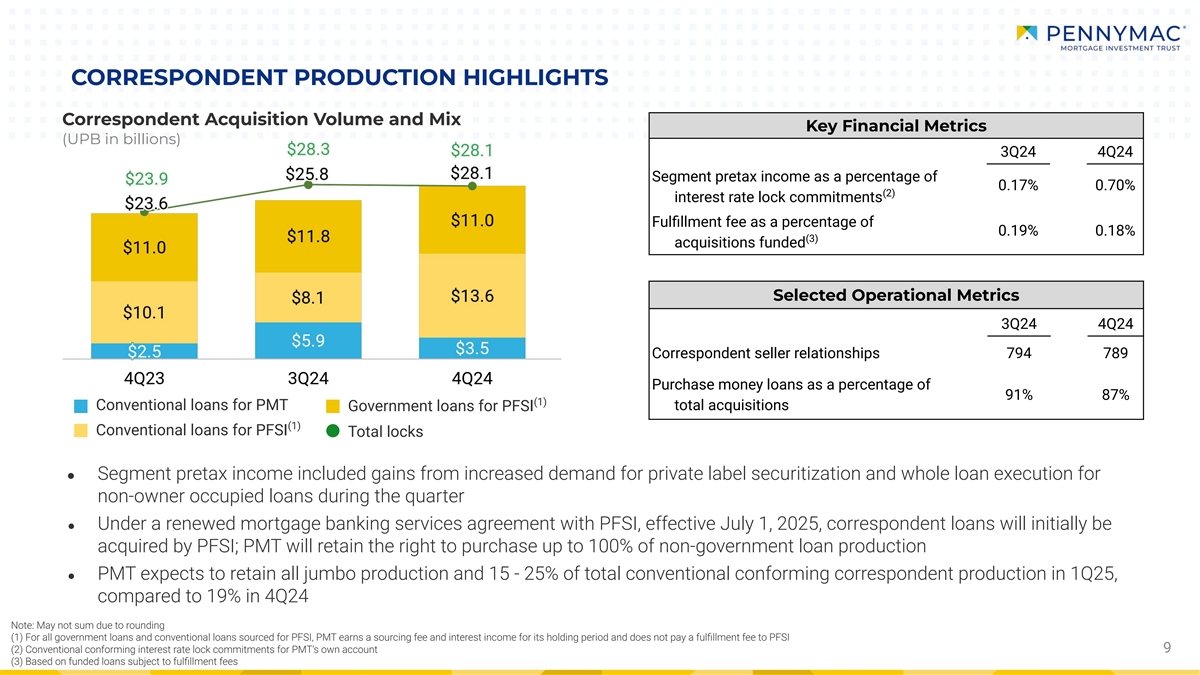

Correspondent Production Segment

PMT acquires newly

originated loans from correspondent sellers and typically sells or securitizes the loans, resulting in current-period income and additions to its investments in MSRs related to a portion of its production. PMT’s Correspondent Production segment

generated pretax income of $22.5 million in the fourth quarter, up from $13.2 million in the prior quarter.

6

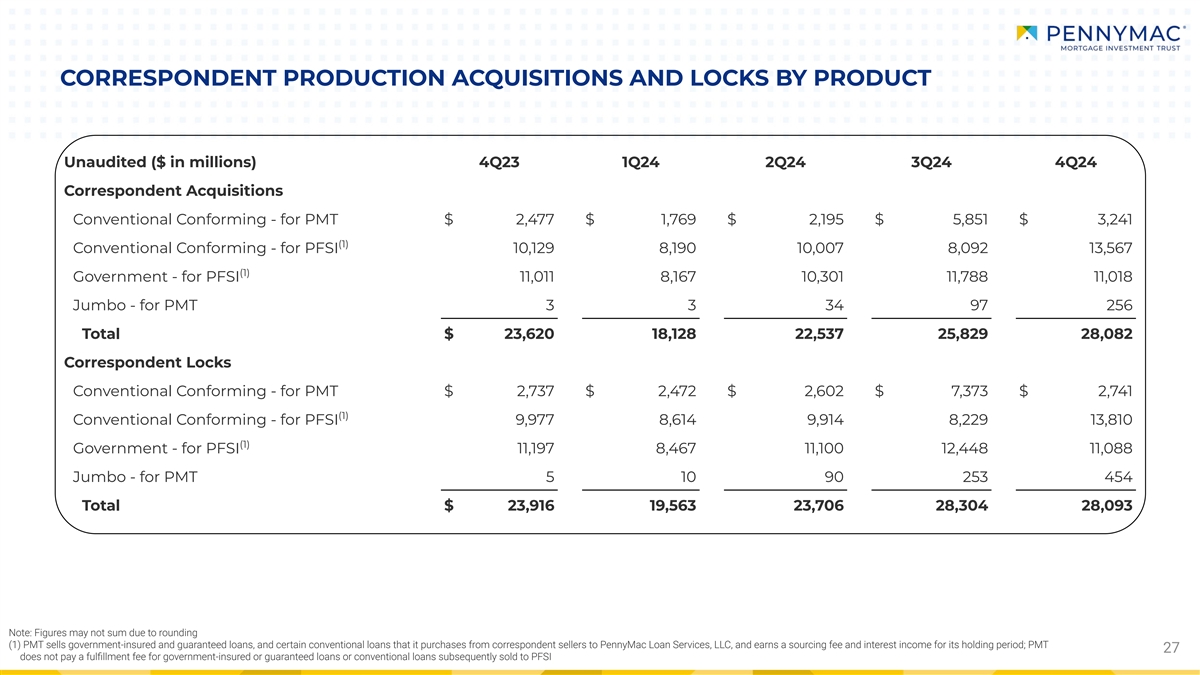

Through its correspondent production activities in the fourth quarter, PMT acquired a total of

$28.1 billion in UPB of loans, up 9 percent from the prior quarter and 19 percent from the fourth quarter of 2023. Of total correspondent acquisitions, government-insured or guaranteed acquisitions totaled $11.0 billion, down

7 percent from the prior quarter, while conventional conforming and jumbo acquisitions totaled $17.1 billion, up 22 percent from the prior quarter. $3.5 billion of conventional conforming and jumbo volume was for PMT’s

account, down 41 percent from the prior quarter due to PMT retaining a smaller percentage of conventional conforming correspondent loan production. PMT is expected to retain all jumbo production and 15 to 25 percent of total conventional

conforming correspondent production in the first quarter of 2025, compared to 19 percent in the fourth quarter of 2024, as PMT continues to pursue investment opportunities in the private label securitization market. Interest rate lock

commitments on conventional conforming and jumbo loans for PMT’s account totaled $3.2 billion, down 58 percent from the prior quarter.

