UNITED STATES

SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C.

20549

FORM 6-K

Report of Foreign Private

Issuer

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange

Act of 1934

For the month of

February, 2025

Commission File Number

1-15106

PETRÓLEO BRASILEIRO

S.A. – PETROBRAS

(Exact name of registrant

as specified in its charter)

Brazilian Petroleum

Corporation – PETROBRAS

(Translation of Registrant's

name into English)

Avenida Henrique Valadares, 28 – 9th floor

20231-030 – Rio de Janeiro, RJ

Federative Republic of Brazil

(Address of principal

executive office)

Indicate by check mark

whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form

40-F _______

Indicate by check mark

whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission

pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes _______ No___X____

Table of Contents

| |

PETROBRAS | Performance Report | 4Q24 | 2 |

| DISCLAIMER |

|

This report may contain forward-looking

statements about future events. Such forecasts reflect only the expectations of the company's management about future economic conditions,

as well as the company's industry, performance and financial results, among others. The terms "anticipates", "believes",

"expects", "predicts", "intends", "plans", "projects", "aims", "should",

as well as other similar terms, are intended to identify such forecasts, which, of course, involve risks and uncertainties foreseen or

not foreseen by the company and, consequently, are not guarantees of the company's future results. Therefore, future results of the company's

operations may differ from current expectations, and the reader should not rely solely on the information contained herein. The Company

undertakes no obligation to update the presentations and forecasts in the light of new information or future developments. The figures

reported for 4Q24 onwards are estimates or targets. Additionally, this presentation contains some financial indicators that are not recognized

under BR GAAP or IFRS. These indicators do not have standardized meanings and may not be comparable to indicators with a similar description

used by other companies. We provide these indicators because we use them as measures of the company's performance; they should not be

considered in isolation or as a substitute for other financial metrics that have been disclosed in accordance with BR GAAP or IFRS. See

definitions of Free Cash Flow, Adjusted EBITDA and Net Debt in the Glossary and respective reconciliations in the Liquidity and Capital

Resources, Reconciliation of Adjusted EBITDA and Net Debt sections. Consolidated financial information prepared in accordance with International

Accounting Standard and audited by the independent auditors.

|

| |

PETROBRAS | Performance Report | 4Q24 | 3 |

CEO’s Message

Dear shareholders and investors,

It is with great satisfaction that

I address you to present some of the many achievements we have obtained in 2024 and to talk a little about the near future of our Petrobras.

The excellent operational and financial

results of 2024 demonstrate, once again, our company's ability to generate value that is returned to society and our investors. I highlight

the operational generation of US$ 38 billion and the financial debt of US$ 23 billion, the lowest level since 2008.

The variation in profit that we report

is fundamentally due to, an accounting issue that does not affect our cash: the exchange rate variation of debts between Petrobras and

its subsidiaries abroad*. The annual result was also impacted by the effects, in 2Q24, of the tax transaction that concluded

legal disputes amounting to R$ 45 billion. This tax transaction has broadly positive repercussions for Petrobras in terms of risk mitigation

and cash outflows. Excluding one-off events, the net profit for the year would be US$ 19.4 billion (R$ 103 billion) and EBITDA would be

US$ 45.9 billion (R$ 245.8 billion).

In 2024, we once again achieved our

oil and gas production targets. As I always emphasize: every drop of oil that generates profit for the company matters. Thus, achieving

production targets is fundamental for Petrobras, as it allows us to maximize value generation through better integration with our downstream

assets. Our commitment to these targets also reflects our focus on operational efficiency and project management.

I would like to mention some achievements

of 2024 related to our production targets: the early start-up of the FPSO Maria Quitéria in the Jubarte field, the achievement

of the maximum production capacity of the FPSO Sepetiba in the Mero field, and the start-up of the FPSO Marechal Duque de Caxias, also

in the Mero field.

In refining, we increased the utilization

rate of our refineries to 93%, the highest in ten years, and set a record for processing pre-salt oils, which accounted for 70% of the

total processed. Historical records were also set for the production of gasoline and S-10 diesel.

Despite the excellence of our results

in 2024, we want to and will do much more.

In refining, by 2025, we will have

an increase of 25 kbpd in processing capacity with the completion of the revamp of Train 1 at RNEST, already considering the start-up

of the SNOx unit in 2024. We will also achieve an additional production of 63 kbpd of diesel S-10 with the new Hydrocracking unit (HDT)

at Replan.

In Exploration & Production (E&P),

we will increase oil production by 100 kbpd, moving towards the milestone of 2.5 million bpd by 2027. We will also increase gas supply

to 50 million m³/day by 2026. To achieve this goal, we will start operating, in 2025, the second module of the gas processing unit

at the Boaventura Complex, with the capacity to process 10.5 million m³/day, totaling 21 million m³/day of total capacity.

Also in 2025, we will add a production capacity of 585 kbpd through the commissioning of three new production units in the pre-salt.

The first of these, the FPSO Almirante Tamandaré, is the largest platform to enter operation in the Búzios field and has

been producing since February. This unit, which is the sixth in the Búzios field, was fundamental for an extremely relevant achievement:

on Monday, February 24, we surpassed the mark of 800 kbpd barrels in Búzios.

Regardless of the magnitude of the

results and the infrastructure to be implemented, we know we cannot rest. Oil and natural gas fields, no matter how productive, are finite

and therefore deplete naturally. For this reason, pursuing the replenishment of oil and gas reserves is fundamental for Petrobras to maintain

its prominent position in the coming decades. Thus, the importance of responsible exploration of the Equatorial Margin stands out, always

in line with the commitments made with environmental agencies. In the same vein, we will prioritize our exploratory efforts in the Pelotas

basin and other assets in our portfolio.

|

* The exchange rate variation in these transactions is reflected

in the net income of the holding company in Brazil. |

| |

PETROBRAS | Performance Report | 4Q24 | 4 |

I reiterate that our diligence in

replenishing oil and gas reserves does not contradict our relentless pursuit of neutrality in our operational emissions. Our current oil

and gas production already stands out with one of the lowest environmental footprints in the industry. Nevertheless, we remain committed

to reducing our operational emissions and seeking profitable investments for scope 3 emissions.

I emphasize the prospect of profitability:

our governance establishes that our investments, in all business segments, must be profitable, even in a scenario with more challenging

assumptions. This is what we have done, for example, in the E&P segment: we have only sanctioned projects that present an expectation

of profitability considering the Brent price at US$ 45/bbl in the long term. Only with the generation of economic value will we continue

to build a long-lasting, responsible Petrobras capable of generating wealth for future generations.

And this is what we proposed with

our new Strategic Plan. We continue to focus on E&P, with production growth and prioritization of reserve replenishment. At the same

time, we maintain our integration strategy with downstream and increase our decarbonization and green energy generation efforts to be

leaders in the just energy transition.

In this sense, we continue to analyze

opportunities for profitable diversification and integrated operations in petrochemicals. We are advancing in partnership studies with

major players for the production of ethanol, in addition to the initiative, also in collaboration with partners, for the production of

e-methanol, aiming to implement the first commercial-scale plant in Brazil, among other decarbonization initiatives.

We are returning to the fertilizers

segment, with the ANSA operation scheduled for 2025 and the resumption of construction of UFN 3.

All these initiatives contribute to

the sustainable growth of Petrobras, generating returns for government and private shareholders and for society.

In 2024, we delivered a total return

to shareholders of around 20%, considering the appreciation of the share price and the payment of dividends. We invested R$ 91 billion

(5% of total investments in Brazil), sustaining 250 thousand jobs. We paid R$ 270 billion in taxes; we distributed R$102.6 billion, of

which R$37.9 billion corresponded to the control group;; and we allocated more than R$ 1 billion in voluntary and mandatory investments,

sponsorships and donations.

Our efforts in the environmental,

social, and governance areas received important recognition: this year, Petrobras returned to the Dow Jones Sustainability Index, one

of the most important in the world. Petrobras is one of nine global energy companies qualified among more than 50 companies in the sector

evaluated.

We will continue to generate high

returns for society and shareholders, and I am confident that the way to achieve this is to continue investing in profitable projects,

with capital discipline, rationality, governance, and efficiency, working with integrity, safety, innovation, and care for people, our

main asset. Petrobras has an even brighter future ahead. Brazil is our energy.

Magda Chambriard, Petrobras’

CEO

| |

PETROBRAS | Performance Report | 4Q24 | 5 |

Highlights – 2024

Highlights - 2024

“2024 was a positive year for Petrobras.

We consistently maintained strong cash generation, reaching US$ 38 billion in Operating Cash Flow in 2024. This result demonstrates the

company's financial health and the quality of its assets, which operate profitably, generating resources to make investments, remunerate

shareholders and meet all its obligations. In 2025, with the entry of three new production systems in the year and an expected increase

of 100,000 barrels per day, we expect to have even more consistent results.”

Fernando Melgarejo, Chief Financial and Investor

Relations Officer

Main financial highlights

| • | Maintenance of a strong cash generation with Operating Cash Flow of US$

38.0 billion and Free Cash Flow of US$ 23.3 billion in 2024 |

| • | Financial debt of US$ 23.2 billion at year end, the lowest level since

2008 |

| • | Consistent performance: Adjusted EBITDA without one-off events of US$

45.9 billion and Net Profit without one-off events of US$ 19.4 billion |

“Petrobras' result in 2024 was mainly

impacted by an item of an accounting nature: the exchange rate variation on debts between Petrobras and its subsidiaries abroad. These

are financial transactions between companies in the same group, which generate opposite effects that in the end balance out economically.

This is because the currency variation in these transactions enters the net result of the Holding in Brazil and negatively impacted the

profit for 2024. At the same time, there was a direct positive impact on equity.”

Fernando Melgarejo, Chief Financial and Investor

Relations Officer

| |

PETROBRAS | Performance Report | 4Q24 | 6 |

Highlights – 2024

Commitment to investments

| • | Capex of US$ 16.6 billion in 2024 |

“The CAPEX of US$ 16.6 billion,

higher than the guidance, does not represent an additional cost but an anticipation, as we were able to reduce the gap between the physical

and financial evolution of the platforms in Búzios. We expected this reduction in the mentioned mismatch to occur throughout 2025,

but we acted strongly in contractual management and the solution was totally anticipated to 2024. Petrobras benefits from reduced risks

and increased potential for anticipations. This is what we are focused on: executing our investment plan and achieving our production

targets.”

Fernando Melgarejo, Chief Financial and Investor

Relations Officer

Contribution to society

| • | We paid R$ 270 billion in taxes to the Federal Government, states and

municipalities, the second highest payment in the last 10 years |

| • | We distributed R$102.6 billion, of which R$37.9 billion corresponded

to the control group |

| • | We allocated more than R$ 1 billion in voluntary and mandatory investments,

sponsorships and donations |

Main operational highlights

| • | We increased our proven reserves, reaching a reserve replacement ratio

(RRR) of 154% and a production reserve ratio (R/P) of 13.2 years |

| • | We had the production start-up on FPSO Maria Quitéria and FPSO

Marechal Duque de Caxias and reached the top of production on FPSO Sepetiba |

| • | We set new annual records for total own and operated production in pre-salt,

with 2.2 million boed and 3.2 million boed, respectively. The production volume in pre-salt represents 81% of the company's total production

in 2024 |

| • | We confirmed, together with partners, a discovery of 6 trillion cubic

feet (Tcf) in place (VGIP), with the drilling of the Sirius-2 well. The largest gas discovery in Colombia's history |

| • | Total utilization factor (FUT) in 2024 was 93%, the highest of the refining

system in the last 10 years considering Petrobras current refineries |

| • | We achieved a record of 70% share of pre-salt oil in refinery throughput

and set production records for gasoline (420 kbpd) and S-10 diesel (452 kbpd) |

| • | We started commercial operation of the natural gas processing unit at

Boaventura Energy Complex and the start-up of SNOx at RNEST. |

| |

PETROBRAS | Performance Report | 4Q24 | 7 |

Highlights – 2024

Main items

Table 1 – Main items

| |

|

|

|

|

|

Variation (%) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Sales revenues |

20,815 |

23,366 |

27,107 |

91,416 |

102,409 |

(10.9) |

(23.2) |

(10.7) |

| Gross profit |

9,983 |

12,005 |

14,654 |

45,972 |

53,974 |

(16.8) |

(31.9) |

(14.8) |

| Operating expenses |

(7,196) |

(3,605) |

(6,632) |

(19,096) |

(15,941) |

99.6 |

8.5 |

19.8 |

| Consolidated net income (loss) attributable to the shareholders of Petrobras |

(2,780) |

5,870 |

6,259 |

7,528 |

24,884 |

− |

− |

(69.7) |

| Consolidated net income (loss) without one-off events attributable to the shareholders of Petrobras (*) |

3,083 |

5,475 |

7,642 |

19,370 |

25,634 |

(43.7) |

(59.7) |

(24.4) |

| Net cash provided by operating activities |

8,204 |

11,307 |

11,669 |

37,984 |

43,212 |

(27.4) |

(29.7) |

(12.1) |

| Free cash flow |

3,766 |

6,857 |

8,073 |

23,318 |

31,074 |

(45.1) |

(53.4) |

(25.0) |

| Adjusted EBITDA |

7,165 |

11,480 |

13,470 |

40,399 |

52,414 |

(37.6) |

(46.8) |

(22.9) |

| Adjusted EBITDA without one-off events (*) |

9,879 |

11,614 |

14,985 |

45,886 |

55,158 |

(14.9) |

(34.1) |

(16.8) |

| Gross debt (US$ million) |

60,311 |

59,132 |

62,600 |

60,311 |

62,600 |

2.0 |

(3.7) |

(3.7) |

| Net debt (US$ million) |

52,240 |

44,251 |

44,698 |

52,240 |

44,698 |

18.1 |

16.9 |

16.9 |

| Net debt/LTM Adjusted EBITDA ratio |

1.29 |

0.95 |

0.85 |

1.29 |

0.85 |

35.8 |

51.8 |

51.8 |

| Average commercial selling rate for U.S. dollar |

5.84 |

5.55 |

4.95 |

5.39 |

4.99 |

5.2 |

18.0 |

8.0 |

| Brent crude (US$/bbl) |

74.69 |

80.18 |

84.05 |

80.76 |

82.62 |

(6.8) |

(11.1) |

(2.3) |

| Price of basic oil products - Domestic Market (US$/bbl) |

83.30 |

88.10 |

104.30 |

89.57 |

101.05 |

(5.4) |

(20.1) |

(11.4) |

| TRI (total recordable injuries per million men-hour frequency rate) |

- |

- |

- |

0.70 |

0.80 |

- |

- |

(12.5) |

| ROCE (Return on Capital Employed) |

7.2% |

9.2% |

11.2% |

7.2% |

11.2% |

-2 p.p. |

-4 p.p. |

-4 p.p. |

| (*) See reconciliation of net income and Adjusted EBITDA in the One-off events section. |

| |

PETROBRAS | Performance Report | 4Q24 | 8 |

Consolidated results

Consolidated results

In 2024, Petrobras posted strong cash

generation, evidencing its financial strength while maintaining its commitment to investments and shareholders remuneration.

Throughout 2024, the external environment

was marked by a 2% decline in Brent prices and a 39% reduction in diesel crackspreads. Despite these factors, Petrobras achieved Adjusted

EBITDA without one-off events of US$ 45.9 billion.

Adjusted EBITDA without one-off events

in 2024 was 17% lower than in 2023, reflecting a deterioration in the external environment with lower oil prices and international margins

in the refining segment, as well as lower oil production volumes.

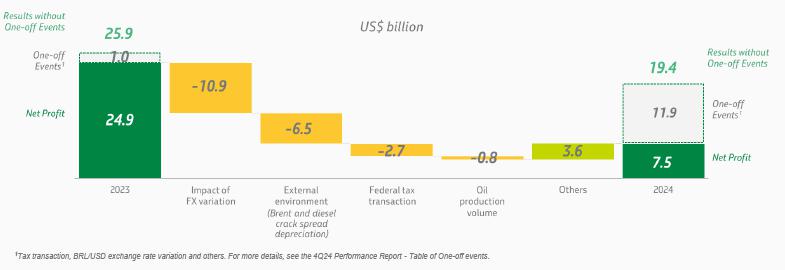

Net income for 2024 amounted to US$ 7.5

billion, a 70% reduction compared to 2023, mainly due to an accounting effect that does not affect our cash or equity: the exchange rate

variation of debts between Petrobras and its overseas subsidiaries. Without one-off events, net profit would have been US$ 19.4 billion.

Due to the depreciation of the final exchange

rate, the financial result for 2024 was negative by US$ 15.1 billion. In addition, financial expenses associated with the Tax Transaction

were recognized in 2Q24. The tax transaction was positive for the company as it ended billion-dollar disputes that caused great uncertainty

for the company’s cash position. Petrobras shares rose more than 3% following the announcement of the transaction.