Segment revenues were $33.4 million and included net gains on loans acquired for sale of $26.4 million, other income of $4.0 million, which

primarily consists of volume-based origination fees, and net interest income of $2.9 million. Net gains on loans acquired for sale increased $6.3 million from the prior quarter, primarily due to increased demand for private label

securitization and whole loan execution for investor loans during the quarter. Interest income was $32.5 million, up from $23.9 million in the prior quarter, and interest expense was $29.5 million, up from $24.3 million in the

prior quarter, both due to higher inventory of loans held for sale at fair value.

Segment expenses were $10.9 million, down from $13.1 million

in the prior quarter. The weighted average fulfillment fee rate in the fourth quarter was 18 basis points, down from 19 basis points in the prior quarter.

Under a renewed mortgage banking services agreement with PFSI, effective July 1, 2025, correspondent production volumes will initially be acquired by

PFSI. PMT will retain the right to purchase up to 100 percent of non-government correspondent loan production.

Corporate

Corporate includes interest income from cash

and short-term investments, management fees, and corporate expenses.

7

Corporate revenues were $2.3 million, up from $1.9 million in the prior quarter. Management fees

were $7.1 million, and other expenses were $4.5 million.

Taxes

PMT recorded a provision for tax expense of $8.6 million, driven by income from correspondent production and gains on MSRs held in PMT’s taxable REIT

subsidiary.

***

Management’s slide

presentation and accompanying materials will be available in the Investor Relations section of the Company’s website at pmt.pennymac.com after the market closes on Thursday, January 30, 2025. Management will also host a conference

call and live audio webcast at 6:00 p.m. Eastern Time to review the Company’s financial results. The webcast can be accessed at pmt.pennymac.com, and a replay will be available shortly after its conclusion.

Individuals who are unable to access the website but would like to receive a copy of the materials should contact the Company’s Investor Relations

department at 818.224.7028.

About PennyMac Mortgage Investment Trust

PennyMac Mortgage Investment Trust is a mortgage real estate investment trust (REIT) that invests primarily in residential mortgage loans and mortgage-related

assets. PMT is externally managed by PNMAC Capital Management, LLC, a wholly-owned subsidiary of PennyMac Financial Services, Inc. (NYSE: PFSI). Additional information about PennyMac Mortgage Investment Trust is available at pmt.pennymac.com.

|

|

|

| Media |

|

Investors |

|

|

| Kristyn Clark |

|

Kevin Chamberlain |

|

|

| mediarelations@pennymac.com |

|

Isaac Garden |

|

|

| 805.225.8224 |

|

investorrelations@pennymac.com |

|

|

|

|

818.224.7028 |

8

“Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934”, as amended, regarding

management’s beliefs, estimates, projections and assumptions with respect to, among other things, the Company’s financial results, future operations, business plans and investment strategies, as well as industry and market conditions, all

of which are subject to change. Words like “believe,” “expect,” “anticipate,” “promise,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as

“will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. Actual results and operations for any future period may vary materially from those

projected herein and from past results discussed herein. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not limited to: changes in interest rates; the Company’s

ability to comply with various federal, state and local laws and regulations that govern its business; volatility in the Company’s industry, the debt or equity markets, the general economy or the real estate finance and real estate markets;

events or circumstances which undermine confidence in the financial and housing markets or otherwise have a broad impact on financial and housing markets; changes in real estate values, housing prices and housing sales; changes in macroeconomic,

consumer and real estate market conditions; the degree and nature of the Company’s competition; the availability of, and level of competition for, attractive risk-adjusted investment opportunities in mortgage loans and mortgage-related assets

that satisfy the Company’s investment objectives; the inherent difficulty in winning bids to acquire mortgage loans, and the Company’s success in doing so; the concentration of credit risks to which the Company is exposed; the

Company’s dependence on its manager and servicer, potential conflicts of interest with such entities and their affiliates, and the performance of such entities; changes in personnel and lack of availability of qualified personnel at its

manager, servicer or their affiliates; our ability to mitigate cybersecurity risks, cybersecurity incidents and technology disruptions; the development of artificial intelligence; the availability, terms and deployment of short-term and long-term

capital; the adequacy of the Company’s cash reserves and working capital; the Company’s ability to maintain the desired relationship between its financing and the interest rates and maturities of its assets; the timing and amount of cash

flows, if any, from the Company’s investments; our substantial amount of indebtedness; the performance, financial condition and liquidity of borrowers; our exposure to risks of loss and disruptions in operations resulting from severe weather events, man-made or other natural conditions, including climate change and pandemics; the ability of the Company’s servicer, which also provides the Company with fulfillment services, to approve and

monitor correspondent sellers and underwrite loans to investor standards; incomplete or inaccurate information or documentation provided by customers or counterparties, or adverse changes in the financial condition of the Company’s customers

and counterparties; the Company’s indemnification and repurchase obligations in connection with mortgage loans it purchases and later sells or securitizes; the quality and enforceability of the collateral documentation evidencing the

Company’s ownership and rights in the assets in which it invests; increased rates of delinquency, defaults and forbearances and/or decreased recovery rates on the Company’s investments; the performance of mortgage loans underlying

mortgage-backed securities in which the Company retains credit risk; the Company’s ability to foreclose on its investments in a timely manner or at all; increased prepayments of the mortgages and other loans underlying the Company’s

mortgage-backed securities or relating to the Company’s mortgage servicing rights and other investments; risks associated with the discontinuation of LIBOR; the degree to which the Company’s hedging strategies may or may not protect it

from interest rate volatility; the effect of the accuracy of or changes in the estimates the Company makes about uncertainties, contingencies and asset and liability valuations when measuring and reporting upon the Company’s financial condition

and results of operations; the Company’s ability to maintain appropriate internal control over financial reporting; the Company’s ability to detect misconduct and fraud; developments in the secondary markets for the Company’s mortgage

loan products; legislative and

9

regulatory changes that impact the mortgage loan industry or housing market; regulatory or other changes that impact government agencies or government-sponsored entities, or such changes that

increase the cost of doing business with such agencies or entities; the Consumer Financial Protection Bureau and its issued and future rules and the enforcement thereof; changes in government support of homeownership; changes in government or

government-sponsored home affordability programs; changes in the Company’s investment objectives or investment or operational strategies, including any new lines of business or new products and services that may subject it to additional risks;

limitations imposed on the Company’s business and its ability to satisfy complex rules for it to qualify as a REIT for U.S. federal income tax purposes and qualify for an exclusion from the Investment Company Act of 1940 and the ability of

certain of the Company’s subsidiaries to qualify as REITs or as taxable REIT subsidiaries for U.S. federal income tax purposes; changes in governmental regulations, accounting treatment, tax rates and similar matters; the Company’s ability

to make distributions to its shareholders in the future; the Company’s failure to deal appropriately with issues that may give rise to reputational risk; and the Company’s organizational structure and certain requirements in its charter

documents. You should not place undue reliance on any forward-looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by the Company with

the Securities and Exchange Commission from time to time. The Company undertakes no obligation to publicly update or revise any forward-looking statements or any other information contained herein, and the statements made in this press release are

current as of the date of this release only.