In 4Q24, the company recorded a loss of

US$ 2.8 billion, mainly reflecting the impact of foreign exchange rate depreciation, which, as mentioned, is a purely accounting event,

as well as higher provisions, with no cash effect, in operating expenses, partially offset by lower income tax and social contribution

(IR/CSLL). Without one-off events, Petrobras would have recorded a profit of US$ 3.1 billion.

| |

PETROBRAS | Performance Report | 4Q24 | 9 |

One-off events

One-off events

Table 2 – One-off events

| |

|

|

|

|

|

Variation (%) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Net income (loss) |

(2,766) |

5,891 |

6,282 |

7,605 |

24,995 |

− |

− |

(69.6) |

| Items with one-off events |

(8,880) |

601 |

(2,092) |

(17,063) |

(1,139) |

− |

324.5 |

1398.1 |

| Items with one-off events that do not affect Adjusted EBITDA |

(6,166) |

735 |

(577) |

(11,576) |

1,605 |

− |

968.6 |

− |

| Impairment of assets and investments |

(1,579) |

(3) |

(2,208) |

(1,518) |

(2,682) |

52533.3 |

(28.5) |

(43.4) |

| Gains and losses on disposal/write-offs of assets |

39 |

(97) |

145 |

228 |

1,295 |

− |

(73.1) |

(82.4) |

| Results from co-participation agreements in bid areas |

156 |

− |

237 |

259 |

284 |

− |

(34.2) |

(8.8) |

| Effect of the tax transaction on net finance income (expense) |

(13) |

110 |

− |

(2,052) |

− |

− |

− |

− |

| Discount and premium on repurchase of debt securities |

(14) |

24 |

34 |

10 |

76 |

− |

− |

(86.8) |

| Gains/(losses) with foreign exchange variation Real x U.S. dollar (*) |

(4,755) |

701 |

979 |

(8,503) |

2,396 |

− |

− |

− |

| Legal agreement with Eletrobras - compulsory loans |

− |

− |

236 |

− |

236 |

− |

− |

− |

| Other items with one-off events |

(2,714) |

(134) |

(1,515) |

(5,487) |

(2,744) |

1925.4 |

79.1 |

100.0 |

| Voluntary Separation Plan |

− |

11 |

2 |

8 |

8 |

− |

− |

− |

| Collective bargaining agreement |

− |

− |

(211) |

(8) |

(217) |

− |

− |

(96.3) |

| Amounts recovered from Lava Jato investigation |

22 |

31 |

10 |

60 |

109 |

(29.0) |

120.0 |

(45.0) |

| Gains/(losses) on decommissioning of returned/abandoned areas |

(2,575) |

− |

(1,179) |

(2,584) |

(1,195) |

− |

118.4 |

116.2 |

| Gains/(losses) related to legal proceedings |

(188) |

(287) |

(125) |

(996) |

(797) |

(34.5) |

50.4 |

25.0 |

| Effect of the tax transaction on other taxes |

14 |

105 |

− |

(671) |

− |

(86.7) |

− |

− |

| Equalization of expenses - Production Individualization Agreements |

13 |

(5) |

(12) |

(16) |

(50) |

− |

− |

(68.0) |

| Gains/(losses) arising from actuarial review of health care plan |

− |

− |

− |

(1,291) |

− |

− |

− |

− |

| Gains/(losses) with the transfer of rights on concession agreements |

− |

11 |

− |

11 |

− |

− |

− |

− |

| Compensation for the termination of a vessel charter agreement |

− |

− |

− |

− |

(317) |

− |

− |

− |

| Export tax on crude oil |

− |

− |

− |

− |

(285) |

− |

− |

− |

| Net effect of items with one-off events on IR/CSLL |

3,017 |

(206) |

709 |

5,224 |

390 |

− |

325.5 |

1239.5 |

| Net income without one-off events |

3,097 |

5,496 |

7,665 |

19,444 |

25,744 |

(43.6) |

(59.6) |

(24.5) |

| Shareholders of Petrobras |

3,083 |

5,475 |

7,642 |

19,370 |

25,634 |

(43.7) |

(59.7) |

(24.4) |

| Non-controlling interests |

14 |

21 |

23 |

74 |

110 |

(33.3) |

(39.1) |

(32.7) |

| Adjusted EBITDA |

7,165 |

11,480 |

13,470 |

40,399 |

52,414 |

(37.6) |

(46.8) |

(22.9) |

| Items with one-off events |

(2,714) |

(134) |

(1,515) |

(5,487) |

(2,744) |

1925.4 |

79.1 |

100.0 |

| Adjusted EBITDA without one-off events |

9,879 |

11,614 |

14,985 |

45,886 |

55,158 |

(14.9) |

(34.1) |

(16.8) |

| (*) As of 4Q24, the line "gains/(losses) with foreign exchange variation Real x U.S. dollar" was added to the table above to calculate adjusted EBITDA and net income without one-off events. For comparative purposes, the periods previously disclosed were updated. |

In management's view, the one-off events

presented above, although related to the Company's business, were highlighted as complementary information for a better understanding

and evaluation of the result. Such items do not necessarily occur in all periods and shall be disclosed when relevant.

| |

PETROBRAS | Performance Report | 4Q24 | 10 |

Capex

Capex

Table 3 - Capex

| |

|

|

|

|

|

Variation (%) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Exploration & Production |

4,899 |

3,773 |

2,752 |

13,912 |

10,283 |

29.8 |

78.0 |

35.3 |

| Refining, Transportation and Marketing |

538 |

452 |

530 |

1,799 |

1,559 |

18.8 |

1.5 |

15.4 |

| Gas & Low Carbon Energies |

129 |

97 |

134 |

426 |

277 |

33.7 |

(3.7) |

53.9 |

| Others |

163 |

111 |

142 |

461 |

413 |

47.2 |

15.2 |

11.7 |

| Subtotal |

5,729 |

4,433 |

3,558 |

16,598 |

12,532 |

29.2 |

61.0 |

32.4 |

| Signature bonus |

2 |

21 |

− |

23 |

141 |

(91.9) |

− |

(83.9) |

| Total |

5,731 |

4,454 |

3,558 |

16,621 |

12,673 |

28.7 |

61.1 |

31.2 |

n 2024, Capex totaled $16.6 billion,

representing a 31% increase compared to 2023, mainly due to higher spending on major pre-salt projects, especially in the new production

systems of the Búzios field and the revitalization of the Marlim field.

The investment made in 2024 was 15% above

the guidance disclosed in August 2024, largely due to the recovery from the discrepancy observed in the first half of the year between

the physical progress of activities and the financial progress based on the fulfillment of key delivery milestones of the five owned FPSOs

under construction for the Búzios field.

The company expected this mismatch to

be reduced throughout 2025. However, it took strong action to seek alternatives to fully resolve this issue still in 2024, implementing

various contractual diligence measures to ensure the completion of physical delivery packages that enable payment milestones. These efforts

allowed us to accelerate financial progress in the last quarter and recover a significant portion of the shortfall attributable to the

under-execution of CAPEX compared to the disclosed plan.

The reduction of the physical-financial

mismatch and the greater alignment of incentives with suppliers for achieving the milestones are fundamental vectors for bringing the

new systems into production as planned, mitigating risks of delays and increasing the potential for anticipations.

We reaffirm Petrobras' management commitment

to continuously seek initiatives that support the timely commissioning of production systems established in the strategic plan. This is

exemplified by the successful startup of the FPSOs Maria Quitéria, Marechal Duque de Caxias, and Almirante Tamandaré in

the Jubarte, Mero, and Búzios fields, respectively, which were achieved either ahead of schedule or in accordance with the deadlines

set in the 2024-28+ Strategic Plan timeline.

The company reiterates the proposed Capex

guidance for the year 2025 (under the exchange rate assumptions of the Business Plan) of $18.5 billion, with a variation of +/- 10%, considering

the potential for value generation with the advancement of the Capex vector over the coming years, without this resulting in an increase

in the total value projected for executing the projects during the period from 2024 to 2029 (Guidance + PN 2025-29). However, we will

maintain the most likely dates disclosed for the entry of the systems and the CAPEX of the PN 2025-29, considering the intrinsic risks

and uncertainties related to the implementation of the projects, contained in the margin of +/- 10%.

In 4Q24 2024, Capex totaled $5.7 billion,

29% higher than 2Q24, mainly due to higher spending on major pre-salt projects, especially in the new production systems of the Búzios

field.

In the Exploration and Production segment,

4Q24 Capex amounted to $4.9 billion, 30% higher than in 3Q24, and were mainly concentrated on: (i) developing production in the Santos

Basin pre-salt area ($2.8 billion); (ii) developing production in the Campos Basin pre/post-salt areas ($0.9 billion); and (iii) exploratory

investments ($0.3 billion). The increase compared to the previous quarter is due to progress in the construction of new production systems

in the Búzios field, with a focus on investments associated with the arrival of equipment at platforms P-80, P-82, and P-83, and

the construction of modules for units P-78 and P-79.

| |

PETROBRAS | Performance Report | 4Q24 | 11 |

Capex

In the Refining, Transportation, and Marketing

segment, Capex totaled $0.5 billion in 4Q24, a growth of 19% compared to 3Q24. This increase occurred due to higher spending on scheduled

refinery stoppages, particularly at RNEST, REPLAN, and REGAP, in addition to progress on the RNEST Train 1 project and small-scale refinery

projects.

In the Gas and Low-Carbon Energies segment,

Capex totaled $0.1 billion in 4Q24, 34% higher than 3Q24. The increase was mainly due to the maintenance and operational continuity of

thermal plants, as well as spending on infrastructure maintenance of GASBOL in TBG.

Additionally, in 4Q24, US$ 2 million was

recognized related to signing bonuses for 26 blocks (partnership with Shell) in the Pelotas Basin.

It is worth highlighting the start of

operations in 4Q24 of the leased FPSOs Marechal Duque de Caxias (Mero 3) and Maria Quitéria (Integrado Parque das Baleias), with

total lease costs amounting to US$ 3.5 billion (Petrobras' share). Similarly to the owned units, leased FPSOs are recognized as assets

of the Company and represent an investment effort to expand production capacity with new units. However, they are not included in Capex.

The following table presents the main

information about the new oil and gas production systems, already contracted.

| |

PETROBRAS | Performance Report | 4Q24 | 12 |

Capex

Table 4 – Main projects

| Unit |

Start-up |

FPSO capacity (bbl/day) |

Petrobras Actual Investment

(US$ bn) |

Petrobras Total Investment

(US$ bn) (1) |

Petrobras Stake |

Status |

|

Mero 2

FPSO Sepetiba

(Chartered unit) |

2023 |

180,000 |

0.8 |

1.0 |

38.6% |

Project in execution phase with production system in operation.

13 wells drilled and 13 completed. |

|

Integrado Parque das Baleias (IPB)

FPSO Maria Quitéria

(Chartered unit) |

2024 |

100,000 |

1.1 |

1.9 |

100% |

Project in execution phase with production system in operation.

4 wells drilled and 3 completed. (2) |

|

Mero 3

FPSO Marechal Duque de Caxias

(Chartered unit) |

2024 |

180,000 |

0.5 |

0.9 |

38.6% |

Project in execution phase with production system in operation.

12 wells drilled and 11 completed. |

|

Búzios 7

FPSO Almirante Tamandaré

(Chartered unit) |

2025 |

225,000 |

1.2 |

2.0 |

88.99% |

Project in execution phase with production system in operation.

15 wells drilled and 14 completed. |

|

Búzios 6

P-78

(Owned unit) |

2025 |

180,000 |

2.2 |

5.2 |

88.99% |

Project in execution phase with production system under construction.

7 wells drilled and 4 completed. |

|

Mero 4

FPSO Alexandre de Gusmão

(Chartered unit) |

2025 |

180,000 |

0.2 |

1.3 |

38.6% |

Project in execution phase with production system in transit to Brazil.

8 wells drilled and 6 completed. |

|

Búzios 8

P-79

(Owned unit) |

2026 |

180,000 |

2.1 |

5.7 |

88.99% |

Project in execution phase with production system under construction.

9 wells drilled and 6 completed. |

|

Búzios 9

P-80

(Owned unit) |

2027 |

225,000 |

1.6 |

6.5 |

88.99% |

Project in execution phase with production system under construction.

3 wells drilled and 2 completed. |

|

Búzios 10

P-82

(Owned unit) |

2027 |

225,000 |

1.3 |

7.4 |

88.99% |

Project in execution phase with production system under construction.

1 well drilled. |

|

Búzios 11

P-83

(Owned unit) |

2027 |

225,000 |

1.0 |

6.8 |

88.99% |

Project in execution phase with production system under construction.

3 wells drilled and 1 completed. |

|

Raia Manta e Raia Pintada

FPSO Raia

(Non-operated project) |

2028 |

126,000 |

0.8 |

2,7 (3) |

30% |

Project in execution phase with production system under construction. |

|

Atapu 2

P-84 |

2029 |

225,000 |

0.3 |

6.4 |

65.7% |

Project in execution phase with production system under construction. |

|

Sépia 2

P-85 |

2030 |

225,000 |

0.2 |

4.7 |

55.3% |

Project in execution phase. |

|

(1) Total investment with the 2025-29+ Strategic Plan assumptions

and Petrobras work interest (WI). Chartered units leases are not included.

(2) Production Unit for revitalization project. Refers only to new wells.

The scope of the project also includes the relocation of some wells of the units being decommissioned.

(3) Total investment considering Petrobras work interest (WI). It is included

the FPSO, contracted on a lump sum turnkey modality, which includes engineering, procurement, construction and installation for the unit.

The contractor will also provide FPSO operation and maintenance services during the first year from the start of production. |

| |

PETROBRAS | Performance Report | 4Q24 | 13 |

Liquidity and capital resources

Liquidity and capital resources

Table 5 - Liquidity and capital resources

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

| Adjusted cash and cash equivalents at the beginning of period |

14,881 |

13,470 |

17,272 |

17,902 |

12,283 |

| Government bonds, bank deposit certificates and time deposits with maturities of more than 3 months at the beginning of period (*) |

(6,187) |

(5,586) |

(5,162) |

(5,175) |

(4,287) |

| Cash and cash equivalents at the beginning of period |

8,694 |

7,884 |

12,110 |

12,727 |

7,996 |

| Net cash provided by operating activities |

8,204 |

11,307 |

11,669 |

37,984 |

43,212 |

| Net cash (used in) provided by investing activities |

(3,271) |

(4,742) |

(3,228) |

(13,369) |

(7,955) |

| Acquisition of PP&E and intangible assets |

(4,429) |

(4,443) |

(3,594) |

(14,644) |

(12,114) |

| Acquisition of equity interests |

(9) |

(7) |

(2) |

(22) |

(24) |

| Proceeds from disposal of assets - Divestment |

72 |

25 |

42 |

863 |

3,606 |

| Financial compensation from co-participation agreements |

− |

− |

− |

397 |

391 |

| Divestment (investment) in marketable securities |

1,070 |

(374) |

313 |

(109) |

98 |

| Dividends received |

25 |

57 |

13 |

146 |

88 |

| (=) Net cash provided by operating and investing activities |

4,933 |

6,565 |

8,441 |

24,615 |

35,257 |

| Net cash used in financing activities |

(9,654) |

(5,895) |

(7,871) |

(33,088) |

(30,700) |

| Changes in non-controlling interest |

23 |

(232) |

103 |

(84) |

1 |

| Net financings |

(2,122) |

(1,457) |

(1,207) |

(6,325) |

(3,961) |

| Proceeds from finance debt |

576 |

986 |

910 |

2,129 |

2,210 |

| Repayments |

(2,698) |

(2,443) |

(2,117) |

(8,454) |

(6,171) |

| Repayment of lease liability |

(2,099) |

(1,913) |

(1,792) |

(7,895) |

(6,286) |

| Dividends paid to shareholders of Petrobras |

(5,456) |

(2,293) |

(4,436) |

(18,327) |

(19,670) |

| Share repurchase program |

− |

− |

(538) |

(380) |

(735) |

| Dividends paid to non-controlling interests |

− |

− |

(1) |

(77) |

(49) |

| Effect of exchange rate changes on cash and cash equivalents |

(702) |

140 |

47 |

(983) |

174 |

| Cash and cash equivalents at the end of period |

3,271 |

8,694 |

12,727 |

3,271 |

12,727 |

| Government bonds, bank deposit certificates and time deposits with maturities of more than 3 months at the end of period (*) |

4,800 |

6,187 |

5,175 |

4,800 |

5,175 |

| Adjusted cash and cash equivalents at the end of period |

8,071 |

14,881 |

17,902 |

8,071 |

17,902 |

| Reconciliation of Free Cash Flow |

|

|

|

|

|

| Net cash provided by operating activities |

8,204 |

11,307 |

11,669 |

37,984 |

43,212 |

| Acquisition of PP&E and intangible assets |

(4,429) |

(4,443) |

(3,594) |

(14,644) |

(12,114) |

| Acquisition of equity interests |

(9) |

(7) |

(2) |

(22) |

(24) |

| Free cash flow (**) |

3,766 |

6,857 |

8,073 |

23,318 |

31,074 |

|

(*) Includes government bonds, bank deposit certificates and time deposits

of companies classified as held for sale.