10

PENNYMAC MORTGAGE INVESTMENT TRUST AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

December 31, 2024 |

|

|

September 30, 2024 |

|

|

December 31, 2023 |

|

| |

|

|

|

|

|

|

|

|

|

| |

|

(in thousands except share amounts) |

|

| ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

| Cash |

|

$ |

337,694 |

|

|

$ |

344,358 |

|

|

$ |

281,085 |

|

| Short-term investments at fair value |

|

|

103,198 |

|

|

|

102,787 |

|

|

|

128,338 |

|

| Mortgage-backed securities at fair value |

|

|

4,063,706 |

|

|

|

4,182,382 |

|

|

|

4,836,292 |

|

| Loans acquired for sale at fair value |

|

|

2,116,318 |

|

|

|

1,665,796 |

|

|

|

669,018 |

|

| Loans at fair value |

|

|

2,193,575 |

|

|

|

1,429,525 |

|

|

|

1,433,820 |

|

| Derivative assets |

|

|

56,840 |

|

|

|

81,844 |

|

|

|

177,984 |

|

| Deposits securing credit risk transfer arrangements |

|

|

1,110,708 |

|

|

|

1,135,447 |

|

|

|

1,209,498 |

|

| Mortgage servicing rights at fair value |

|

|

3,867,394 |

|

|

|

3,809,047 |

|

|

|

3,919,107 |

|

| Servicing advances |

|

|

105,037 |

|

|

|

71,124 |

|

|

|

206,151 |

|

| Due from PennyMac Financial Services, Inc. |

|

|

16,015 |

|

|

|

8,538 |

|

|

|

56 |

|

| Other |

|

|

438,221 |

|

|

|

224,806 |

|

|

|

252,538 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total assets |

|

$ |

14,408,706 |

|

|

$ |

13,055,654 |

|

|

$ |

13,113,887 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

| Assets sold under agreements to repurchase |

|

$ |

6,500,938 |

|

|

$ |

5,748,461 |

|

|

$ |

5,624,558 |

|

| Mortgage loan participation and sale agreements |

|

|

11,593 |

|

|

|

28,790 |

|

|

|

— |

|

| Notes payable secured by credit risk transfer and mortgage servicing assets |

|

|

2,929,790 |

|

|

|

2,830,108 |

|

|

|

2,910,605 |

|

| Unsecured senior notes |

|

|

605,860 |

|

|

|

814,915 |

|

|

|

600,458 |

|

| Asset-backed financing of variable interest entities at fair value |

|

|

2,040,375 |

|

|

|

1,334,797 |

|

|

|

1,336,731 |

|

| Interest-only security payable at fair value |

|

|

34,222 |

|

|

|

35,098 |

|

|

|

32,667 |

|

| Derivative and credit risk transfer strip liabilities at fair value |

|

|

7,351 |

|

|

|

16,151 |

|

|

|

51,381 |

|

| Accounts payable and accrued liabilities |

|

|

139,124 |

|

|

|

114,085 |

|

|

|

354,989 |

|

| Due to PennyMac Financial Services, Inc. |

|

|

30,206 |

|

|

|

32,603 |

|

|

|

29,262 |

|

| Income taxes payable |

|

|

163,861 |

|

|

|

155,544 |

|

|

|

190,003 |

|

| Liability for losses under representations and warranties |

|

|

6,886 |

|

|

|

8,315 |

|

|

|

26,143 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities |

|

|

12,470,206 |

|

|

|

11,118,867 |

|

|

|

11,156,797 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

| Preferred shares of beneficial interest |

|

|

541,482 |

|

|

|

541,482 |

|

|

|

541,482 |

|

| Common shares of beneficial interest—authorized, 500,000,000 common shares of $0.01 par

value; issued and outstanding 86,860,960, 86,860,960 and 86,760,408 common shares, respectively |

|

|

869 |

|

|

|

869 |

|

|

|

866 |

|

| Additional paid-in capital |

|

|

1,925,067 |

|

|

|

1,924,596 |

|

|

|

1,923,437 |

|

| Accumulated deficit |

|

|

(528,918 |

) |

|

|

(530,160 |

) |

|

|

(508,695 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total shareholders’ equity |

|

|

1,938,500 |

|

|

|

1,936,787 |

|

|

|

1,957,090 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities and shareholders’ equity |

|

$ |

14,408,706 |

|

|

$ |

13,055,654 |

|

|

$ |

13,113,887 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11

PENNYMAC MORTGAGE INVESTMENT TRUST AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Quarterly Periods Ended |

|

| |

|

December 31, 2024 |

|

|

September 30, 2024 |

|

|

December 31, 2023 |

|

| Investment Income |

|

|

|

|

|

|

|

|

|

|

|

|

| Net loan servicing fees: |

|

|

|

|

|

|

|

|

|

|

|

|

| From nonaffiliates |

|

|

|

|

|

|

|

|

|

|

|

|

| Servicing fees |

|

$ |

164,437 |

|

|

$ |

166,617 |

|

|

$ |

165,403 |

|

| Change in fair value of mortgage servicing rights |

|

|

93,267 |

|

|

|

(184,918 |

) |

|

|

(232,332 |

) |

| Hedging results |

|

|

(51,209 |

) |

|

|

(67,220 |

) |

|

|

(11,191 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

206,495 |

|

|

|

(85,521 |

) |

|

|

(78,120 |

) |

| From PennyMac Financial Services, Inc. |

|

|

926 |

|

|

|

441 |

|

|

|

290 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

207,421 |

|

|

|

(85,080 |

) |

|

|

(77,830 |

) |

| Net gains on loans acquired for sale |

|

|

26,387 |

|

|

|

20,059 |

|

|

|

15,380 |

|

| Loan origination fees |

|

|

3,986 |

|

|

|

6,640 |

|

|

|

3,004 |

|

| Net (losses) gains on investments and financings |

|

|

(105,655 |

) |

|

|

146,695 |

|

|

|

164,338 |

|

| Interest income |

|

|

163,135 |

|

|

|

176,734 |

|

|

|

165,278 |

|

| Interest expense |

|

|

187,120 |

|

|

|

184,171 |

|

|

|

185,523 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest expense |

|

|

(23,985 |

) |

|

|

(7,437 |

) |

|

|

(20,245 |

) |

| Other |

|

|

(227 |

) |

|

|

(13 |

) |

|

|

127 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

107,927 |

|

|

|

80,864 |

|

|

|

84,774 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| Earned by PennyMac Financial Services, Inc.: |