(**) Free cash flow (FCF) is in accordance with the new Shareholder Remuneration

Policy (“Policy”) approved on 07/28/2023 and corresponds to operating cash flow minus acquisitions of property, plant and

equipment, intangible assets and equity interests. For comparative purposes, figures prior to 2Q23 have been adjusted in accordance with

the new Policy. |

| |

PETROBRAS | Performance Report | 4Q24 | 14 |

Liquidity and capital resources

As of December 31, 2024, cash and cash equivalents

totaled US$ 3.3 billion and adjusted cash and cash equivalents totaled US$ 8.1 billion.

In 4Q24, funds generated by operating activities

reached US$ 38.0 billion and free cash flow totaled US$ 23.3 billion. This level of cash generation was used to: (a) shareholders remuneration

(US$ 18.7 billion), (b) investments (US$ 14.6 billion), (c) lease liabilities amortization (US$ 7.9 billion), and (d) amortization of

principal and interest due in the period (US$ 8.5 billion).

In 2024, the company paid off various loans

and financings, amounting to US$ 8.5 billion, and the highlight was the repurchase and redemption of US$ 2.5 billion of bonds in the international

capital markets and the prepayment of US$ 250 million in loans in the international banking market.

In 2024, the company raised US$ 2.1 billion,

notably by offering bonds on the international capital markets (Global Notes) amounting to US$ 1.0 billion maturing in 2035 and raising

funds in the national banking market amounting to US$ 1.1 billion.

| |

PETROBRAS | Performance Report | 4Q24 | 15 |

Debt indicators

Debt indicators

As of December 31, 2024, gross debt reached

$60.3 billion, a decrease of 3.8% compared to December 31, 2023.

Average maturity increased from 11.38

years on December 31, 2023, to 12.52 years on December 31, 2024, and the average cost varied from 6.4% p.a. to 6.8% p.a. during the same

period.

The gross debt/adjusted EBITDA ratio was

1.49x on 12/31/2024, compared to 1.19x on 12/31/2023.

On 12/31/2024, the net debt reached $52.2

billion, an increase of 16.9% compared to 12/31/2023.

Table 6 – Debt indicators

| US$ million |

12.31.2024 |

09.30.2024 |

Δ % |

12.31.2023 |

| Financial Debt |

23,162 |

25,756 |

(10.1) |

28,801 |

| Capital Markets |

14,490 |

16,005 |

(9.5) |

17,514 |

| Banking Market |

6,519 |

7,490 |

(13.0) |

8,565 |

| Development banks |

508 |

587 |

(13.5) |

698 |

| Export Credit Agencies |

1,508 |

1,517 |

(0.6) |

1,870 |

| Others |

137 |

157 |

(12.7) |

154 |

| Finance leases |

37,149 |

33,376 |

11.3 |

33,799 |

| Gross debt |

60,311 |

59,132 |

2.0 |

62,600 |

| Adjusted cash and cash equivalents |

8,071 |

14,881 |

(45.8) |

17,902 |

| Net debt |

52,240 |

44,251 |

18.1 |

44,698 |

| Net Debt/(Net Debt + Market Cap) - Leverage |

39% |

33% |

18.2 |

30% |

| Average interest rate (% p.a.) |

6.8 |

6.6 |

3.0 |

6.4 |

| Weighted average maturity of outstanding debt (years) |

12.52 |

11.57 |

8.2 |

11.38 |

| Net debt/LTM Adjusted EBITDA ratio |

1.29 |

0.95 |

35.8 |

0.85 |

| Gross debt/LTM Adjusted EBITDA ratio |

1.49 |

1.27 |

17.9 |

1.19 |

| |

PETROBRAS | Performance Report | 4Q24 | 16 |

Results by business segment

Results by business segment

Exploration and Production

Table 7 – E&P results

| |

|

|

|

|

|

Variation (%) (*) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Sales revenues |

13,388 |

15,383 |

18,506 |

60,516 |

66,880 |

(13.0) |

(27.7) |

(9.5) |

| Gross profit |

7,386 |

9,404 |

10,909 |

35,693 |

39,641 |

(21.5) |

(32.3) |

(10.0) |

| Operating expenses |

(4,236) |

(1,222) |

(3,778) |

(7,639) |

(5,615) |

246.6 |

12.1 |

36.0 |

| Operating income |

3,150 |

8,182 |

7,131 |

28,054 |

34,026 |

(61.5) |

(55.8) |

(17.6) |

| Net income (loss) attributable to the shareholders of Petrobras |

2,094 |

5,416 |

4,734 |

18,593 |

22,453 |

(61.3) |

(55.8) |

(17.2) |

| Adjusted EBITDA of the segment |

6,404 |

10,451 |

11,575 |

38,097 |

44,707 |

(38.7) |

(44.7) |

(14.8) |

| EBITDA margin of the segment (%) |

48 |

68 |

63 |

63 |

67 |

(20.1) |

(14.7) |

(4) |

| ROCE (Return on Capital Employed) (%) |

11.0 |

13.4 |

14.5 |

11.0 |

14.5 |

(2.4) |

(3.5) |

(3.5) |

| Average Brent crude (US$/bbl) |

74.69 |

80.18 |

84.05 |

80.76 |

82.62 |

(6.8) |

(11.1) |

(2.3) |

| Production taxes Brazil |

2,618 |

2,833 |

3,255 |

11,378 |

12,111 |

(7.6) |

(19.6) |

(6.1) |

| Royalties |

1,643 |

1,774 |

1,942 |

7,126 |

7,086 |

(7.4) |

(15.4) |

0.6 |

| Special participation |

966 |

1,050 |

1,304 |

4,216 |

4,981 |

(8.0) |

(25.9) |

(15.4) |

| Retention of areas |

9 |

9 |

9 |

36 |

44 |

− |

− |

(18.2) |

| Lifting cost Brazil (US$/boe) |

6.34 |

5.78 |

5.52 |

6.05 |

5.59 |

9.8 |

14.8 |

8.3 |

| Pre-salt |

4.01 |

3.78 |

3.78 |

3.91 |

3.67 |

6.2 |

6.1 |

6.4 |

| Deep and ultra-deep post-salt |

17.52 |

16.57 |

12.12 |

16.43 |

12.52 |

5.7 |

44.5 |

31.2 |

| Onshore and shallow waters |

19.00 |

16.74 |

16.15 |

17.22 |

15.67 |

13.5 |

17.7 |

9.9 |

| Lifting cost + Leases |

9.11 |

8.23 |

7.79 |

8.56 |

7.66 |

10.6 |

16.9 |

11.8 |

| Pre-salt |

6.65 |

6.10 |

6.13 |

6.32 |

5.77 |

9.1 |

8.5 |

9.5 |

| Deep and ultra-deep post-salt |

21.56 |

20.41 |

14.37 |

20.03 |

14.84 |

5.6 |

50.0 |

35.0 |

| Onshore and shallow waters |

19.00 |

16.74 |

16.15 |

17.22 |

15.67 |

13.5 |

17.7 |

9.9 |

| Lifting cost + Production taxes |

19.21 |

19.49 |

19.78 |

19.73 |

19.69 |

(1.4) |

(2.9) |

0.2 |

| Lifting cost + Production taxes + Leases |

21.97 |

21.94 |

22.05 |

22.24 |

21.76 |

0.1 |

(0.4) |

2.2 |

| (*) EBITDA margin and ROCE variations in percentage points. |

In 2024, the E&P gross profit

was US$ 35.7 billion, a 10% decrease compared to 2023, mainly due to the decrease

in Brent prices and lower production. Nevertheless, we met the oil production targets established in the Strategic Plan 2024-2028+, considering

the range of ± 4%.

The annual operating profit was

US$ 28.1 billion, 18% lower than in 2023, mainly due to higher provisions expenses related to decommissioning of fields that are in the

process of being returned and tax expenses recorded in 2Q24, as well as lower revenue from divestments.

| |

PETROBRAS | Performance Report | 4Q24 | 17 |

Results by business segment

In 4Q24, the E&P gross profit

was US$ 7.4 billion, a 21% decrease compared to 3Q24, mainly due to the decrease in Brent prices and lower production.