|

|

|

|

|

|

|

|

|

|

|

|

| Loan servicing fees |

|

|

20,486 |

|

|

|

22,240 |

|

|

|

20,324 |

|

| Management fees |

|

|

7,149 |

|

|

|

7,153 |

|

|

|

7,252 |

|

| Loan fulfillment fees |

|

|

6,356 |

|

|

|

11,492 |

|

|

|

4,931 |

|

| Professional services |

|

|

6,041 |

|

|

|

2,614 |

|

|

|

2,084 |

|

| Loan collection and liquidation |

|

|

2,537 |

|

|

|

2,257 |

|

|

|

1,184 |

|

| Safekeeping |

|

|

1,336 |

|

|

|

1,174 |

|

|

|

1,059 |

|

| Compensation |

|

|

997 |

|

|

|

1,326 |

|

|

|

2,327 |

|

| Loan origination |

|

|

914 |

|

|

|

1,408 |

|

|

|

817 |

|

| Other |

|

|

6,987 |

|

|

|

4,666 |

|

|

|

4,476 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total expenses |

|

|

52,803 |

|

|

|

54,330 |

|

|

|

44,454 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income before provision for (benefit from) income taxes |

|

|

55,124 |

|

|

|

26,534 |

|

|

|

40,320 |

|

| Provision for (benefit from) income taxes |

|

|

8,589 |

|

|

|

(14,873 |

) |

|

|

(12,590 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

|

46,535 |

|

|

|

41,407 |

|

|

|

52,910 |

|

| Dividends on preferred shares |

|

|

10,455 |

|

|

|

10,455 |

|

|

|

10,455 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income attributable to common shareholders |

|

$ |

36,080 |

|

|

$ |

30,952 |

|

|

$ |

42,455 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings per common share |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

$ |

0.41 |

|

|

$ |

0.36 |

|

|

$ |

0.49 |

|

| Diluted |

|

$ |

0.41 |

|

|

$ |

0.36 |

|

|

$ |

0.44 |

|

| Weighted average shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

|

86,861 |

|

|

|

86,861 |

|

|

|

86,659 |

|

| Diluted |

|

|

86,861 |

|

|

|

86,861 |

|

|

|

110,987 |

|

12

PENNYMAC MORTGAGE INVESTMENT TRUST AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Year ended December 31, |

|

| |

|

2024 |

|

|

2023 |

|

|

2022 |

|

| |

|

(in thousands, except earnings per common share) |

|

| Net investment income |

|

|

|

|

|

|

|

|

|

|

|

|

| Net loan servicing fees: |

|

|

|

|

|

|

|

|

|

|

|

|

| From nonaffiliates |

|

|

|

|

|

|

|

|

|

|

|

|

| Contractually specified |

|

$ |

644,642 |

|

|

$ |

659,438 |

|

|

$ |

625,210 |

|

| Other |

|

|

14,722 |

|

|

|

17,008 |

|

|

|

26,041 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

659,364 |

|

|

|

676,446 |

|

|

|

651,251 |

|

| Change in fair value of mortgage servicing rights |

|

|

(170,409 |

) |

|

|

(296,847 |

) |

|

|

449,435 |

|

| Mortgage servicing rights hedging results |

|

|

(226,608 |

) |

|

|

(92,775 |

) |

|

|

(204,879 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

262,347 |

|

|

|

286,824 |

|

|

|

895,807 |

|

| From PennyMac Financial Services, Inc. |

|

|

2,193 |

|

|

|

1,784 |

|

|

|

13,744 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

264,540 |

|

|

|

288,608 |

|

|

|

909,551 |

|

| Net gains on loans acquired for sale: |

|

|

|

|

|

|

|

|

|

|

|

|

| From nonaffiliates |

|

|

65,055 |

|

|

|

32,695 |

|

|

|

20,724 |

|

| From PennyMac Financial Services, Inc. |

|

|

8,069 |

|

|

|

7,162 |

|

|

|

4,968 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

73,124 |

|

|

|

39,857 |

|

|

|

25,692 |

|

| Loan origination fees |

|

|

15,085 |

|

|

|

18,231 |

|

|

|

52,085 |

|

| Net gains (losses) on investments and financings |

|

|

61,050 |

|

|

|

178,099 |

|

|

|

(658,787 |

) |

| Net interest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

| Interest income |

|

|

635,263 |

|

|

|

639,907 |

|

|

|

383,794 |

|

| Interest expense |

|

|

714,659 |

|

|

|

735,968 |

|

|

|

410,420 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest expense |

|

|

(79,396 |

) |

|

|

(96,061 |

) |

|

|

(26,626 |

) |

| Results of real estate acquired in settlement of loans |

|

|

(437 |

) |

|

|

(186 |

) |

|

|

496 |

|

| Other |

|

|

228 |

|

|

|

472 |

|

|

|

1,360 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

334,194 |

|

|

|

429,020 |

|

|

|

303,771 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

| Earned by PennyMac Financial Services, Inc.: |

|

|

|

|

|

|

|

|

|

|

|

|

| Loan servicing fees |

|

|

83,252 |

|

|

|

81,347 |

|

|

|

81,915 |

|

| Management fees |

|

|

28,623 |

|

|

|

28,762 |

|

|

|

31,065 |

|

| Loan fulfillment fees |

|

|

26,291 |

|

|

|

27,826 |

|

|

|

67,991 |

|

| Professional services |

|

|

12,779 |

|

|

|

7,621 |

|

|

|

9,569 |

|

| Loan collection and liquidation |

|

|

6,834 |

|

|

|

4,562 |

|

|

|

5,396 |

|

| Compensation |

|

|

5,608 |

|

|

|

7,106 |

|

|

|

5,941 |

|

| Safekeeping |

|

|

4,403 |

|

|

|

3,766 |

|

|

|

8,201 |

|

| Loan origination |

|

|

3,328 |

|

|

|

4,602 |

|

|

|

12,036 |

|

| Other |

|

|

20,428 |

|

|

|

19,033 |

|

|

|

18,570 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total expenses |

|

|

191,546 |

|

|

|

184,625 |

|

|

|

240,684 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income before (benefit from) provision for income taxes |

|

|

142,648 |

|

|

|

244,395 |

|

|

|

63,087 |

|

| (Benefit from) provision for income taxes |

|

|

(18,336 |

) |

|

|

44,741 |

|

|

|

136,374 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income (loss) |

|

|

160,984 |

|

|

|

199,654 |

|

|

|

(73,287 |

) |

| Dividends on preferred shares |

|

|

41,819 |

|

|

|

41,819 |

|

|

|

41,819 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income (loss) attributable to common shareholders |

|

$ |

119,165 |

|

|

$ |

157,835 |

|

|

$ |

(115,106 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings (losses) per common share |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