The operating profit in 4Q24 was

US$ 3.1 billion, 62% lower than in 3Q24, reflecting the increase in operating expenses, mainly due to higher provisions related to decommissioning

of fields that are in the process of being returned.

The 2024 lifting cost, excluding

government participation and leases, was US$ 6.05/boe, representing a 8% increase compared to 2023 (US$ 5.59/boe), primarily due to higher

integrity expenses (especially on platform maintenance), subsea inspections and well interventions, associated with higher gas flow expenses

due to the startup of the Route 3 gas pipeline. These increases were offset by the devaluation of the Brazilian Real against the Dollar,

active portfolio management (including divestments), the production ramp-up of new systems that came into operation in 2023 (FPSO Almirante

Barroso, FPSO Anna Nery, and FPSO Anita Garibaldi), the startup of production from new systems in 2024 (FPSO Sepetiba, Maria Quitéria,

and Duque de Caxias), and the increase in the P-71 production capacity.

In 4Q24, we recorded a 10% increase

in lifting cost compared to 3Q24, mainly due to higher gas flow expenses associated with the startup of the Rota 3 pipeline, increased

expenses on well interventions in the Campos Basin, particularly in the Barracuda, Caratinga, Marlim Sul, and Roncador fields, and the

impact of lower production due to maintenance shutdowns in the Búzios field. These effects were partially offsets by the devaluation

of the Brazilian Real against the Dollar.

In the pre-salt, the lifting cost

increased by 6%, primarily due to the lower production in the Búzios field caused by production shutdowns, as well as higher gas

flow expenses resulting from the increased volume being transported with the startup of the Rota 3 pipeline. These effects were partially

offsets by the devaluation of the Brazilian Real against the Dollar.

In the post-salt, there was a

6% increase due to the intensification of well interventions in the Campos Basin, particularly in the Barracuda, Caratinga, Marlim Sul,

and Roncador fields, partially offset by the effect of the exchange rate depreciation.

In the onshore and shallow water

assets, there was a 14% increase due to rising costs associated with the intensification of well interventions in the Bahia onshore fields,

partially offset by the effect of the exchange rate depreciation.

| |

PETROBRAS | Performance Report | 4Q24 | 18 |

Results by business segment

Refining, Transportation and Marketing

Table 8 - RTM results

| |

|

|

|

|

|

Variation (%) (1) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Sales revenues |

19,291 |

21,739 |

25,278 |

85,281 |

94,868 |

(11.3) |

(23.7) |

(10.1) |

| Gross profit |

1,498 |

1,236 |

2,175 |

6,445 |

9,169 |

21.2 |

(31.1) |

(29.7) |

| Operating expenses |

(939) |

(781) |

(966) |

(3,257) |

(4,086) |

20.2 |

(2.8) |

(20.3) |

| Operating Income |

559 |

455 |

1,209 |

3,188 |

5,083 |

22.9 |

(53.8) |

(37.3) |

| Net income (loss) attributable to the shareholders of Petrobras |

15 |

255 |

711 |

1,324 |

3,036 |

(94.1) |

(97.9) |

(56.4) |

| Adjusted EBITDA of the segment |

1,500 |

1,078 |

1,963 |

5,932 |

8,052 |

39.1 |

(23.6) |

(26.3) |

| EBITDA margin of the segment (%) |

8 |

5 |

8 |

7 |

8 |

3 |

− |

(2) |

| ROCE (Return on Capital Employed) (%)(2) |

2.5 |

3.2 |

5.6 |

2.5 |

5.6 |

(0.7) |

(3.1) |

(3.1) |

| Refining cost (US$ / barrel) - Brazil |

2.48 |

2.84 |

2.75 |

2.65 |

2.38 |

(12.7) |

(9.8) |

11.3 |

| Price of basic oil products - Domestic Market (US$/bbl) |

83.30 |

88.10 |

104.30 |

89.57 |

101.05 |

(5.4) |

(20.1) |

(11.4) |

|

(1) Changes in EBITDA and ROCE margins in percentage points.

(2) Number for 3Q24 and 4Q23 revised due to the reclassification of fertilizer

assets that left G&EBC and were migrated to RTC in 2023 and, until then, were not fully reflected in the ROCE calculation. |

In 2024, the gross profit was

US$ 2.7 billion lower than in 2023, reflecting a deterioration in the external environment with the reduction of international margins

in the refining segment. Adjusting for the effect of inventory turnover of US$ 1.6 billion in 2024 and US$ 0.5 billion in 2023, the gross

profit would have been US$ 4.9 billion in 2024 and US$ 9.6 billion in 2023.

The sales volume was lower, mainly

for diesel, due to the increase in imports by third parties, primarily from Russia, and the rise in the mandatory blending content of

biodiesel in type B diesel and gasoline, reflecting the recovery of hydrated ethanol's share compared to C gasoline in flex-fuel vehicles.

The operating income in 2024 was

lower than in 2023, reflecting the reduction in gross profit, partially offset by lower operating expenses, mainly due to reduced selling

expenses resulting from the lower volume.

In 2024, the refining cost in

dollars per barrel was 11% higher than in 2023. This was mainly due to higher personnel expenses related to the collective labor agreement

and increased costs with materials and services related to maintenance and conservation. The processed throughput was slightly higher

in the year-over-year comparison (+0.8%), which, combined with the exchange rate effect, partially offset the increase in absolute costs.

Regarding the comparison between

the quarters, the RTM gross profit was 21% higher than that of 3Q24, mainly due to higher margins on oil products in the domestic market.

Adjusting for the effect of inventory turnover of $383 million in Q4 2024 and $186 million in Q3 2024, the RTM gross profit would have

been US$ 1,115 million in Q4 2024 and US$ 1,050 million in Q3 2024.

It is worth noting that in Q4

2024, higher margins were observed in the domestic market, mainly for diesel, following the increase in international margins for this

oil product. The sales volume in the domestic market was lower, primarily for diesel, due to seasonality with the end of the grain harvest

and reduced industrial activity, and for LPG due to higher temperatures and lower industrial activity. On the other hand, there was a

higher sales volume of gasoline and jet fuel, driven by the seasonality of the year-end holiday period.

In 4Q24, the operating income

was 23% higher than in Q3 2024, reflecting the increase in gross profit, partially offset by the rise in operating expenses.

Finally, in 4Q24, the refining

cost in dollars per barrel was 13% lower than in 3Q24. There were notable reductions in expenses with materials and services related to

the maintenance and conservation of operational units, along with the exchange rate effect that contributed to the decrease in the absolute

dollar value during the period. Throughput did not vary significantly between the quarters.

| |

PETROBRAS | Performance Report | 4Q24 | 19 |

Results by business segment

Gas and Low Carbon Energies

Table 9 – G&LCE results

| |

|

|

|

|

|

Variation (%) (1) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Sales revenues |

2,557 |

2,341 |

2,859 |

9,518 |

11,109 |

9.2 |

(10.6) |

(14.3) |

| Gross profit |

1,170 |

970 |

1,433 |

4,487 |

5,424 |

20.6 |

(18.4) |

(17.3) |

| Operating expenses |

(940) |

(801) |

(934) |

(3,497) |

(3,384) |

17.4 |

0.6 |

3.3 |

| Operating income |

230 |

169 |

499 |

990 |

2,040 |

36.1 |

(53.9) |

(51.5) |

| Net income (loss) attributable to the shareholders of Petrobras |

152 |

109 |

308 |

682 |

1,286 |

39.4 |

(50.6) |

(47.0) |

| Adjusted EBITDA of the segment |

368 |

299 |

715 |

1,529 |

2,694 |

23.1 |

(48.5) |

(43.2) |

| EBITDA margin of the segment (%) |

14 |

13 |

25 |

16 |

24 |

2 |

(11) |

(8) |

| ROCE (Return on Capital Employed) (%) (2) |

4.2 |

6.2 |

10.7 |

4.2 |

10.7 |

(2.0) |

(6.5) |

(6.5) |

| Natural gas sales price - Brazil (US$/bbl) |

57.79 |

59.61 |

62.60 |

62.25 |

68.22 |

(3.1) |

(7.7) |

(8.8) |

| Natural gas sales price - Brazil (US$/MMBtu) |

9.74 |

10.05 |

10.56 |

10.50 |

11.50 |

(3.1) |

(7.8) |

(8.7) |

| Fixed revenues from power auctions (3)(4) |

57 |

61 |

89 |

182 |

258 |

(8.0) |

(36.6) |

(29.3) |

| Average electricity sales price (US$/MWh) (4)(5) |

73.55 |

28.11 |

18.63 |

62.83 |

14.23 |

161.7 |

294.8 |

341.7 |

|

(1) EBITDA margin and ROCE variations in percentage points.

(2) 3Q24 and 4Q23 figure revised due to the reclassification of fertilizer

assets that left the G&LCE and were migrated to the RTM in 2023 and, until then, were not fully reflected in the ROCE calculation.

(3) The fixed revenue from auctions takes into account the remuneration

for thermal availability and inflexible electricity committed in auctions.

(4) For the current period, the figures for the Energy segment are subject

to possible changes once the final report from the Chamber of Electric Energy Commercialization - CCEE is issued.

(5) Previous quarter number revised after the issuance of the final report

from the Chamber of Electric Energy Commercialization - CCEE.

|

In 2024, the gross profit was

17% lower than in 2023, reflecting lower volumes and gas selling prices, resulting from the opening of the natural gas market, the reduction

in market share and the measures taken to preserve Petrobras's competitiveness, such as the performance premium that has been implemented

since June. The terminations of energy contracts, both in the regulated and free markets, also contributed to the drop in the annual gross

profit.

On the other hand, in 4Q24, the

segment's gross profit was 21% higher than in 3Q24, due to the accounting of revenues from annual contractual commitments in December

2024. This increase in revenues offset the reduction in the average selling price of natural gas, resulting from exchange rate fluctuations

and lower Brent prices.

| |

PETROBRAS | Performance Report | 4Q24 | 20 |

Reconciliation of Adjusted EBITDA

Reconciliation of Adjusted EBITDA

EBITDA is an indicator calculated as

the net income for the period plus taxes on profit, net financial result, depreciation and amortization. Petrobras announces EBITDA, as

authorized by CVM Resolution No. 156, of June 2022.

In order to reflect the management view

regarding the formation of the company's current business results, EBITDA is also presented adjusted (Adjusted EBITDA) as a result of:

results in equity-accounted investments; impairment, results with co-participation agreement in production fields and gains/losses on

disposal/write-offs of assets.

Adjusted EBITDA, reflecting the sum

of the last twelve months (Last Twelve Months), also represents an alternative to the company's operating cash generation. This measure

is used to calculate the Gross Debt and Net Debt to Adjusted EBITDA metric, helping to evaluate the company's leverage and liquidity.

EBITDA and adjusted EBITDA are not provided

for in International Financial Reporting Standards (IFRS) and should not serve as a basis for comparison with those disclosed by other

companies and should not be considered as a substitute for any other measure calculated in accordance with IFRS. These measures should

be considered in conjunction with other measures and indicators for a better understanding of the company's performance and financial

condition.

Table 10 - Reconciliation of Adjusted EBITDA

| |

|

|

|

|

|

Variation (%) (*) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Net income (loss) |