$ |

1.37 |

|

|

$ |

1.80 |

|

|

$ |

(1.26 |

) |

| Diluted |

|

$ |

1.37 |

|

|

$ |

1.63 |

|

|

$ |

(1.26 |

) |

| Weighted average common shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

|

86,815 |

|

|

|

87,372 |

|

|

|

91,434 |

|

| Diluted |

|

|

86,815 |

|

|

|

111,700 |

|

|

|

91,434 |

|

13

Exhibit 99.2 4Q24 EARNINGS REPORT PennyMac Mortgage Investment Trust

January 2025

FORWARD LOOKING STATEMENTS This presentation contains forward-looking

statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding management’s beliefs, estimates, projections and assumptions with respect to, among other things, the Company’s financial

results, future operations, business plans and investment strategies, as well as industry and market conditions, all of which are subject to change. Words like “believe,” “expect,” “anticipate,”

“promise,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may”

are generally intended to identify forward-looking statements. Actual results and operations for any future period may vary materially from those projected herein and from past results discussed herein. These forward-looking statements include, but

are not limited to, statements regarding future changes in interest rates, housing, and prepayment rates; future loan originations and production; future loan delinquencies, defaults and forbearances; future investment and hedge expenses; future

investment strategies, future earnings and return on equity as well as other business and financial expectations. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not

limited to: changes in interest rates; the Company’s ability to comply with various federal, state and local laws and regulations that govern its business; the general economy or the real estate finance and real estate markets; events or

circumstances which undermine confidence in the financial and housing markets or otherwise have a broad impact on financial and housing markets; changes in real estate values, housing prices and housing sales; changes in

macroeconomic, consumer and real estate market conditions; the degree and nature of the Company’s competition; the availability of, and level of competition for, attractive risk adjusted investment opportunities in mortgage loans and mortgage

related assets that satisfy the Company’s investment objectives; the inherent difficulty in winning bids to acquire mortgage loans, and the Company’s success in doing so; the concentration of credit risks to which the Company is

exposed; the Company’s dependence on its manager and servicer, potential conflicts of interest with such entities and their affiliates, and the performance of such entities; changes in personnel and lack of availability of

qualified personnel at its manager, servicer or their affiliates; our ability to mitigate cybersecurity risks, cybersecurity incidents and technology disruptions; the development of artificial intelligence; the availability, terms

and deployment of short term and long term capital; the adequacy of the Company’s cash reserves and working capital; the Company’s ability to maintain the desired relationship between its financing and the interest rates and

maturities of its assets; the timing and amount of cash flows, if any, from the Company’ s investments; our substantial amount of indebtedness; the performance, financial condition and liquidity of borrowers; our exposure to risks

of loss and disruptions in operations resulting from severe weather events, man-made or other natural conditions, including climate change and pandemics; the ability of the Company’s servicer, which also provides the Company with

fulfillment services, to approve and monitor correspondent sellers and underwrite loans to investor standards; incomplete or inaccurate information or documentation provided by customers or counterparties, or adverse changes in the

financial condition of the Company’s customers and counterparties; the Company’s indemnification and repurchase obligations in connection with mortgage loans it purchases and later sells or securitizes; the quality and

enforceability of the collateral documentation evidencing the Company’ s ownership and rights in the assets in which it invests; increased rates of delinquency, defaults and forbearances and/or decreased recovery rates on the Company’s

investments; the performance of mortgage loans underlying mortgage backed securities in which the Company retains credit risk; the Company’s ability to foreclose on its investments in a timely manner or at all; increased prepayments of the

mortgages and other loans underlying the Company’s mortgage backed securities or relating to the Company’s mortgage servicing rights and other investments; risks associated with the discontinuation of LIBOR; the degree to which the

Company’s hedging strategies may or may not protect it from interest rate volatility; the effect of the accuracy of or changes in the estimates the Company makes about uncertainties, contingencies and asset and liability valuations when

measuring and reporting upon the Company’s financial condition and results of operations; the Company’s ability to maintain appropriate internal control over financial reporting; the Company’s ability to detect

misconduct and fraud; developments in the secondary markets for the Company’s mortgage loan products; legislative and regulatory changes that impact the mortgage loan industry or housing market regulatory or other changes that impact

government agencies or government sponsored entities, or such changes that increase the cost of doing business with such agencies or entities; the Consumer Financial Protection Bureau and its issued and future rules and the enforcement thereof;

changes in government support of homeownership; changes in government or government sponsored home affordability programs; changes in the Company’s investment objectives or investment or operational strategies, including any new lines of

business or new products and services that may subject it to additional risks volatility in the Company’s industry, the debt or equity markets; limitations imposed on the Company’s business and its ability to satisfy complex rules for it

to qualify as a REIT for U.S. federal income tax purposes and qualify for an exclusion from the Investment Company Act of 1940 and the ability of certain of the Company’s subsidiaries to qualify as REITs or as taxable REIT subsidiaries for

U.S. federal income tax purposes; changes in governmental regulations, accounting treatment, tax rates and similar matters; the Company’s ability to make distributions to its shareholders in the future; the Company’s failure to deal

appropriately with issues that may give rise to reputational risk; and the Company’s organizational structure and certain requirements in its charter documents. You should not place undue reliance on any forward-looking statement and should

consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by the Company with the Securities and Exchange Commission from time to time. The Company undertakes no

obligation to publicly update or revise any forward-looking statements or any other information contained herein, and the statements made in this presentation are current as of the date of this presentation only. This presentation contains

financial information calculated other than in accordance with U.S. generally accepted accounting principles (“GAAP”), such as income excluding market driven value changes that provide a meaningful perspective on the

Company’s business results since the Company utilizes this information to evaluate and manage the business. Non-GAAP disclosures have limitations as an analytical tool and should not be viewed as a substitute for financial information