(2,766) |

5,891 |

6,282 |

7,605 |

24,995 |

− |

− |

(69.6) |

| Net finance income (expense) |

6,018 |

281 |

(295) |

15,107 |

2,333 |

2041.6 |

− |

547.5 |

| Income taxes |

(788) |

2,205 |

1,966 |

3,537 |

10,401 |

− |

− |

(66.0) |

| Depreciation, depletion and amortization |

2,996 |

2,983 |

3,632 |

12,479 |

13,280 |

0.4 |

(17.5) |

(6.0) |

| EBITDA |

5,460 |

11,360 |

11,585 |

38,728 |

51,009 |

(51.9) |

(52.9) |

(24.1) |

| Results of equity-accounted investments |

323 |

23 |

69 |

627 |

304 |

1304.3 |

368.1 |

106.3 |

| Impairment of assets (reversals), net |

1,577 |

− |

2,198 |

1,531 |

2,680 |

− |

(28.3) |

(42.9) |

| Results on disposal/write-offs of assets |

(39) |

97 |

(145) |

(228) |

(1,295) |

− |

(73.1) |

(82.4) |

| Results from co-participation agreements in bid areas |

(156) |

− |

(237) |

(259) |

(284) |

− |

(34.2) |

(8.8) |

| Adjusted EBITDA |

7,165 |

11,480 |

13,470 |

40,399 |

52,414 |

(37.6) |

(46.8) |

(22.9) |

| Adjusted EBITDA margin (%) |

34 |

49 |

50 |

44 |

51 |

(15.0) |

(16.0) |

(7.0) |

| (*) EBITDA Margin variations in percentage points. |

| |

PETROBRAS | Performance Report | 4Q24 | 21 |

Exhibits

Exhibits

Financial statements

Table 11 - Income statement - Consolidated

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

| Sales revenues |

20,815 |

23,366 |

27,107 |

91,416 |

102,409 |

| Cost of sales |

(10,832) |

(11,361) |

(12,453) |

(45,444) |

(48,435) |

| Gross profit |

9,983 |

12,005 |

14,654 |

45,972 |

53,974 |

| Selling expenses |

(1,080) |

(1,193) |

(1,329) |

(4,874) |

(5,038) |

| General and administrative expenses |

(440) |

(409) |

(454) |

(1,845) |

(1,594) |

| Exploration costs |

(198) |

(406) |

(154) |

(913) |

(982) |

| Research and development expenses |

(218) |

(195) |

(214) |

(789) |

(726) |

| Other taxes |

(108) |

(55) |

(247) |

(1,251) |

(890) |

| Impairment (losses) reversals, net |

(1,577) |

− |

(2,198) |

(1,531) |

(2,680) |

| Other income and expenses, net |

(3,575) |

(1,347) |

(2,036) |

(7,893) |

(4,031) |

| |

(7,196) |

(3,605) |

(6,632) |

(19,096) |

(15,941) |

| Operating income |

2,787 |

8,400 |

8,022 |

26,876 |

38,033 |

| Finance income |

434 |

491 |

588 |

1,954 |

2,169 |

| Finance expenses |

(1,072) |

(881) |

(1,047) |

(5,957) |

(3,922) |

| Foreign exchange gains (losses) and inflation indexation charges |

(5,380) |

109 |

754 |

(11,104) |

(580) |

| Net finance income (expense) |

(6,018) |

(281) |

295 |

(15,107) |

(2,333) |

| Results of equity-accounted investments |

(323) |

(23) |

(69) |

(627) |

(304) |

| Income (loss) before income taxes |

(3,554) |

8,096 |

8,248 |

11,142 |

35,396 |

| Income taxes |

788 |

(2,205) |

(1,966) |

(3,537) |

(10,401) |

| Net Income (loss) |

(2,766) |

5,891 |

6,282 |

7,605 |

24,995 |

| Net income (loss) attributable to: |

|

|

|

|

|

| Shareholders of Petrobras |

(2,780) |

5,870 |

6,259 |

7,528 |

24,884 |

| Non-controlling interests |

14 |

21 |

23 |

77 |

111 |

| |

PETROBRAS | Performance Report | 4Q24 | 22 |

Exhibits

Table 12 - Statement of financial position

– Consolidated

| ASSETS - US$ million |

12.31.2024 |

12.31.2023 |

| Current assets |

21,836 |

32,445 |

| Cash and cash equivalents |

3,271 |

12,727 |

| Marketable securities |

4,263 |

2,819 |

| Trade and other receivables, net |

3,566 |

6,135 |

| Inventories |

6,710 |

7,681 |

| Recoverable taxes |

1,966 |

1,178 |

| Assets classified as held for sale |

510 |

335 |

| Other current assets |

1,550 |

1,570 |

| Non-current assets |

159,809 |

184,622 |

| Long-term receivables |

20,610 |

26,798 |

| Trade and other receivables, net |

1,256 |

1,847 |

| Marketable securities |

582 |

2,409 |

| Judicial deposits |

11,748 |

14,746 |

| Deferred income taxes |

922 |

965 |

| Other recoverable taxes |

3,601 |

4,516 |

| Other non-current assets |

2,501 |

2,315 |

| Investments |

659 |

1,358 |

| Property, plant and equipment |

136,285 |

153,424 |

| Intangible assets |

2,255 |

3,042 |

| Total assets |

181,645 |

217,067 |

| |

|

|

| |

|

|

| LIABILITIES - US$ million |

12.31.2024 |

12.31.2023 |

| Current liabilities |

31,460 |

33,860 |

| Trade payables |

6,082 |

4,813 |

| Finance debt |

2,566 |

4,322 |

| Lease liability |

8,542 |

7,200 |

| Taxes payable |

4,684 |

5,466 |

| Dividends payable |

2,657 |

3,539 |

| Provision for decommissioning costs |

1,696 |

2,032 |

| Employee benefits |

2,315 |

2,932 |

| Liabilities related to assets classified as held for sale |

713 |

541 |

| Other current liabilities |

2,205 |

3,015 |

| Non-current liabilities |

90,835 |

104,232 |

| Finance debt |

20,596 |

24,479 |

| Lease liability |

28,607 |

26,599 |

| Income taxes payable |

530 |

299 |

| Deferred income taxes |

1,470 |

10,910 |

| Employee benefits |

10,672 |

15,579 |

| Provision for legal proceedings |

2,833 |

3,305 |

| |

PETROBRAS | Performance Report | 4Q24 | 23 |

| Provision for decommissioning costs |

24,507 |

21,171 |

| Other non-current liabilities |

1,620 |

1,890 |

| Shareholders' equity |

59,350 |

78,975 |

| Attributable to the shareholders of Petrobras |

59,106 |

78,583 |

| Share capital (net of share issuance costs) |

107,101 |

107,101 |

| Capital reserve and capital transactions |

29 |

410 |

| Profit reserves |

61,446 |

72,641 |

| Retained earnings (losses) |

− |

− |

| Accumulated other comprehensive deficit |

(109,470) |

(101,569) |

| Attributable to non-controlling interests |

244 |

392 |

| Total liabilities and shareholders' equity |

181,645 |

217,067 |

| |

PETROBRAS | Performance Report | 4Q24 | 24 |

Table 13 - Statement of cash flow –

Consolidated

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

| Cash flows from operating activities |

|

|

|

|

|

| Net income (loss) for the period |

(2,766) |

5,891 |

6,282 |

7,605 |

24,995 |

| Adjustments for: |

|

|

|

|

|

| Pension and medical benefits |

390 |

409 |

389 |

2,934 |

1,542 |

| Results of equity-accounted investments |

323 |

23 |

69 |

627 |

304 |

| Depreciation, depletion and amortization |

2,996 |

2,983 |

3,632 |

12,479 |

13,280 |

| Impairment of assets (reversals), net |

1,577 |

− |

2,198 |

1,531 |

2,680 |

| Inventory write down (write-back) to net realizable value |

− |

2 |

(3) |

(42) |

(7) |

| Allowance (reversals) for credit loss on trade and other receivables, net |

206 |

6 |

(9) |

260 |

40 |

| Exploratory expenditure write-offs |

68 |

309 |

11 |

482 |

421 |

| Gain on disposal/write-offs of assets |

(39) |

97 |

(145) |

(228) |

(1,295) |

| Foreign exchange, indexation and finance charges |

6,264 |

168 |

(316) |

15,407 |

2,498 |

| Income taxes |

(788) |

2,205 |

1,966 |

3,537 |

10,401 |

| Revision and unwinding of discount on the provision for decommissioning costs |

2,803 |

242 |

1,390 |

3,584 |

2,052 |

| Results from co-participation agreements in bid areas |

(156) |

− |

(237) |

(259) |

(284) |

| Early termination and cash outflows revision of lease agreements |

(115) |

(88) |

(54) |

(349) |

(415) |

| Losses with legal, administrative and arbitration proceedings, net |

188 |

287 |

125 |

996 |

797 |

| Decrease (Increase) in assets |

|

|

|

|

|

| Trade and other receivables |

200 |

163 |

(499) |

1,822 |

88 |

| Inventories |

59 |

1 |

432 |

(295) |

1,564 |

| Judicial deposits |

(185) |

(160) |

(623) |

229 |

(1,723) |

| Other assets |

(56) |

(38) |

155 |

(165) |

324 |

| Increase (Decrease) in liabilities |

|

|

|

|

|

| Trade payables |

352 |

392 |

63 |

986 |

(954) |

| Other taxes payable |

(667) |

(459) |

(10) |

(2,988) |

(431) |

| Pension and medical benefits |

(243) |

(276) |

(244) |

(1,001) |

(927) |

| Provisions for legal proceedings |

(171) |

(96) |

(225) |

(467) |

(591) |

| Other employee benefits |

(209) |

499 |

193 |

(80) |

356 |

| Provision for decommissioning costs |

(232) |

(282) |

(305) |

(977) |

(902) |

| Other liabilities |

(130) |

(250) |

(198) |

(737) |

(569) |

| Income taxes paid |

(1,465) |

(721) |

(2,368) |

(6,907) |

(10,032) |

| Net cash provided by operating activities |

8,204 |

11,307 |

11,669 |

37,984 |

43,212 |

| Cash flows from investing activities |

|

|

|

|

|

| Acquisition of PP&E and intangible assets |

(4,429) |

(4,443) |

(3,594) |

(14,644) |

(12,114) |

| Acquisition of equity interests |

(9) |

(7) |

(2) |

(22) |

(24) |

| Proceeds from disposal of assets - Divestment |

72 |

25 |

42 |

863 |

3,606 |

| Financial compensation from co-participation agreements |

− |

− |

− |

397 |

391 |

| Divestment (investment) in marketable securities |

1,070 |

(374) |

313 |

(109) |

98 |

| |

PETROBRAS | Performance Report | 4Q24 | 25 |

| Dividends received |

25 |

57 |

13 |

146 |

88 |

| Net cash (used in) provided by investing activities |

(3,271) |

(4,742) |

(3,228) |

(13,369) |

(7,955) |

| Cash flows from financing activities |

|

|

|

|

|

| Changes in non-controlling interest |

23 |

(232) |

103 |

(84) |

1 |

| Financing and loans, net: |

|

|

|

|

|

| Proceeds from finance debt |

576 |

986 |

910 |

2,129 |

2,210 |

| Repayment of principal - finance debt |

(2,309) |

(1,909) |

(1,711) |

(6,536) |

(4,193) |

| Repayment of interest - finance debt |

(389) |

(534) |

(406) |

(1,918) |

(1,978) |

| Repayment of lease liability |

(2,099) |

(1,913) |

(1,792) |

(7,895) |

(6,286) |

| Dividends paid to Shareholders of Petrobras |

(5,456) |

(2,293) |

(4,436) |

(18,327) |

(19,670) |

| Share repurchase program |

− |

− |

(538) |

(380) |

(735) |

| Dividends paid to non-controlling interests |

− |

− |

(1) |

(77) |

(49) |

| Net cash used in financing activities |

(9,654) |

(5,895) |

(7,871) |

(33,088) |

(30,700) |

| Effect of exchange rate changes on cash and cash equivalents |

(702) |

140 |

47 |

(983) |

174 |

| Net change in cash and cash equivalents |

(5,423) |

810 |

617 |

(9,456) |

4,731 |

| Cash and cash equivalents at the beginning of the period |

8,694 |

7,884 |

12,110 |

12,727 |

7,996 |

| Cash and cash equivalents at the end of the period |

3,271 |

8,694 |

12,727 |

3,271 |

12,727 |

| |

PETROBRAS | Performance Report | 4Q24 | 26 |

Exhibits

Table 14 – Net revenues by products

| |

|

|

|

|

|

Variation (%) |

| US$ million |

4Q24 |

3Q24 |

4Q23 |

2024 |

2023 |

4Q24 X 3Q24 |

4Q24 X 4Q23 |

2024 X 2023 |

| Diesel |

6,436 |

7,031 |

8,685 |

27,522 |

32,260 |

(8.5) |

(25.9) |

(14.7) |

| Gasoline |

3,274 |

3,140 |

3,428 |

12,692 |

14,309 |

4.3 |

(4.5) |

(11.3) |

| Liquefied petroleum gas (LPG) |

766 |

849 |

784 |

3,166 |

3,506 |

(9.8) |

(2.3) |

(9.7) |

| Jet fuel |

1,041 |

1,146 |

1,338 |

4,518 |

5,015 |

(9.2) |

(22.2) |

(9.9) |

| Naphtha |

479 |

480 |

480 |

1,869 |

1,837 |

(0.2) |

(0.2) |

1.7 |

| Fuel oil (including bunker fuel) |

190 |

209 |

324 |

976 |

1,158 |

(9.1) |

(41.4) |

(15.7) |

| Other oil products |

969 |

1,212 |

1,064 |

4,273 |

4,428 |

(20.0) |

(8.9) |

(3.5) |

| Subtotal oil products |

13,155 |

14,067 |

16,103 |

55,016 |

62,513 |

(6.5) |

(18.3) |

(12.0) |

| Natural gas |

1,097 |