determined in accordance with GAAP. 2

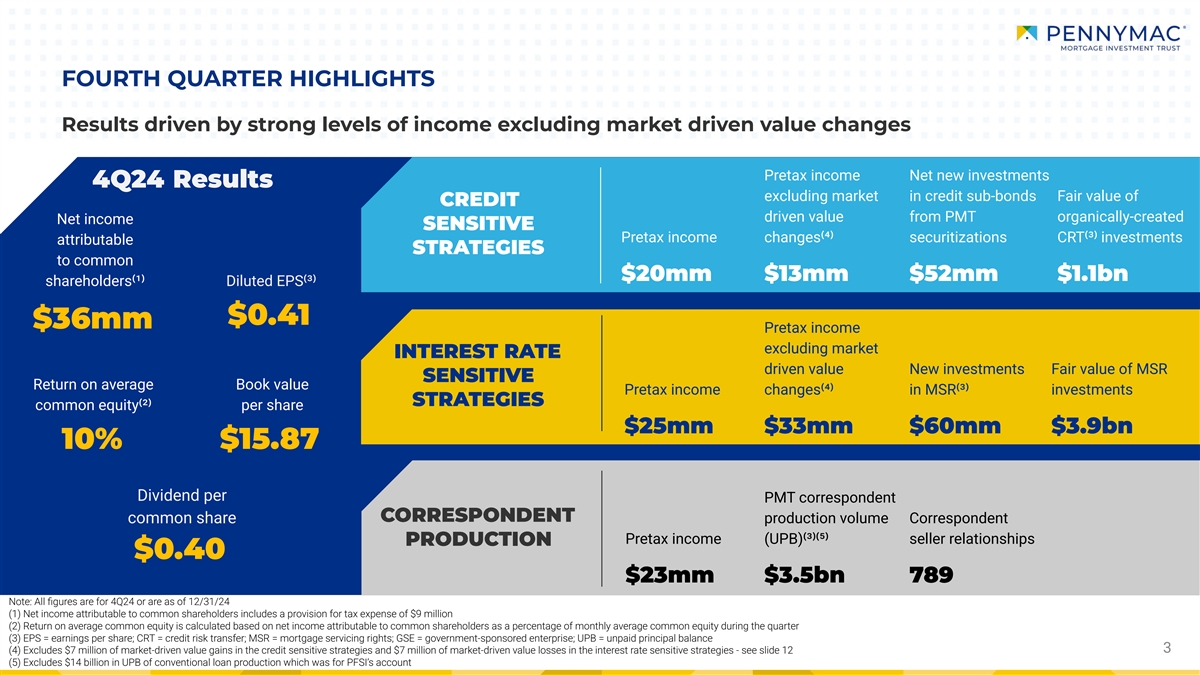

FOURTH QUARTER HIGHLIGHTS Results driven by strong levels of income

excluding market driven value changes Pretax income Net new investments 4Q24 Results excluding market in credit sub-bonds Fair value of CREDIT driven value from PMT organically-created Net income SENSITIVE Pretax income changes⁽⁴⁾

securitizations CRT⁽³⁾ investments attributable STRATEGIES to common $20mm $13mm $52mm $1.1bn shareholders⁽¹⁾ Diluted EPS⁽³⁾ $0.41 $36mm Pretax income excluding market INTEREST RATE driven value New

investments Fair value of MSR SENSITIVE Return on average Book value Pretax income changes⁽⁴⁾ in MSR⁽³⁾ investments STRATEGIES common equity⁽²⁾ per share $25mm $33mm $60mm $3.9bn 10% $15.87

Dividend per PMT correspondent CORRESPONDENT common share production volume Correspondent Pretax income (UPB)⁽³⁾⁽⁵⁾ seller relationships PRODUCTION $0.40 $23mm $3.5bn 789 Note: All figures are for 4Q24 or are

as of 12/31/24 (1) Net income attributable to common shareholders includes a provision for tax expense of $9 million (2) Return on average common equity is calculated based on net income attributable to common shareholders as a percentage of monthly

average common equity during the quarter (3) EPS = earnings per share; CRT = credit risk transfer; MSR = mortgage servicing rights; GSE = government-sponsored enterprise; UPB = unpaid principal balance 3 3 (4) Excludes $7 million of market-driven

value gains in the credit sensitive strategies and $7 million of market-driven value losses in the interest rate sensitive strategies - see slide 12 (5) Excludes $14 billion in UPB of conventional loan production which was for PFSI’s

account

PMT’S 2024 PERFORMANCE ESTABLISHES STRONG FOUNDATION FOR 2025

Diverse strategies provided multiple Hedging strategy protected book value sources of returns despite significant interest rate volatility Pretax income contribution by strategy: 4.70% 4.57% Credit Interest rate Correspondent sensitive

sensitive production 3.88% 3.62% $123mm $16mm $57mm 10-Year Treasury Yield Book Value per Share Strengthened and repositioned Expanding on our proven track balance sheet for higher rates record of organic credit investments ● Sold $833 million

of low coupon MBS and $111 ● Completed two securitizations of Agency-eligible million of opportunistic investments in GSE CRT as investor loans from PMT production credit spreads tightened ‒ Generated $52 million of net new credit

investments ● New MSR investments of $219 million with attractive expected returns ● Issued $1.3 billion of term debt to address and ‒ Strong investor demand and significant opportunity to leverage PMT’s production and

securitization extend maturities, generally at tighter financing expertise spreads 4

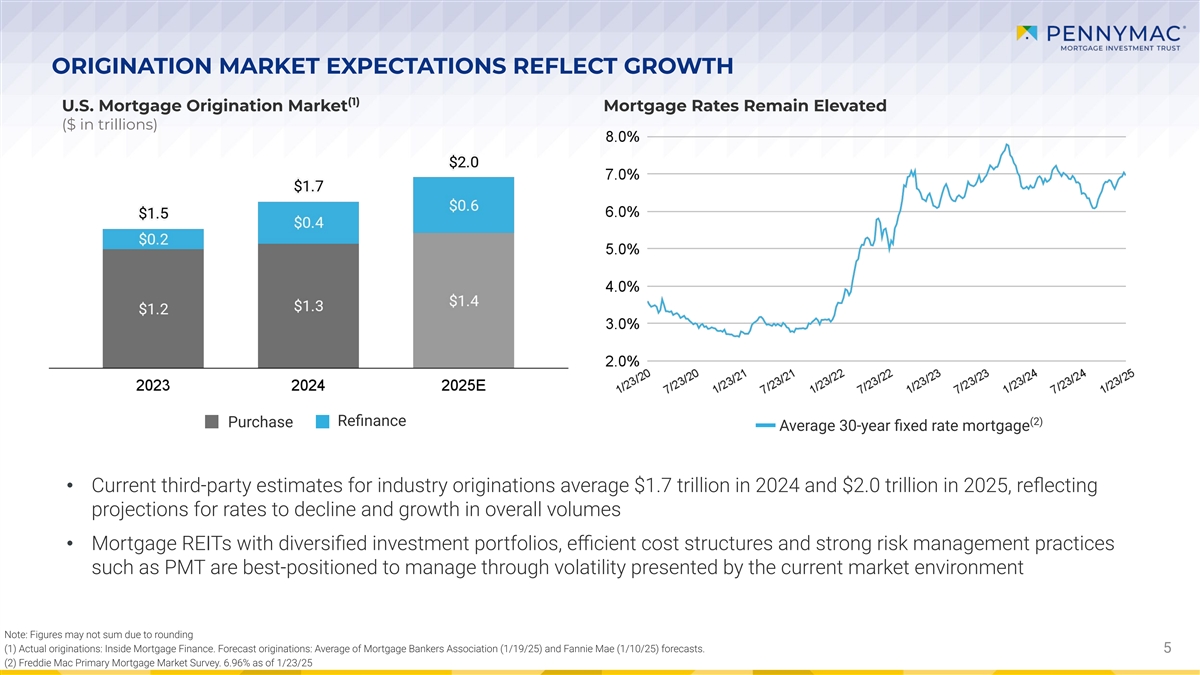

ORIGINATION MARKET EXPECTATIONS REFLECT GROWTH (1) U.S. Mortgage

Origination Market Mortgage Rates Remain Elevated ($ in trillions) (2) Refinance Purchase Average 30-year fixed rate mortgage • Current third-party estimates for industry originations average $1.7 trillion in 2024 and $2.0 trillion

in 2025, reflecting projections for rates to decline and growth in overall volumes • Mortgage REITs with diversified investment portfolios, efficient cost structures and strong risk management practices such as PMT are

best-positioned to manage through volatility presented by the current market environment Note: Figures may not sum due to rounding (1) Actual originations: Inside Mortgage Finance. Forecast originations: Average of Mortgage Bankers Association

(1/19/25) and Fannie Mae (1/10/25) forecasts. 5 (2) Freddie Mac Primary Mortgage Market Survey. 6.96% as of 1/23/25

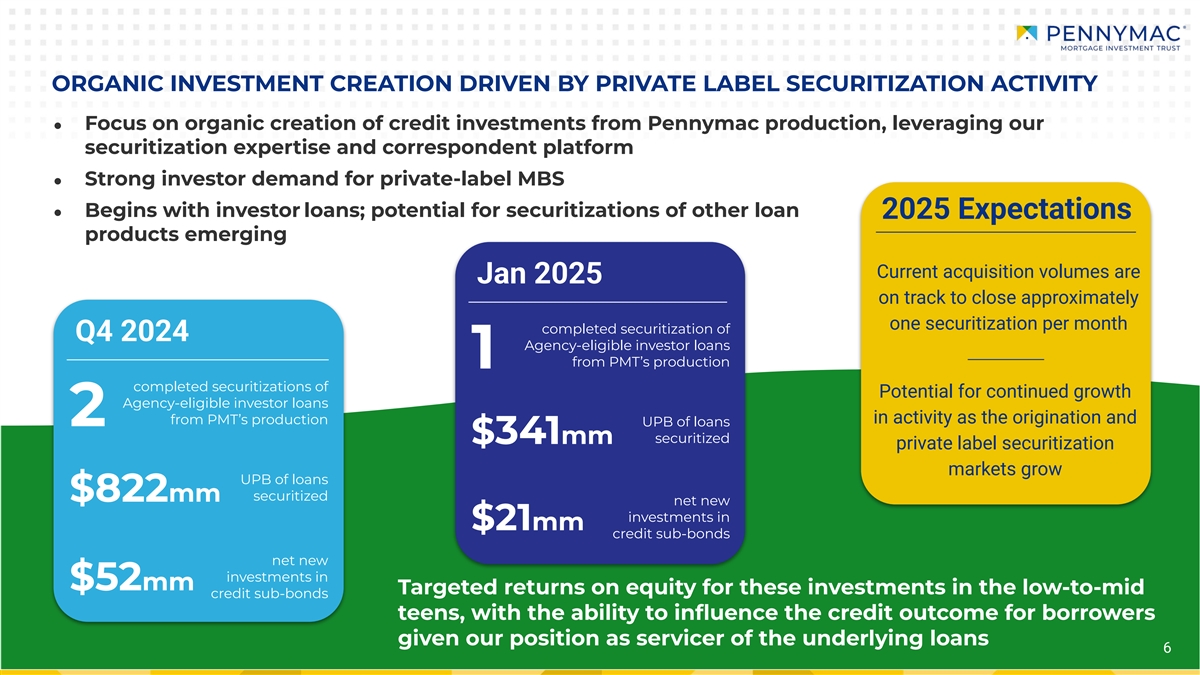

ORGANIC INVESTMENT CREATION DRIVEN BY PRIVATE LABEL SECURITIZATION

ACTIVITY ● Focus on organic creation of credit investments from Pennymac production, leveraging our securitization expertise and correspondent platform ● Strong investor demand for private-label MBS ● Begins with investor loans;

potential for securitizations of other loan 2025 Expectations products emerging Current acquisition volumes are Jan 2025 on track to close approximately one securitization per month completed securitization of Q4 2024 Agency-eligible investor loans

from PMT’s production 1 completed securitizations of Potential for continued growth Agency-eligible investor loans in activity as the origination and from PMT’s production 2 UPB of loans $341mm securitized private label securitization

markets grow UPB of loans securitized $822mm net new investments in $21mm credit sub-bonds net new investments in $52mm Targeted returns on equity for these investments in the low-to-mid credit sub-bonds teens, with the ability to influence

the credit outcome for borrowers given our position as servicer of the underlying loans 6

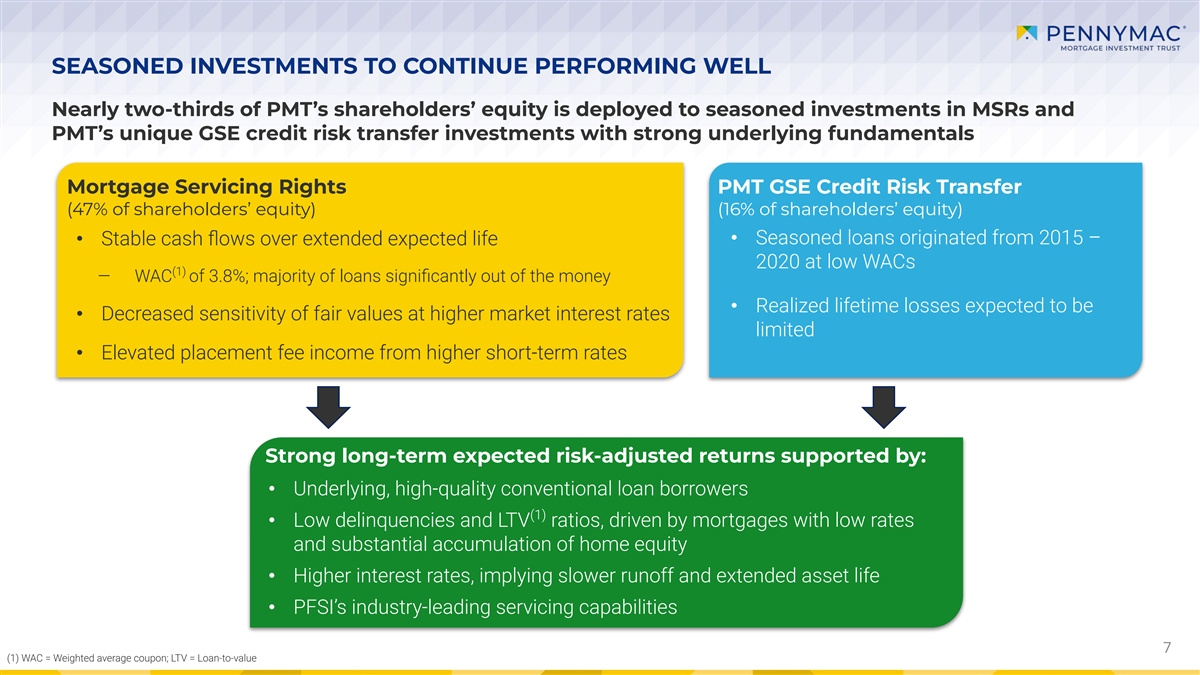

SEASONED INVESTMENTS TO CONTINUE PERFORMING WELL Nearly two-thirds of

PMT’s shareholders’ equity is deployed to seasoned investments in MSRs and PMT’s unique GSE credit risk transfer investments with strong underlying fundamentals Mortgage Servicing Rights PMT GSE Credit Risk Transfer (47% of

shareholders’ equity) (16% of shareholders’ equity) • Stable cash flows over extended expected life • Seasoned loans originated from 2015 – 2020 at low WACs (1) ‒ WAC of 3.8%; majority of loans

significantly out of the money • Realized lifetime losses expected to be • Decreased sensitivity of fair values at higher market interest rates limited • Elevated placement fee income from higher short-term rates Strong

long-term expected risk-adjusted returns supported by: • Underlying, high-quality conventional loan borrowers (1) • Low delinquencies and LTV ratios, driven by mortgages with low rates and substantial accumulation of home equity •

Higher interest rates, implying slower runoff and extended asset life • PFSI’s industry-leading servicing capabilities 7 (1) WAC = Weighted average coupon; LTV = Loan-to-value

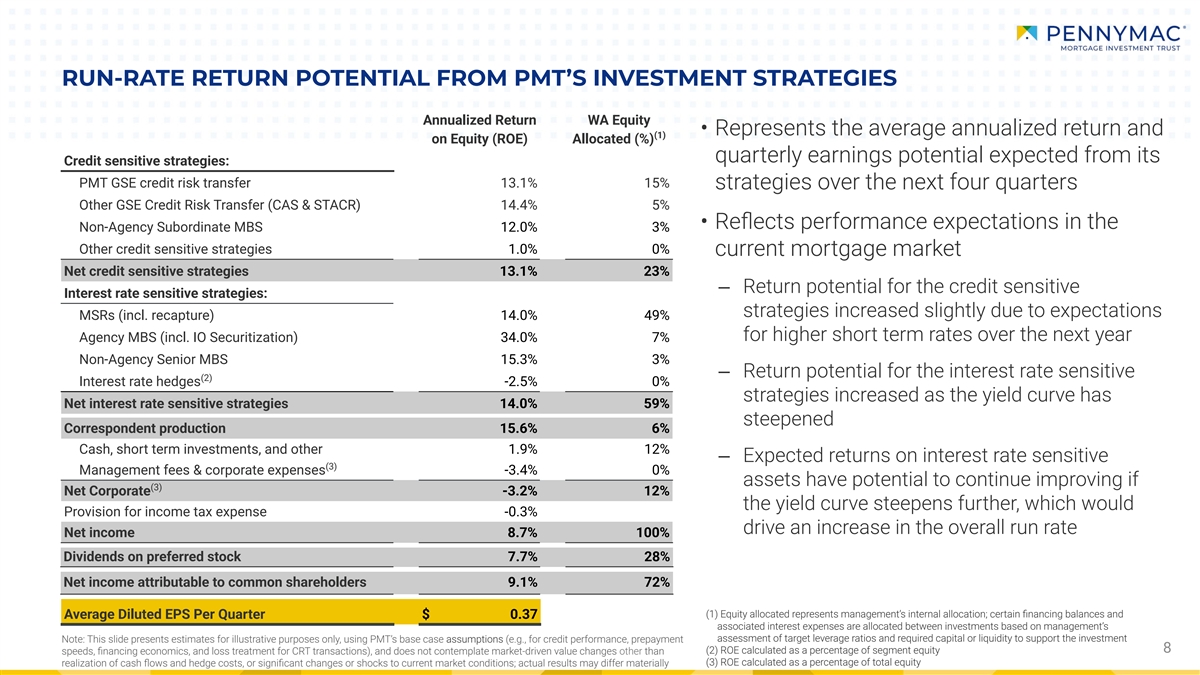

RUN-RATE RETURN POTENTIAL FROM PMT’S INVESTMENT STRATEGIES

Annualized Return WA Equity • Represents the average annualized return and (1) on Equity (ROE) Allocated (%) quarterly earnings potential expected from its Credit sensitive strategies: PMT GSE credit risk transfer 13.1% 15% strategies over the

next four quarters Other GSE Credit Risk Transfer (CAS & STACR) 14.4% 5% • Reflects performance expectations in the Non-Agency Subordinate MBS 12.0% 3% Other credit sensitive strategies 1.0% 0% current mortgage market Net credit

sensitive strategies 13.1% 23% ‒ Return potential for the credit sensitive Interest rate sensitive strategies: strategies increased slightly due to expectations MSRs (incl. recapture) 14.0% 49% for higher short term rates over the next year

Agency MBS (incl. IO Securitization) 34.0% 7% Non-Agency Senior MBS 15.3% 3% ‒ Return potential for the interest rate sensitive (2) Interest rate hedges -2.5% 0% strategies increased as the yield curve has Net interest rate sensitive

strategies 14.0% 59% steepened Correspondent production 15.6% 6% Cash, short term investments, and other 1.9% 12% ‒ Expected returns on interest rate sensitive (3) Management fees & corporate expenses -3.4% 0% assets have potential to

continue improving if (3) Net Corporate -3.2% 12% the yield curve steepens further, which would Provision for income tax expense -0.3% drive an increase in the overall run rate Net income 8.7% 100% Dividends on preferred stock 7.7% 28% Net income

attributable to common shareholders 9.1% 72% (1) Equity allocated represents management’s internal allocation; certain financing balances and Average Diluted EPS Per Quarter $ 0.37 associated interest expenses are allocated between

investments based on management’s assessment of target leverage ratios and required capital or liquidity to support the investment Note: This slide presents estimates for illustrative purposes only, using PMT’s base case assumptions

(e.g., for credit performance, prepayment 8 (2) ROE calculated as a percentage of segment equity speeds, financing economics, and loss treatment for CRT transactions), and does not contemplate market-driven value changes other than (3) ROE